What Thanksgiving Cranberries and Bitcoin Have in Common

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

Football is as much a part of Thanksgiving as turkey and family are, and nearly as old as the holiday itself. It was President Abraham Lincoln who proclaimed Thanksgiving a national holiday in 1863, saying that he hoped all Americans would carve out some time to bless the “widows, orphans, mourners or sufferers in the lamentable civil strife in which we are unavoidably engaged.”

In 1876, a little more than a decade after the end of that “civil strife,” students from Yale and Princeton met in Hoboken, New Jersey, to play what is believed to be the first football game held on Thanksgiving Day. Yale ended up besting its fellow Ivy League competitor, two “goals” to zero.

At the time, “football” still more closely resembled rugby than the sport we enjoy today. But a tradition was born. On subsequent Thanksgivings, the Yale-Princeton matchups generated so much cash in ticket sales that they funded the two universities’ athletic programs for the rest of the year.

The model was such a success that the National Football League (NFL) made sure to carry on the tradition upon its founding in 1920. Professional football has been played on Turkey Day ever since, except for those in the years from 1941 to 1945.

The Cost of Thanksgiving Just Came Down for the Third Straight Year…

For most families, football comes second to the real Thanksgiving pastime—eating. But unlike ticket prices for an NFL game, which have gone up about 50 percent in the past 10 years, the cost of enjoying a Thanksgiving meal got slightly cheaper in 2018.

|

According to the American Farm Bureau Federation (AFBF), the cost of a typical Turkey Day feast for 10 people deflated about $0.22 from last year to $48.90. That’s the third straight year of declines, and the lowest level since 2010.

More affordable energy and an oversupply in the turkey market contributed to lower food prices, as did the trade dispute between the U.S. and China. You would think that tariffs on Chinese products would raise prices, but as the Wall Street Journal explains, “China’s retaliatory moves are having the opposite effect.”

“Tariffs on U.S. agricultural products have dampened Chinese demand, boosting supplies of some staples of the Thanksgiving table,” writes the WSJ’s Justin Lahart. Because of the supply glut, cranberry growers in particular have seen prices fall below the cost of production, estimated at $35 per barrel—which is bad for the farmers, obviously, but good for American consumers. As much as 25 percent of the U.S. supply of cranberries had to be dumped this season in order to support prices.

…But Christmas Continues to See Inflation

Cranberries are one thing, a partridge in a pear tree is another.

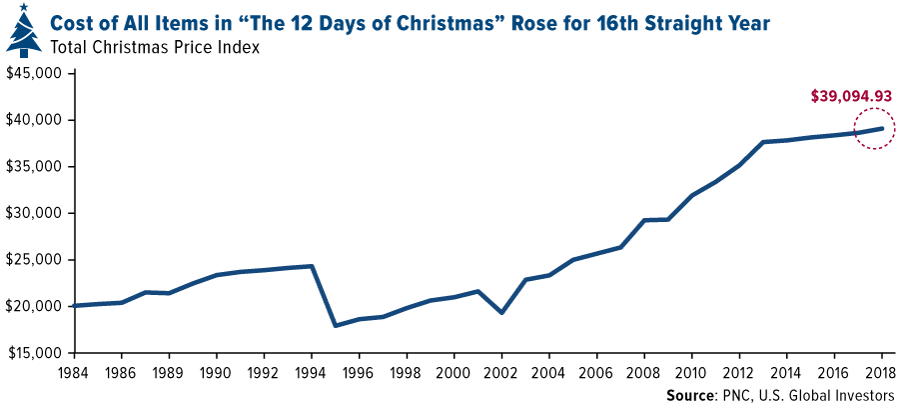

Every year for the past 35 years, PNC Financial Services has priced out all the items listed in the holiday song “The 12 Days of Christmas.” The cost of all 364 gifts, from turtle doves to pipers piping, rose 1.2 percent this year to $39,094.93. That’s almost double what the same items cost back in 1984.

Interestingly, just as the U.S. Bureau of Labor Statistics excludes food and energy from its “core” consumer price index (CPI) because they tend to be more volatile than the other items, PNC excludes the price of swans from its Christmas index for the very same reason.

The gift that rose the most from Christmas 2017 was the six geese a-laying. They’ll set you back $390 this year, 8.3 percent more than last year.

The gift that fell the most, meanwhile, was the five gold rings. They cost $750, down 9.1 percent from $825 in 2017. That’s good news for jewelers such as newcomer Menè, which prices its merchandise based on the gold and platinum weight value.

Bitcoin Miners Await a Recovery in Prices

Like the cranberry growers, many bitcoin miners are choosing to limit supply as prices right now are lower than operating costs. Bitcoin fell below $5,000 on Monday and was trading around $4,250 on Friday, levels we haven’t seen in over a year. The average of mining a single bitcoin, meanwhile, is estimated to be between $6,000 and $7,000, meaning miners are operating at a loss.

The global bitcoin hash rate, therefore, is rolling over as smaller miners shut down rigs and await a recovery in prices. The hash rate, which measures how much power the bitcoin network is consuming, is now at August levels. It’s worth pointing out, though, that the rate is still up sharply this year, even as the world’s largest cryptocurrency has struggled to find the momentum that carried it to nearly $20,000 last December.

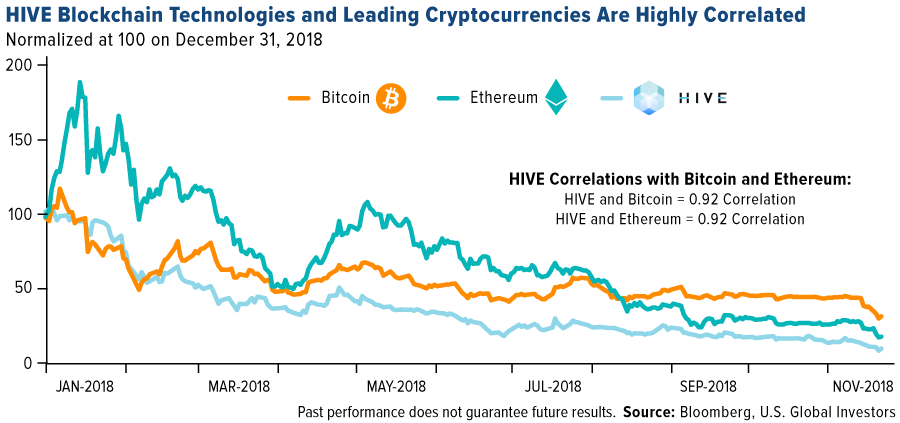

This should be good news for the bigger players in the industry, most notably HIVE Blockchain Technologies, since they’ll control a larger share of the market.

Vancouver-based HIVE, the first publicly listed blockchain infrastructure company, is a pure play blockchain and Ethereum investment for the capital markets. As such, many investors trade HIVE as an easy proxy for those digital coins. In the chart above, you can see that its share price shares a very strong correlation with both bitcoin and Ethereum. For 2018, HIVE had a correlation coefficient of 0.92 with those two coins. A correlation of 1.0 would mean that the two assets trade perfectly in sync. When cryptocurrencies begin to recovery, then, it seems logical to expect that HIVE would follow suit.

Gold Market

This week spot gold closed at $1,223.21, up $1.71 per ounce, or 0.14 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 0.08 percent. The S&P/TSX Venture Index came in off 3.64 percent. The U.S. Trade-Weighted Dollar rose 0.50 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-20 | Housing Starts | 1228k | 1228k | 1210k |

| Nov-21 | Durable Goods Orders | -2.6% | -4.4% | 0.7% |

| Nov-21 | Initial Jobless Claims | 215k | 224k | 221k |

| Nov-26 | Hong Kong Exports YoY | 9.5% | -- | 4.5% |

| Nov-27 | Conf. Board Consumer Confidence | 135.7 | -- | 137.9 |

| Nov-28 | GDP Annualized QoQ | 3.6% | -- | 3.5% |

| Nov-28 | New Home Sales | 582k | -- | 553k |

| Nov-29 | Germany CPI YoY | 2.3% | -- | 2.5% |

| Nov-29 | Initial Jobless Claims | 220k | -- | 224k |

| Nov-30 | Eurozone CPI Core YoY | 1.1% | -- | 1.1% |

Strengths

- The best performing metal this week was gold, up 0.14 percent. The Bloomberg Intelligence Global Senior Gold Valuation Peers Index is heading for a fourth straight gain to mark the longest rally since September. The index posted its first monthly gain in seven months in October as investors are giving gold equities a second look now. Bloomberg’s Susanne Barton writes that gold equities are benefitting as investors bet that signs of a cooling global economy might mean gold prices have finally reached a bottom.

- The stock market faced some of its worst days in years this week. On Tuesday, the S&P 500 Index erased all of its gains for 2018, oil fell to a one-year low and bitcoin has been in freefall. Amid this turmoil, traditional safe haven assets such as Treasuries, the yen and gold stood still. On Monday, gold actually gained slightly, demonstrating its ability to hold up against stock market volatility.

- Bloomberg reports that holdings in ETFs backed by gold climbed to a 14-week high this week. The money plowed into ETFs on Monday after gold futures posted their biggest weekly gain in more than a month. Since this rate-hiking cycle started back in late 2015, holdings in gold ETFs have climbed 50 percent while the metal price is up 15 percent. Central banks, too, are buying up the yellow metal. Russia boosted its gold holdings in October to 66.4 million troy ounces, valued at $81.1 billion, up from $77.5 billion in September. Kazakhstan also increased its holdings in October to 10.97 million ounces, up from 10.77 million the prior month. Turkey, which has been selling their gold for six months, appears to have increased its holdings last month to 15.16 million ounces. Lastly, Malaysia added to its bullion stores for the first time since January 2017, to bring holdings up to 1.25 million ounces, the highest level since 1999.

Weaknesses

- The worst performing metal this week was palladium, down 4.46 percent with a slide removing much of last week’s surge. UBS writes that gold positioning turned net short again after a four-week breather. Data shows that gold shorts re-established positions, accounting for the bulk of the selling.

- The civil lawsuit accusing JPMorgan of manipulating the precious metals market might be in for more delays. The Justice Department has asked a judge to halt the proceedings in the lawsuit filed in 2015 by a hedge fund manager and two commodity traders. They are asking for a six-month delay, citing an ongoing criminal case as the reason for the request, according to court filings. Last month a former JPMorgan trader pleaded guilty in Connecticut to manipulation charges, writes CNBC.

- London’s gold market is not as big as some thought. Last week London Bullion Market Association data showed that an average of $36.9 billion of gold changed hands in London’s over-the-counter market. Previous estimates from the World Gold Council (WGC) were between three and six times higher, using 2016 data. Bloomberg writes that while the data was only for a single week, it does demonstrate that the Comex futures market in New York is in fact a bigger venue for gold than London. However, more gold was traded in London than was traded on the FAANG stocks – Facebook, Apple, Amazing, Netflix and Alphabet. Bloomberg writes that almost $37 billion of gold was traded on average last week, which is 27 percent more than the volume for the largest technology stocks.

Opportunities

- President Donald Trump continued to call for the Federal Reserve to lower interest rates, describing the central bank as a “problem.” This criticism comes during a week when stocks stumbled on concerns ranging from slower global growth to an expanded trade war. However, MNI reports that the Fed might actually be considering a pause to its gradual monetary tightening and could end its cycle of interest rate hikes as early as next spring. Lower interest rates could be a tailwind for the gold price.

- Citigroup estimates that the U.S. dollar will weaken next year as the economic boost from fiscal policy wanes and rising interest rates will begin to hurt. One analyst wrote that “our view is that the fiscal support to growth eventually fades in the U.S. and tighter monetary policy starts to bite.” Goldman Sachs also sees the dollar declining in 2019 as the U.S. growth boom “catches down” to the moderate pace of expansion in the rest of the world. Gold historically moves in the opposite direction of the dollar. The bank also says it might be wise to dial back on risk and boost cash positions. Goldman strategists led by David Kostin wrote in a report that “cash will represent a competitive asset class to stocks for the first time in many years.”

- Ray Dalio, founder of Bridgewater Associates, sees parallels in the financial markets today to the 1930s of being in the late stages of a short-term business cycle, given that the Fed is tightening monetary policy. Dalio said “the role of the U.S. dollar will diminish, and the returns on U.S. dollar-denominated debt will suffer.” The billionaire investor recommends that investors consider placing 5 to 10 percent of their assets in gold as a hedge against political risks.

Threats

- Investors withdrew $3.9 billion from macro hedge funds in October, with macro funds falling an average of 1.7 percent on an asset-weighted basis. Overall the hedge fund industry saw $7.1 billion of outflows in October, bringing total redemptions for the year to around $10.1 billion, writes Bloomberg. For the first time since 2008, high-yield and investment-grade notes in both euros and dollars are headed for negative returns at the same time, based on Bloomberg Barclay’s indexes. Credit markets are set for their worst year since the global financial crisis and Marco Stoeckle, head of corporate credit strategy at Commerzbank AG said that “most people have buried hopes for a year-end rally.”

- Proposed changes to the Mexican Mining Code hit the share prices of those companies with operations in the country. Some of the latest proposals center around mining concessions that impact indigenous areas and their environmental and social impact. While it is still too early to know how these proposals will play out, investors immediately placed a higher discount on these companies.

- The Organization of Petroleum Exporting Countries (OPEC) could be facing a big challenge next year as Permian producers expect to iron out distribution problems that will add three pipelines and as much as two million barrels of oil a day, writes Bloomberg. Javier Blas writes that “if Saudi Arabia and its allies cut production to keep prices higher, shale will thrive, robbing them of market share. But because the Saudis need higher crude prices to make money than U.S. producers, OPEC can’t afford to let prices fall.”

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 4.44 percent. The S&P 500 Stock Index fell 3.79 percent, while the Nasdaq Composite fell 4.26 percent. The Russell 2000 small capitalization index 2.54 percent this week.

- The Hang Seng Composite lost 1.01 percent this week, while the KOSPI fell 1.67 percent.

- The 10-year Treasury bond yield fell 2 basis points to 0.49 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector this week relative to the other sectors, down 1.35 versus an overall decrease of 3.33 percent for the S&P 500 Index.

- Rockwell Collins was the best performing stock for the week, increasing 7.02 percent.

- Agilent Technologies’ stock surged this week after reporting better-than-expected earnings in the fourth quarter. Net income rose 21 percent to $0.81 per share, higher than the average analysts’ estimate of $0.73 per share. Agilent CEO Mike McMullen said, “Our performance this quarter caps off an excellent 2018 as we achieved our highest annual core growth rate and profitability since becoming a stand-alone life sciences company in 2014.”

Weaknesses

- Information Technology was the worst performing sector for the week, decreasing 6.08 percent versus an overall decrease of 3.33 percent for the S&P 500.

- Ross Stores was the worst performing stock for the week, falling 15.65 percent.

- Wall Street erased stocks' gains for the year Tuesday, reports Business Insider, as some of the biggest technology companies fell into a bear market, adding to fears about slowing growth and trade tensions.

Opportunities

- Best Buy, bucking the retail rout, rose after topping earnings, revenue and sales estimates in the third quarter.

- Andrew Left of Citron Research says he is bullish on Nio, the so-called Tesla of China, reports Business Insider. In a note on Monday, he said the electric-car company's shares had "little resistance" on their way to rallying to $12, a jump of about 60 percent.

- Microsoft announced this week its acquisition of FSLogix, for an unknown sum. Brad Anderson, corporate vice president at Office 365, and Julia White, corporate vice president at Microsoft Azure, said that FSLogix's technology would enable faster load times for user profiles in Outlook and OneDrive. This would lead to improved overall Office 365 performance in "multi-user virtual environments," according to a Microsoft blog post.

Threats

- FANG stocks—Facebook, Amazon, Apple, Netflix (and Google-parent company Alphabet)—fell further into bear market territory on Monday. From their June highs, FANG stocks dropped more than 20 percent this week. Alphabet's fall marked the company’s first bear market in seven years.

- Target dropped more than 11 percent after reporting weaker-than-expected quarterly earnings and same-store sales ahead of the holiday season, reports CNBC.

- According to Bank of America Merrill Lynch, the turmoil in markets has only just begun. The CBOE Volatility Index, known for its gauge of market unrest, and its relationship with Treasury yields, is one that the bank has tracked since the mid-2000s. BAML examined the VIX and the yield curve, which displays the gap between shorter-term, two-year Treasury yields and longer-term, 10-year yields, reports Business Insider. This spread narrowed to nearly zero earlier this year (as the yield curve flattened). "A flattening yield curve signaled a withdrawal of liquidity and over the last three cycles has preceded rising volatility by a few years," Savita Subramanian, BAML's head of U.S. equity and quant strategy, said in a note. According to Subramanian, the VIX should double through 2021.

The Economy and Bond Market

Strengths

- U.S. housing starts in October rose amid a rebound in multifamily housing projects, reports Reuters. Housing starts increased 1.5 percent to a seasonally adjusted annual rate of 1.228 million units last month.

- The Federal Reserve may soon change its communications to ensure future rate hikes are accompanied by a more cautious approach, according to Morgan Stanley. "What used to be hawkish rate hikes may turn into dovish hikes," strategists led by Hans Redeker wrote. They see just two increases next year, half the number anticipated by Goldman and JPMorgan. Speculation that the Fed will pause hiking rates after December’s meeting has sent the 10-year Treasury yield to its lowest level since mid-September.

- Data for Wednesday and Thanksgiving (Thursday) sales suggests holiday-season spending could come in well ahead of 2017. According to Adobe Analytics, shoppers spent $2.4 billion online on Wednesday, a 31.8 percent increase over last year. Through 5:00 P.M. Thanksgiving Day, top online retailers saw $1.75 billion in sales, up 28.6 percent from the year earlier. This weekend marks the busiest shopping season of the year, with an estimated 164 million consumers planning to shop over the five-day Thanksgiving period, according to the National Retail Federation (NRF). “Compared to older generations, younger consumers under the age of 35 are more likely to be attracted by the social aspects of shopping over the weekend or by the fact that it is a family tradition,” commented Prosper Insights Executive Vice President of Strategy Phil Rist.

Weaknesses

- A decline in orders for long-lasting factory goods in October suggests business investment is softening, a discouraging sign for economic growth in the fourth quarter. Orders for durable goods decreased 4.4 percent from the prior month in October, the Commerce Department said Wednesday. That was the biggest monthly decline in new orders since July 2017, and it was much steeper than the 2.6 percent drop Wall Street analysts had expected.

- Initial jobless claims in the U.S. rose to more than a four-month high last week, increasing by 3,000 to a seasonally adjusted 224,000 for the week ended November 17, the highest level since the end of June, the Labor Department said on Wednesday.

- Consumer sentiment for November fell more than anticipated in the final reading of the month, although the index remained near record highs. The University of Michigan’s monthly survey of consumers slipped to 97.5 in the final November reading, more than the fall to 98.3 expected by economists surveyed by Refinitiv.

Opportunities

- The next release of third quarter gross domestic product (GDP) will be released next Wednesday. The reading is forecasted at 3.6 percent, higher than the previous 3.5 percent estimate.

- Personal income has been on an uptrend. Next Thursday’s release is forecasted to show growth of 0.4 percent, accelerating from the previous release of 0.2 percent.

- The Chicago PMI survey next Friday is forecasted at 58.5, reflecting high levels of economic activity.

Threats

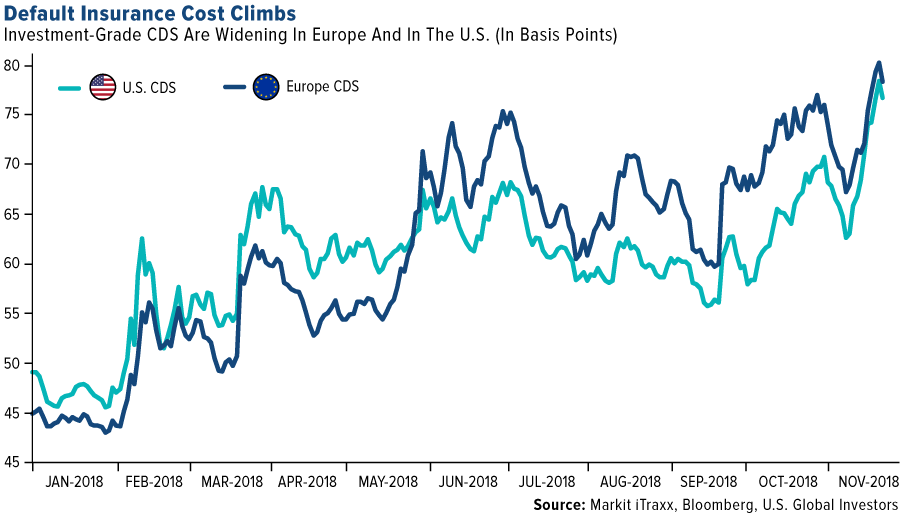

- Credit is suffering as global volatility prompts investors to seek safety after years of riding market wide gains, reports Bloomberg. “The cost of insuring investment-grade debt is set for the biggest annual increase since 2011 in both Europe and the U.S.,” the article reads. This data is based on Markit iTraxx indexes of credit-default swaps. Growing investor wariness is reflected in higher costs as the global economy cools and central banks tighten monetary policy after years of easing.

- Consumer confidence took a hit this week with a softer reading on the University of Michigan Sentiment survey. Next week’s release of the Conference Board’s Consumer Confidence survey is likely to confirm the moderating consumer sentiment ahead of the holiday shopping season.

- American farmers are struggling to find storage for their crops as exports slow and U.S. tariffs take their toll, reports CNBC. The trade war between Washington and Beijing is forcing some farmers to bury their harvest under soil, and the problem is most acute for soybean growers, Reuters reported.

Energy and Natural Resources Market

Strengths

- Natural gas was the best performing major commodity this week rising 4.5 percent. The commodity rose for a fourth straight week driven by forecasts for a lingering autumn chill in the eastern half of the country through early December.

- The best performing sector this week was the NYSE Arca Gold Miners Index. The index rose 0.3 percent as physical gold holdings in ETFs backed by the metal ticked up to the highest since August 6.

- The best performing stock for the week was Saras. The Italian crude oil refiner rose 6.5 percent as investors expect greater realized prices after French giant Total is forced to reduce output from its Gonfreville-Normandy and Grandpuits refineries due to a labor strike.

Weaknesses

- Crude oil was the worst performing commodity this week. The commodity dropped 9 percent, the seventh straight week of declines, after Saudi Arabia’s energy minister Khalid Al-Falih said his country has raised crude oil output to near record production volumes.

- The worst performing sector this week was metals and mining. The group dropped 6.9 percent with base metals prices retreating amid reports that the U.S. has been on a campaign to get foreign allies to stop using equipment made by Chinese telecoms – reigniting fears that the trade war rhetoric may continue to escalate.

- The worst performing stock for the week was Southern Copper. The major copper producer dropped 15.1 percent to a 52-week low on increased uncertainty in Mexico’s mining sector. Mexico’s new Congress is set to consider new bills and resolutions regarding indigenous communities and the environment could create a “perfect storm” for miners operating in the country.

Opportunities

- President Donald Trump and Chinese leader Xi Jinping signal readiness for trade talks ahead of the G-20 meeting. The world’s biggest economies are set to meet in Argentina next week to discuss trade, bringing hopes that a resolution may be near. Both Trump and Xi appeared optimistic about the talks, with Trump maintaining his aggressive stance telling reporters that China wants to make a deal “very badly” after his administration placed additional tariffs on some $200 billion worth of Chinese goods.

- Goldman Sachs expects a broad fall in the U.S. dollar next year as U.S. economic growth slows to be more in line with the global average. Goldman said the view meant it had revised its long-standing bearish view on other currencies, and expects commodity-dependent currencies such as the Canadian and Australian dollar to recover.

- India’s oil imports hit a seven-year high in October. India imported 21.02 million tons of crude last month, the highest number in at least seven years and a 10.5 percent increase from October 2017. The increase followed the end of maintenance season at many refineries, with demand for fuels still healthy despite rising prices at the pump.

Threats

- Oil slumped to a one-year low after the Saudis signaled record output. Saudi Arabia signaled its crude oil output may have reached record highs, while U.S. stockpiles crept higher stoking concerns over a potential supply glut.

- JPMorgan cut its oil price outlook for 2019. The head of the bank’s Asia-Pacific oil and gas operations, Scott Darling, said analysts had factored in the increase in supply in North America that will occur in the second half of 2019 and will eventually pressure prices even lower in 2020.

- Major European purchasing manager’s index (PMI) data flags growth concerns in the region. The flash Eurozone Manufacturing PMI fell to a five-year low, reflecting slowing order books growth and a drop in exports.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 2.4 percent. Strong economic data supported equites trading at the Warsaw Exchange this week. Poland recorded a pick up in retail sales, construction output and gross wages. Employment in Polish companies increased 3.2 percent year-over-year. The economy grew 5.1 percent in the third quarter of this year.

- The Turkish lira was the best performing currency this week, gaining 90 basis points against the dollar. Berat Albayrak, Turkey’s treasury and finance minister, said that the country might not need additional lira borrowing this year. Turkey’s consumer confidence rose to 59.6 in November, from 57.3 reading in the prior month.

- Information technology was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 3.8 percent. The Central Bank of Greece announced the proposal for the management of non-performing loan exposure (NPEs), which should allow for a reduction in the NPE ratios to single digits within two to three years.

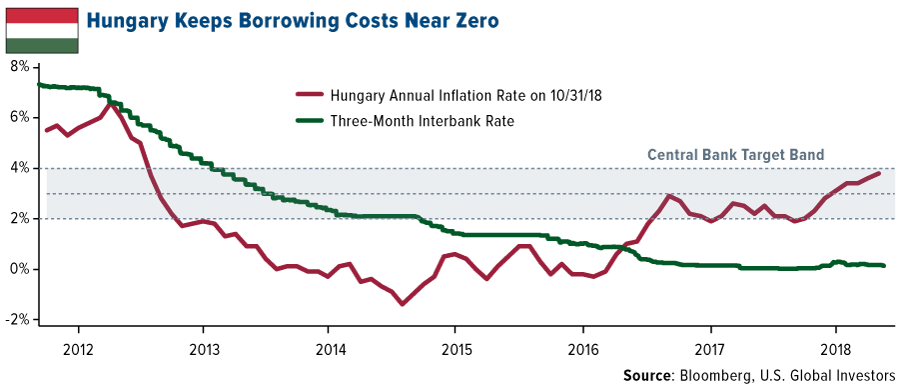

- The Hungarian forint was the worst performing currency this week, losing 94 basis points against the dollar. Its central bank stated that loose monetary policy is necessary to bring inflation up to its target of 3 percent.

- Industrials was the worst performing sector among Eastern European markets this week.

Opportunities

- Hungary’s central bank said loose financial conditions were still needed to sustainably reach its inflation target, even as prices rose at their fastest pace in almost six years. The central bank left its main interest rate unchanged at 90 basis points, and the overnight deposit rate at minus 15 basis points. Hungary’s dovish stance contrasts with multiple hikes this year in the Czech Republic and Romania. A dovish central bank stance should support equites trading on Budapest exchange.

- France and Germany have agreed to press ahead with plans for a eurozone budget, which could be in place by 2021. It would be part of the seven-year-long budget upon which all member states would have to agree. Only the 19 eurozone members would be able to utilize it, however. France’s Bruno Le Maire said that the budget would help “promote greater convergence” and “have a stabilization function” that can absorb sudden economic shocks.

- Poland indicated its desire to get more energy from nuclear reactors. It plans to build six to nine gigawatts of nuclear power generation by 2043, with the first one to five gigawatt units completed in 2033. This investment will be worth more than $100 billion, and it will provide clean energy in a country still dependent on coal.

Threats

- If an escalation of the U.S.-China trade dispute triggers a major global risk off environment, currencies from Turkey, South Africa, Mexico, Chile, Philippines, Argentina, Hungary and Poland could drop at least 20 percent, Wells Fargo says. Counties with higher current-account deficits, low real rates, low short-term coverage and political risk are the most vulnerable under that extreme scenario.

- Poland on Tuesday said that it would not support the global migration pact. The pact, according to Poland, fails to meet its demands regarding the confirmation of adequately strong guarantees of the sovereign right to decide whom the countries accept in their territory and the distinction between legal and illegal migration, according to Bloomberg. Hungary withdrew in July, and Austria in October, with Czech Republic and Bulgaria expressing their reservations. Europe has been divided over migration law, and the countries’ differences on migration policies are becoming more visible.

- The eurozone’s confidence data has been weakening since the January peak of 116.2. Next week the downtrend may continue as the economy is expected to slow down over trade discussions, Italian debt and Brexit noise.

China Region

Strengths

- The Philippines had a strong week, jumping 3.64 percent over the last five trading days. Vietnam was another place to be, with the Ho Chi Minh Stock Index climbing by 2.20 percent for the week.

- Utilities was the top-performing sector for the week, rising 64 basis points even as most sectors were red during that time.

- Industrial production in Taiwan came in better than expected for the October measurement cycle, reading an 8.25 percent year-over-year gain versus a 3.55 percent expectation by analysts.

Weaknesses

- The Shanghai Composite dropped 3.72 percent over the course of the last week, outpacing its regional peer indices to the downside.

- The Hang Seng Composite’s energy sector was the worst-performing one for the week, falling 3.02 percent and keeping declining oil prices company.

- Thailand’s third quarter gross domestic product (GDP) clocked in at only 3.3 percent, down significantly from the prior reading of 4.6 percent and well below the surveyed expectation consensus for 4.2 percent.

Opportunities

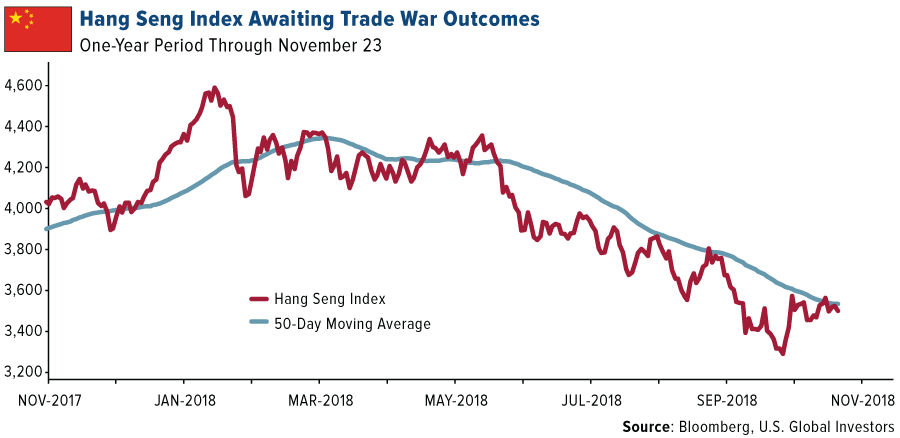

- Despite all the hullabaloo surrounding trade and uncertainty, it remains worth remembering that regional indices like the Hang Sang Composite have already fallen something like 24.5 percent or so from the peaks reached earlier this year amid some broader concerns of trade wars and slowdowns. While we’ve discussed the relative attractiveness of some markets with low price/earnings ratios and reasonably high dividend outlooks in the past, we would call particular attention to markets like Hong Kong’s, which has lifted off its recent lows and seems to be awaiting more direction following trade war outcomes and better understanding of the broader global economic situation. Note the HSCI’s chart for the past 52 weeks.

- President Donald Trump and Chinese leader Xi Jinping remain on course to meet and discuss trade at next week’s upcoming G-20 conference. The meeting, while already downplayed in terms of potential details forthcoming, could possibly and nonetheless provide some momentum for U.S.-China trade talks and possibly indicate some thaw in the recently-cooled relations between the two economic juggernauts. On the principle that some talks are better than no talks, and in keeping with the “warmer” and “fuzzier” headlines (if you will) and outlook over the past week as we head into the meetings, there seems to be some possible opportunity for a truce or thaw.

- China and the Philippines continued to build rapport amidst their disagreements over certain issues as Xi Jinping traveled to Manila for the first state visit to the Southeast Asian island nation in some 13 years.

Threats

- Taiwanese elections this weekend should bring more clarity to the issue of whether or not the island will seek to shift its formal Olympic registry to “Taiwan” from “Chinese Taipei,” a move possibly symbolic and minor but, as always, highly sensitive and a possible sticking point. Free bonus: Several recent global elections and referenda have provided all sorts of interesting and indeed, intriguing results and trends. Stay tuned, election watchers!

- Foxconn took a significant hit this week as that major supplier to Apple indicated weaker demand going forward than analysts expected. Read-throughs are obviously negative, and the company is reportedly slashing expenses for the upcoming year.

- Trade war concerns remain elevated, and as opportunistic and “warm and fuzzy” as the upcoming G-20 meeting between Trump and Xi may be, there remain risks as well.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended November 23 was Veros, up 9,000 percent.

- Switzerland’s main stock exchange has approved the first exchange-traded product (ETP) tracking various cryptocurrencies, reports Seeking Alpha. The ETP, which is called the Amun Crypto ETF, will be invested in bitcoin, Ripple, Ether, Bitcoin Cash and Litecoin, the article continues. Trading will begin next week.

- As part of a broader push to spur blockchain development, the IBM Blockchain Accelerator and Columbia Blockchain Launch Accelerator were announced on Monday, reports Coindesk. The collaboration between the technology giant and the university will support 10 startups each, with hopes of supplementing early-stage companies with the required technologies and social networks to grow their businesses, according the David Post, IBM Blockchain Accelerator managing director.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended November 23 was StarChain, down 35.63 percent.

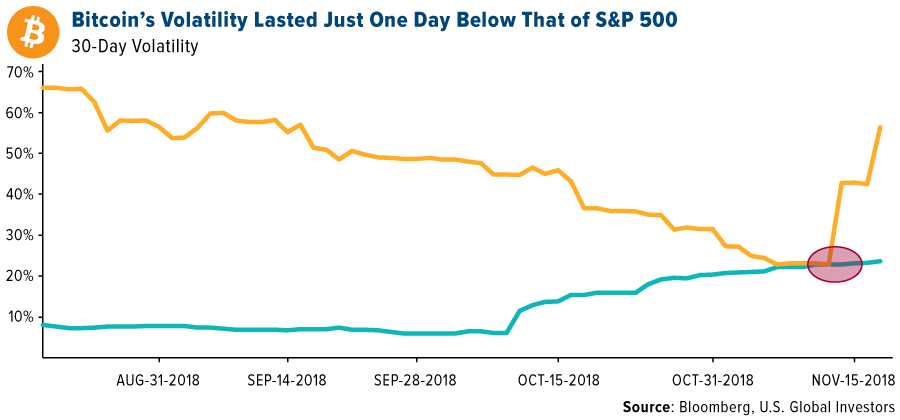

- Bitcoin dropped to its lowest level since October 2017 at the start of the week, reports Bloomberg, with other alternative coins slumping as well. The popular digital currency fell past the crucial $6,000 level last week, and reached $5,165 on Monday. After slowly becoming less volatile throughout the year, bitcoin’s volatility shot up this week after briefly being lower than that of the S&P 500. As of Wednesday bitcoin’s price was hovering just above $4,000, down 40 percent for the month and down almost 80 percent since December.

- Hong Kong-based OKEX, a cryptocurrency exchange that handles more than $1 billion in trades daily, forced the early settlement of its Bitcoin Cash contracts without warning last Wednesday. One trader who spoke with Bloomberg said the move “might not be illegal, but it is very unusual.” The move, intended to protect investors from the volatility associated with the Bitcoin Cash split, blindsided traders and has added to the number cryptocurrency exchange controversies in the last year.

Opportunities

- A new bitcoin index launched on Tuesday geared toward institutional investors. The MVIS Bitcoin US OTC Spot Index (MVBTCO), launched by MV Index Solutions (MIVS), which is a subsidiary of VacnEck, is said to be the first that tracks the performance of bitcoin on selected over-the-counter platforms in the U.S. Gabor Gurbacs, director of digital asset strategies at VanEck and MVIS said “the index may pave the way for institutionally oriented products, such as ETFs.”

- Nigel Green, founder and chief executive of U.K. consulting firm deVere group, thinks the three-day decline in cryptocurrencies is a bargain that investors don’t want to miss, reports MarketWatch. “Savvy investors understand that digital currencies are the future of money and, as such, they will be capitalizing on the lower prices in order to build their portfolios and shore-up their positions,” Green said. He believes this selloff has fueled unnecessary criticism of the technology, the article continues.

- Boeing announced a collaboration with Spark Cognition to form a joint venture called SkyGrid, which will focus on urban aerial mobility use cases and leverage blockchain, artificial intelligence, data analytics and cybersecurity applications. This move represents a growing number of companies utilizing blockchain to develop new technologies.

Threats

- According to one study, bitcoin as a payment system fell somewhat out of favor in 2018. Citing data from blockchain research firm Chainalysis, Reuters reports that the “value of bitcoins handled by major payment processors shriveled nearly 80 percent in the year to September.” This suggests that the world’s largest digital currency is still struggling to mature past a speculative asset and become a widely accepted method of transaction.

- The U.S. Justice Department is investigating whether last year’s epic cryptocurrency rally was fueled in part by manipulation, reports Bloomberg, as the price of bitcoin plummets over recent days. The speculation comes from whether or not traders drove up the price with Tether, a popular but controversial digital token. A broad criminal probe was opened up by federal prosecutors months ago, but they have recently homed in “on suspicions that a tangled web involving Bitcoin, Tether and crypto exchange Bitfinex might have been used to illegally move prices,” the article continues.

- Bitcoin mining company Giga Watt filed for Chapter 11 bankruptcy on Monday, revealing that it owes its largest creditors nearly $7 million. According to the court documents, the firm has estimated assets worth less than $50,000 and liabilities are in the range of $10-$50 million, writes CoinDesk. Giga Watt held an initial coin offering last May that raised around $22 million in cryptocurrencies at the time, then in January it was sued by a group of plaintiffs for allegedly conducting an unregistered securities offering.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All