- Central Bankers Under Stress

- One Night in Buenos Aires

- Brexit in Chaos

Many outdoor team sports begin with a kickoff that leads one team to find itself in possession of the ball deep in its own territory. At first, the ball can be advanced with little resistance. But after initial gains, threats begin coming from multiple directions. Reading the field becomes more difficult and second-guessing from commentators becomes more animated.

Similarly, after being hailed for their actions during the 2008 financial crisis and their subsequent progress in normalizing financial conditions, monetary authorities are now encountering fierce resistance. Criticism is coming from multiple directions, and progress is becoming much more difficult.

At some level, this was inevitable; policy is always less popular when it becomes more restrictive. But the politics surrounding monetary policy are thickening and will likely make 2019 an unpleasant year for central banks.

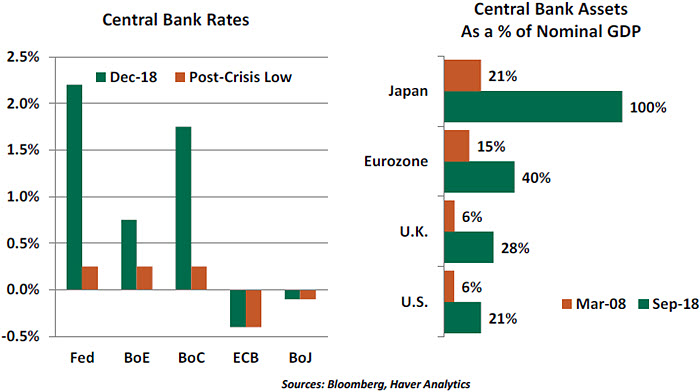

We’ve come a long way since 2008. The United States is enjoying what is likely to become the longest economic expansion in its history, and growth in other world markets has been excellent over the past five years. This has allowed some central banks to roll back the exceptional accommodation that was applied to promote recovery after the crisis. Interest rates have been rising in America, Britain and Canada, while quantitative easing (QE) programs in the U.S. and the eurozone have been curtailed.

The first tentative steps toward monetary normalcy were greeted as signs of progress. But more recently, disapproval of central bankers has been rising. The president of the United States recently said he was “not even a little bit happy” with his selection of Jerome Powell, the current head of the Federal Reserve. There is a long history of battles between the Fed and the White House, but the public nature and tone of the rebuke raised eyebrows.

Mark Carney, the Governor of the Bank of England, has earned disapproval for increasing interest rates while issuing dire warnings about the potential consequences of Brexit. This week’s meeting of the Governing Council of the European Central Bank (ECB) concluded with the questioning of ECB president Mario Draghi over why QE is being capped amid a period of economic softness.

Why have tributes turned into tribulations for central banks? There are four central reasons.

1. Indebtedness. Leverage was kindling for the crisis, and in its aftermath, there were calls to reduce it. But global debt today is higher than it was in 2007. The composition of global debt has changed: households are generally better balanced, but governments have gone in the opposite direction. Rising interest rates and reduced central bank purchases of sovereign debt could make the fiscal equation more difficult to solve in many countries, leading to pressure from politicians for easy money.

Global corporate debt has also grown dramatically since 2009, with much of the new issuance just above investment grade. This means even a modest increase in debt servicing costs could trigger delinquency or default.

As the Fed, in particular, searches for that neutral rate of interest that neither promotes nor hinders economic activity, the presence of large amounts of debt may have a bearing on their answer. The Fed issued a warning about leverage in its recent report on financial stability.

