Fox Business recently discussed a new study showing that more Americans doubted they would be able to save enough for retirement than those confident of reaching their goals. There were some interesting stats from the study:

- 37% are NOT confident they can save enough to retire

- 32% ARE confident they can save enough.

- 48%, however, don’t think their retirement savings will reach $1 million.

Northwestern Mutual also did a study that showed equally depressing statistics.

“Americans feel under-prepared for the financial realities of retirement, according to new data from Northwestern Mutual. Nearly eight in 10 (78%) Americans are “extremely” or “somewhat” concerned about affording a comfortable retirement while two-thirds believe there is some likelihood of outliving retirement savings.”

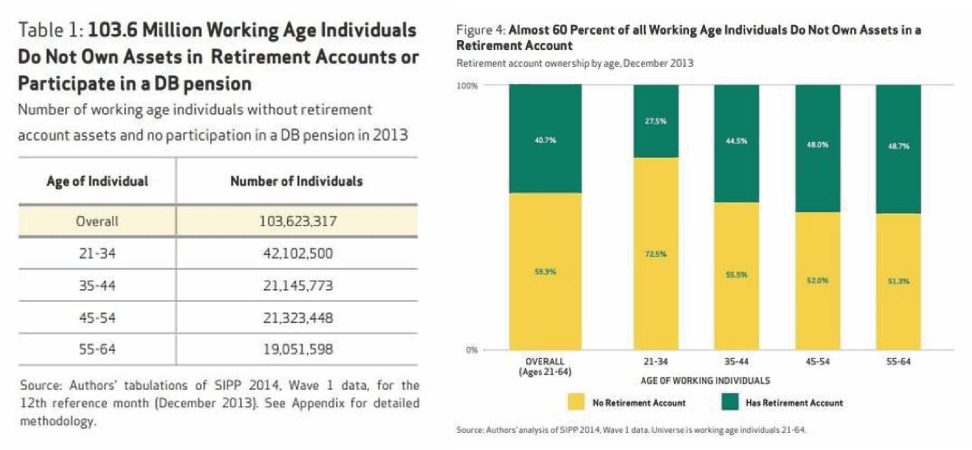

Those fears are substantiated even further by a new report from the non-profit National Institute on Retirement Security which found that nearly 60% of all working-age Americans do not own assets in a retirement account.

Here are some additional findings from the report:

- Account ownership rates are closely correlated with income and wealth. More than 100 million working-age individuals (57 percent) do not own any retirement account assets, whether in an employer-sponsored 401(k)-type plan or an IRA nor are they covered by defined benefit (DB) pensions.

- The typical working-age American has no retirement savings. When all working individuals are included—not just individuals with retirement accounts—the median retirement account balance is $0 among all working individuals. Even among workers who have accumulated savings in retirement accounts, the typical worker had a modest account balance of $40,000.

- Three-fourths (77 percent) of Americans fall short of conservative retirement savings targets for their age and income based on working until age 67 even after counting an individual’s entire net worth—a generous measure of retirement savings.

So, what’s the problem?

Why do so many Americans face a retirement crisis today after a decade of surging stock market returns?

