The “Black Swan” Author Just Issued a Powerful Warning About Global Debt

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

By Photo:flickr/Joe Loong | Creative Commons Attribution 2.0 Generic |

The world is more fragile today than it was in 2007. That’s the opinion of former derivatives trader Nassim Taleb, whose bestseller, The Black Swan, is about how people make sense of unexpected events, especially in financial markets. True to form, he made a whole lot of money after predicting the global financial crisis more than a decade ago.

Speaking with Bloomberg’s Erik Schatzker this week, Taleb said the reason why he has reservations about today’s economy is that it suffers from the “same disease” as before. The meltdown in 2007 was a “crisis of debt,” and if anything, the problem has only worsened.

Indeed, debt is on the rise. By the end of the first quarter, the total amount the world owes climbed to a record $247 trillion, according to the Institute of International Finance (IIF). That’s up almost $150 trillion over the past 15 years.

A lot of this debt, Taleb said, may have moved to different places since the financial crisis—it’s shifted from housing to governments and corporate balance sheets—but the debt “is still there.” Student loan debt in the U.S., for example, stands at about $1.5 trillion today, or nearly $33,000 per borrower. After mortgages, student debt is now the largest form of debt in the U.S.

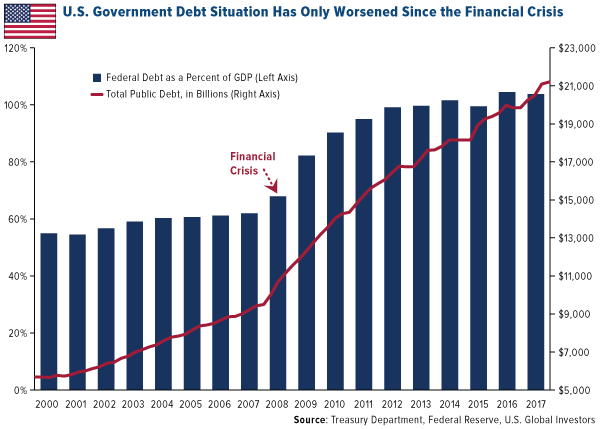

Just look at the federal government’s balance sheet. Gross debt has more than doubled from pre-recession levels, meaning Washington now owes slightly more than the entire size of the U.S. economy.

Higher Debt Levels Pose an “Economic Threat”

President Donald Trump said this week that “we’re going to start paying down debt.” But all the signs appear to say otherwise. The Treasury Department estimates that it will issue some $1.338 trillion in debt this year—more than twice the amount as last year. And the Office of Management and Budget (OMB) recently reported that the government is set to run trillion-dollar deficits for the next four years, despite a roaring economy.

Photo: Gage Skidmore | Creative Commons Attribution-Share Alike 3.0 Unported license |

According to Taleb, the U.S. government is now in a “debt spiral,” meaning it must borrow to repay its creditors. And with rates on the rise, servicing all this debt will continue to get more and more expensive.

Did you know that the government could soon pay more in interest than on defense? Interest costs are projected to become the third largest category in the federal budget by 2026, according to the Peter G. Peterson Foundation’s analysis of Congressional Budget Office (CBO) data. By 2046, these payments could become the second largest category; and by 2048, the single largest category.

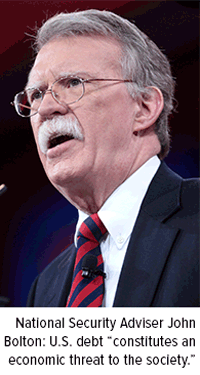

“It is a fact that when your national debt gets to the level ours is, that it constitutes an economic threat to the society,” National Security Adviser John Bolton said this week in Washington, D.C. “And that kind of threat ultimately has a national security consequence for it.”

Spending reform, especially entitlement spending reform, is politically unpopular and will require bipartisan support, according to Senate Majority Leader Mitch McConnell.

“I think it’s pretty safe to say that entitlement changes, which is the real driver of the debt by any objective standard, may well be difficult if not impossible to achieve when you have unified government,” McConnell told Bloomberg last month.

The U.S. isn’t alone in its budget woes, of course. Several European Union (EU) members are facing big budget crunches of their own, with Belgium, Spain and Italy leading the way. Last month, Moody’s Investors Service reported that “rising mandatory spending and slowing economic growth have left a number of euro area governments with less budget flexibility than before the financial crisis a decade ago.”

So how will this all play out, and what can investors do?

Could the “Barbell Strategy” Whip Your Portfolio Into Shape?

We all know what happened in 2007 and 2008, after debt levels became unsustainable. During the interview, Taleb stopped short of predicting another such crash, but he stressed the importance of paying attention to the risks.

