Debt Alarm Ringing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAddicted to Debt

Lost Exorbitant Privilege

Trigger Points

Frankfurt, Cleveland, Golf, and Here and There

Is debt good or bad? The answer is “Yes.”

Debt is future spending pulled forward in time. It lets you buy something now for which you otherwise don’t have cash available yet. Whether it’s wise or not depends on what you buy. Debt to educate yourself so you can get a better job may be a good idea. Borrowing money to finance your vacation? Probably not.

Unfortunately, many people, businesses, and governments borrow because they can, which for many is possible only because central banks made it so cheap in the last decade. It was rational in that respect but is growing less so as the central banks tighten their policies.

Earlier this year, I wrote a series of articles (synopsis and links here) predicting a debt “train wreck” and eventual liquidation—an event I dubbed The Great Reset. I estimated we have another year or two before the crisis becomes evident.

That’s still my expectation… but I’m beginning to wonder again. Several recent events tell me the reckoning could be closer than I thought just a few months ago. Today, we’ll review those and end with a few suggestions on how to prepare.

Addicted to Debt

As noted, debt can be appropriate—even government debt, in some (rare) circumstances. I am glad FDR issued war bonds to help defeat the Nazis, for instance. Now, however, governments go into debt not because they face existential threats, but simply to keep their citizens and benefactors comfortable.

Similarly, central banks enable debt because they think it will generate economic growth. Sometimes it does, too. The problem is they create debt with little regard for how it will be used. That’s how we get artificial booms and subsequent busts.

We are told not to worry about absolute debt levels so long as the economy is growing in concert with them. That makes sense. A country with a larger GDP can carry more debt. But that is increasingly not what is happening. Let me give you two data points.

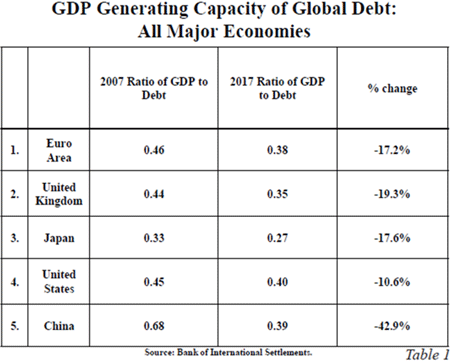

Lacy Hunt tracks Bank for International Settlements data that shows debt is losing its ability to stimulate growth. In 2017, one dollar of non-financial debt generated only 40 cents of GDP in the US and even less elsewhere. This is down from (if memory serves) more than four dollars of growth for each dollar of debt 50 years ago.

This has significantly worsened over the last decade. China’s debt productivity dropped 42.9% between 2007 and 2017. That was the worst among major economies, but others lost ground, too. All the developed world is pushing on the same string and hoping for results like we saw 40–50 years ago. As my friend Rob Arnott constantly reminds me, hope is not a strategy.

Source: Hoisington Investment Management

Now, if you are accustomed to using debt to stimulate growth, and debt loses its capacity to do so, what happens next? You guessed it: The brilliant powers-that-be add even more debt. This is classic addiction behavior. You have to keep raising the dose to get the same high.

At this point, Paul Krugman and others usually call me a debt curmudgeon and argue the debt doesn’t matter. I point them to Ken Rogoff and Carmen Reinhart’s book from 10 years ago, This Time Is Different, which demonstrates that in every prior debt run-up, over centuries of history, accumulated debt clearly eventually made a difference. There is always an eventual Day of Reckoning.

The US economy is so huge and powerful that our current $24.5 trillion government debt (including state and local) could quite easily grow to $40 trillion before we meet that day. We are one recession away from having a $30 trillion US government debt total. It will happen seemingly overnight. And deficits will stay well above $1 trillion per year every year after that, not unlike now.

Some argue the US has almost $150 trillion of personal and corporate assets to offset that debt. That is true enough, but I think there might be some slight resistance if the government demanded 15% of your total assets, including your house, real estate, investment assets, furniture and goods, to pay off the debt. That would be in addition to your regular taxes, and then they begin accumulating more debt.

Even though you are reading about a budget deficit of under $800 billion this year, the actual amount of debt added last year was well over $1 trillion. That is due to “off budget” items that Congress, in its wisdom, thinks shouldn’t be part of the normal budgetary process. It includes things like Social Security and Medicare—which vary from time to time and year to year—and can be anywhere from $200 billion to almost $500 billion.

And here’s the point that you need to understand. The US Treasury borrows those dollars and it goes on the total debt taxpayers owe. The true deficit that adds to the debt is actually much higher than the number you see in the news. It brings to mind the scene in the Wizard of Oz, when they wizard says, “Pay no attention to the man behind the screen.”

Household and corporate debt is growing fast, too, and not just in the US. Here’s a note from Lakshman Achuthan.

Notably, the combined debt of the US, Eurozone, Japan, and China has increased more than ten times as much as their combined GDP [growth] over the past year.

Yes, you read that right. In the last year, the world’s largest economies are generating debt 10X faster than economic growth. Adding debt at that pace, if it continues, will boost the debt-to-GDP ratio at an alarming rate.

Lakshman continues.

Remarkably, then, the global economy—slowing in sync despite soaring debt—finds itself in a situation reminiscent of the Red Queen Effect we referenced 15 years ago, when tax cuts boosted the US budget deficit much more than GDP. As the Red Queen says to Alice in Lewis Carroll's Through the Looking Glass, “Now, here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!”

I am trying to imagine a scenario in which this ends in something less than chaos and crisis. The best I can conceive is a decade-long (and possibly more) stagnation while the debt gets liquidated. But realistically, that won’t happen because debtors won’t let it, and they outnumber lenders. Hence, something like the Great Reset will happen first.

The rational course would be to delay the inevitable as long as possible. Yet in the US, at least, we’re hastening it.

Lost Exorbitant Privilege

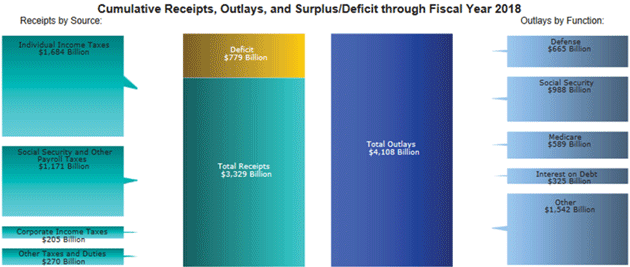

This month, the US Treasury closed the books on Fiscal Year 2018. It was a success in the sense that the government is still open and doing the things it should. Financially speaking, it was another debt-financed failure.

Source: US Treasury

The federal government spent approximately $4.1 trillion in FY 2018, of which it had to borrow $779 billion on budget and a few hundred billion more off-budget (amount TBD). And over 40% of the on-budget deficit went simply to pay $325 billion in interest on previously-issued debt.

Obviously, the government should spend less. But where to cut? There is no political agreement on that and little prospect of one. Nor, barring an economic boom of a magnitude and duration I think unlikely, are we going to grow out of this. So, I expect continued and even bigger deficits.

Deficits mean the Treasury has to borrow cash, which it does by selling Treasury bills, notes, and bonds. This wasn’t a problem for most of the last decade but is rapidly becoming one as the amounts grow larger.

Thanks to the “exorbitant privilege” I discussed earlier this month, the US has long had many foreigners willing to buy our debt. Now they are losing interest (forgive the pun) because hedging their currency exposure costs more. There are some complex reasons behind this, relating to swaps and the differentials between the US economy and others, but here’s the bottom line: European and Japanese investors can no longer buy US Treasury debt at a positive rate of return unless they want to take currency risk, which most do not. This is a new development.

This might be fine if US investors made up the difference, but that’s not happening, either, and might not be great anyway. Capital that goes into Treasury debt is capital that’s not going into bank loans, corporate bonds, mortgages, venture capital, stocks, or anything else in the private sector, which generates the growth we’ll need to pay off the government’s debt.

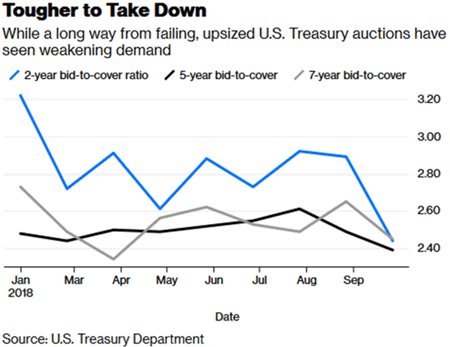

Treasury auction data shows it is getting harder to attract buyers. According to Bloomberg, last month’s two-year note auction matched the lowest bid-to-cover ratio for that maturity since December 2008.

Source: Bloomberg

The problem is manageable for now, and Treasury will always be able to borrow at some price… but the price could get awkwardly high, with interest costs rising dramatically.

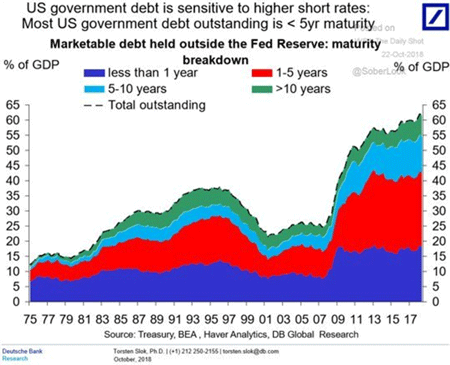

Given the debt’s maturity structure, it could be sooner than you might think. Treasury took advantage of lower short-term rates in recent years, which reduced interest costs, but also created refinancing risk. Here’s a Torsten Slok chart (via my friend Luke Gromen on Twitter).

Source: Luke Gromen

Looking only at federal debt not held by the Federal Reserve, Treasury will need to borrow something like 43% of GDP over the next five years just to rollover existing debt at much higher interest rates. That’s not counting any new debt we accumulate, which could be quite a lot if we enter recession or (God forbid) another war.

But set aside the hypothetical possibilities. Just the things we know are already locked in, like Social Security and Medicare, are enough to blow up the debt. Somebody has to buy all that Treasury paper. If it’s not foreigners, and not the Fed, and not American savers, we are out of prospects.

Now, buyers will appear at the right price, i.e. some higher interest rate. Barring recession-induced lower rates (which would be a different problem), government borrowing could get way more expensive.

Which is more likely: a double-digit ten-year Treasury yield or a worldwide debt liquidation? Neither will be fun. But I’ll bet that we see one or the other at some point in the 2020s.

Trigger Points

My renewed fear comes from the very real possibility the global economy breaks down in the next six months. Anything could trigger a crisis, and it could well be something no one presently foresees, but here are three candidates.

Corporate Credit Crisis: As a whole, US companies are significantly more leveraged now than they were ahead of the 2008 crisis. We saw then what happens when the commercial paper market seizes up, and that was without a Fed in tightening mode. Now we have a central bank both raising short-term rates and slowly ending its crisis-era accommodations. Recent comments from FOMC members say they have no intent of stopping, either. A few high-profile junk bond defaults could ignite fears quickly.

There are trillions of dollars of low-rated corporate debt that can easily slide into the junk debt category in a recession. Since most public pension, insurance, and endowment programs are not legally allowed to own junk-rated debt, I can see where it could easily cause a debt crisis along the lines of the previous subprime crisis.

Trade war: One reason the US economy seems to be booming right now is a surge in imports. Companies are rushing to build inventory ahead of the 25% tariff on Chinese goods that takes effect January 1. Coming on top of usual holiday season stockpiling, it is jamming ports, highways, and warehouses—generating many jobs in the process.

