Take Advantage of Volatility with Active Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

October was at it again this week. After Wednesday’s close, the S&P 500 Index, Dow Jones Industrial Average and small-cap Russell 2000 Index had all erased their gains for 2018, while the tech-heavy NASDAQ Composite dipped into correction territory.

I don’t believe there’s any single cause for the selloff. Investors are simply nervous, thanks to rising interest rates and the upcoming midterm elections, among other things.

Meanwhile, gold performed precisely as we would expect it to. The price of the yellow metal jumped above its 100-day moving average, a bullish sign that could mean further moves to the upside if market volatility persists. Today gold was trading at a three-month high of $1,246 an ounce.

So can we expect additional volatility going forward? In a recent note to investors, Citibank says it estimates that “some more volatility is likely through December” due to the impact of trade disputes on growth, rise in U.S.-Saudi Arabia tensions and Brexit stalemate. Analysts point out, though, that the present slowdown doesn’t necessarily signal the end of the historic bull market. Compared to the start of the previous two bear markets, in 2000 and 2007, only four out of 18 factors are flashing “sell” right now on Citi’s “bear market checklist.” Among those factors are overinflated global equity valuations, a flattening yield curve and high debt levels.

The bull is “tripping, not dying,” Citi says.

But Is It the End of “Buying the Dip”?

The bull market might not be dead, but we could be facing the end of “buying the dip.” According to a report this week by Morgan Stanley, buying the S&P 500 after a week of negative returns was a profitable strategy from 2005 through 2017. That may no longer be the case, as you can see in the chart below. Buying the dip in 2018 has resulted in an average loss of around 5 basis points.

So what’s changed? I think the most significant difference between now and the past decade or so is that, for the first time since the financial crisis, central banks are finally starting to withdraw liquidity. This means cheap money is no longer as plentiful as it once was, for investors and corporations alike.

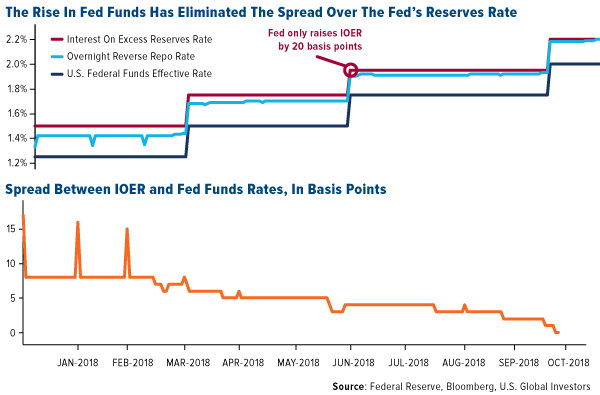

Some might disapprove of President Donald Trump publically criticizing Federal Reserve Chairman Jerome Powell for raising rates—Powell “almost looks like he’s happy raising interest rates,” Trump said—but he’s not wrong in expressing concern about the ramifications. I’ve shared with you before that a majority of recessions and bear markets in the past 100 years were preceded by monetary tightening cycles.

And there could be something else roiling markets right now.

Get Ready for $7.4 Trillion in Passive Index Selling

Last month I wrote about what I see as an imminent “passive index meltdown.” Over the past decade, billions of dollars have poured into ETFs and other passive investment products. This has led to a number of unexpected consequences, including price distortion and trading based not on fundamentals but on low fees. I said then that when these multibillion-dollar ETFs automatically rebalance, sometime at the end of this year or the beginning of next year, a correction of between 10 percent and 20 percent could be triggered.

Now, other people are starting to recognize the risk this poses. Speaking to CNBC this week, Goldman Sachs CEO David Solomon said that this month’s selloffs have been prompted by “programmatic trading.”

According to Solomon, “some of the selling is the result of programmatic selling because as volatility goes up, some of these algorithms force people to sell.”

Remember the 2010 Flash Crash? In the days following the May 6 incident, the Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) found that ETFs “suffered a disproportionate number of broken trades relative to other securities.” Of the securities that fell 60 percent or more that day, approximately 70 percent were ETFs.

But that was in 2010. Passive investing accounted for less than 30 percent of the assets under management (AUM) in actively managed funds. Today, that figure falls somewhere between 80 percent and 90 percent, representing some $7.4 trillion in “big selling pressure” concentrated in large- to small-cap equities, according to a report this week by J.P. Morgan.

“This is something worth noting at this late stage of a cycle given that passive investing seems to be trend following, with inflows pushing equities higher during bull markets, and outflows likely to magnify their fall during correction,” J.P. Morgan analysts Eduardo Lecubarri and Nishchay Dayal wrote.