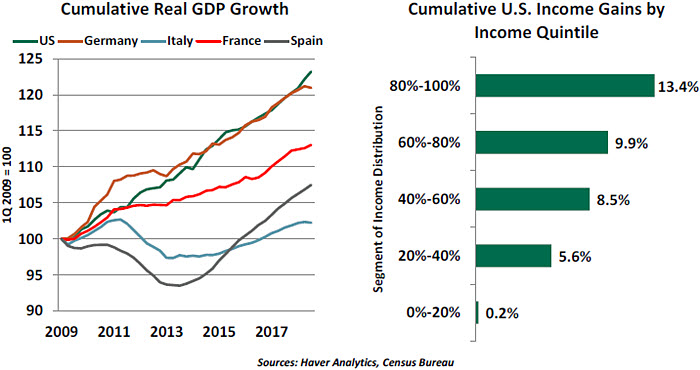

2. Inequality. Monetary policy is a blunt instrument that aims best at aggregate outcomes. But underneath the surface, countries and communities within countries have fared more poorly than average. To these latter audiences, tighter monetary policy is inconsistent with the circumstances they are experiencing.

Those who have not felt renewed prosperity have been driving a complicated global political dynamic. This has led some leaders to lean toward nationalism; they expect a country’s institutions (including its central bank) to fall into line behind them. This makes it difficult for monetary policy to retain its independence. Just this week, the head of the Reserve Bank of India resigned in the face of government pressure.

3. Inflation. Price levels have been slow to increase in developed markets, falling persistently short of inflation targets. Some think new secular governors (automation, analytics and Amazon) have created a new paradigm for the price level, while others predict that normal patterns will vigorously reassert themselves in the year ahead. It is best to fight inflation proactively, but it is hard to muster support for doing so when inflation seems so benign.

Inflation is also a term that can be applied to asset prices. QE programs were designed, in part, to bolster asset prices by reducing rates of return on safer investments. The unwinding of these efforts works in the opposite direction, much to the chagrin of equity markets. Reducing QE may be a sensible way of preserving financial stability; but once

again, it is hard to muster support for restraint when everything seems to be going so well.

4. Instability. As highlighted in this week’s other segments, there is no shortage of worrisome situations around the world. Any one of them could threaten the aging business cycle and work through financial markets to bring about recession.

The Federal Reserve will likely raise interest rates one more time next week. But after that, their course becomes much less clear. Fed Chair Powell compared the challenge to navigating a dark room; only incoming data and global developments can shed light on the situation. Communication around upcoming decisions will have to be carefully calibrated.

Popularity is not an objective of central banks. But their heads will need to be on swivels next year to take stock of threats coming from multiple directions. Their ability to read the field correctly will determine how long the global expansion can last.

He Said, Xi Said

Two weeks ago, presidents Donald Trump and Xi Jinping shared a dinner at the G-20 forum in Argentina. Expectations were low that concrete resolutions would emerge from the encounter, but it was encouraging to see the leaders re-engage after a year of rising tensions, failed negotiations and new tariffs.

Initial proclamations suggested a productive meeting. The White House committed to a 90-day delay in threatened tariff increases and trumpeted a few tangible concessions made by China. China’s statements were less specific, committing only to further conversations. This created uncertainty about what had actually been agreed to; nonetheless, markets cheered.

In the days that followed, the tone changed. President Trump described himself as a “Tariff Man” in a tweet. Days later, U.S. Trade Representative Robert Lighthizer was named the leader of the U.S. delegation to those talks. He was a natural choice, given his current senior role in the administration and his career experience in trade matters.

However, some market observers were nervous about Lighthizer’s open suspicions of China. Lighthizer has given several recent interviews that have reinforced his hard-line reputation. He emphasized that March 1 is a firm deadline, at which time the U.S. will raise tariffs from 10% to 25% on $200 billion in goods unless a new deal is in place. Financial markets were discomfited by these strong statements, and suffered through a difficult few days.

On a separate stage, officials in Canada arrested Meng Wanzhou, the chief financial officer and daughter of the founder of Chinese telecommunications firm Huawei, following the U.S. investigation of Chinese firms’ violations of U.S. sanctions. China’s critics claim China flouts such sanctions without consequence, and a prosecution would be a strong lesson. China has responded by detaining two Canadian citizens, perpetuating a pattern of retaliation in kind. The timing of the arrest appears to have been opportunistic and coincidental to the Buenos Aires leadership meeting, though Meng’s fate is now another matter for negotiation.

Huawei is a stakeholder in China’s long-term technology strategy, in which China seeks to develop more technology domestically and set the standards for emerging products like 5G networking. Of course, the United States has other ideas, seeing Chinese gains in this area as both an economic and a strategic threat.