That’s all good right now, but those truck drivers and warehouse workers will no longer be necessary once the shelves are stocked. Working down that inventory will take months, at least, and the resulting slowdown could ease the economy into recession next year.

We might avert that outcome if the US and China reach some trade resolution, but that doesn’t appear likely. The latest reports say the Trump administration is digging in for a long siege and, if anything, may get even more aggressive against China. Nor does China seem likely to bend.

You may have heard the tennis term, “unforced errors.” Those are mistakes of your own, not a result of your opponent’s good shots. I think the tariffs may be an unforced error in US economic policy that could cause a serious growth decline, or worse.

European Slowdown: This week, we got October PMI reports from Markit. Its eurozone manufacturing and services index dropped to the lowest point since September 2016, with export-dependent Germany particularly weak. Meanwhile, Italy’s new budget is wildly out of line with its revenue and growth prospects. This threatens to set off another euro crisis. And then there’s the serious possibility of a hard Brexit in early 2019.

In short, Europe (at least some of it) is in real danger of entering recession next year. If that happens, the impact will spread around the globe as the continent reduces imports from the US, China, and elsewhere. Not to mention the potential fireworks if Italy or anyone else actually defaults on debt payments to foreign lenders, i.e. German, French, and other European banks with minimal loss reserves.

If the European Central Bank won’t buy Italian bonds, and the Italians won’t do it themselves, then Italian interest rates could jump dramatically, precipitating a crisis. This is essentially what forced the ECB into its first quantitative easing program. In theory, the Italians were then in compliance. That is not the case today. I have been pointing my finger at Italy for years. It is the linchpin in the whole euro experiment on debt and solidarity.

I could go on, but you get the point. The US economy looks fine just ahead, but problems lurk over the horizon. Bad things could happen soon.

So, what do you do? I have three suggestions.

- Build a cash reserve: I know every financial advisor says that, but disturbingly few people actually do it. Have several months of living expenses readily available in risk-free cash equivalents. Cash is also an option on buying discounted assets at lower prices in the future.

- Deleverage: If you carry business or personal debt, reduce it as much as you can and don’t assume you will be able to refinance. Banks can cut your credit lines in a heartbeat, and they will.

- Have a plan for your longer-term investments, whether they are stocks, real estate, or anything else. Decide now what you will sell, and to whom, because buyers may not be there when you need them. At the same time, decide what you plan to hold through any slowdown. I have assets in private companies and even a few public ones that I truly consider “for the long term.”

I sincerely hope I’m wrong. Maybe I’m jumping the gun here and 2019 will be another banner year. But I see major risks ahead, and I want you to be ready for them.

Frankfurt, Cleveland, Golf, and Here and There

I find myself today looking over a golf course in Puerto Rico. The weather is perfect, which is a far cry from what we left in Texas yesterday. Late next week, I catch a plane to Frankfurt where I will speak to a large group of institutional investors at the Lupus Alpha Investment Conference. I am really looking forward to this conference, as I will meet a few people I have always wanted to and hopefully learn more about what is going on in Germany and Europe. I have two brand-new presentations for them with the appropriate trigger warnings. While my host tells me that they don’t want me to pull any punches, I am not sure the audience is going to be happy with the message.

As if I needed more to do, I actually had myself fitted for golf clubs last Saturday. It was a 3½ hour process, and I was amazed at the technology available now. It’s been 20 years since someone stole my last golf clubs right out of my garage. I took it as a sign that God wanted me to quit. And while I’ve played a few times with rented clubs, I have resisted actually buying any.

I had a righteous 29 handicap back when I played regularly. I imagine my legitimate handicap for the next year will be close to 40, so none of you will really want to play with me. But then again, I’ve noticed that when I do play, I am looser for the next few days. I think, combined with my workout routine, this will keep me much healthier in the long run.

And with that, I will hit the send button. Have a great week and hit ‘em straight!

Your going to enjoy a few warm days analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All