The asset class with the greatest exposure to passive indexing, and therefore “momentum selling during market downturns,” is large-cap stocks, which have 10 times the passive AUM as small- and mid-cap stocks.

So how can investors prepare themselves?

Look at How Much Ultra-Short Treasuries Are Yielding Now

With riskier assets starting to look shaky, it might be time to ensure you have an adequate position in fixed income.

For the first time in over a decade, the three-month Treasury bill—the closest proxy we have for hard cash—is yielding more than the three main measures of U.S. inflation. That includes the headline consumer price index (CPI), which measures volatile food and energy prices. Bond yields and prices move inversely to interest rates, remember.

Ultra-short yields stood at 2.34 percent as of today, compared to a 2.27 percent change in consumer prices over the same period last year. This means that cash is finally yielding a positive real return for the first time in over 10 years, without inflation having to turn negative

What’s more, the three-month yield is well above the dividend yield for the much more volatile S&P 500 Index.

With interest rates on the rise, it’s important to stay on the short end of the yield curve. Retail investors seem to agree. Last month, rate-sensitive investors poured more than $4.7 billion into actively managed ultra-short bond funds, which have an average maturity of just six months, according to Morningstar data.

Passive instruments are attractive because of low fees, but it’s important not to discount actively managed funds just yet, and especially now as volatility is spiking. As Wells Fargo put it in the most recent Monthly Market Advisor,“late-cycle market characteristics could present many opportunities for investors who hold quality actively managed funds.”

Mining & Investment Latin America Summit

On a final note, I’m pleased to share with you that Texas Governor Greg Abbott yesterday retweeted my article, “6 Reasons Why Texas Trumps All Other U.S. Economies.” Governor Abbott has done a fabulous job keeping Texas on a pro-growth trajectory, making the Lone Star State the very best in the U.S. to do business in, I believe. If you didn’t get a chance to read the article, you can click the screengrab below.

Lastly, I’m incredibly honored to be the keynote speaker next week at the Mining & Investment Latin America Summit in Lima, Peru. My presentation will focus on how metals prices are being impacted by a combination of global growth and macro volatility. I’ll also be moderating a discussion on the political landscape in Latin American and its implications for the mining industry. I’ll be sure to share insights and observations from the conference in the coming days!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 2.97 percent. The S&P 500 Stock Index fell 4.10 percent, while the Nasdaq Composite fell 3.78 percent. The Russell 2000 small capitalization index lost 3.81 percent this week.

- The Hang Seng Composite lost 3.19 percent this week; while Taiwan was down 4.34 percent and the KOSPI fell 5.99 percent.

- The 10-year Treasury bond yield fell 11.3 basis points to 3.08 percent.

Domestic Equity Market

Strengths

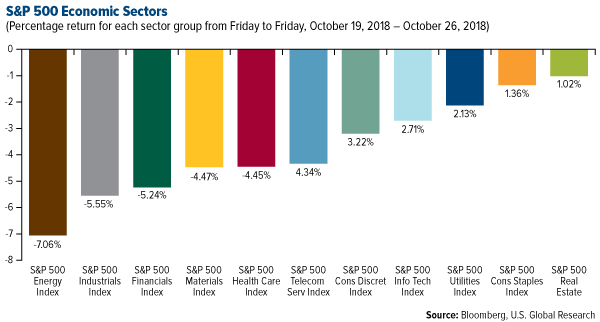

- Real estate was the best performing sector of the week, decreasing by 1.02 versus an overall decrease of 3.94 percent for the S&P 500.

- Cadence Design was the best performing stock for the week, increasing 13.49 percent.

- On Wednesday, Microsoft reported fiscal first-quarter results that topped expectations. The positive results came despite slowing revenue from its Azure cloud-computing service. Revenue from the service grew at a 76 percent annual rate, which is down from its 89 percent rate the prior quarter. Shares were up more than 4 percent ahead of Thursday's opening bell, reports Business Insider.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 7.06 percent versus an overall decrease of 3.94 percent for the S&P 500.

- EQT Corp was the worst performing stock for the week, falling 29.82 percent.

- The Dow Jones Industrial Average plunged more than 600 points on Wednesday, sending it into negative territory for the year.

Opportunities

- Twitter's share price surged this week after the company beat analyst expectations on revenue and profit for its third-quarter period. The company reported earnings of $0.21 a share on revenue of $758.1 million.

- Tesla reported a surprise profit with analysts describing the earnings as a “truly historic” quarter. The electric-car maker earned an adjusted $2.10 a share on revenue of $6.8 billion, topping the $0.15 loss and $6.3 billion that Wall Street analysts were expecting. Following the earnings release, shares rose as much as 10 percent in after-hours trading.