Concessions appear to have already started in initial talks, with China offering to reduce its tariffs on imported vehicles from 40% to 15%. (China had raised its auto tariffs to 40% in retaliation to the U.S.’ first round of tariffs against China.) The offered reduction would merely restore the U.S. to the same barrier faced by the rest of the world, so it should be viewed as a very minor step. In the same vein, the resumption of Chinese purchases of U.S. soybeans is less of a concession than a restoration of typical pre-tariff trade patterns.

However, we expect that more substantial progress is possible. Both the U.S. and China have much to gain from a trade deal and would risk pain if negotiations falter. Chinese stock markets are reeling, and industrial activity appears to be cooling just as a bevy of debt is coming due. In the U.S., high tariffs could increase inflation and lead to job losses in import-dependent industries. And people working in those communities will vote in the 2020 presidential election.

It has been a busy two weeks. With a deadline approaching fast, we do not foresee much of a holiday break for trade negotiators.

Commotion in Commons

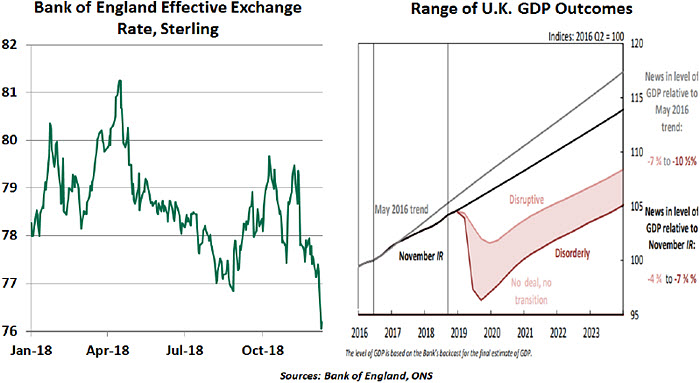

With less than four months until the U.K. is due to exit the European Union (EU) on March 29, 2019, the already chaotic Brexit process has been plunged into further disorder. On Monday, Prime Minister (PM) Theresa May decided to defer the crucial vote on the Brexit withdrawal agreement to obtain “further reassurances” on the key issue of a backstop for Northern Ireland. The parliamentary arithmetic that was heavily stacked against her soon transformed into a no-confidence vote on her leadership.

Though the prime minister has won the vote for now (and cannot be challenged again for 12 months), the turmoil is far from over. Late in the week, she was back in Brussels seeking a revised deal that would give the U.K. improved terms. Whatever agreement emerges from those talks (and it could be very similar to the one currently on offer) is slated to be brought back to the House of Commons before 21 January 2019. In the absence of any major revision, particularly to the backstop, the deal is likely to be rejected in the parliament and preparations for an EU exit without a formal departure agreement will intensify.

While there are other options for a new relationship between the U.K. and the EU (namely “Norway Plus” or “Canada”), none seems overly attractive. May’s deal could succeed eventually, for the simple reason that other alternatives are even worse. But the risk of a no-deal departure, whether managed or accidental, is rising. A change in the leadership or government at this stage will only add to the uncertainty delaying the process further, possibly extending Article 50. And the odds of a second Brexit referendum are rising.

A no-deal outcome will have far reaching consequences for the UK’s economy. According to the Bank of England’s recently published withdrawal scenarios, a “disorderly no-deal” would result in a severe recession, a sharp fall in the pound’s value, high inflation and sharp interest rate hikes.

As Theresa May has stated before, the choice is still “this deal or no deal.” It is time to put the political differences aside and deliver a Brexit that causes minimal economic pain. The U.K. is running out of time, and Brussels is running out of patience.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust

Concessions appear to have already started in initial talks, with China offering to reduce its tariffs on imported vehicles from 40% to 15%. (China had raised its auto tariffs to 40%

Concessions appear to have already started in initial talks, with China offering to reduce its tariffs on imported vehicles from 40% to 15%. (China had raised its auto tariffs to 40%