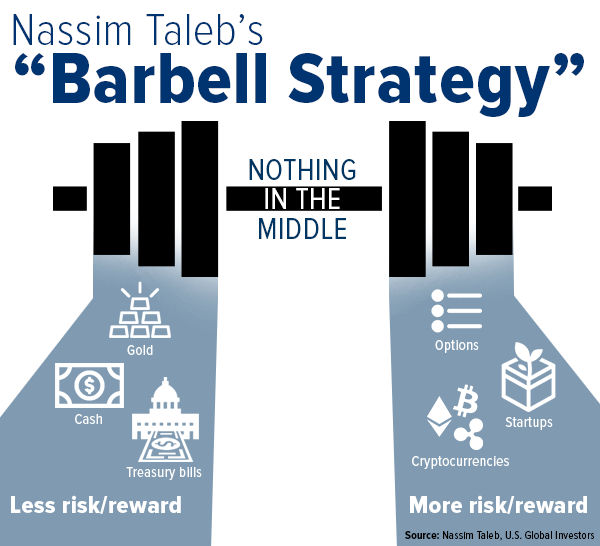

As for his current allocations, he’s invested in real estate, short-term Treasuries and gold, “just in case.” If you own stocks, he said, make sure you have some kind of put protection. Readers of his books might recognize this approach as the “barbell strategy.” Here he is in The Black Swan:

If you know that you are vulnerable to prediction errors, and if you accept that most “risk measures” are flawed… then your strategy is to be as hyperconservative and hyperaggressive as you can be instead of being mildly aggressive or conservative. Instead of putting your money in “medium risk” investments… you need to put a portion, say 85 to 90 percent, in extremely safe instruments, like Treasuries—as safe a class of instruments as you can manage to find on this planet. The remaining 10 to 15 percent you put in extremely speculative bets, as leveraged as possible (like options), preferably venture capital-style portfolios. That way you do not depend on errors of risk management.

I share Taleb’s unconventional allocation strategy with you not because I fully endorse it but simply as food for thought. It evokes the discussion I had earlier in the week about investing vs. speculating, with gold and government bonds on one end, venture capital and digital currencies on the other. And although I believe your portfolio should leave room for equities—domestic as well as emerging market—there is some merit to Taleb’s idea that you should be both incredibly defensive and incredibly aggressive.

You can watch the full Bloomberg interview by clicking here.

The Fear Trade and Love Trade Make Gold Look Compelling

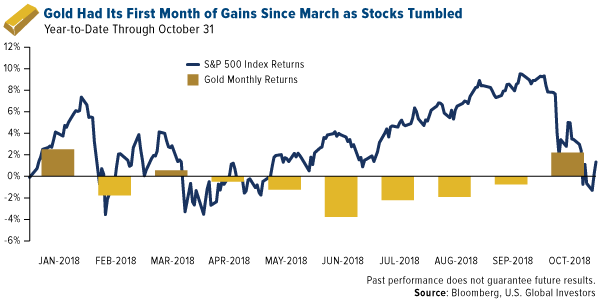

Speaking of gold, the Fear Trade moved prices in October, the “jinx month,” as volatility spiked and stocks lost most of their gains for the year. The yellow metal managed to notch its first positive month since March, despite still being under pressure from a stronger U.S. dollar and higher yields.

The third quarter was a solid one for gold’s Love Trade, according to the most recent report by the World Gold Council (WGC). Total demand in India was up 10 percent from the same time a year ago, just ahead of next week’s Diwali festival. Chinese demand increased at about the same rate, with jewelry sales up during the Qixi festival, China’s equivalent of Valentine’s Day.

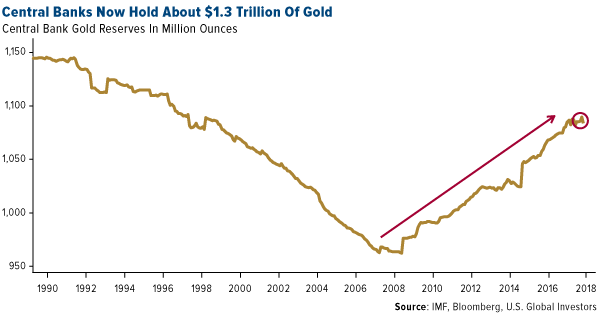

Purchases made by central banks, meanwhile, were very robust in the third quarter, up an impressive 22 percent from a year ago. At 148.8 metric tons, the amount was the highest for any quarter since the end of 2015.

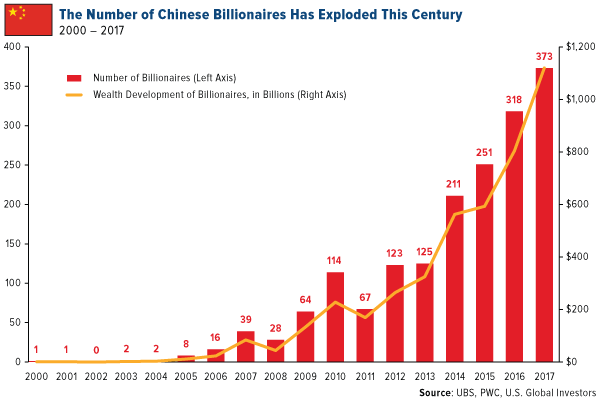

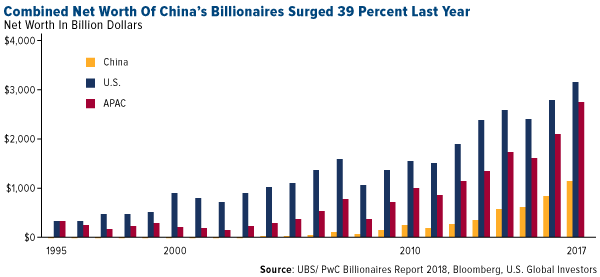

I’ve pointed out before that global gold demand has benefited from a rise in wealth, which we’re seeing today. A recent report by UBS showed that wealth shared among the world’s billionaires enjoyed its greatest-ever increase in 2017, rising 19 percent to a new all-time high of close to $9 trillion. China, however, was the clear standout, with wealth among its now-373 billionaires climbing 39 percent to $1.12 trillion. That’s double the global rate.