- Shares of Visa also gained this week after the credit card company reported quarterly results that beat estimates. The company said its fiscal fourth-quarter earnings rose to $1.23 per Class A share, from 90 cents per Class A share a year ago. Analysts surveyed by FactSet had forecast quarterly earnings for Visa of $1.20 a share.

Threats

- Trump's trade war with China is starting to get nasty for U.S. companies, writes Business Insider this week. Surveys from the Federal Reserve and market-research firms released Wednesday show American businesses growing increasingly concerned that goods coming into the U.S. from other countries were becoming more expensive. Concerns regarding retaliatory tariffs making it harder to sell to places such as Canada and China were also noted in the survey results.

- Advanced Micro Devices (AMD) missed on revenue and guidance this week. The chipmaker reported third-quarter revenue and fourth-quarter guidance that fell short of estimates, causing shares to slide 20 percent on Wednesday.

- Snap experienced a third-quarter drop in users on its Android app, and announced that is currency in the process of updating it. The company lost 2 million daily active users in the third quarter, sending its shares down to a new low.

The Economy and Bond Market

Strengths

- The U.S. economy grew at a faster rate than expected in the third quarter, according to the Commerce Department's advance report released Friday. Gross domestic product (GDP) increased at an annualized rate of 3.5 percent while economists had forecast 3.3 percent growth, according to estimates compiled by Bloomberg. With that result, the U.S. economy had its strongest back-to-back quarters of growth in four years.

- The flash reading of IHS Markit’s manufacturing purchasing manager’s index (PMI) rose to a five-month high of 55.9 in October from 55.6, while the flash services PMI rose to a two-month high of 54.7 from 53.5 in September. The U.S. economy stepped up a notch in October after hurricane disruption last month. Improving domestic economic conditions were the main factor behind rising client demand, IHS Markit said.

- The four-week moving average of initial claims, considered a better measure of labor market trends as it irons out week-to-week volatility, was unchanged at 211,750 last week. The labor market is viewed as being near or at full employment, with the unemployment rate close to a 49-year low of 3.7 percent.

Weaknesses

- New-home sales dropped sharply in September. Sales in the U.S. fell 5.5 percent, marking the fourth straight monthly decline according to data released Wednesday by the Commerce Department.

- New orders for key U.S.-made capital goods fell for a second straight month in September and shipments were unchanged, suggesting that growth in business spending on equipment moderated further in the third quarter. The Commerce Department said on Thursday that orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, dipped 0.1 percent last month amid weakening demand for fabricated metals and electrical equipment, appliances and components.

- Consumer sentiment for October was weaker than anticipated in the latest survey result, although the index remained near historically high levels. The University of Michigan’s monthly survey of consumers hit 98.6 in the final reading of October, below the 99 expected by economists.

Opportunities

- The personal income and spending numbers will start the week on Monday. Personal income growth is expected to have increased slightly from 0.3 percent to 0.4 percent month-over-month in September, while personal consumption is forecast to have expanded by 0.3 percent, unchanged from the prior month.

- Investors will have all eyes on the October jobs report on Friday. Nonfarm payrolls are projected to have risen by 190,000 in October, improving on September’s 134,000, which was negatively impacted by Hurricane Florence.

- The jobless rate is anticipated to remain at 3.7 percent in October, but average hourly earnings growth are likely to have accelerated to above 3 percent, rising to a more than 9-year high of 3.1 percent year-over-year according to consensus forecasts.

Threats

- Goldman Sachs says the stock market will become a drag on the U.S. economy in 2019. "Looking ahead, our baseline expectation is a decline in the equity impulse to real GDP growth to about -0.25pp in the first half of next year," Jan Hatzius, the chief economist at Goldman, said in a recent note to clients.

- On Tuesday, the Conference Board will publish its consumer confidence gauge for October, with the index expected to ease from 18-year highs. Other U.S. surveys to keep an eye on next week are the Chicago PMI on Wednesday and the ISM manufacturing PMI on Thursday.

- Thursday will see the releases of the preliminary prints on third quarter labor costs and productivity. Higher productivity growth is seen as key in boosting wages, though this doesn’t appear to have taken place yet as productivity growth is forecast to slow from 2.9 percent to 2.0 percent during the third quarter.

Gold Market

This week spot gold closed at $233.13, up $6.23 per ounce, or 0.51 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 5.08 percent. The S&P/TSX Venture Index fared worse, off 5.66 percent. The U.S. Trade-Weighted Dollar rose 0.73 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-24 | New Home Sales | 625k | 553k | 585k |

| Oct-25 | Hong Kong Export YoY | 8.6% | 4.5% | 13.1% |

| Oct-25 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Oct-25 | Durable Goods Orders | -1.5% | 0.8% | 4.6% |

| Oct-25 | Initial Jobless Claims | 215k | 215k | 210k |

| Oct-26 | GDP Annualized QoQ | 3.3% | 3.5% | 4.2% |

| Oct-30 | Germany CPI YoY | 2.4% | -- | 2.3% |

| Oct-30 | Conf. Board Consumer Confidence | 135.4 | -- | 138.4 |

| Oct-31 | Eurozone CPI Core YoY | 1.0% | -- | 0.9% |

| Oct-31 | ADP Employment Change | 190k | -- | 230k |

| Oct-31 | Caixin China PMI Mfg | 50.0 | -- | 50.0 |

| Nov-1 | Initial Jobless Claims | 213k | -- | 215k |

| Nov-1 | ISM Manufacturing | 59.0 | -- | 59.8 |

| Nov-2 | Change in Nonfarm Payrolls | 190k | -- | 134k |

| Nov-2 | Durable Goods Orders | -- | -- | 0.8% |

Strengths

- The best performing metal this week was palladium, up 2.16 percent as hedge funds boost their net long position to a 7-month high on supply concerns. Traders and analysts in the weekly Bloomberg survey were the most bullish in a month as gold heads for its highest price since mid-July. The yellow metal was up for a fourth straight week, the longest run of gains since January, as sentiment is increasingly bullish and investors are adding to their holdings, according to Bloomberg data.

- Exchange-traded funds (ETFs) backed by gold hit a two month high this week. Gold futures gained on Thursday despite the equity selloff slowing and the U.S. dollar firming. Holdings of gold-backed ETFs rose to 2,118 tons as of Wednesday, the highest level since the end of August.

- Japan’s largest bullion retailer, Tanaka Kikinzoku K.K., reported that sales of gold bars rose 52 percent year-over-year in the first three quarters of 2018. This demand was fueled by falling gold prices, writes Masumi Suga of Bloomberg. Nine month sales of gold bars totaled 640,089 troy ounces while platinum bar sales for the same time period totaled 6,792 kilograms, a 17 percent increase year-over-year.

Weaknesses

- The worst performing metal this week was platinum, up just 0.22 percent as shorts added to their bearish position. Reports came out this week that Venezuelan President Nicolas Maduro has been illegally exporting his country’s gold to Turkey in an effort to rescue the collapsing economy, according to a top U.S. official. Mining minister Victor Cano said that Venezuela was no longer sending its gold to Switzerland, but rather to allied country Turkey, where there isn’t risk of the gold being seized under international sanctions. Meanwhile, Turkey continues to be a bullion seller, with total gold reserves falling over 6 percent for the year and down 11.3 tons from August to September.

- China’s purchases of gold from Hong Kong fell to the lowest in more than seven years due to possible shifts in trade routes by suppliers. Capital Economics economist Ross Strachan remains positive, saying that “we don’t believe that jewelry demand has been weak enough to explain this sustained shift and instead it seems likely that it reflects businesses changing supply routes.”

- Goldcorp Inc.’s stock fell almost 19 percent on Thursday after reporting a $101 million loss for the third quarter, compared to $111 million profit in the previous year. Peter Jacobs, an analyst with Stifel RMG Group, said that “it’s almost as if it’s business as usual, just another failed gold mining stock.” Goldcorp CEO David Garofalo said that there are an unhealthily large number of gold miners competing for the same capital.

Opportunities

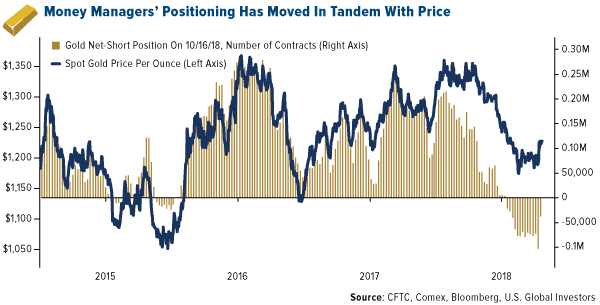

- Bloomberg data shows that money managers left gold shorts at a record pace, just a week after bets against the yellow metal hit an unprecedented high. Based on data going back to 2006, we saw the biggest short followed by the biggest buy this week. Bloomberg’s Eddie van der Walt writes that if the short position keeps unwinding, then an upward pressure in gold prices should follow. When money managers moved to a net long position in 2015, prices rose shortly after by 30 percent.

- Central banks are on a gold buying spree and 2018 could be the first time in five years that central banks increase their purchases of the yellow metal. Net purchases are forecast to rise to 450 metric tons this year, up from 375 tons in 2017, according to consultancy Metals Focus Ltd. Junlu Liang, a senior analyst at Metals Focus, said that “official sector purchases are likely to remain healthy, as a result of ongoing efforts to diversify reserves among emerging market countries.”

- Morgan Stanley released a report this week saying that inflation is here and “this time it’s for real.” They cite two reasons for expecting inflation to rise: wage growth improvement globally and a changing macro backdrop. Economists write that 2012 to 2016 was characterized by deleveraging but, since 2017, the global economy has moved beyond that and a clear sign of change is the pickup in global capex growth. The United States’ gross domestic product (GDP) growth for the third quarter came in above expectations at 3.5 percent, while consumer spending also unexpectedly accelerated to a 4 percent increase, the best since 2014. Perhaps consumers are pushing buy decisions forward in expectations of higher prices in the future.

Threats

- Ned Davis Research has urged investors to reduce their holdings in U.S. stocks for the second time this month, citing a worsening global bear market. Chief global investment strategist Tim Hayes said this week that “we’re in the midst of a global bear market with increased downside participation from the overvalued U.S. market and technology sector that helped the U.S. outperform” and that “conditions are likely to get far worse before they get better.” Bloomberg’s Lu Wang writes that there is a growing consensus that the U.S. is not immune to the market turmoil that has swept through Europe and Asia this year. JPMorgan issued a warning that the $7.4 trillion in passively managed assets around the world are at risk of momentum selling during market downturns and are heavily concentrated in large-cap and U.S. small- and mid-cap stocks.

- In an interview on CNBC this week, John LaForge of the Wells Fargo Investment Institute said that he believes the gold rally will fade and prices will drop in the next few weeks. LaForge estimates that gold’s bearish period will last another three to five years with choppy trading dominating the environment and prices falling in the $1,050 to $1,350 per ounce range.

- SPO Partners & Co., a $5 billion firm that has managed money for almost 50 years, is closing. Eli Weinberg, co-managing partner, said that “today, we are finding it exceedingly difficult to deploy capital with an acceptable margin of safety.” A top Federal Reserve official issued a rare public warning this week saying that banks appear to be going after increasingly risky deals and forgoing protections against borrowers going bust, writes Bloomberg. Todd Vermilyea, head of risk surveillance and data, told bankers at a conference in New York that “some institutions could be taking on risk without the appropriate mitigating controls.”

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 26 was Happycoin, up 364.40 percent.

- “Banks have an enormous opportunity to restore trust by leveraging the technology underpinning cryptocurrencies,” reads an article in MarketWatch this week. That opportunity is blockchain technology – a digital leger in which transactions are recorded in order and publicly, making the data nearly impossible to manipulate. According to the article, if Wall Street wants to regain the trust of Americans, leveraging this technology is the first step to help them do so. This is a promising look at what is missing from our modern banking system.

- Coinbase customers outside of New York can now buy and sell a U.S.-dollar-backed stablecoin, USDC, according to CoinDesk. This fully collateralized token claims to be “easier to program with, to send quickly, to use in dapps, and to store locally than traditional bank account-based dollars,” making it “an important step towards a more open financial system.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended October 26 was Smart Application Chain, down 38.59 percent.

- Harish BV, co-founder of Unocoin, was arrested for allegedly setting up an unregistered bitcoin ATM in Bangalore, according to The Times of India. The Central Crime Branch (CCB) told press that the ATM in question didn’t have “permission from the state government and is dealing in cryptocurrency outside the remit of the law.” Unocoin’s other co-founder, Sathvik Viswanath, was adamant that while cryptos are “not legal tender in India,” they are not illegal, meaning “you bear the risk of your investment and there is no regulation in the industry.”

- Smaller cryptocurrencies are at risk of a “51% attack,” wherein “a miner takes over more than half of a cryptocurrency's mining power, which then allows them to erase a past transaction and replace it with another transaction” according to CoinDesk. College freshman and cryptocurrency enthusiast “geocold51” livestreamed an attempted 51% attack on Bitcoin Private, which held a $47 million market cap at the time, to demonstrate this flaw in the system publicly. He estimates it would cost a malicious hacker only $200 to make a profit this way.

