Know Thyself

Lending Allows Spending

Wealth Gap

A Beautiful Deleveraging

IRA Magic

The Joys of Traveling, Puerto Rico and Cleveland

Science tells us energy can neither be created nor destroyed within a closed system. Whatever amount is there will stay the same, though it might change form. If only the same were true for debt.

Within the closed system called Earth, we are much better at creating debt than eliminating it. But when we have too much, we eventually eliminate it in painful and unpleasant ways via some kind of debt crisis. This has happened over and over again throughout history.

Today we’ll look at a new book by Ray Dalio called Principles for Navigating Big Debt Crises in which he examines those debt cycles and what we can do about them. I read it on my recent trip to Frankfurt and I highly recommend you do the same. That link is for Amazon but you can also get a free PDF copy here. I read it on my Kindle so I could highlight and save notes in the cloud for later reference. Worth every penny of the $14.99 I spent.

At a minimum, you should read the first 60 pages, which explain his principles and thoughts. The rest of the book dives deep in the weeds of 48 modern debt crises, sorting them into different types and then analyzing each type. Data wonks will love that part. Ray gives us a brilliant tour de force examination of how debt crises arise and what you can do when one strikes.

At first blush, you will think that Ray is more optimistic than I am about the next debt crisis and an eventual event which I called The Great Reset, which I’ve written about extensively this year. I see The Great Reset as a generation-scarring economic cataclysm. Debt crises, while painful, have a fundamentally different character.

Ray’s book has helped me refine what I mean by The Great Reset. We’ll explore this more in future letters but here is one very important, critical, point:

It is possible we will have another debt crisis separate from The Great Reset I envision. Indeed, it may be quite likely.

In one sense, what we called the “Great Recession” was just another garden-variety credit cycle. Unlike the Great Depression, so far it doesn’t seem to be changing the behavior of those who went through it. The Great Depression was a soul-searing, generational-impacting event. The events around 2008, bad as they were, had nowhere near that effect.

In fact, we are now many of the things we did in 2006 and 2007—reaching for yield, etc. It is as if we did not learn that the stove was hot. We are loading up on all sorts of unrated and low-rated credit and even leveraged (!!!) loans to juice returns in a low-rate world, telling ourselves “This Time is Different.”

Really, we tell ourselves that. And it never is. Sometimes I sit in awe and amazement at the human capacity for believing Six Impossible Things Before Breakfast. And we do it time and time again, over and over, insanely expecting a different result.

But that is getting ahead of ourselves, so let’s start exploring Ray’s book.

Know Thyself

Before we get into the book, you should know a little about Ray Dalio and the company he founded, Bridgewater Associates. At $150 billion or so under management, it is one of the world’s largest and most successful hedge fund operators. It is also an extremely unusual company.

Dalio decided early in his career, after enduring some painful losses and nearly going bankrupt, to rigorously examine his mistakes. When he was wrong—as all traders sometimes are—he would review his process, identify mistakes and keep a record of them. This helped him avoid making them again.

Eventually he extended this process to his entire company. At Bridgewater, the staff use a computer system to constantly rate each other’s decisions, both small and large. The result is a giant database of who tends to be right and on which subjects they are strong and weak. This affects personnel decisions, work assignments and all sorts of other things. It’s all transparent, too. Everyone at Bridgewater knows everyone else’s business.

Obviously, not everyone thrives in that environment. But over time, it’s made Bridgewater into what Ray calls an “idea meritocracy.” People who make good decisions get identified and rise to the top.

I tell you all that so you understand Dalio is highly empirical. He doesn’t make guesses without evidence, and you see it in this rigorous historical examination of previous debt crises. It was originally an internal Bridgewater study that informed the firm’s (very successful) trading of the 2008 crisis. The team examined 48 debt crises over the last century to develop an “archetype” or template showing how they unfold.

Lending Allows Spending

Like me (and many others throughout history), Ray recognizes that debt can be good or bad, depending on how it is used. He goes further with an important insight on the way debt is cyclical. He explains it so well I will quote him at length here (emphasis mine).

To put these complicated matters into very simple terms, you create a cycle virtually anytime you borrow money. Buying something you can’t afford [out of your capital or cash—JM] means spending more than you make. You’re not just borrowing from your lender; you are borrowing from your future self. Essentially, you are creating a time in the future in which you will need to spend less than you make so you can pay it back. The pattern of borrowing, spending more than you make, and then having to spend less than you make very quickly resembles a cycle. This is as true for a national economy as it is for an individual. Borrowing money sets a mechanical, predictable series of events into motion.

If you understand the game of Monopoly®, you can pretty well understand how credit cycles work on the level of a whole economy. Early in the game, people have a lot of cash and only a few properties, so it pays to convert your cash into property. As the game progresses and players acquire more and more houses and hotels, more and more cash is needed to pay the rents that are charged when you land on a property that has a lot of them. Some players are forced to sell their property at discounted prices to raise that cash. So early in the game, “property is king” and later in the game, “cash is king.” Those who play the game best understand how to hold the right mix of property and cash as the game progresses.

Now, let’s imagine how this Monopoly® game would work if we allowed the bank to make loans and take deposits. Players would be able to borrow money to buy property, and, rather than holding their cash idly, they would deposit it at the bank to earn interest, which in turn would provide the bank with more money to lend. Let’s also imagine that players in this game could buy and sell properties from each other on credit (i.e., by promising to pay back the money with interest at a later date). If Monopoly® were played this way, it would provide an almost perfect model for the way our economy operates. The amount of debt-financed spending on hotels would quickly grow to multiples of the amount of money in existence.

Down the road, the debtors who hold those hotels will become short on the cash they need to pay their rents and service their debt. The bank will also get into trouble as their depositors’ rising need for cash will cause them to withdraw it, even as more and more debtors are falling behind on their payments. If nothing is done to intervene, both banks and debtors will go broke and the economy will contract. Over time, as these cycles of expansion and contraction occur repeatedly, the conditions are created for a big, long-term debt crisis.

In other words, debt actually creates its own cycles. Lending (especially from institutions that can create money under a fractional reserve banking system) allows spending that spawns more spending, which eventually must reverse into contraction that spawns more contraction. That may seem obvious but we often forget it. As we apparently have done even as I write.

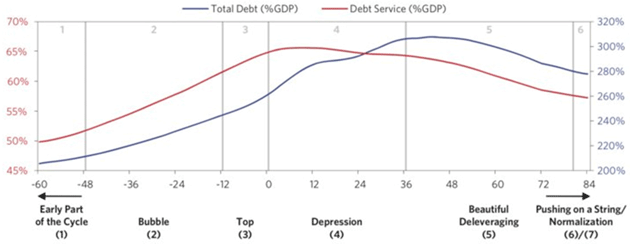

After examining dozens of debt cycles, Ray’s team built this template to describe the six stages of the deflationary variety.

Source: Ray Dalio

Stage 1 is the “good” part. People borrow money, but not too much and they use it for productive purposes. This helps the economy grow and lifts asset prices… which is where things start going wrong.

In Stage 2, which Dalio terms the “Bubble,” people look at the recent past and decide asset prices, total demand, and consumption will keep going up. They overconfidently borrow more money and start having too much leverage, although it is never possible to actually define the moment when the right amount becomes “too much.”

Stage 3, the “Top,” occurs when central banks and regulators and sometimes even the lending institutions themselves see problems and take steps to moderate growth—always thinking they can slow down without braking too hard. They raise interest rates, tighten lending standards, and so on.

Stage 4, ominously called the “Depression,” happens when growth slows or reverses beyond the ability of monetary and political authorities to help. Yet they keep trying. This is when we see interest rates go to zero or negative. The central bankers are out of bullets at this point. Everyone just has to suffer.

Stage 5 is the deleveraging phase, when businesses and families reduce spending to pay down debt and reduce their leverage. It can last a long time, but as leverage falls people get a handle on their debt service costs and slowly start to recover. Eventually the economy reaches Stage 6, normalization, and the cycle repeats.

Wealth Gap

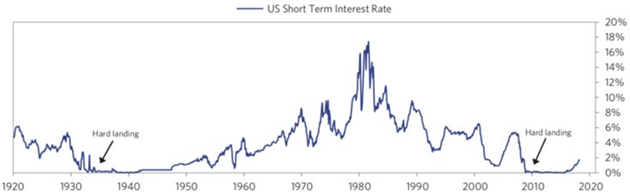

So that was the template for a generic debt crisis. Each one has its unique characteristics (he goes into each historical crisis separately in the last sections of his book) but they generally follow this sequence. Which raises the question, where are we now? Dalio thinks we are in the late stages and points to interest rates as evidence.

Source: Ray Dalio

Twice in this century, the US went through debt crises so severe that the Fed had to drop rates to zero and resort to unconventional policies like quantitative easing. The first time was in the 1930s and then again in 2008-2009. In both cases, it “worked” in the sense that asset prices recovered. But it also had adverse side effects because higher asset prices accrue to asset owners, which most people are not, at least to any significant degree.

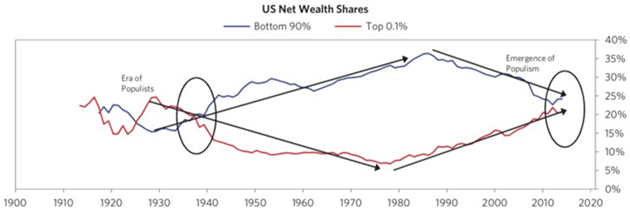

The result is a wealth gap between rich and poor, which of course always exists, but in these periods it grew too obvious to deny. A small part of society prospers as its assets gain value while the majority struggles. It happened in the Great Depression and we saw it again in the post-Great Recession years. Data-driven Dalio quantifies it in this chart.

Source: Ray Dalio

If that looks familiar, it’s because I’ve showed it and similar charts to you before. Ray originally posted it in a 2017 article which I summarized in a letter called The Distribution of Pain. His main point then was that it is a serious mistake to think you can understand “the” economy because we really have two economies. The top 40% live in a different world than the bottom 60%.

Combine those conditions of wealth inequality with representative democracy and the result is populism and our currently divided politics. It may become even more so now that Democrats will control the House next year. The result will be legislative gridlock, which isn’t entirely bad but may stall policy changes that could help postpone recession.

Already-huge federal deficits will therefore keep growing just as the Federal Reserve both raises rates and reduces its balance sheet assets. So far, this combination hasn’t stopped GDP growth or even perceptibly slowed it, but at some point it will. That is the goal, after all, and Ray’s template shows it usually succeeds.

In this case, I think the trigger will be a crowding-out effect as Treasury borrowing combined with Fed tightening raises household and corporate debt service costs. Everyone has a breaking point and it is getting closer.

The “seventh-inning stretch,” if you don’t know the term, is a point near the end of a baseball game. There’s enough time left for the trailing team to catch up so no one wants to leave yet. You stand up, stretch, singing “Take Me Out to the Ballgame,” then settle back in to see what happens.

That’s kind of where we are in the debt cycle: near the end, but not yet sure of the outcome. The difference is that none of us are just spectators. We are all in the game, and we will all either win or lose.

A Beautiful Deleveraging

Ray has been writing over the past few years about what he calls “A Beautiful Deleveraging,” when the central bank manages to defuse the debt-burdened economy without a major crisis. Here is what he says:

The key to handling debt crises well lies in policy makers’ knowing how to use their levers well and having the authority that they need to do so, knowing at what rate per year the burdens will have to be spread out, and who will benefit and who will suffer and in what degree, so that the political and other consequences are acceptable.

There are four types of levers that policy makers can pull to bring debt and debt service levels down relative to the income and cash flow levels that are required to service them:

1. Austerity (i.e., spending less)

2. Debt defaults/restructurings

3. The central bank “printing money” and making purchases (or providing guarantees)

4. Transfers of money and credit from those who have more than they need to those who have less.

1, 2, and 4 above require varying levels of pain for lenders and borrowers. Number 3 still has pain for all concerned, something like 2008-2014 when the Fed and other central banks around the world bought trillions in assets, but it was likely better than what would have happened absent those policies.

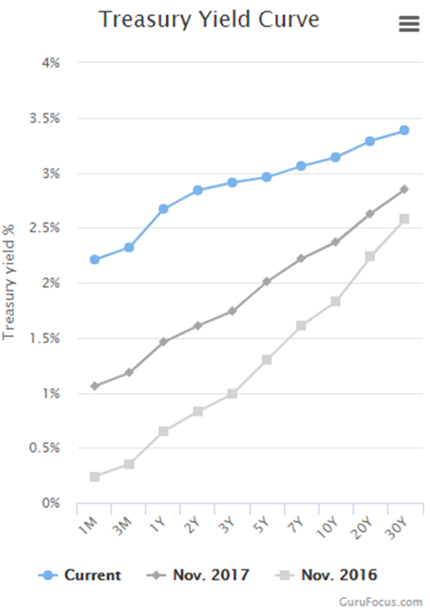

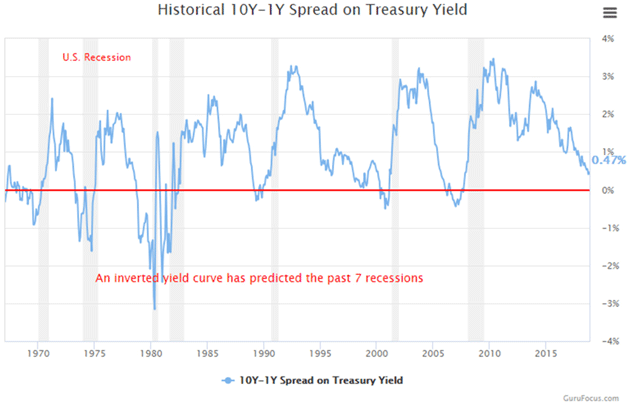

The Federal Reserve is late in the process of raising rates, but under Powell seems committed to reaching what many economists call “the natural rate of interest.” My personal belief is that we are close to that point now. If we go past it, then I think the Fed will tip the economy over into a recession. This will be preceded by an inverted yield curve, or the place where short-term government interest rates are higher than long-term US bond rates. Since World War II, this “inverted yield curve” has always preceded a recession by somewhere between 9 and 15 months.

This first chart from GuruFocus shows the yield curve has been “flattening” for the past few years. Below that, you see the historical yield curve spread since 1970. As they note in the chart, this preceded all of the previous seven recessions.

Source: GuruFocus

Source: GuruFocus

I want to be clear that an inverted yield curve does not cause recession. It is a symptom of imbalances in the banking and financial systems. Think of it like a fever brought on by a virus. The fever is a result, not the cause of the disease. It tells you something is wrong in your body.

Note that in the graphs above, short-term rates have risen roughly two percentage points while long-term rates rose around one point. We call this a “tightening” of the curve and it is the first step toward inversion. You can bet Fed officials are watching this, as they really don’t want the yield curve to invert. It will not surprise me if, even though they have signaled more rate increases, they actually stop short of their current targets. Another point higher at the short end would clearly invert the yield curve unless there is a similar rise in long rates, which has not been happening so far.

At that point, you are really going to wish that you had read Ray Dalio’s book. Next week we will dive deeper into the process. And just as important, why another credit crisis may happen before we have what I think of as The Great Reset. Stay tuned.

IRA Magic

On another note, I know someone with a high six-figure income who pays no income tax at all.

No, he doesn’t need to keep things quiet to stay out of jail. His situation is straight-forward, legal, and entirely on the up-and-up. And it started with something you probably think of as bland and conventional: an IRA.

Some years ago, my acquaintance began moving his entire financial life into his Individual Retirement Account. He wanted to put everything—his investments, his business, everything—in the IRA so profits could grow tax-free.

He didn’t get the job done overnight. It took time. But he kept at it because he could see how wonderful the result would be. And he used a Roth IRA, so that eventually the money would come out to him tax-free.

Now he lives in the no-tax zone. He doesn’t even need to file tax returns.

It really is possible to do that—not overnight, but in time—if you make it a priority. If you want to learn about the strategies that make it possible, I recommend Terry Coxon’s just-published special report, Supersize Your IRA. At $19.95 it’s not expensive and it comes with two free bonuses you will appreciate. Today is the last day it’s available. Terry has asked we close the offer tonight. You can learn more about the report and bonuses here.

The Joys of Traveling, Puerto Rico and Cleveland

I find myself tonight waiting in the Admirals Club in the “airplane lottery.” So far, I have had four flights canceled due to the planes not be able to get in or diverted from LaGuardia. In theory, a flight boards in 45 minutes. (Update: now two 3.5 hours, getting me home about 4:30 (??) am. Oh well, the glamour of travel and all.) That is the theory, we will see what happens in reality.

New York and the entire Northeast are in the middle of a serious snowstorm/blizzard. For the first time in my life, I walked out of the Liberty Tower in downtown New York to catch my Uber, and the snow was blowing from my left to my right. Not up and down or diagonally. I mean from my left to my right. I was soaked after walking 50 feet to the car.

Eventually, I will get back to Texas to start preparing for Thanksgiving with all my children and their families. Sometime in December, Shane and I will go to Puerto Rico and also visit Cleveland to see Dr. Mike Roizen for the Cleveland Clinic’s executive health program. And then the holidays come.

And with that, I will hit the send button. You have a great week. Spend some time with your friends and family, as unlike debt, you can never have too much time with friends.

Your excited-about-all-the-changes-that-are-coming-in-his-life analyst,

John Mauldin

© Mauldin Economics

www.mauldineconomics.com

© Mauldin Economics

Read more commentaries by Mauldin Economics