The Asian giant minted two new billionaires per week last year, according to UBS, an incredible feat for an economy that had only one billionaire at the beginning of the century.

It’s the Policies, Not the Party

On a final note, midterm elections are only four days away. Historically, the president’s party has lost Congressional seats in his first term, but it’s important to temper whatever expectations you might have with some perspective. When evaluating the macro investment climate, it’s not the party that matters so much as the policies, and so I’m a firm believer that there are ways to make money no matter which party is in control. Next week I’ll definitely be sure to share with you my thoughts on the election results!

Gold Market

This week spot gold closed at $1,232.96, down $0.17 per ounce, or 0.1 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.04 percent. The S&P/TSX Venture Index underperformed its large-cap peers by climbing just 1.21 percent. The U.S. Trade-Weighted Dollar rose 0.13 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-30 | Germany CPI YoY | 2.4% | 2.5% | 2.3% |

| Oct-30 | Conf. Board Consumer Confidence | 135.9 | 137.9 | 135.3 |

| Oct-31 | Eurozone CPI Core YoY | 1.1% | 1.1% | 0.9% |

| Oct-31 | ADP Employment Change | 187k | 227k | 218k |

| Oct-31 | Caixin China PMI Mfg | 50.0 | 50.1 | 50.0 |

| Nov-1 | Initial Jobless Claims | 212k | 214k | 216k |

| Nov-1 | ISM Manufacturing | 59.0 | 57.7 | 59.8 |

| Nov-2 | Change in Nonfarm Payrolls | 200k | 250k | 118k |

| Nov-2 | Durable Goods Orders | -- | 0.7% | 0.8% |

| Nov-8 | Initial Jobless Claims | 214k | -- | 214k |

| Nov-8 | FOMC Rate Decision (Upper Bound) | 2.25% | -- | 2.25% |

| Nov-9 | PPI Final Demand YoY | 2.6% | -- | 2.6% |

Strengths

- The best performing metal this week was platinum, up 4.29 percent as hedge funds cut their bearish platinum view to the lowest in seven months. Gold ended October with a gain for the first month in seven. The Bloomberg Intelligence (BI) Global Senior Gold Valuation Peer Group Index is headed for its biggest monthly increase since August 2017, reports Bloomberg. Traders and analysts in the weekly Bloomberg survey are mixed on the gold price outlook this week amid uncertainty of how U.S. midterm elections will affect markets. “If the Democrats win the house, that is positive for gold because we won’t get more tax reform, though the response could be delayed,” says Adrian Day, chairman and CEO of Adrian Day Asset Management.

- In a rare turn of events, both gold and the dollar performed well in October. Historically, the two assets move in opposite directions, with the yellow metal suffering as the dollar gains. Bloomberg reports that both gained ground for the first time in 20 months in the same month.

- Iran is looking to gold for safety during times of increasing sanctions. The country’s demand for gold bars and coins rose to a five-year high in the third quarter of this year after U.S. sanctions imposed on the precious metals trade resumed on August 7. Centamin PLC reported positive third quarter results, with production climbing 27 percent to 117,720 ounces of gold.

Weaknesses

- The worst performing metal this week was gold, coming in essentially unchanged for the week. Australia’s Perth Mint reported that minted gold bar sales fell to just 36,840 ounces in October, down from 62,552 ounces in September. The U.S. plans to impose sanctions on troubled Venezuela to target its recent behavior of exporting gold to Turkey. The nation’s gold reserves have shrunk by more than half since the end of 2014, as the government has been selling bullion to support its struggling economy and government operations, reports Bloomberg. Managing researcher at CPM Group Jeffrey Christian says that most of Venezuela’s gold has been sold to prop up the government and that the nation “is a backwater in terms of the gold market.”

- On Friday morning it was announced that the U.S. economy added more jobs than expected. Bloomberg’s Susanne Barton writes that this could mean the gold rally might not last. The dollar has remained resilient and the rebound in global equities has trimmed demand for gold as a safe haven asset.

- Average hourly earnings for private workers advanced 3.1 percent from a year earlier, the biggest pay leap since 2009, while the unemployment rate held steady at 3.7 percent, a 48-year low. Even as pay continues to rise, Americans are still increasing their spending and pushing down the savings rate to the lowest this year, reports Bloomberg. U.S. Commerce Department data shows that Americans saved 6.2 percent of their disposable income, matching the lowest level since 2013.

Opportunities

- Goldman Sachs economists predict a divided Congress as the most likely outcome of the U.S. midterm elections next week, with Democrats taking control of the House of Representatives and Republicans retaining a small majority in the Senate. Analysts including Mikhail Sprogis and Jeffrey Currie wrote in a report that “this is incrementally bearish on U.S. growth but bullish on gold.” Goldman Sachs also sees strong fundamentals for gold, as the most recent rally coincided with the selloff in equities. The bank forecasts a slowdown in U.S. growth to 2.6 percent, down from 2.9 percent, and a pickup in core inflation to 2.5 percent. Election results could see the dollar’s rally end due to political uncertainty and a smaller chance of fresh economic stimulus, writes Bloomberg’s Austin Weinstein.

- The World Gold Council (WGC) reported this week that central banks bought around $5.8 billion worth of gold in the third quarter of this year, marking the biggest buying spree since 2015. Central banks largely buy gold in an effort to diversify their reserves. Since the yellow metal is a finite asset, as opposed to fiat currency, it can help economies stabilize amid times of economic turbulence. Hungary and Poland emerged recently as big gold buyers in an effort to shift away from the dollar-denominated financial system and brace for a potential currency risk as global inflation picks up.

- The London Bullion Market Association (LBMA) surveyed attendees at its annual gathering in Boston and results show that gold is forecast to climb 26 percent in the next year, up to $1,532 an ounce. According to George Milling-Stanley, head of global strategy at State Street Global Advisors, gold’s next significant resistance level is $1,350 an ounce and prices may test that level within six to 12 months. We’re now entering the historically strongest eight months for gold demand, with festivals in India and China, as well as Christmas and Valentine’s Day celebrations, writes Bloomberg. Perth Mint CEO Richard Hayes said in an interview at the LBMA last week that the recent stock selloff has reignited caution in many investors. Hayes also said that “if the midterms go badly for Trump, you’ll see a return to gold” because “a lot of Trump’s true believers are precious metals buyers.”

Threats

- According to the WGC, demand for gold during India’s festival of Diwali may be moderate due to a lack of liquidity in the market, which has raised the country’s bullion prices. India, the world’s second largest consumer of gold after China, has seen imports on a declining trend due to the government’s efforts to curb its trade deficit. This is significant since the country must import almost all of its gold.

- The $700 million Rhicon Currency Management hedge fund shut down the bulk of its positions three weeks ago, and the fund’s intra-month strategy is completely flat because nothing looks compelling, according to managing director Peter Jacobson. Jacobson is not trading and the restraint has served the fund well, as it is up nearly 5 percent in a year that has seen most macro managers stumble. Rhicon was also previously bullish on the dollar, but is not so much anymore. Bloomberg reports that U.S. auto sales might fall into negative territory for the year as a whole due to plunging demand for passenger cars and costlier loans. China’s automotive market has been damaged by the trade war with the U.S. and might be considering a tax cut to help revive the market.

- According to JPMorgan Chase, if investors want to avoid geopolitical risk they should increase positions in the dollar and volatility indexes, while leaving favorite hideaways such as the yen and gold. The bank said that traditional safe havens haven’t necessarily been holding up as stores of value during times of new geopolitical threats and market turbulence.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.36 percent. The S&P 500 Stock Index rose 2.42 percent, while the Nasdaq Composite climbed 2.65 percent. The Russell 2000 small capitalization index gained 4.32 percent this week.

- The Hang Seng Composite gained 7.76 percent this week; while Taiwan was up 4.40 percent and the KOSPI rose 3.40 percent.

- The 10-year Treasury bond yield rose 14 basis points to 3.22 percent.

Domestic Equity Market

Strengths

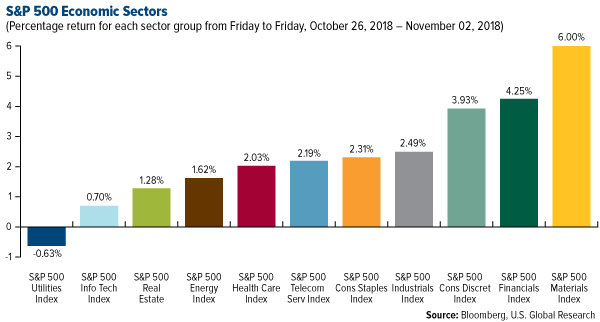

- Materials was the best performing sector of the week, decreasing by 6.09 percent versus an overall increase of 2.43 percent for the S&P 500.

- Red Hat Inc. was the best performing stock for the week, increasing 47.42 percent.

- IBM is acquiring software company Red Hat for $34 billion. IBM will pay $190 per share for Red Hat, which it described as the world's leading provider of open source cloud software.

Weaknesses

- Utilities was the worst performing sector for the week, decreasing by 0.58 basis points versus an overall increase of 2.43 percent for the S&P 500.

- General Electric Co. was the worst performing stock for the week, falling 17.57 percent.

- Things just keep getting worse for Advanced Micro Devices, Inc. (AMD) shareholders. The former stock-market darling and technology company, which saw its stock price explode by as much as 230 percent in the first eight and a half months of the year, has seen its value get cut in half over the past six weeks as disappointing earnings and a comeback by Intel have decimated shares.

Opportunities

- Warren Buffett's Berkshire Hathaway just made a $400 million investment in the Brazilian payments platform StoneCo, according to The Wall Street Journal. The deal comes just a few months after Berkshire invested $300 million in the Indian mobile-payment platform Paytm.

- Under Armour shares surged Tuesday after it reported better than expected quarterly earnings and revenue thanks to a spike in sales overseas and fewer promotions. The company also raised its earnings outlook for the full year. The results offer investors a sign that the retailer’s turnaround efforts are paying off after years of irregular sales.

- A big Tesla shareholder is ready to back Elon Musk with more cash, despite questioning the CEO’s moves recently. A partner at Scottish investment firm Baillie Gifford, one of Tesla's largest shareholders, told The Times of London that they would be willing to back Elon Musk with more cash if needed.

Threats

- Bank of America is on “crash watch.” Michael Hartnett, the firm's chief investment strategist, says the three P's (positioning, profits, and policy) suggest it's still too early to flip from bearish to bullish.

- One key indicator suggests investors need to get more nervous before stocks can bottom. The Arms index, known as TRIN, which compares advancing and declining stock issues and trading volume as an indicator of market sentiment, has yet to cross the threshold that shows true investor panic.

- Betting against FAANG stocks (Facebook, Apple, Amazon, Netflix and Alphabet’s Google) has made traders $5.5 billion during the brutal October selloff. Short-sellers of FAANG stocks have seen $5.52 billion in mark-to-market profits since the beginning of October, a return of 17.14 percent on an average short position of $32.2 billion, according to data from S3 Partners, a financial-analytics firm.

The Economy and Bond Market

Strengths

- Consumer confidence increased in October, following a modest gain in September, and remains at levels last seen in late 2000, said Lynn Franco, senior director of economic indicators at The Conference Board. Consumers' assessment of present-day conditions remains positive, largely due to strong employment growth. The Expectations Index posted another gain last month, suggesting that consumers do not foresee the economy slowing anytime soon. Rather, they expect the strong pace of growth to continue into early next year.

- Consumer spending, which accounts for more than two-thirds of U.S. economic activity, increased 0.4 percent in October as households purchased more motor vehicles and spent more on health care. Data for August was revised up to show spending advancing 0.5 percent, instead of the previously reported 0.3 percent gain.

- Productivity gains in the U.S. posted the best back-to-back quarters since 2015, echoing a pickup in economic growth and offering some hope that faster expansion without triggering inflation is possible. The main measure of nonfarm business employee output per hour grew at a 2.2 percent annualized rate in the July-September period, according to a Labor Department report released on Thursday.

Weaknesses

- U.S. consumer income recorded its smallest gain in more than a year on moderate wage growth, suggesting the current pace of spending is unlikely to be sustained. A report from the Commerce Department on Monday showed the increase in disposable household income was the smallest gain in 15 months and savings dropped to their lowest level since December 2017.

- Home price gains in 20 U.S. cities cooled in August to the slowest pace since 2016 (5.5 percent growth year-over-year), as high borrowing costs and property values limit buyer interest, according to S&P CoreLogic Case-Shiller data released on Tuesday.

- A gauge of U.S. manufacturing fell by more than forecast to a six-month low, as orders and hiring cooled amid escalating trade tensions with China, data from the Institute for Supply Management showed Thursday. The factory index dropped to 57.7, down from 59.8 the month prior. A reading above 50 indicates expansion.

Opportunities

- Next Thursday’s FOMC rate decision is unlikely to see another rate hike, as market participants widely anticipate the last rate hike of the year to take place in December. However, investors will pay close attention to any hints about changes in the Fed’s assessment of the economy, especially given the recent market turbulence.

- Next Friday’s November preliminary release of the University of Michigan Sentiment survey is likely to remain near recent elevated levels. Consumer economic expectations have remained anchored to the upside despite trade war angst among business leaders.

- Next Monday’s release of the ISM Non-Manufacturing Index is likely to remain near recent highs.

Threats

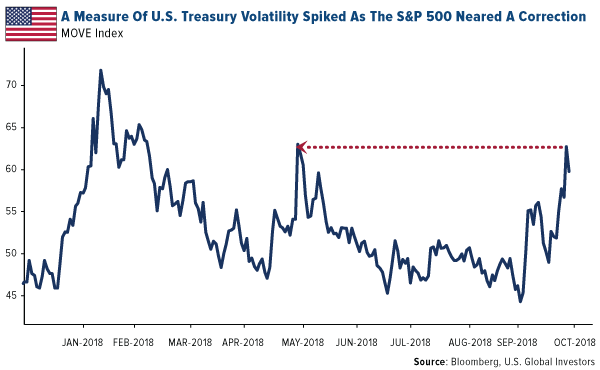

- Volatility expectations for U.S. Treasuries – as measured by the Merrill Lynch Option Volatility Estimate Index – spiked to their highest since May after another rout threatened to push the S&P 500 into a correction. With U.S. stocks headed for their worst month since 2009, the bond market is starting to lose confidence in the Federal Reserve’s policy tightening projections and traders are paring wagers for rate hikes in 2019.

- President Donald Trump is preparing tariffs on the final $257 billion worth of Chinese goods. The Trump administration is set to levy tariffs on all remaining U.S. imports from China in the event that trade talks at the G20 summit between President Trump and Chinese President Xi Jinping fail in late November.

- The U.S. is on track to issue its highest amount of debt since the 2008 recession. The federal government is projected to issue $1.34 trillion of new debt in 2018, according to Treasury Department projections released Monday.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing commodity, rising 9.29 percent for the week. The commodity rebounded to a three week high after a number of producers announced plans to curb supply output to address the softness in the U.S. housing sector.

- The best performing sector for the week was the S&P 1500 Construction & Materials Index. The index rose 14.40 percent, rebounding from a deep oversold condition as prospects for the U.S. equity markets turned positive toward the end of the week. In addition, a number of index constituents reported third quarter earnings this week with better than anticipated results and positive spins on year end guidance.

- The best performing major natural resource stock for the week was Hudbay Minerals Inc. The Canadian base metals producer rose 34.95 percent, soaring the most in nine years after announcing stronger than anticipated third quarter earnings. Last month the company’s share price fell after suggesting a major acquisition could take place. This week the company said that is now unlikely as management is focusing on execution instead.

Weaknesses

- Crude oil was the worst performing commodity for the week. The price fell 6.78 percent, as analysts fear a possible oversupply in the market, resulting from higher OPEC production, near-record Russian output and the prospects of certain buyers receiving waivers to continue importing Iranian crude despite U.S. sanctions.

- The worst performing sector this week was the S&P/TSX Oil & Gas Exploration and Production Index. The index dropped 3.82 percent, tracking the decline in oil prices.

- The worst performing stock for the period was Anadarko Petroleum Corp. The major oil and gas producer dropped 8.94 percent after missing third quarter earnings estimates. In addition, the growth prospects of the company hinge on a controversial Colorado vote next week, which seeks to limit oil and gas drilling in the state.

Opportunities

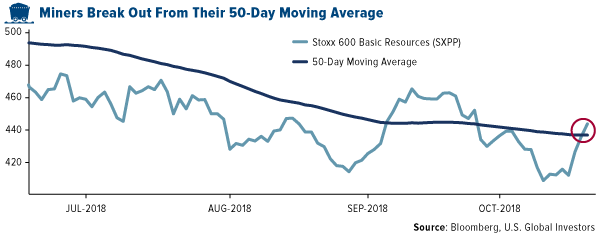

- Mining stocks broke through resistance on U.S.-China trade deal prospects. The Stoxx Europe 600 Basic Resources Index rebounded sharply after people familiar with the matter said U.S. President Donald Trump wants to reach an agreement on trade with Chinese President Xi Jinping at the G20 Summit later this month. The index rose above its 50-day moving average, a major resistance level.

- Goldman Sachs sees solid fundamentals for gold prices. “A low and falling U.S. unemployment rate, combined with slowing growth and rising inflation, should boost ‘fear’-related […] gold demand,” analysts including Mikhail Sprogis and Jeffrey Currie wrote in a report.

- Australian mining giant Fortescue says worsening trade tensions and slowing economic growth have not dampened Chinese demand for iron ore. Similarly, miner and commodity trader Glencore said the price for high quality thermal coal can remain stronger for longer, as production of the fossil fuel struggles to keep up with global demand.

Threats

- China’s manufacturing sector expanded in October at its weakest pace in over two years, hurt by slowing domestic and external demand. This is a sign of deepening cracks in the economy from an intensifying trade war with the U.S. New export orders, an indicator of future activity, contracted for the fifth straight month and at the fastest pace in at least a year. The official PMI fell to 50.2 in October, the lowest since July 2016.

- The euro-area economy grew at its weakest pace in more than four years in the third quarter. GDP rose by 0.2 percent, below the 0.4 percent increase expected by economists. Growth in Germany and Italy ground to a halt, while consumer and business sentiment fell in October to the lowest in 17 months. The slowdown comes at a crucial time for the European Central Bank as it prepares to cap asset purchases.

- The U.S. will allow China, India, South Korea and four other nations keep buying Iranian oil after it reimposes sanctions on November 5. The administration’s goal remains to choke off revenue to Iran’s economy, but waivers are being granted to avoid a rally in crude oil prices.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 4.25 percent. Equites trading on the Warsaw Stock Exchange recovered losses from last week. CDR Project was the best performing equity, gaining 15 percent in the past five days after successfully launching its new game, the Red Dead Redemption 2. Poland’s manufacturing PMI for October was reported at 50.4, above expectations of a 50.2 reading.

- The Turkish lira was the best performing currency this week, gaining 3.1 percent against the dollar. The U.S. Treasury Department lifted sanctions on two Turkish officials targeted in retaliation for the country’s detentions of an American pastor, who was released last month. The country’s trade gap narrowed in October to smallest since 2001, as imports fell and exports increased. October’s manufacturing PMI reading moved a notch higher, but still remains below the 50 level that separates growth from contraction.

- Information technology was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 2.2 percent. Motor Oil, a refinery, was the biggest loser among the stocks trading on the Athens exchange, down more than 16 percent in the past five days. The company unexpectedly announced non-core acquisitions of Alpha TV/Radio & Investment Bank of Greece/CPB. Greece’s manufacturing PMI for October is 53.1, slightly lower than the September reading of 53.6.

- The Russian ruble was the worst performing currency this week, losing 63 basis points against the dollar. The ruble dropped due to a weaker oil price and ahead of a second round of sanctions as a part of the Chemical and Biological Weapons Act.

- Consumer Discretionary was the worst performing sector among eastern European markets this week.

Opportunities

- Russia climbed four places higher to the 31st spot on the World Banks’s Global Ease of Doing Business Index thanks to reforms that helped smooth cross-border trade and cut waiting times for some permits, according to Bloomberg. Back in 2012, Russian President Vladimir Putin ordered Prime Minister Dimitry Medvedov to lift the country to number 20 from 120 as part of a long-term project. However, Russia still ranks 11 places lower than President Putin’s goal of reaching the world’s top 20 economies in the annual list by 2018.

- Moody’s Investor Service thinks that the U.S. will sanction Russia’s sovereign debt, but still might upgrade the country to investment grade. Moody’s analyst Kristin Lindow says that Russia can cope with stricter sanctions because it does not have any urgent need to borrow. The nation’s outstanding debt is among the lowest in emerging markets and is on track to run a budget surplus in 2018 for the first time in seven years.

- Emerging markets may rally on growing optimism that leaders of the U.S. and China will strike a deal on trade when they meet later this month. President Donald Trump has asked his cabinet to draft a possible trade deal with Chinese President Xi Jinping. Prospects for easing trade tensions are helping to increase investors’ appetite for riskier assets.

Threats

- The Eurozone manufacturing PMI declined further in October to a reading of 52, down from the September reading of 53.2. The United Kingdom’s manufacturing growth slumped to 51.1, down from 53.8. Additionally, Italy’s manufacturing PMI dropped below the 50 level that separates growth from contraction. The Eurozone also reported weaker GDP in the third quarter, growing its economy by only 20 basis points, while 40 basis points were expected. Despite the slowdown in economic growth, the European Central Bank might stay on track to end its bond-buying program by December and start hiking rates next year.

- German Chancellor Angela Merkel announced this week that she would step down as head of the center-right Christian Democratic Union (CDU) party in December after almost 20 years. Her announcement came one day after her party suffered huge losses in regional elections.

- Russia is fundamentally strong, but there is still the risk of more U.S. sanctions being imposed. Back in August, the U.S. imposed a first set of sanctions on Russia for the alleged poisoning of a former British spy and their daughter, and the second set of sanctions was to be released within 90 days. More sanctions on Russia may be announced after the U.S. mid-term elections.

China Region

Strengths

- Hong Kong’s Hang Seng Composite Index jumped a rip-roaring 7.76 percent for the week, in a volatile but green week for the region.

- Both imports and exports clocked in higher than expected in South Korea for the October readings. Imports rose 27.9 percent year-over-year, well ahead of an expected 19.9 percent print, while exports jumped 22.7 percent, better than analysts’ anticipated 18.0 percent reading.

- China’s Caixin China Manufacturing PMI held relatively steady this month at 50.1, barely nudging out expectations for a 50.0 print and rising slightly from 50.0.

Weaknesses

- Indonesia’s Jakarta Composite Index climbed a mere 83 basis points in total return for the week, and the Philippines’ Stock Exchange Index climbed only 1.08 percent.

- China’s official Manufacturing and Non-manufacturing PMI readings both came in down from the prior readings and below analysts’ respective expectations for this month. The Manufacturing PMI print was 50.2, shy of 50.6 and down from 50.8; the Non-manufacturing was 53.9, shy of 54.6 and down from 54.9.

- Thailand’s exports number declined to a -5.5 percent year-over-year rate from the prior month’s growth of 5.8 percent.

Opportunities

- The combined wealth of China’s billionaires jumped 39 percent last year to $1.12 trillion, experiencing more than double the gains of peers in the U.S. and Europe. According to the Billionaires Report from UBS and PricewaterhouseCoopers LLP, the nation generated two billionaires a week on average due to a booming tech industry and a rising number of startups. However, these billionaires are not immune to stock market dips, as half of those crowned last year saw their wealth fall below 10 digits by year end.

- It was “long and very good.” That’s what Xi said. Actually, it’s what U.S. President Donald Trump said about his conversation with Chinese President Xi Jinping, on the very important subject of trade, which helped spark a jump in China and Hong Kong (and elsewhere) shares and brings a touch of optimism toward trade talks once again. President Trump is said to have invited President Xi to a dinner he will host at the upcoming G20 summit; President Xi is said to have tentatively accepted (Larry Kudlow confirmed a definite meeting), and while there are still significant differences in the American and Chinese positions, a renewal of discussions is obviously a positive development. President Trump reiterated late in the day Friday that he does indeed think the U.S. will eventually reach a trade deal with China.

- Next week will mark the start of China’s first China International Import Expo, which was first proposed way back in 2013 as part of the Belt and Road initiative. Trade promotion agencies from Malaysia to Cambodia are talking up the opportunity. “It will be a golden opportunity for us to find new markets for our products,” Seang Thay, director general of the Cambodian Ministry of Commerce’s Trade Promotion General Directorate, said.” One intriguing possibility for readers to consider is that, while sure, a U.S.-China spat may have some clear downsides, a possible upside opportunity is that amid the resulting fractures of global trade, intra-regional trade and regional blocs and organizations may serve to deepen ties (e.g. One Belt, One Road) amid the area’s existing trading partners and arrangements. Food for thought.

Threats

- On the other hand, trade war concerns continue (and will until they don’t), with the latest round of headlines indicating that the United States is prepared to go ahead with tariffs following the Trump-Xi discussions at the end of this month if they are not satisfactorily productive, and the U.S. accusing China of stealing Micron’s secrets. Moreover, in a Larry Kudlow interview on Friday afternoon Mr. Kudlow walked back the notion that President Trump might have requested Congress draw up some kind of trade deal with respect to China. He also downplayed the notion that any sort of detailed trade agreement would emerge from a Trump-Xi G20 meeting.

- A bus project aiming to connect Kashgar, Pakistan and Xinjiang, China has come under metaphorical fire from India, which claims the service “will be a violation of India’s sovereignty and territorial integrity,” according to the South China Morning Post. Raveesh Kumar, India’s foreign ministry spokesman, stated that they “have lodged strong protests with China and Pakistan on the proposed bus service” as a result of its route passing through disputed territory. The proposed luxury bus trip is part of the China-Pakistan Economic Corridor (CPEC), a group of infrastructure venture worth nearly $50 billion. CPEC is a piece of the larger Belt and Road Initiative.

- Two men are claiming the title of Sri Lankan prime minister, after President Maithripala Sirisena ejected Ranil Wickremesinghe from the role and installed Mahinda Rajapaksa as his replacement. Sirisena claims this replacement was necessary as the former prime minister was allegedly plotting the president’s assassination. Wickremesinghe, however, has refused to vacate the position, calling the move unconstitutional and demanding that Parliament intervene. Casualties have already occurred during this political standoff.

Blockchain and Digital Currencies

Strengths

-

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 2 was Coupecoin, up 539.29 percent.

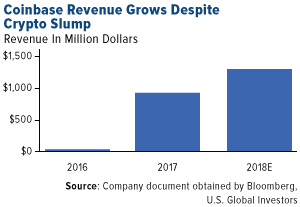

- Coinbase’s projected revenue for 2018 is at $1.3 billion, Bloomberg reports, citing internal documents of the company. Despite a general decline in the digital currency space, the largest U.S. cryptocurrency exchange was also valued at $8 billion this month, quintupling its worth since early 2017.

- Morgan Stanley acknowledged that bitcoin and altcoins have been a “new institutional investment class” since 2017 in a new report titled “Bitcoin Decrypted: A Brief Teach-In and Implications.” The document goes on to frame the decentralized technology in a positive light.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 2 was BitWhite, down 35.38 percent.

- Coincheck, a Japanese crypto exchange, experienced a 66 percent decrease in revenue during the third quarter of 2018, according to Monex Group. The exchange underwent major updates following the theft of $532 million worth of NEM in January. “Since service suspension in January 2018, Coincheck only allowed existing customers to sell their cryptocurrency,” says a report from Monex Group, resulting in a segment loss of around $5.3 million.

- At the New York Times Dealbook Conference, CEO Larry Fink stated that BlackRock has no intention of launching an exchange traded fund (ETF) for cryptocurrencies. For his position to change, bitcoin would “ultimately have to be backed by a government” as he believes “the world doesn't need [digital currency as] a store of wealth unless you need that store of wealth for things you should not be doing.” Despite his lack of support for cryptocurrencies, Fink did state that he is a “huge believer in blockchain.”

Opportunities

- During the ASEAN Energy Business Forum in Singapore, SP Group announced its blockchain-powered renewable energy certificate (REC) marketplace. RECs provide documentation that a set amount of energy has been produced via solar batteries. Cleantech Solar Asia, LYS Energy Solutions and Katoen Natie Singapore will reportedly join the marketplace, according to CoinTelegraph.

- The Economic Development and Trade Ministry of Ukraine announced it is taking the first steps toward legalizing cryptocurrencies by creating “understandable conditions for conducting activities in the field of virtual assets and virtual currencies,” according to Ukrinform. The proposed plan will be implemented in two stages, which should be completed in 2021.

- Russian diamond mining firm Alrosa has joined Tracr, a diamond supply blockchain by De Beers, according to Mining Weekly. These digital certificates aim to set customers at ease regarding “conflict diamonds,” also known as “blood diamonds,” by increasing transparency from mine to retail. Together, Alrosa and De Beers produce half the world’s supply of diamonds.

Threats

- Climate change scientists expressed mounting concern about bitcoin’s carbon footprint in a publication on Nature.com. The report posits that, if bitcoin is adopted at a rate equivalent to “the slowest broadly adopted technologies,” it could “cross the 2 degrees Celsius threshold within 22 years.” At the highest potential rate of adoption, that threshold could be crossed within 11 years. Scientists have abstained from making predictions about the future of the cryptocurrency itself, stating simply that “electricity de-carbonization could help to mitigate Bitcoin’s carbon footprint — but only where the cost of electricity from renewable sources is cheaper than fossil fuels.”

- Canadian crypto-exchange MapleChange was allegedly hacked, resulting in the loss of an undetermined amount of bitcoin and the company tweeting they had “no more funds” with which to pay investors. When the company’s Twitter profile disappeared, some media outlets began reporting this event as an exit scam, rather than a hacking. The page has since been restored and MapleChange denies the allegations of a scam.

- South Korea’s National Intelligence Service (NIS) reported that North Korea is responsible for the continued hacking of South Korean computers. Hackers have been installing malware which uses the afflicted computers to mine cryptocurrency and transfer it to Kim Il Sung University in Pyongyang, North Korea. The NIS believes the crypto-jacking is a way for the economically weaker country to generate cash flow.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All