Opportunities

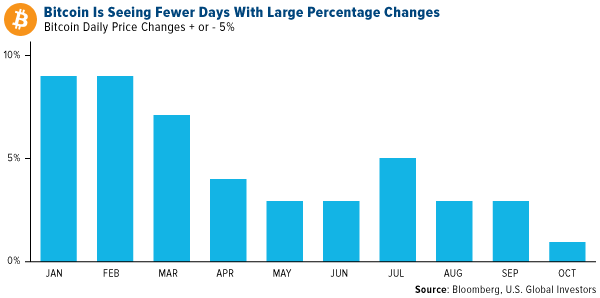

- Bitcoin is going through a “serious quiet spell,” writes Bloomberg. The cryptocurrency is seeing fewer major price swings, with only a single day of movement of 5 percent or more so far in October, the article continues, compared to nine in January and February. According to Bloomberg Intelligence analyst Mike McGlone, low volatility is “a sign of speculation leaving the market and eventually a bottoming process.”

- The Capital Markets and Technology Association (CMTA) published new anti-money-laundering (AML) standards in the hopes of encouraging further adoption of distributed ledger technology (DLT) and digital assets within the financial markets. The Switzerland-based non-profit stated their standards “clarify […] measures to be taken in order to comply with the Swiss regulations against money laundering and the financing of terrorism.” Although the standards do not have any formal standing yet, CMTA was clear these “represent a consensus” between experts on what should be considered best practices in this growing, digital space.”

- Mallow, a program for cross-chain transactions between bitcoin and Ethereum, launched this week, making it the first federated blockchain built using the Open Federated Gateway Protocol (OFGP). Developed by iBitcome and DEx.top, OFGP allows for trades between separate cryptocurrencies via a token called WBCH. As OFGP is an open-source protocol, competitors to Mallow could appear soon to create competition for the program and choices for crypto-users.

Threats

- During its pre- IPO funding round, Bitmain Technologies solicited investors with pitch desks that falsely suggested the company had received funding from Digital Sky Technologies Global and GIC Private Limited, according to a CoinDesk investigation. Whether or not legal action will be taken remains to be seen.

- Following a ten-month investigation, an Australian woman was arrested this week for stealing 100,000 XRP, reports ZDNet. The victim’s email was hacked in January, allowing the unnamed woman to access their digital wallet. “An email account is more valuable than people realise,” said Arthur Katsogiannis, Cybercrime Squad Commander at New South Wales Police Force. “Scammers are increasingly targeting emails as they link the individual to financial accounts and other personal information.” Ripple was trading around $3.50 at the time of the theft, but has since dropped to only $0.45 at the time of writing.

- Plans to launch Royal Mint Gold (RMG) tokens have been put on hold after the U.K. Royal Mint and the CME Group’s partnership fell through, reports Reuters. Initially, RMG was meant to be issued in fall of 2017, making this the second time plans have been postponed. “Sadly, due to market conditions this [launch] did not prove possible at this time,” says a Royal Mint spokesperson, “but we will revisit this if and when market conditions are right.”

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week rising 4.48 percent. The commodity rallied after Vale’s CEO said Chinese demand for iron ore is stronger than expected.

- The best performing sector this week was the Bloomberg Global Coal Producers Index. The index rose 57 basis points after reports came out of Chinese steel mills stockpiling steelmaking inputs ahead of the winter season.

- The best performing stock for the week was International Paper Co. The Tennessee packaging producer rose 6.98 percent after the company reported earnings ahead of Wall Street consensus and CEO Mark Sutton stated that he sees “continued healthy demand for our products.”

Weaknesses

- Lumber was the worst performing commodity this week. The commodity dropped 5.5 percent after The Commerce Department reported that new home sales dropped 5.5 percent last month and reached their lowest level in nearly two years.

- The worst performing sector this week was the TSX Diversified Metal and Mining Index. The index dropped 17.12 percent after its largest weighting plunged to the lowest in more than a year. Canada’s largest diversified miner, Teck Resources, reported third-quarter results that trailed analysts’ estimates amid rising costs in its coal business.

- The worst performing stock for the week was Goldcorp Inc. The major Canadian gold producer dropped 19.06 percent after operating results were hurt by lower output of all metals from the company’s Peñasquito mine, while costs climbed.

Opportunities

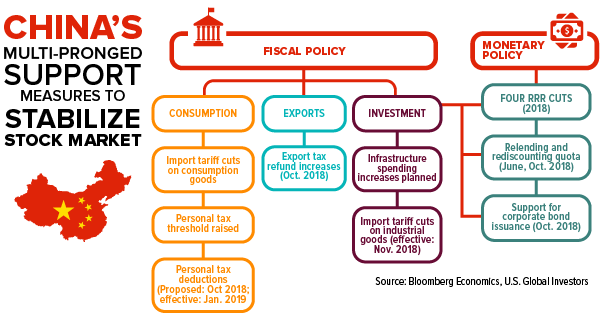

- China intensified efforts to stabilize its equity market. President Xi Jinping vowed “unwavering” support for non-state firms over the past weekend, stock exchanges committed to help manage share-pledge risks and the government released a plan to cut income taxes. That tax reduction is a big positive for growth and may spur consumption, according to Bloomberg Intelligence.

- China is banking on its dominance of global supply chains to help it ride out the pain from Donald Trump’s trade war. Exports to the U.S account for less than a fifth of China’s total exports. Deutsche Bank AG estimates that overall, China’s industrial output has only a five percent exposure to the U.S. market.

- Explorers expanded drilling in U.S. oilfields for a third straight week. “This visibility gives us confidence that super-spec drilling activity will continue to grow,” Andy Hendricks CEO of Patterson Energy said during a Thursday conference call. Crude producers in the U.S. are pumping a near-record 10.9 million barrels a day, according to the Energy Information Administration.

Threats

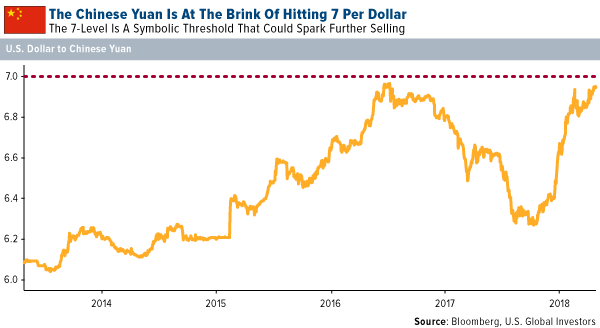

- The Chinese yuan hit 6.9725 per U.S. dollar in offshore trading on Friday, the weakest in nearly two years. The currency has fallen against the greenback each day this week, and on Thursday it sank past a prior low from August. After a nearly 7 percent selloff so far this year, the yuan is at the brink of hitting 7 per dollar—a symbolic threshold that could spark further selling—if Chinese businesses and individuals decide this means they need to expatriate capital ahead of any further decline, according to the Wall Street Journal.

- OPEC should boost crude production at the next meeting, the IEA says. Without an increase in output from OPEC, IEA Executive Director Fatih Birol reiterated his warning the global economy will enter “a red zone” because momentum is already slowing amid trade disputes. The world still needs more oil to compensate for losses from Iran and Venezuela, he said.

- Imports via Hong Kong to China, the world's top consumer of the metal, decreased to 11.059 tonnes in September from 31.857 tonnes in August, according to data from the Hong Kong Census and Statistics Department. That is the lowest since May 2011, when imports were at 4.37 tonnes.

China Region

Strengths

- The Shanghai Composite Index actually rose 1.91 percent for the week, a notable standout in a generally down week for the region.

- Properties and construction was the top-performing sector in the Hang Seng Composite Index for the week, closing down only 1.18 percent amid a week that saw all sectors in the red.

- The Philippine peso strengthened this week, and BSP Governor Nestor Espenilla reiterated the potential for further central bank action in the near future if necessary.

Weaknesses

- Vietnam took a shellacking this week, tumbling 6 percent over the last five trading days. South Korea kept it company, falling 5.99 percent.

- Information technology fell 6.76 percent for the week, the worst-performing sector in Hong Kong’s Hang Seng Composite Index. Hong Kong’s export orders came in at only a 4.5 percent growth rate versus analysts’ anticipated 8.6 percent.

- South Korea’s preliminary third quarter gross domestic product (GDP) reading clocked in at only a 2 percent year-over-year growth rate, shy of the 2.3 percent reading expected by analysts.

Opportunities

- Following our short discussion on long-term investors’ possible consideration of valuations in markets like Hong Kong’s, Barron’s ran an interesting story over the weekend noting that, in the opinions of some, emerging market (EM) tech juggernauts such as Tencent and Alibaba may now be in the running for relative bargains. More food for thought.

- Chinese authorities continue to offer multi-pronged support for the economy in the form of both fiscal and monetary policies and in a manner that will likely serve to help soften the dual blows of continued deleveraging and an ongoing trade dispute with the United States of America.

- China and Japan demonstrated increased alignment on “free and fair trade” as Xi Jinping and Shinzo Abe met in Beijing on Friday. The two leaders signed several new agreements between the two countries, and the countries’ central banks signed a currency swap agreement.

Threats

- Trade wars continue to remain firmly in the foreground of regional investors’ landscapes, with the latest media reports suggesting that while President Donald Trump and Chinese President Xi Jinping are still on schedule to meet at next month’s G20 gathering in Argentina, the U.S. is considering nixing the top of trade from the agenda entirely until China demonstrates concrete progress toward making concessions.

- In yet another recent initial public offering (IPO) delay, the U.S.-based STX Entertainment allowed its application for listing in Hong Kong to lapse. The company blamed the rocky market conditions. Similarly, Singaporean entrepreneur Ron Sim has “‘aborted’ plans to list [his] V3 Group Ltd. in Hong Kong amid intense volatility and weakness in the global stock market,” Bloomberg News reported this week.

- The U.S. dollar is again flirting with new 52-week highs which could continue to place pressure on EM currencies.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 1.35 percent. The market remains volatile after the country’s bailout program ended over the summer. Banks gained the most in the past five days, with Alpha Bank up 15 percent, followed by Piraeus Bank up 12.5 percent.

- The Turkish lira was the best performing currency this week, gaining 1.05 percent against the U.S. dollar. The currency continues to recover after the American pastor held in Turkey was released a few weeks ago, which investors believe will lead to a warmer relationship with the U.S. The nation’s central bank left its main rate unchanged at 24 percent, in-line with Bloomberg expectations.

- Consumer staples was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 6.13 percent. Consumer confidence was reported at 57.3, the lowest level in nearly a decade, as inflation rocketed to a 15-year high a month earlier. Households' financial expectations and unemployment situation for the next 12 months also weakened sharply.

- The Hungarian forint was the worst performing currency this week, losing 1.23 percent against the U.S. dollar. Despite rising inflation last week, Hungary’s central bank left its main rate unchanged at 90 basis points, keeping its dovish stance even as other central banks in central Europe started raising interest rates. Inflation picked up to 3.6 percent in September, up from 3.4 percent in August, the highest rate since January 2013, but still within the bank’s 2 to 4 percent target range.

- Information technology was the worst performing sector among eastern European markets this week.

Opportunities

- Dutch bank ABN Amro sees the Polish zloty, Czech koruna and Hungarian forint appreciating through end of 2019, as economic growth remains relatively strong, according to strategist Georgette Boele and economist Nora Neuteboom. They also comment that the Central Emerging Europe (CEE) economies would remain resilient in the event of an escalation in the U.S.-China trade war.

- The Kepler Cheuvreux research team believes that the volatile October we are experiencing will be followed by a year-end rally through November and December. They removed a sizable underweight in Europe’s unloved bank sector and reduced the scale of their super overweight positions in defensive, healthcare and consumer staples stocks.

- Political tension between the U.S. and Russia is growing. President Donald Trump threatened to withdraw from the 1987 Intermediate-Range Nuclear Forces Treaty, after accusing Russia of violations of the agreement. However, President Trump and Russian President Vladimir Putin will meet again next month in France, which might present an opportunity for a dialogue.

Threats

- Poland’s current ruling party, the Law and Justice Party, won again in the regional elections last Sunday. However, the win was by a narrower margin than the polls predicted, winning less than a third of the votes and falling short of its 2015 general election result nationwide. The party’s confrontation with the E.U. over judicial reform has hurt its image with voters. According to the latest Eurobarometer survey, 46 percent of Poles trust the E.U. while 41 percent do not. At the same time, only 28 percent trust the national government while 65 percent do not.

- The European Commission, which is the European Union’s executive arm, rejected Italy’s budget and asked for it to be revised, marking the first time such a demand has been made of a member state. Italy’s budget deficit was set at 2.4 percent of gross domestic product, while having the highest debt ratio in the euro area after Greece. Moody’s cut Italy’s credit rating one notch lower to Baa3, the lowest investment grade, and gave it a stable outlook. S&P Global Ratings is set to review the country on Friday.

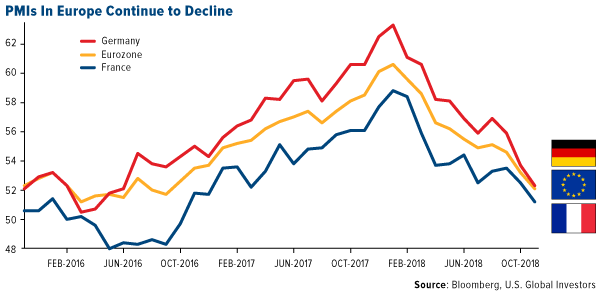

- Preliminary October PMI data for the euro area was released this week, and as predicted, manufacturing continues to decline in the region. Germany’s PMI slid to 52.3, down from 53.7, while France declined to below 52. The eurozone manufacturing index tumbled to 52.1, down from a reading of 53.2 in September.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All