Gear Up for Lower Gear

The global economy looks set to move into a lower gear as both advanced and emerging economies will find it hard to extend their recent robust economic performance into 2019.

The temporary (90-day) truce between the U.S. and China is a positive outcome for those directly or indirectly affected by the tit-for-tat protectionist moves. Yet the possibility of renewed escalation remains high. We expect the Trump administration to eventually hike the tariff rates to 25% on $200 billion worth of Chinese imports.

Oil has been in the news over the past few weeks. The commodity has witnessed a dramatic sell-off thanks to sanction exemptions to Iran’s biggest customers, rising uncertainty about global demand and the soaring U.S. shale supply. Lower oil prices, if sustained, could boost consumers’ purchasing power. It also could pose challenges for those central banks already struggling to achieve their inflation objectives. Oil producers will try to rebalance the market by reducing output.

Overall, we don’t think this imminent slowdown will snowball into something more serious. But there is a long list of downside risks.

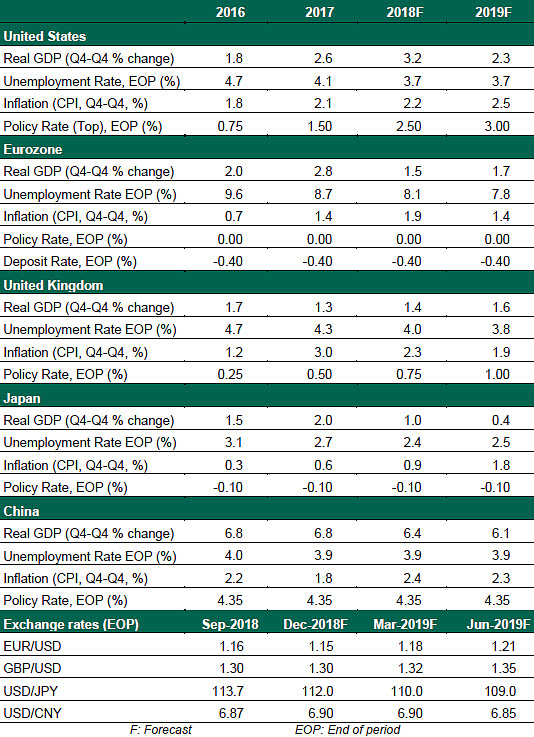

United States

- U.S. gross domestic product (GDP) growth for the third quarter was confirmed at a 3.5% annualized rate. The last revision included encouraging growth in business investment, a soft spot in the initial estimate, offset by a reduction in consumer spending. A strong holiday shopping season will support the fourth quarter, and we forecast full-year growth of more than 3%.

- Although Federal Reserve Chair Jerome Powell has downplayed the importance of forward guidance, the market has been attuned to Fed statements. Powell’s most recent characterization that the Fed funds rate was “just below neutral” was interpreted as a signal that rate increases will soon end, boosting risk appetites. We expect to see a rate increase following the Federal Open Market Committee meeting on December 19, followed by two hikes in 2019.

- Labor markets remain resilient, with the unemployment rate holding at 3.7%. The prime-age (25 to 54) labor force participation rate remains below the peaks observed in past growth cycles, suggesting some slack remains in the labor market.