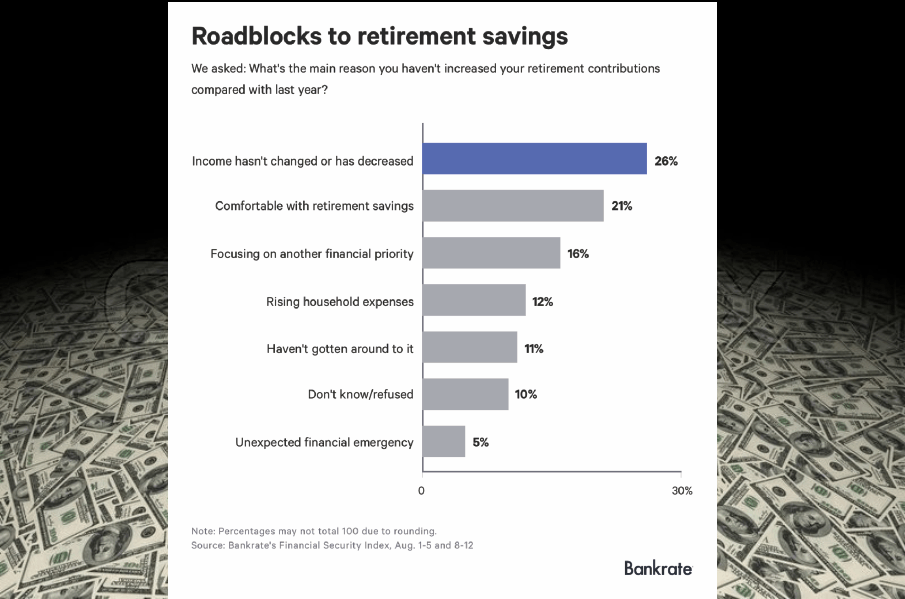

A survey from Bankrate.com touched on the issue.

“13 percent of Americans are saving less for retirement than they were last year and offers insight into why much of the population is lagging behind. The most popular response survey participants gave for why they didn’t put more away in the past year was a drop, or no change, in income.”

Just Getting By

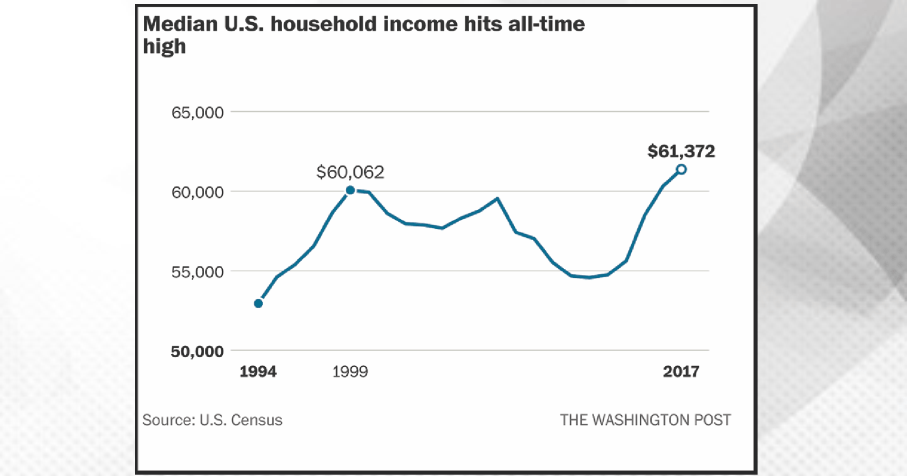

Just last Wednesday, the Census Bureau released its latest report on “Income and Poverty In The United States”which showed that median incomes just hit a record high.

“For the third consecutive year, households in the United States experienced an increase in real annual median income. Median household income was $61,372 in 2017, a 1.8 percent increase from the 2016 median of $60,309 in real terms. Since 2014, median household income has increased 10.4 percent in real terms.”

So, if median incomes just hit an all-time high, then why are Americans having such a problem saving for retirement?

Simple.

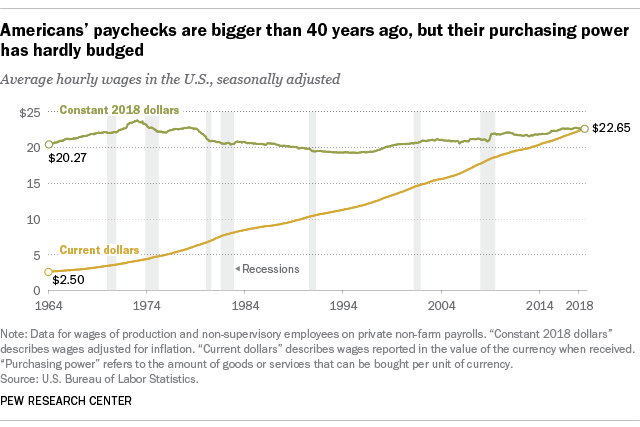

The cost of living has risen much more dramatically than incomes. According to Pew Research:

“In fact, despite some ups and downs over the past several decades, today’s real average wage (that is, the wage after accounting for inflation) has about the same purchasing power it did 40 years ago. And what wage gains there have been have mostly flowed to the highest-paid tier of workers.”

But the problem isn’t just the cost of living due to inflation, but the “real” cost of raising a family in the U.S. has grown incredibly more expensive with surging food, energy, health, and housing costs.

Researchers at Purdue University recently studied data culled from across the globe and found that in the U.S., $65,000 was found to be the optimal income for “feeling” happy. In other words, this was a level where bills were met and there was enough “excess” income to enjoy life. (However, that $65,000 was based on a single individual. For a “family of four” in the U.S., that number was $132,000 annually.)

Gallup also surveyed to find out what the “average” family required to support a family of four in the U.S. (Forget about being happy, we are talking about “just getting by.”) That number turned out to be $58.000.

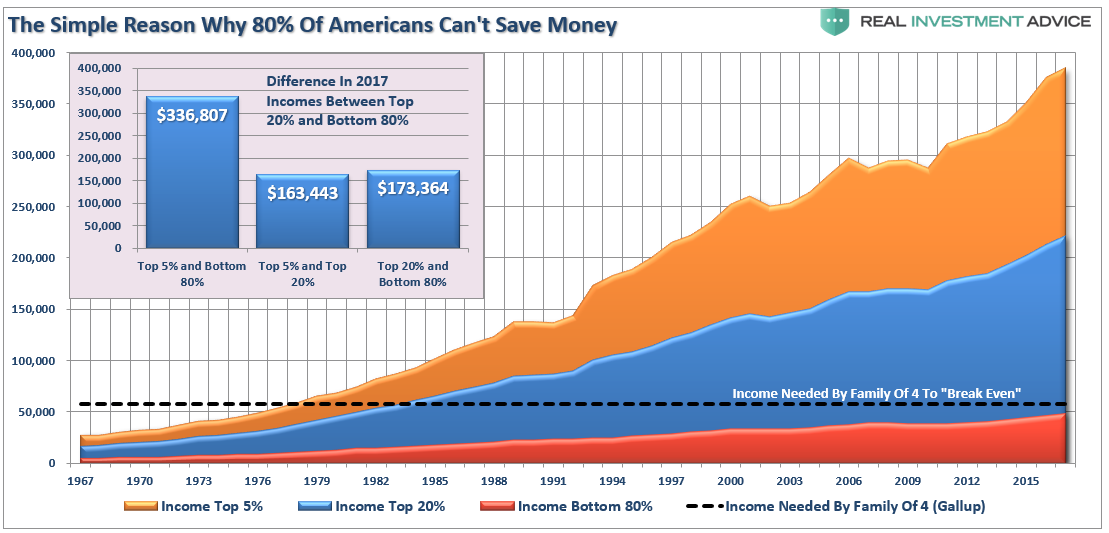

Skewed By The 1%

The issue with the Census Bureau’s analysis is that the income numbers are heavily skewed by those in the top 20% of income earners. For the bottom 80%, they are well short of the incomes needed to obtain “happiness.”

The chart below shows the “disposable income” of Americans from the Census Bureau data. (Disposable income is income after taxes.)

So, while the “median” income has broken out to all-time highs, the reality is that for the vast majority of Americans there has been little improvement. Here are some stats from the survey data which was NOT reported:

- $306,139 – the difference between the annual income for the Top 5% versus the Bottom 80%.

- $148,504 – the difference between the annual income for the Top 5% and the Top 20%.

- $157,635 – the difference between the annual income for the Top 20% and the Bottom 80%.

So, if you are in the Top 20% of income earners, congratulations. If not, it is a bit of a different story.

No Money, But I Got Credit

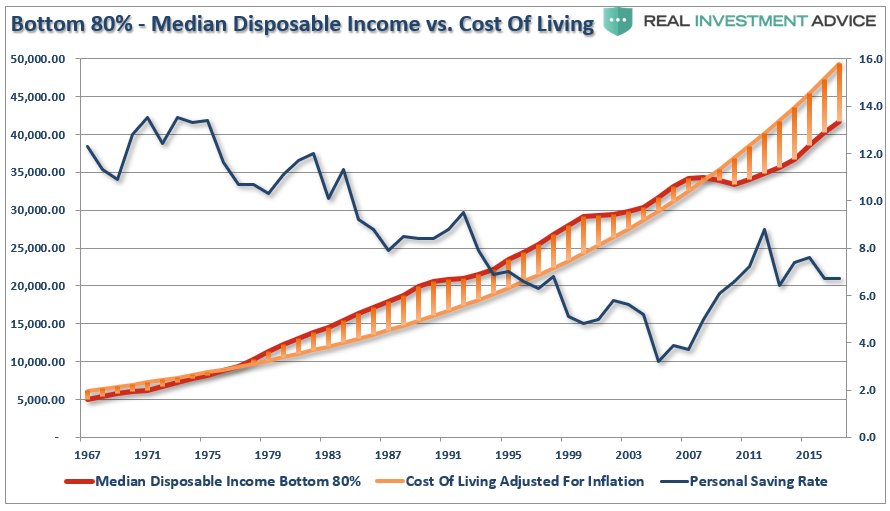

As noted above, sluggish wage growth has failed to keep up with the cost of living which has forced an entire generation into debt just to make ends meet.

While savings spiked during the financial crisis, the rising cost of living for the bottom 80% has outpaced the median level of “disposable income” for that same group. As a consequence, the inability to “save” has continued.

So, if we assume a “family of four” needs an income of $58,000 a year to be “make it,” such becomes problematic for the bottom 80% of the population whose wage growth falls far short of what is required to support the standard of living, much less to obtain “happiness.”

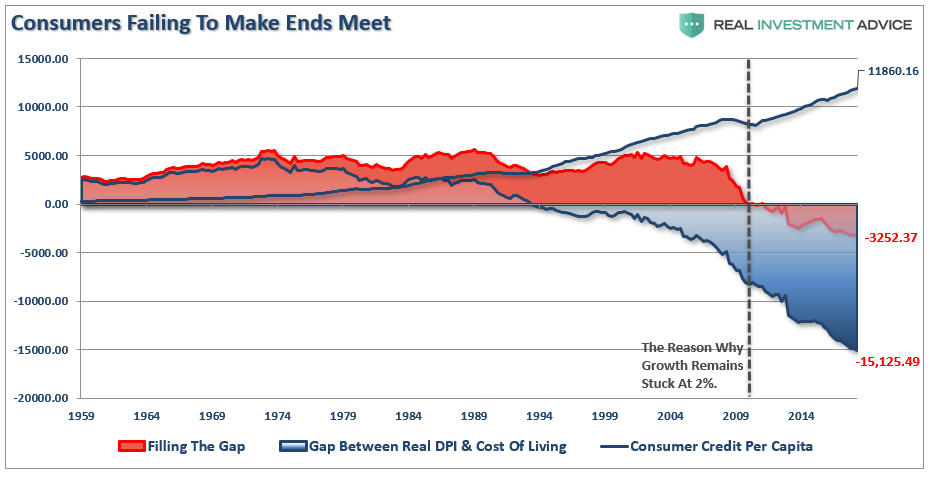

The “gap” between the “standard of living” and real disposable incomes is more clearly shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living so consumers turned to debt to fill the “gap.” However, following the “financial crisis,” even the combined levels of income and debt no longer fill the gap. Currently, there is almost a $3300 annual deficit that cannot be filled.

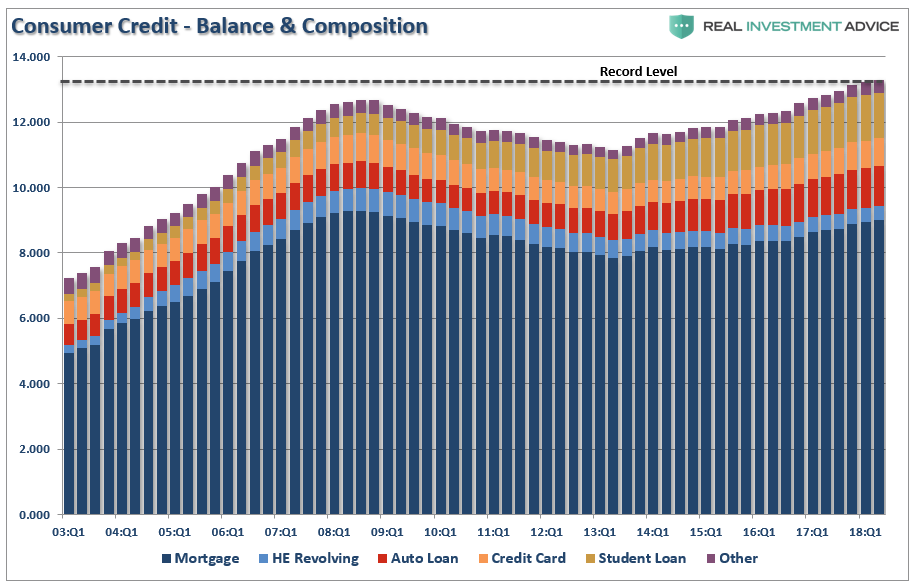

This is why we continue to see consumer credit hitting all-time records despite an economic boom, rising wage growth, historically low unemployment rates.

The mirage of consumer wealth has not been a function of a broad increase in the net worth of Americans, but rather a division in the country between the Top 20% who have the wealth and the Bottom 80% dependent on increasing debt levels to sustain their current standard of living.

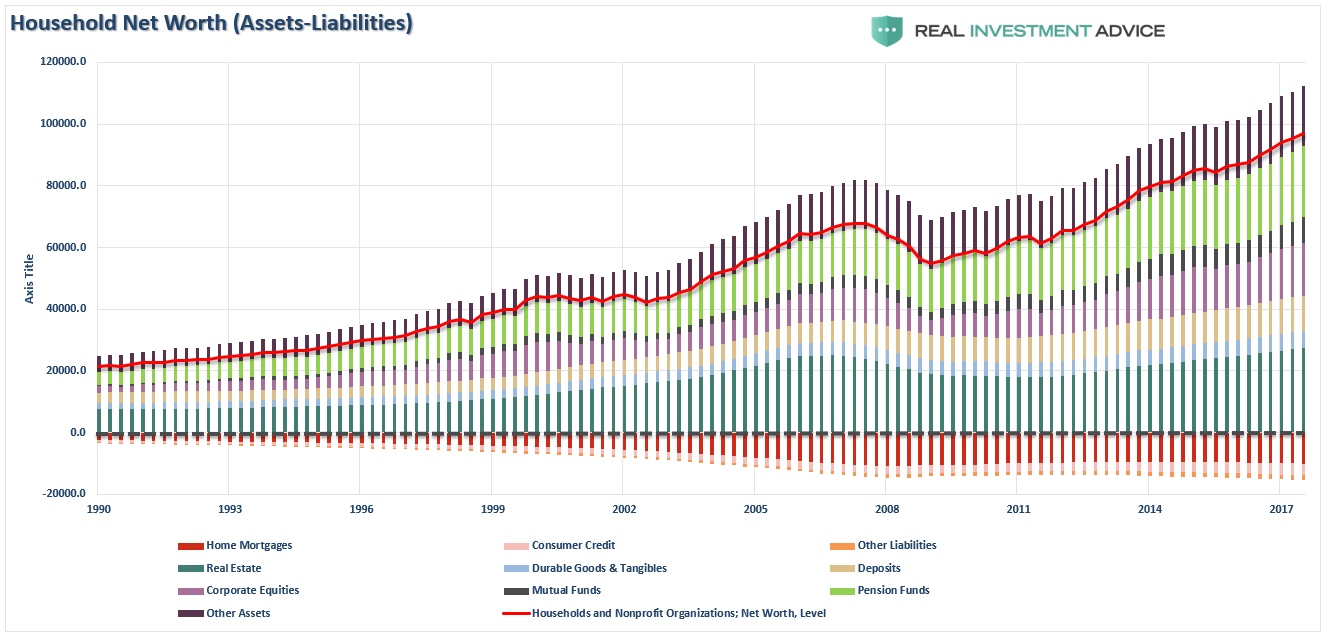

Nothing brought this to light more than the Fed’s own report on “The Economic Well-Being Of U.S. Households.” The overarching problem can be summed up in one chart:

More Money

Of course, by just looking at household net worth, once again you would not really suspect a problem existed. Currently, U.S. households are the richest ever on record. The majority of the increase over the last several years has come from increasing real estate values and the rise in various stock-market linked financial assets like corporate equities, mutual and pension funds.

However, once again, the headlines are deceiving even if we just slightly scratch the surface. Given the breakdown of wealth across America we once again find that virtually all of the net worth, and the associated increase thereof, has only benefited a handful of the wealthiest Americans.

Despite the mainstream media’s belief that surging asset prices, driven by the Federal Reserve’s monetary interventions, has provided a boost to the overall economy, it has really been anything but. Given the bulk of the population either does not, or only marginally, participates in the financial markets, the “boost” has remained concentrated in the upper 10%. The Federal Reserve study breaks the data down in several ways, but the story remains the same – “if you are wealthy – life is good.”

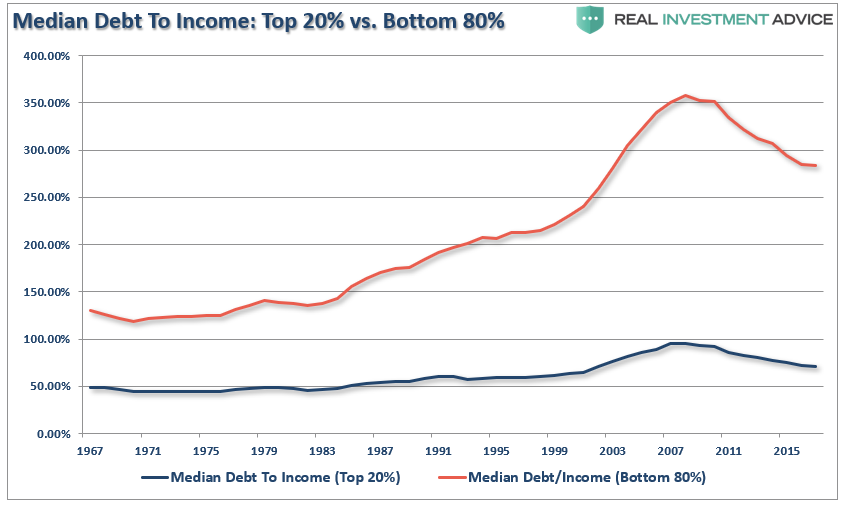

The illusion by many of ratios of “economic prosperity,” such as debt-to-income ratios, wages, assets, etc., is they are heavily skewed to the upside by the top 20%. Such masks the majority of Americans who have an inability to increase their standard of living. The chart below is the debt-to-disposable income ratios of the Bottom 80% versus the Top 20%. The solvency of the vast majority of Americans is highly questionable and only missing a paycheck, or two, can be disastrous.

While the ongoing interventions by the Federal Reserve have certainly boosted asset prices higher, the only real accomplishment has been a widening of the wealth gap between the top 10% of individuals that have dollars invested in the financial markets and everyone else. What monetary interventions have failed to accomplish is an increase in production to foster higher levels of economic activity.

It is hard to make the claim the economy is on the verge of acceleration with the underlying dynamics of savings and debt suggesting a more dire backdrop. It also goes a long way in explaining why, as stated above, the majority of Americans are NOT saving for their retirement.

“In addition, many workers whose employers do offer these plans face obstacles to participation, such as more immediate financial needs, other savings priorities such as children’s education or a down payment for a house, or ineligibility. Thus, less than half of non-government workers in the United States participated in an employer-sponsored retirement plan in 2012, the most recent year for which detailed data were available.”

But more importantly, they are not saving on their own either for the same reasons.

“Among filers who make less than $25,000 a year, only about 8% own stocks. Meanwhile, 88% of those making more than $1 million are in the market, which explains why the rising stock market tracks with increasing levels of inequality. On average across the United States, only 18.7% of taxpayers directly own stocks.”

With the vast amount of individuals already vastly under-saved, the next major correction will reveal the full extent of the “retirement crisis” silently lurking in the shadows of this bull market cycle.

This isn’t just about the “baby boomers,” either.

Millennials are haunted by the same problems, with 40%-ish unemployed, or underemployed, and living back home with parents.

In turn, parents are now part of the “sandwich generation” who are caught between taking care of kids and elderly parents.

But the real crisis will come when the next downturn rips a hole in the already massively underfunded pension funds on which many American’s are now solely dependent.

For the 75.4 million “boomers,” about 26% of the population, heading into retirement by 2030, the reality is that only about 20% will be able to actually retire.

The rest will be faced with tough decisions in the years ahead.

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice