The fourth quarter has been hectic for equity, fixed income and energy markets. On any volatile day, market observers look for a root cause. We have seen both blame and praise placed on Federal Reserve commentary, presidential tweets and trade proclamations. The signals are getting harder to separate from the noise.

Amid all this, the economy remains fundamentally sound. Growth continues, employment is still strong and wages are rising. Consumers are confident and enjoying a momentary gain from lower oil prices, supporting holiday spending. As the year reaches its end, we look back on a year of outsized growth and anticipate a reversion to more typical cyclical progressions.

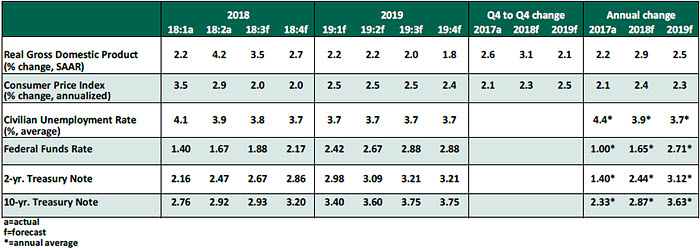

Key Economic Indicators

Influences on the Forecast

-

- The unemployment rate has held at a very low rate of 3.7% for three consecutive months. Job growth continues, but in a more moderate way: the November payroll gain of 155,000 jobs was slightly slower than anticipated, and was accompanied by downward revisions to past months. The labor force has had sufficient slack to provide workers on the margin to fill newly created jobs.

- The prolonged decline in worldwide oil prices surprised the market throughout November. The price of a barrel of West Texas Intermediate crude oil peaked at $76 on October 3 and has since fallen as low as $50. Ample global supply has exceeded demand. OPEC’s recent announcement of reduced production will set the foundation for an upturn in prices.

- The reduction in oil prices will cool the pace of inflation in the near term. The Consumer Price Index grew by 2.5% year-over-year in October, poised to fall in November. The core personal consumption expenditure (PCE) price index, which excludes food and energy, was revised down to 1.5% in the third quarter, suggesting soft inflation is not solely due to an energy dividend.

- A statement by Federal Reserve Chair Jerome Powell that the Fed Funds rate is “just below neutral” was interpreted as a dovish statement and a meaningful reduction in the outlook for future rate increases. The statement sparked a short-lived equity market rally. But whether we are “a long way from” or “just below” neutral, rates will only move upward. A rate increase following the December 18-19 meeting seems certain, with two more increases in 2019 ending this rate cycle at a neutral level.

- The inflation-adjusted gross domestic product (GDP) growth for the third quarter was affirmed at 3.5%. In the second revision, business investment was revised upward to a rate of 2.5%, improving on a slow initial estimate. Consumer expenditures were revised down slightly but remain elevated. We anticipate more typical economic growth rates in 2019 as the cost of trade actions becomes apparent and stimulus measures run their course.

- Corporate profits in the third quarter were estimated to have grown by 10.3% before tax, a strong return to capital. Higher costs, such as from higher wages and new tariffs, are not yet shrinking profit margins.

- At November’s G-20 meeting, a brief détente was agreed between the U.S. and China, with the U.S. committing not to raise tariffs to 25% from 10% on $200 billion of imported goods. Both sides will gain from finding common ground, and we hold out hope for a resolution to the trade dispute in the year ahead.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2018 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust