Christmas Comes Early for This Precious Metals Streaming Company

Membership required

Membership is now required to use this feature. To learn more:

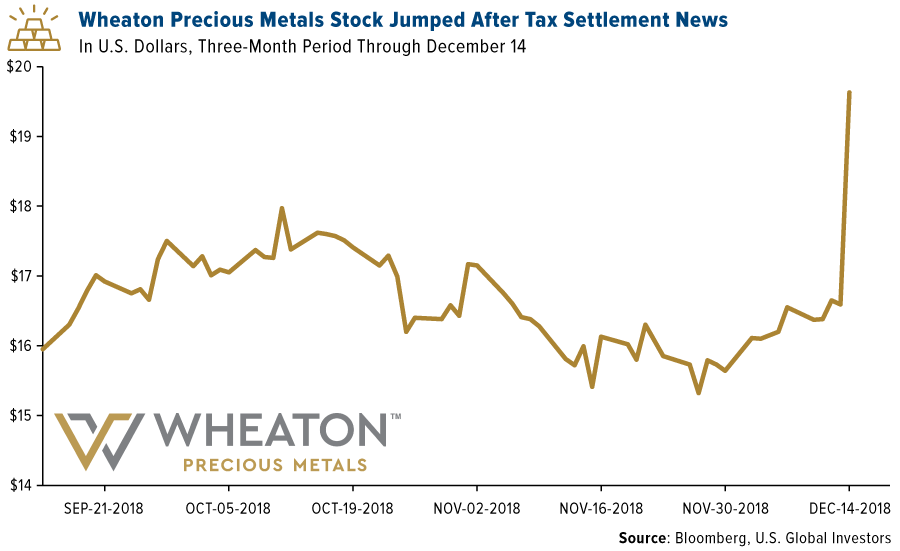

View Membership BenefitsToday gold mining investors and Canadian capital markets received an early Christmas gift. Wheaton Precious Metals, one of the largest precious metals streaming companies in the world, announced that it reached a settlement with the Canadian Revenue Agency (CRA), the equivalent of the IRS. Before now, Wheaton had been in an ongoing legal feud with the agency over international transactions between 2005 and 2010.

According to the agreement, income generated through Wheaton’s foreign subsidiaries will not be subject to Canadian taxes. The company, however, will need to mark-up the cost of service provided to foreign subsidiaries, from 20 percent to 30 percent.

“The settlement removes uncertainty with the use of our business model going forward and puts the tax issue behind us so that we can continue to focus on what we do best: building and managing our high-quality portfolio both organically and by accretive acquisitions,” commented Randy Smallwood, Wheaton president and CEO.

“We expect the stock to react positively to the news given the tax dispute was an overhang,” Credit Suisse analysts shared in a note to investors today. Indeed, Wheaton stock was trading up as much as 12.4 percent in New York following the news, hitting a four-month high of $19.63 a share.

I want to congratulate everyone at Wheaton, particularly Randy for his resilience and strong leadership. He’s always offered invaluable insights to our team and investors. I encourage interested registered investment advisors (RIAs) to check out the July 2018 webcast I did with Randy, where we discussed our seven top reasons to invest in gold. You can listen to the replay by clicking here.

Monetary and Fiscal Risks Boost Gold’s Investment Case

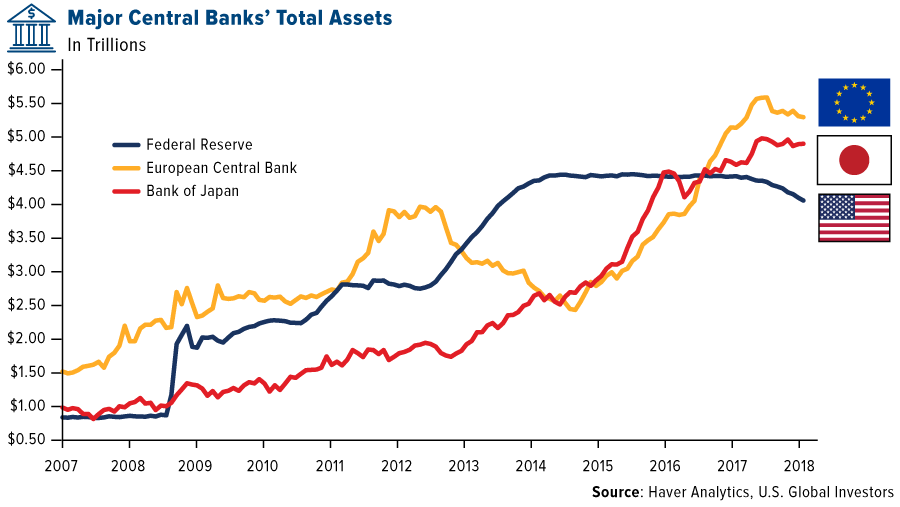

The investment case for gold and other precious metals got a boost this week in light of news that might concern some equity investors. The European Central Bank (ECB) announced that it would be drawing quantitative easing (QE) measures to a close by halting its 2.6 trillion-euro bond-purchasing program, begun four years ago as a means to provide liquidity to the eurozone economy after the financial crisis. Interest rates, however, will be kept at historically low levels for the time being.

The ECB, then, will become the next big central bank, after the Federal Reserve, to end QE and normalize monetary policy. Although it’s steadily been tapering its own purchases of bonds, the Bank of Japan (BOJ) is still committed to providing liquidity at this point. Assets in the Japanese bank now stand north of 553.6 trillion yen ($4.86 trillion)—which, amazingly, is more than 100 percent of the country’s entire gross domestic product (GDP). Holdings, in fact, are larger than the combined economies of India, Turkey, Argentina, Indonesia and South Africa.

In the past, I’ve discussed the economic and financial risks when central banks unwind their balance sheets. The Fed has reduced its assets six times before now, and all but one of those times ended in recession, according to research firm MKM Partners.

“Business cycles don’t just end accidentally,” MKM Chief Economist Mike Darda said in 2017. “They are killed by the Fed.”

We can now add the ECB and, at some point, the BOJ to this list. The three top central banks control approximately $14 trillion in assets, a mind-boggling sum, and it’s unclear at this point what the ramifications might be once these assets are allowed to roll over.

The Widest November Budget Deficit on Record

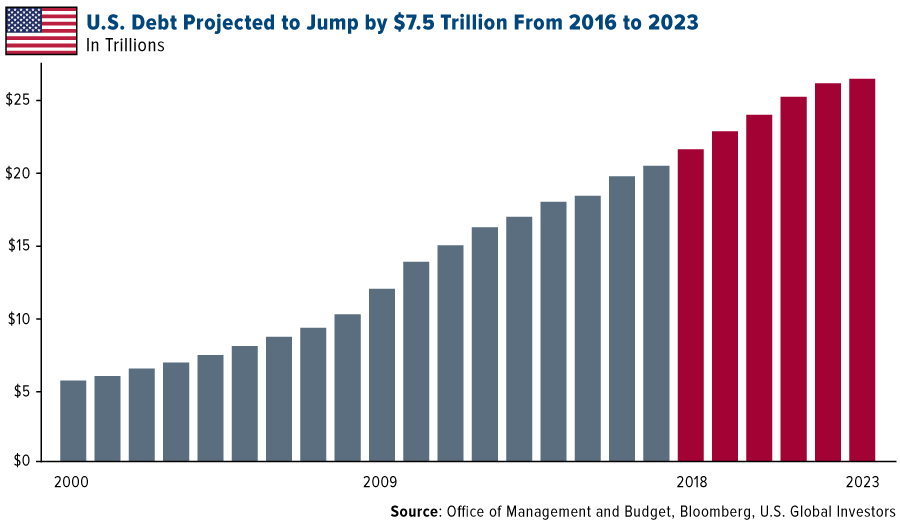

In addition, the Treasury Department revealed this week that the U.S. posted its widest budget deficit in the nation’s history for the month of November, as spending was double the amount of revenue the government brought in. The budget shortfall, then, came in at a record $205 billion, almost 50 percent over the spending gap from a year ago.

This follows news that U.S. government debt is on pace to expand this year at its fastest pace since 2012. Total public debt has jumped by $1.36 trillion, or 6.6 percent, since the start of 2018, making it the biggest expansion in percentage terms since the last year of President Barack Obama’s first term, Bloomberg reports.

As of this Monday, the national debt stood at just under $22 trillion, and by as soon as 2022, it could top $25 trillion, according to estimates.

As I shared with you in November, the government could very well be in a “debt spiral” right now, in the words of Black Swan author Nassim Taleb. This means it must borrow to repay its creditors. And with rates on the rise, servicing all this debt will continue to get more and more expensive.

It’s for this reason, among others, that I recommend a 10 percent weighting in gold, with 5 percent in bullion and gold jewelry, the other 5 percent in high-quality gold stocks, mutual funds and ETFs.

Will There Be a Santa Claus Rally?

There are only a few more trading days left to 2018. Will we see a Santa Claus rally? This week I had the opportunity to speak with CNBC Asia’s Akiko Fujita on this very topic. To watch the interview and hear my thoughts, click here!

The Rule of Law

|

| Photo: Wmpearl | Creative Commons 1.0 Universal Public Domain Dedication |

If you’ve ever taken a tour of any government buildings in Washington, D.C., as I did last week, you may have noticed the prevalent depictions of Moses. The ancient biblical prophet can be seen on the east wall of the Supreme Court, above the gallery doors of the House Chamber, above American artist Rembrandt Peale’s portrait of President George Washington and elsewhere. But why?

To answer that, it might help to remember that Moses is often recognized as the first lawgiver. After he frees the Hebrews and leads them out of Egypt, Moses ascends Mount Sinai to receive the 10 Commandments, a set of principles that many today believe serves as the basis for Western law.

Not everyone agrees with this, of course.

We should all agree, however, that the United States is an exceptional country for a whole host of reasons, one of them being the concept of the rule of law.

The rule of law guarantees that every American is subject to the same sets of precepts, and that no one is above the law, regardless of race, background, religion or politics. It helps give us peace of mind that we won’t be targeted by law enforcement arbitrarily or incarcerated without due process.

The rule of law is also essential to secure a healthy, vibrant economy as well as capital markets. Without property rights and a strong judicial system, uncertainty and instability would prevail, and markets wouldn’t function nearly as efficiently.

Whether or not there’s historical proof that Moses had any influence on the Framers of the Constitution, his repeated likeness in Washington is a reminder that ours is a nation of laws.

Gold Market

This week spot gold closed at $1,238.33, down $10.02 per ounce, or 0.80 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week largely unchanged. The S&P/TSX Venture Index came in off 2.97 percent. The U.S. Trade-Weighted Dollar rose 0.98 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-11 | Germany ZEW Survey Current Situation | 55.0 | 45.3 | 58.2 |

| Dec-11 | Germany ZEW Survey Expectations | -25.0 | -17.5 | -24.1 |

| Dec-11 | PPI Final Demand YoY | 2.5% | 2.5% | 2.9% |

| Dec-12 | CPI YoY | 2.2% | 2.2% | 2.5% |

| Dec-13 | Germany CPI YoY | 2.3% | 2.3% | 2.3% |

| Dec-13 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Dec-13 | Initial Jobless Claims | 226k | 206k | 233k |

| Dec-13 | China Retail Sales YoY | 8.8% | 8.1% | 8.6% |

| Dec-17 | Eurozone CPI Core YoY | 1.0% | -- | 1.0% |

| Dec-18 | Housing Starts | 1230k | -- | 1228k |

| Dec-19 | FOMC Rate Decision (Upper Bound) | 2.50% | -- | 2.25% |

| Dec-20 | Initial Jobless Claims | 219k | -- | 206k |

| Dec-21 | GDP Annualized QoQ | 3.5% | -- | 3.5% |

| Dec-21 | Durable Goods Orders | 1.8% | -- | -4.3% |

Strengths

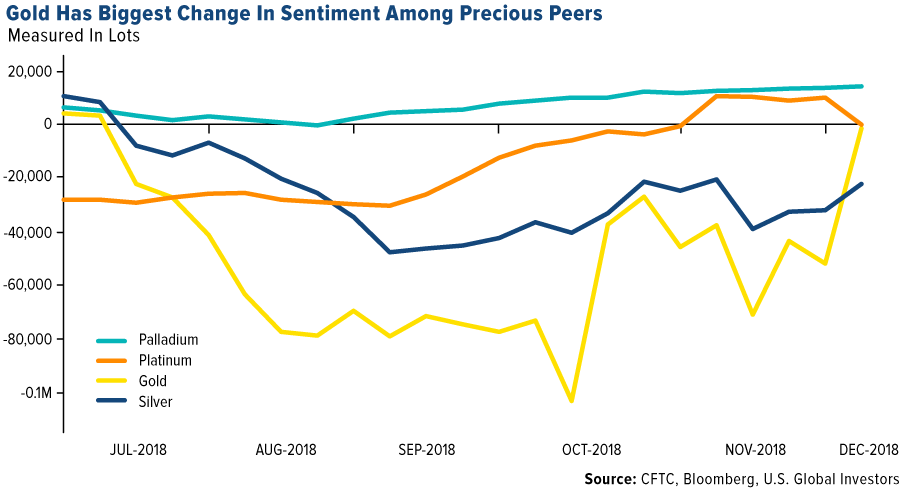

- The best performing metal this week was palladium, up 1.41 percent, though hedge funds cut their long position to a three-week low. ICBC Standard Bank, however, sees palladium hitting $1,500 an ounce by 2020. Gold traders and analysts were mostly bullish on the yellow metal this week on concerns about a potential U.S. government shutdown and ongoing uncertainty around Brexit, according to the weekly Bloomberg survey. Gold sentiment is increasing as holdings in gold-backed ETF holdings rise and as investors are unwinding net short positions. Bloomberg writes that U.S. Commodity Futures Trading Commission data shows that among its precious metal peers – palladium, platinum and silver – gold has seen the biggest change in sentiment over the last two months.

- Turkey continues growing its gold holdings after selling off its reserves for most of this year. Bullion holdings rose $69 million from the previous week and are worth $19.4 billion as of December 7, according to the Turkish central bank’s filings. In another sign of gold bullishness, Turkey will begin selling gold-backed bonds in an effort to diversify borrowing instruments. Bloomberg writes that only 22 karat and 24 karat gold will be accepted and that investors will be paid interest in the lira, but may request principal payments back in the form of physical gold.

- South Africa, once the world’s top gold producer, has seen output contract for a 13th consecutive month in October, the longest streak of declines in six years, writes Bloomberg. The country released figures showing production declined 15.1 percent from a year earlier. The Perth Mint Physical Gold ETF saw inflows of 11 percent, or $80.9 million, on Wednesday, marking the biggest one-day increase since September 18.

Weaknesses

- The worst performing metal this week was platinum, down 0.81 percent with hedge funds flipping this week to net bearish on price direction. High gold prices have dented demand in Asia leading up to the holiday season, with buying interest in India likely to be subdued for the rest of the year, reports Reuters. The world’s top gold consumer China saw premiums of $5.00 to $6.50 over the benchmark, down from last week’s $5.00 to $7.40 range. Gold posted its third straight day of losses on Thursday after a Trump administration official signaled that China will have to do more to end the trade war, writes Bloomberg.

- Paulson & Co. won control over the Detour Gold board of directors after convincing shareholders to overthrow most of the board, including its interim CEO. It is difficult to ascertain how the market will view Detour going forward in the shorter term window. Certainly, the new directors will have the best interest of shareholders at heart as this is the reason Paulson pushed for change at the company. This board replacement should also be seen as a warning shot to other gold company boards where shareholders believe they are not being served.

- Alamos Gold fell as much as 9.3 percent in Canada on Thursday after Desjardins lowered its rating on the stock to hold from buy. The lowered rating is due to company news that it has slowed down development activities and spending on its Kirazli Project in Turkey until it is granted an operating license, reports Bloomberg. Adding to the company’s stock turbulence is the news that two employees are feared dead at the Alamos Mulatos Mine in Mexico after an unexpected pit slope movement.

Opportunities

- Hedge fund manager Paul Tudor Jones said in an interview on Monday with CNBC that he doesn’t think the Federal Reserve will hike rates at all in 2019 due to the drop in commodity prices putting inflationary pressure on the economy. Jones said we should expect to see “a lot more volatility next year” in the markets and that we’re “probably sitting on a big global credit bubble.” Goldman Sachs said the odds of a rate hike at the Fed’s meeting in March are now below 50 percent due to worsening economic data. Zach Pandl, head of global currency and emerging-market strategy said that “the latest news from the Fed raises our convictions in those forecasts and suggest that the dollar depreciation could be more front-loaded than we previously anticipated.”

- Martin Roberge of Canaccord Genuity Corp. wrote in a note this week that gold could be set up for a sustained rally and would be the prime beneficiary of a dovish Fed. When the Fed paused following the December 2015 rate hike, the U.S. dollar peaked soon after and there was a monster rally in the gold miners in the first half of 2016. Roberge notes 2019 could be a similar setup if the Fed pauses and oil regains some strength, stroking inflation expectations.

- Wheaton Precious Metals saw a big boost on Friday after announcing that it reached a settlement with the Canadian Revenue Agency (CRA). The agreement says that income generated through Wheaton’s foreign subsidiaries will not be subject to Canadian taxes, though the company will need to mark-up the cost of service provided to foreign subsidiaries from 20 percent to 30 percent. Wheaton’s stock was trading up 14.4 percent following by the market close. The CRA tax issue has been an overhang on the stock for several years and with the issue finally being put to rest, Wheaton should see money flow back into the shares.

Threats

- Following a multiyear boom, home sales are starting to slow around the United States. While values in most of the country haven’t fallen, reports Bloomberg, the rate of appreciation is slipping, particularly in the New York area. Another area is slowing too – the number of new hedge funds in this $3 trillion market. In fact, closures have been the new theme in 2018, writes Bloomberg, with closures outnumbering launches for the third year running with hedge funds noting a lack of good opportunities and or converting to family offices and only managing their own assets.

- The Fed is piling up unrealized losses, raising questions about its finances at a “politically dicey moment for the independent central bank,” reports Bloomberg. Mark-to-market losses at the Fed dwarfed central bank capital on September 30, according to its quarterly financial report. “A central bank with a negative net worth matters not in theory,” former Fed Governor Kevin Warsh said in an email. “But in practice, it runs the risk of chipping away at Fed credibility, its most powerful asset.”

- Economists at some of the largest banks are beginning to notice signs of a U.S. recession looming in 2019, reports Bloomberg, citing an inversion in part of the bond yield curve and a sell-off in stocks. JPMorgan, specifically, forecasts a 35 percent chance of recession next year, which is up from 16 percent probability back in March. In a global study done by UBS of 40 countries over the time frame of 40 years, the bank says the U.S. is among those currently behaving in a way inconsistent with prior peaks.

December 13, 2018Will There Be a Santa Claus Rally in Q4? |

December 11, 2018Frank Holmes' Forecast for Gold in 2019 |

December 6, 2018U.S. Global Investors Continues GROW Dividends and Share Repurchase Program |

|||

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.18 percent. The S&P 500 Stock Index fell 1.25 percent, while the Nasdaq Composite fell 0.84 percent. The Russell 2000 small capitalization index lost 2.57 percent this week.

- The Hang Seng Composite gained 0.15 percent this week; while Taiwan was up 0.14 percent and the KOSPI fell 0.31 percent.

- The 10-year Treasury bond yield rose 5 basis points to 2.89 percent.

Domestic Equity Market

Strengths

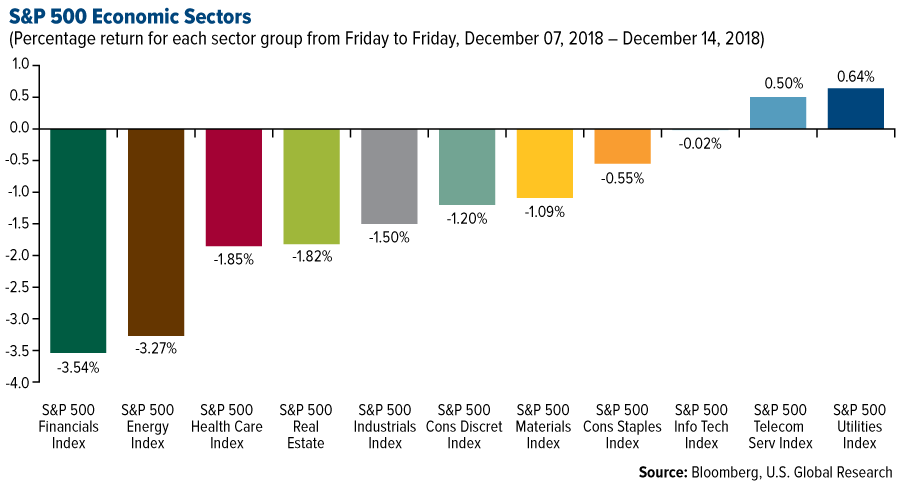

- Utilities was the best performing sector of the week, increasing by 0.64 percent versus an overall decrease of 1.36 percent for the S&P 500.

- Broadcom was the best performing stock for the week, increasing 11.49 percent.

- Tesla’s shares have rallied 45 percent since hitting a 2018 low in October despite traders having a short bet of nearly $10.4 billion. On the other hand, the S&P 500 is down 8 percent over the same time period.

Weaknesses

- Financials was the worst performing sector for the week, decreasing by 3.54 percent versus an overall decrease of 1.36 percent for the S&P 500.

- Under Armour was the worst performing stock for the week, falling 19.66 percent.

- A death cross refers to a chart pattern when an index or stock’s short-term moving average crosses below its long-term moving average, which indicates the potential for a major selloff. The S&P 500 posted a death cross this week and it could be bad news this time around. The S&P 500 has a downward-sloping 200-day moving average, meaning its effect will be amplified, according to a team of technical analysts at Bank of America Merrill Lynch.

Opportunities

- China's largest music streaming service, Tencent Music, launched its initial public offering on the New York Stock Exchange this week under the ticker symbol TME. At closing price, Tencent Music’s market value was $18.65 billion, writes MarketWatch.

- Reuters reports that SoftBank Group Corp is set to raise 2.65 trillion yen, or $23.5 billion, in Japan’s largest-ever initial public offering.

- Dell voted to go public once again. The company announced on Tuesday that it had agreed to buy back "tracking" shares of VMware — a company of which it owns 80 percent — for $120 apiece, or $23.9 billion. This will allow Dell to trade publicly on the New York Stock Exchange beginning on December 28 under the ticker DVMT.

Threats

- Pivotal Research Group, a research firm that has caused troubles for Facebook and Snap, just released its media, internet and communications predictions for 2019. One of the analysts’ predictions is to "expect material Facebook management changes," referring to the firm's "sell" rating on the stock.

- Shares of the athletic-apparel maker Under Armour fell more than 10 percent on Wednesday after the company's outlook underwhelmed.

- Verizon expects to write down the value of Oath in the fourth quarter of this year by $4.6 billion. The company blamed competitive pressures in the ads business.

The Economy and Bond Market

Strengths

- U.S. consumer spending gathered momentum in November, which could calm fears of an economic slowdown. On Friday the Commerce Department reported retail sales excluding automobiles, gasoline, building materials and food services surged 0.9 percent last month. Core retail sales, which correspond most closely with the consumer spending component of gross domestic product, were previously reported to have gained 0.3 percent in October, reports CNBC. Economists polled by Reuters had forecast core retail sales rising 0.4 percent last month.

- Initial claims for state unemployment benefits fell to a 49-year low, dropping 27,000 to a seasonally adjusted 206,000 for the week ended December 8, according to the Labor Department. Last week’s decline in claims was the largest since April 2015.

- The consumer price index (CPI) was unchanged in November, matching the forecast of economists polled by MarketWatch. The increase in the cost of living over the past 12 months slowed to 2.2 percent from 2.5 percent – cheaper gas is likely one of the main reasons for this.

Weaknesses

- The U.S. flash purchasing managers’ index (PMI) reading fell to a 13-month low in December to 53.9 from 55.3 in November, IHS Markit reported. This signals the weakest overall improvement in operating conditions since November 2017.

- In the Wall Street Journal’s monthly survey of economists, around 85 percent of those surveyed are the most worried they have been in years about the U.S. economy, reports Business Insider. The top concern? President Trump’s trade war with China.

- Japan’s economy contracted by 2.5 percent in the third quarter, which is double the preliminary reading of 1.2 percent, reports Business Insider. A Reuter’s poll of Japanese businesses didn’t show much optimism look forward either, with only 14 percent of respondents believing Japan’s economy will grow next year.

Opportunities

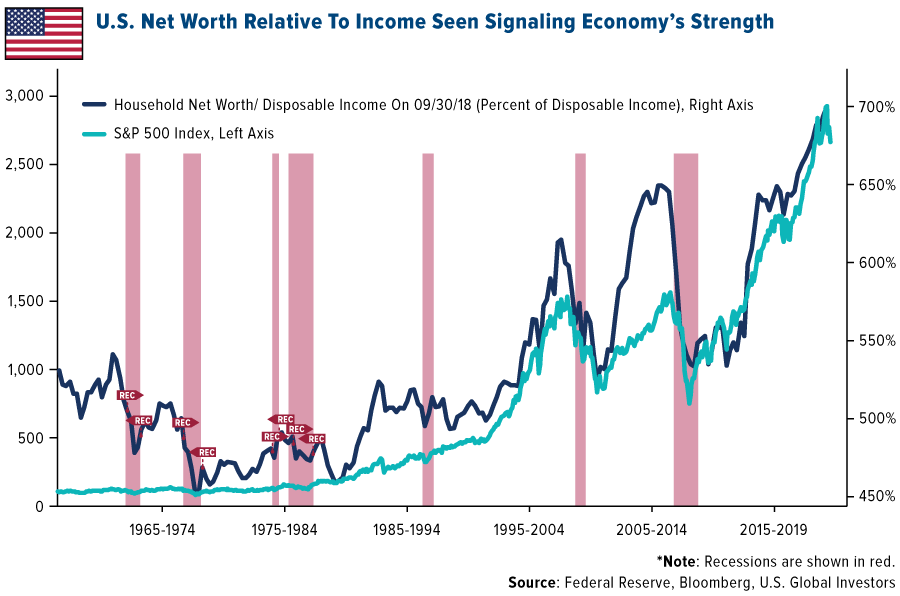

- The timing of the next U.S. recession is likely to hinge on the performance of stocks, bonds and other assets, according to Peter Boockvar, chief investment officer at Bleakley Financial Group LLC. Boockvar gave his outlook in a report Tuesday that referred to households’ net worth as a percentage of disposable income, as compiled quarterly by the Federal Reserve. Last quarter’s figure was a record 700 percent. “The direction of asset prices and its impact on confidence and funding” will determine when the economy’s next slump arrives, he wrote.

- The Federal Reserve’s policy meeting will be the main attraction next week as speculation grows that the U.S. central bank could signal slowing down the pace of rate hikes.

- China slashed tariffs on U.S. automobiles, removing the additional 25 percent tariffs on U.S. autos in an effort to ease trade tensions, according to Reuters.

Threats

- Legendary investor Paul Tudor Jones said in a recent CNBC interview that the Federal Reserve won't hike rates in 2019. He added that commodities are a leading indicator the Federal Reserve should be watching closely.

- The positive correlation that existed between the U.S. Dollar Index and U.S. treasury yields last year has now turned negative. Traders are bullish on the U.S. Dollar Index and U.S. treasuries right now, something Morgan Stanley says is “rare.” The last time this occurred, volatility in developed market currencies exceeded that in emerging market currencies for nearly a year.

- The fallout from the arrest of Huawei's CFO in Canada last week continues, with China threatening 'further action' if the U.S. does not withdraw its arrest warrant. China summoned the U.S. ambassador over the weekend to register its protest at Meng Wanzhou's arrest.

Energy and Natural Resources Market

Strengths

- Iron ore was the best performing major commodity this week rising 1.69 percent. The commodity rose after China’s steel output contracted to its weakest in seven months in November as Tangshan city stepped up efforts to fight pollution, lifting demand for higher quality iron ore.

- The best performing sector this week was the S&P/TSX Diversified Metals & Miners Index. The index rose 2.27percent after investors felt more comfortable with risk after China took more steps to defuse trade tensions with the U.S., confirming it will remove certain retaliatory duties.

- The best performing stock for the week was Wheaton Precious Metals Corps. The Canadian royalty and streaming company rose 14.44 percent after the company reached a settlement with the Canadian tax authorities that will mean a far lower tax bill than many feared.

Weaknesses

- Natural gas was the worst performing commodity this week. The commodity dropped 15.04 percent after weather forecasts showed easing cold from Texas to the Midwest, signaling a decline in demand for the heating fuel.

- The worst performing sector this week was the S&P 1500 Oil & Gas Equipment and Services Index. The index dropped 6.77 percent, to a 52-week low after shale explorers in the U.S. continue to dial back drilling as they reported double-digit oilfield cost inflation.

- The worst performing stock for the week was Canfor Corp. The Canadian paper and forest producer dropped 15.11percent to the lowest level this year after escalating diplomatic tensions between Canada and China raise concerns over the stability of a key export market for the Canadian producer.

Opportunities

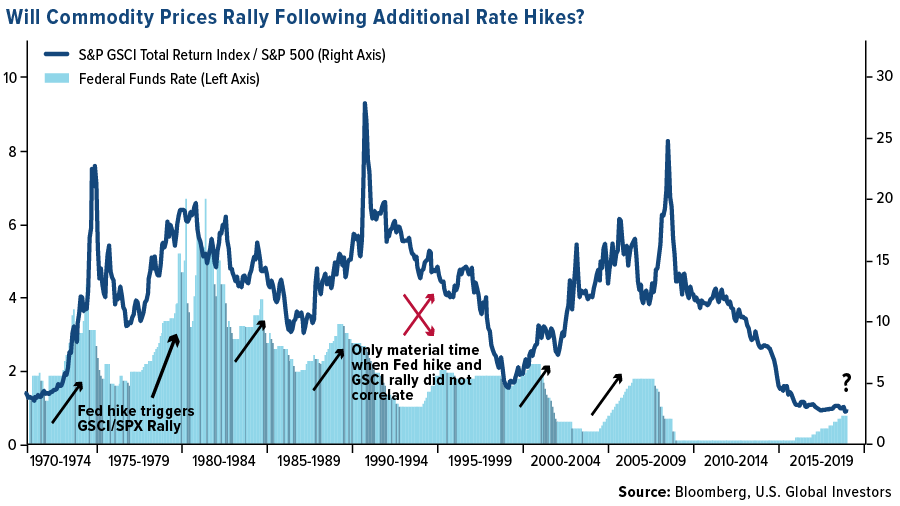

- Goldman Sachs, Morgan Stanley and Citi all agree that commodities as a complex is compelling. This chart, starting in the early 1970s, shows the S&P Commodities Index divided by the S&P 500. It's a ratio to show you how overpriced or underpriced the commodities universe is relative to the market as a whole, if you take the S&P 500 as a good proxy for the market as a whole. The next overlay that you can put on that chart is the correlation with the Federal Reserve rates. Interestingly, there have been seven Fed rate hiking cycles over those 50-odd years, and all but one of those cycles have coincided with the commodities outperforming the market.

- China is taking steps to address U.S. complaints that Beijing engages in unfair trade practices. The WSJ reported “Chinese officials are also considering making changes to the “Made in China 2025” plan, a state-led industrial policy aimed at enabling Chinese companies to dominate a number of industrials such as artificial intelligence and robotics. This policy is a focal point of the U.S. complaints against China.

- China will keep its economic growth within a reasonable range next year, striving to support jobs, trade and investment while pushing reforms and curbing risks, the top decision-making body of the Communist Party, the politburo, said on Thursday. “We will promote steady growth, promote reform, adjust structure, benefit people’s livelihood and prevent risks in a coordinated way, and keep economic operation in a reasonable range”

Threats

- Chinese economic data for November was highly disappointing. Industrial production dropped to 5.4 percent growth, a 33-month low and missing consensus expectations. Retail sales grew 8.1 percent, a 15-year low and well below consensus. Lastly, fixed asset investment rose 5.9 percent, a slight rebound from the previous month, but hardly enough to reactivate the slowing economy.

- The flash reading of U.S. manufacturing purchasing managers’ index fell to a 13-month low of 53.9 in December from 55.3 in November, IHS Markit reported Friday, mainly on a decline from new orders and employment. “Importantly, although growth remains relatively robust, momentum is being lost and is likely to continue to fade as we move into 2019,” said Chris Williamson, chief business economist at IHS Markit.

- The IEA underscored doubts about OPEC supply cuts, saying it’s too early to tell if they’ll succeed in balancing the market. Even if the group curbs as much as promised, a surplus may still emerge. Potential supply declines in Libya and Venezuela would help offset that risk.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 1.9 percent. Despite street protests over a new labor law and the creation of a new government-controlled court system, stocks trading on the Budapest exchange moved higher. OTP bank was the best performing equity, gaining 4 percent.

- Russian ruble was the best relative performing currency this week, losing 45 basis points against the dollar. Central bank of Russia, unexpectedly hiked its main rate to 7.75 percent, from 7.5 percent, on expectation that inflation will spike above central bank’s target next year.

- Material was the best performing sector among eastern European markets this week.

Weaknesses

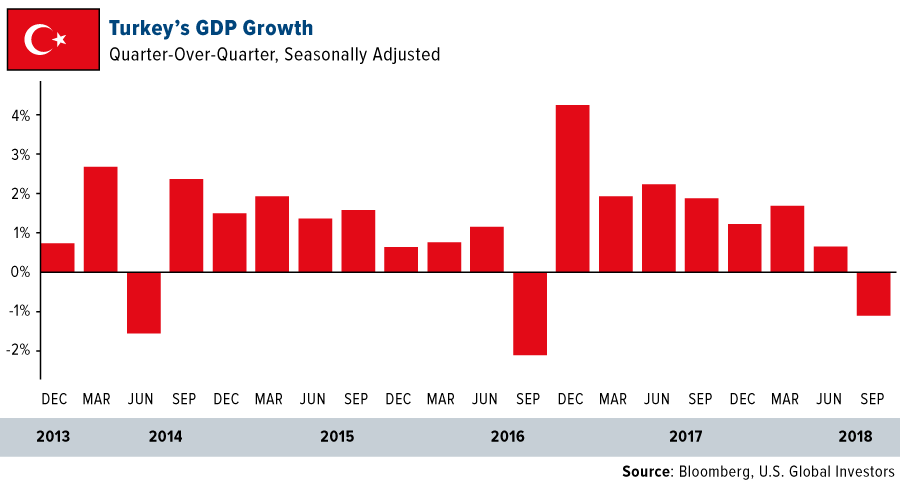

- Turkey was the worst performing country this week, losing 3.4 percent. Turkey is set to launch a military intervention in northeastern Syria to fight U.S.-backed Kurdish rebels, signaling more tension between the two NATO members.

- The Turkish lira was the worst performing currency this week, losing 1.2 percent against the U.S. dollar. The central bank left its main rate unchanged at 24 percent, as expected. Fitch will announce Turkey’s credit rating review after market close on Friday. The company downgraded Turkey’s sovereign debt rating to BB in July, one notch below investment grade, with a negative outlook.

- The industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- Theresa May survived the vote of no confidence on Wednesday with the conservative party lawmakers voting 200-117 in her favor. In a little more than three months, the U.K. will leave the European Union (EU) with or without an agreement, but her exit now would be negative for further negotiations. The British pound appreciated against the U.S. dollar after news came out that she will stay in the office for now.

- Wood & Company analysts see Romanian banks as safer, stronger and richer with Romania’s economy growing at 4.3 percent year-over-year, above the expected 3 percent growth. Romanian banks continue to offer a safe place with strong capital ratios, high ROEs and solid dividend yields, according to Alex Boulougouris. Stocks trading on the Bucharest exchange are the only ones in emerging Europe that have a positive year-to-date return in U.S. dollar terms.

- China confirmed it would lift retaliatory tariffs on U.S. automobile imports for three months, effective January 1. Press reports also suggest China will delay some targets in its “Made in China 2025” plan, which has become a lightning rod in U.S.-China relations, according to BBH Global Currency Strategy research. Less trade tension between China and the U.S. could support global trading.

Threats

- Investor sentiment for the eurozone dropped to the lowest level in four years in December. The Sentix measure dropped into negative territory in December, falling to -0.3 from 8.8 in the previous month, and down from 32.9 at the start of the year. This compared with forecasts from Reuters and Bloomberg of 8.1, respectively. Sentix highlighted escalating trade tensions, the budget crisis in Italy, unrest in France and Brexit uncertainty as headwinds.

- Mario Draghi admitted economic data had been weaker than expected and said the balance of risk is moving to the downside. He lowered growth forecasts for this year and next, and cut the inflation forecast for next year, while raising it for this year. The European Central Bank (ECB) also confirmed it would halt its quantitative easing (QE) program this month. On Friday, preliminary December PMI data for the euro-area declined to 51.4 from 51.8. France’s PMI reading dropped below 50, the level which separates growth from contraction.

- Turkey’s economy contracted by 1.1 percent in the third quarter and economic activity will most likely remain weak in the first quarter of 2019. Private consumption and investment demand plunged sharply. However, exports soared and imports declined, placing net exports as a main driver of GDP growth with the largest contribution since the first quarter of 2009.

China Region

Strengths

- The Philippines Stock Exchange Index climbed 85 basis points for the week, while India’s NIFTY 50 and SENSEX Indices climbed 1.05 percent and 0.81 percent, respectively.

- The properties and construction sector was the top-performing one in the Hang Seng Composite Index for the week, climbing 1.85 percent.

- In Malaysia, industrial production increased 4.2 percent for the year-over-year October period, accelerating from 2.3 percent in September and beating the 3 percent estimate.

Weaknesses

- Thailand’s SET Index declined by 2.36 percent for the week.

- Telecommunication was the worst-performing sector in the Hang Seng Composite Index for the week, declining by 1.36 percent.

- China’s year-over-year industrial production number missed for November, coming in up 5.4 percent, shy of estimates for 5.9 percent and down from last month’s 5.9 percent. Retail sales also missed, up only 8.1 percent for the same timeframe and short of expectations for 8.8 percent.

Opportunities

- There’s been more progress (to some degree) in thawing trade tensions between the United States and China. China resumed some purchases of U.S. soybeans and plans to eliminate the retaliatory 25 percent import tariff on U.S. autos for a three-month period as negotiations continue throughout that time. U.S. auto imports to China will return to the general 15 percent tariff level, down from the 40 percent retaliatory level. U.S. corn exports may be the next major development.

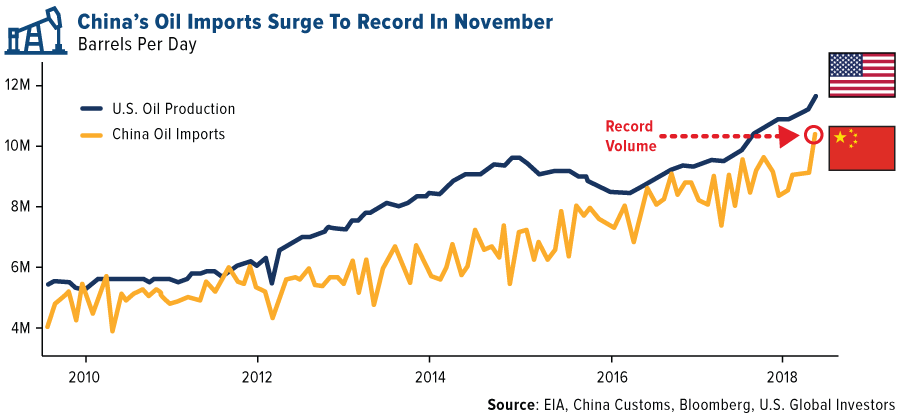

- While there are clearly quite a few questions surrounding the ultimate outcome of trade talks between the U.S. and China, it remains notable that China’s oil imports actually jumped to a record in November. And curiously enough, the U.S. has recently shifted to net-exporting status.

- Following the recent pause in rising inflation in the Philippines, which we highlighted last week, the central bank this week stood pat, perhaps accordingly, on the interest rate situation, in what is hopefully a sign that inflation may be coming under control in that island-nation.

Threats

- The flipside to further resolution in the U.S.-China trade war and progress in developments and agreements and a so-called “truce” is escalation; this must remain as a distinct threat until it isn’t. Put differently, the only thing truly concrete is that there’s nothing concrete at this point, and markets typically prefer certainty to uncertainty. Thus while “progress” in “talks” and “negotiations” is good, and while temporary tariff reductions are useful and positive, and a “truce” is nice, all of these things taken in toto demonstrate the distinct uncertainty posed by the situation, and this should be borne in mind.

- A Chinese ban on sales of the iPhone would force Apple to settle a long and bitter licensing battle with Qualcomm, writes Bloomberg News, an outcome that could “harm the country’s smartphone industry and give its fiercest legal rival a boost.” This week a Chinese court ruled that Apple overstepped two Qualcomm patents in addition to issuing injunctions against the sale of six older versions of the iPhone. According to the tech giant, this decision could harm the Asian nation’s interests if royalties or fees paid to Qualcomm were raised.

- Huawei’s CFO Meng Wanzhou has been released on bail and surrendered her passports in Vancouver, and the U.S. has a 60-day window in which to arrange extradition.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended December 14 was TokenDesk, up 587.42 percent.

- Mike Novogratz, former hedge fund manager and Goldman Sachs Group partner, explains in a recent Bloomberg article why he is still all in on cryptocurrencies. He started Galaxy Digital Holdings last year, a crypto merchant bank, which has since reported $136 million in trading losses since bitcoin’s plunge. Despite this, Novogratz is undeterred. In the article he notes the future of cryptocurrencies and blockchain technology in “virtual worlds,” the opportunity for a security tokens market, and how he believes Galaxy Digital will break even next year, if not make money.

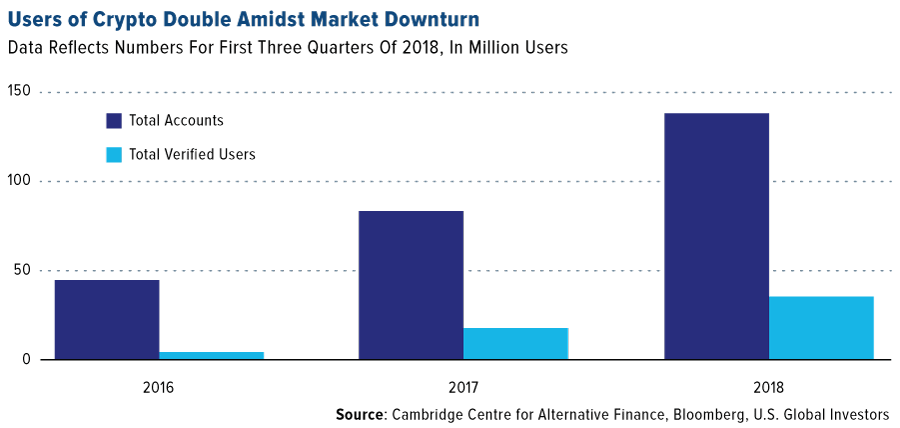

- According to a study released by the University of Cambridge, despite bitcoin tumbling nearly 80 percent from the start of the year, ranks of cryptocurrency users swelled in 2018, reports Bloomberg. In fact, the number of verified users of cryptos doubled in the first three quarters of the year. As the article explains, it turns out that industry enthusiasts were committed well beyond “the HODL rallying call that urged them to hold on during this year’s digital-asset market collapse.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended December 14 was HyperQuant, down 70.74 percent.

- Bitcoin is headed for its seventh weekly slump on Friday, reports Bloomberg, hovering above $3,000. This is a level that the digital coin has not broken below since September of last year.

- Some analysts are saying the bear market in bitcoin is far from over, reports MarketWatch. Stephen Innes, head of Asia Pacific trading at Oanda, for example, believes this is the case because bitcoin hasn’t yet provided a significant use case. “It’s been a disastrous year for cryptos, and by all indication, the current bear market could go from bad to worse with no fundamental or underlying reasons to buy BTC even more so when the only support offered up is a squiggly line on an analyst chart,” Innes said.

Opportunities

- In May of this year Facebook launched its blockchain team, with the aim of exploring the emerging technology, reports Coindesk. The social media giant has not given up on this plan, and is hiring five new staff members for its blockchain team, the article continues, in the areas of data science, software engineering and marketing.

- Cosmetics chain Sephora announced that it is joining a list of other retailers where shoppers can earn cash back, in the form of bitcoin, through an app called Lolli, reports Coindesk. So why did Sephora agree to take the plunge? According to the bitcoin rewards startup, 30 percent of the app’s users are women.

- Looking at a long-term bitcoin price indicator, the relative strength index (RSI), the cryptocurrency appears to be oversold for the first time in nearly four years, reports Coindesk. An asset is oversold if the RSI is holding below 30, and this week it reached 29.80. Not only does the under-30 reading on the 14-week RSI indicate that recent heavy selling from highs above $6,200 may have reached a point of exhaustion, the article explains, many experts also think such a drop can be followed by a strong corrective bounce.

Threats

- Unfortunately for cryptocurrency companies, the latest “trend” has been layoffs, reports the Wall Street Journal, in an effort to survive the nascent market’s biggest selloff to date. Just last week a firm known as Steemit, which runs a blockchain-based social network, laid off 70 percent of its staff. In addition, ConsenSys, a blockchain venture firm, said on Thursday that it would cut 13 percent of its staff, the article continues.

- The U.S. government’s Cybersecurity and Infrastructure Agency announced on Thursday that is has been made aware of bomb threat emails demanding bitcoin from organizations as well as suggested steps to take, reports Coindesk. According to the report, the emails state that a device will detonate unless a ransom in bitcoin is paid. The National Cybersecurity and Communications Integration Center (NCCIC) advises citizens that, if they receive one of the bomb threat emails, do not try to contact the sender or pay the ransom.

- One of the most well-funded stablecoin startups, Basis, announced that it is shutting down and returning all of its remaining funds to investors, reports Coindesk. Founder Nader Al-Naji explained in a blog post that the regulatory landscape was simply too unfavorable to launch the project: “As regulatory guidance started to trickle out over time, our lawyers came to a consensus that there would be no way to avoid securities status for bond and share tokens.”

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All