Powell, the Third Mandate, the New Fed and Crawdads

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPowell and the New Fed

Late in the Cycle

Bond Boom

Priced to Sell

A Little Nostalgia

We have reached the best time of year, when we can look to the future with hope. We can stop wondering what will happen in 2018 and look forward to 2019. The investment industry always does this enthusiastically, as you will see in forecasts everywhere the next few weeks.

Not wanting to be left out, or leave you wondering what I think, I usually review several other forecasts and later add my own. This year, I’m turning that sequence around. Recently I did a “2019 Investment Outlook” webinar with my business partner Steve Blumenthal. So right or wrong, my thoughts are now on record. In this letter, I’ll give you an abbreviated version of that webinar and add a few other thoughts at the end. Then in January, I’ll spend a letter or two reacting to other interesting forecasts.

But first, I am going to offer some different thoughts than the mainstream media spin on Jerome Powell, his press conference, and the Federal Reserve.

And even before that, I’m happy to announce that Alpha Society membership is now open for a limited time. This is a big deal if you love discussing investments, the economy, big picture ideas, and all the bits and pieces of trends, data, and events that make our world go round.

With the Alpha Society, you get all of our subscription services now and in the future for the lifetime of the service... plus exclusive Alpha Society benefits available to no one else. For example, our Quarterly Conference Calls give Alpha Society members direct answers from our editors.

You also get invited to exclusive networking and meetup events including future quarterly conference calls, a gated community for Alpha Society members only through our online Council, “velvet rope” privileges at our famed Strategic Investment Conference and much more.

Take a look at everything on offer and consider joining now before the holidays distract you from what could be the most important membership offer you’ll ever receive.

Powell and the New Fed

My inbox and the mainstream media are packed with criticism of Jerome Powell’s press conference. The market didn’t like what it heard and immediately tanked. People called him tone deaf for not listening to the market. Looking at US-based indexes, and indeed most foreign ones, we are clearly in bear market territory with many benchmarks down well over 20% from their highs. What was Powell thinking?

There were many accusations that Powell fumbled the ball, not telling the market what it wanted to hear. As if that were his job.

I think Powell may have said exactly what he wanted to communicate. The last three Federal Reserve Chairs have acted like the Fed has three mandates: the two official ones (low inflation and full employment) and an unofficial third one: making sure asset prices rise as the market wants. Not just the stock market, but real estate and all other investment assets. It started with the Greenspan “Put” which morphed into the Bernanke Put (remember the taper tantrum?) and reached its apex with the Yellen Put.

And what did we get? A series of bubbles.

- As Stan Druckenmiller says, the really big Fed mistake was when Greenspan kept rates too low for too long in 2003–2004, setting up the housing bubble and Great Recession. He clearly helped the massive bubble in 1999–2000.

- Then Bernanke’s reluctance to raise rates above zero in 2012–2013, when the economy was manifestly recovering, refueled the asset price bubble.

- Yellen continued that course. Her reluctance to raise rates until Trump won the election, the economy was booming, and unemployment clearly falling was inexcusable.

I think there is the very real possibility Powell wasn’t being tone deaf at all. He could have wanted to remind everyone that the Federal Reserve is independent from Wall Street as well as politics.

Yes, Powell worked on Wall Street, is quite wealthy and was an investment banker, and even ran his own hedge funds, as well as numerous posts for the Treasury before he came to the Fed, so he is clearly an “insider.” He is also wicked smart, maybe even wicked brilliant. He didn’t stumble or mumble at his press conference. He was quite deliberate. He knew exactly what he was saying and I’ll bet you a dollar against 27 doughnuts he knew the market would react negatively. You cannot have his resume and not know exactly what the market would do given his quite careful press conference.

This makes me think Powell is perfectly willing to walk away from that unofficial third mandate. Is he letting his inner Volcker show just a little bit? If so… damn, Skippy, it’s about time!

The Federal Reserve should be just as concerned about Main Street as it is about Wall Street. The serial bubbles of the last 30 years all had serious negative consequences. Yes, the ride was often fun, and some of us made good money in both the up and down cycles. But Main Street would be better served with a steady-as-she-goes Fed policy.

Wall Street (and the financial world in general) should create earnings and value companies based on those earnings, and not game the system to the point where valuations get incredibly stretched and then the bubble pops. It kills the average investor who buys late in the cycle and then gets scared out of the market at exactly the wrong time. People come to see investing as a game Wall Street plays for its own benefit. In fact, it is anything but a game. To most people, investing is about retirement and life.

How will we know if Jay Powell is serious about his inner Volcker? In Texas, we would look to see if he “crawdads” on us. Let me explain that. I grew up in West Texas where farmers and ranchers would create “tanks” or ponds to catch and hold rainwater for the cattle to drink.

Little creatures we call crawdads (crayfish in more polite circles, which look like tiny lobsters) would burrow holes around these tanks and live happy little crawdad lives… until some young kid would come along, throw a piece of small bacon with a string attached to it in front of their home. When they would come out and grab the bacon, you would jerk the string, put the crawdads in a bucket and sell them to strange adults who would pay you a nickel apiece. Just for a silly crawdad.

Later in life, I learned that crawfish etouffee is a serious meal in Louisiana and much of Texas. Next time you go to Pappadeaux’s, order the crawfish etouffee. It is not cholesterol friendly, but it is really good.

But back to the main plot: When crawdads sense danger, they start walking backwards (as in this video) to hide in their hole. Hence the term, “Are you crawdadding on me?” Meaning, “Are you backing away from what you said or want back what you gave me?” It was generally not said in a polite manner. To crawdad on someone meant you broke your word.

If Powell lets the markets fall and doesn’t crawdad on us without coming back and giving a speech essentially saying “I’m sorry, I really meant to be more dovish,”, then we will know he really wants to end the third mandate. That would make me stand up and applaud. Loudly and with enthusiasm. Will it cause me personal pain? Sure. I’m trying to sell my home now, and what he did probably won’t help real estate values. (By the way, if you are reading this and thinking about buying my home, don’t lowball me. I’m not paying attention to Powell and the Fed either. Value is value.)

That being said, if Powell really sticks to his guns (I know I’m mixing metaphors here), then the United States and the world will be better in the long run—especially if his successors at the Fed do the same. They should politely take the president’s call, ignore the tweets, and set their own independent course.

Will there be a time to cut rates? Absolutely. And I fully expect Powell to do it when unemployment starts to rise or inflation rears its head. But not because of some tantrum in the %#$! markets. That is not the Fed’s mandate.

I want the Fed chair not to be the second most important person in a world where most of the people don’t even know his or her name. Where we don’t live and die by some stupid dot plot, but on whether companies actually increase their earnings by growing their businesses. I can dream, but I’m not the only one…

And now, let’s look at an abbreviated version of my recent webinar.

|

|

As a preface, I think I have a pretty good record calling major economic and market turns. My weakness is timing. I tend to be early and, as I mentioned last week, miss some opportunities near the top. My solution is to separate my own outlook from my portfolio decisions. Using multiple, systematic trading systems seems to work better, which is why I’m in business with Steve Blumenthal.

However, the annual forecasting exercise still helps. It forces me to review the data and identify the key issues that will affect my investments. Then, as the year unfolds, I can watch what actually happens and compare it with what the machines are doing to my money. When they’re not in sync, I can more intelligently evaluate why. This gives me more confidence in the systems and helps me stick with them through the inevitable bumps. The end result is better investment results over the long run. So, this isn’t just academic thought or entertainment. It matters to your and my money.

What follows is a mix of my own thoughts as well as Steve’s. We’ll look at three topics: recession probability, credit conditions, and stock valuations. We went deeper on the webinar. You can read a transcript or view a recording here, which is about three times as long with more charts.

Source: CMG Capital Management

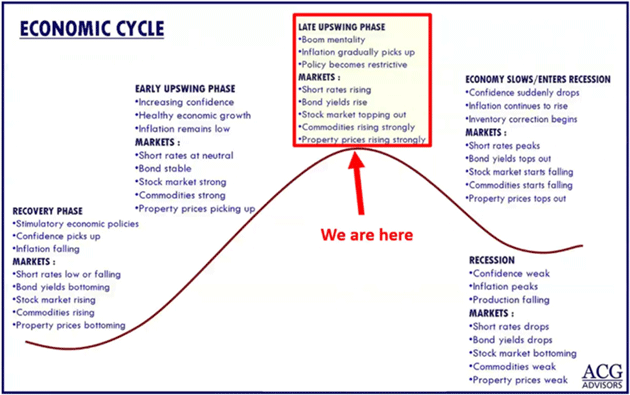

Steve started the webinar by noting we currently sit late in an economic cycle. He showed the chart above to illustrate how all cycles have expansion periods and end with recession. The longest expansion cycle (1991–2001) lasted 10 years or 120 months. The average since 1854 is 40 months and then recession, then expansion, then recession.

The 2001 post-recession recovery lasted 80 months—ending, of course, with the Great Recession. We are 114 months into the current expansion, the second-longest in US history. Again, a recession is coming. The question is when. This expansion will break the record if it persists through 2019.

If recession strikes next year, then what? Aside from the layoffs and business problems, the stock market declines on average about 37% in recessions. The last two saw 50% drops. If you think your buy-and-hold portfolio can ride that out, everything we know about behavioral finance says you are probably wrong.

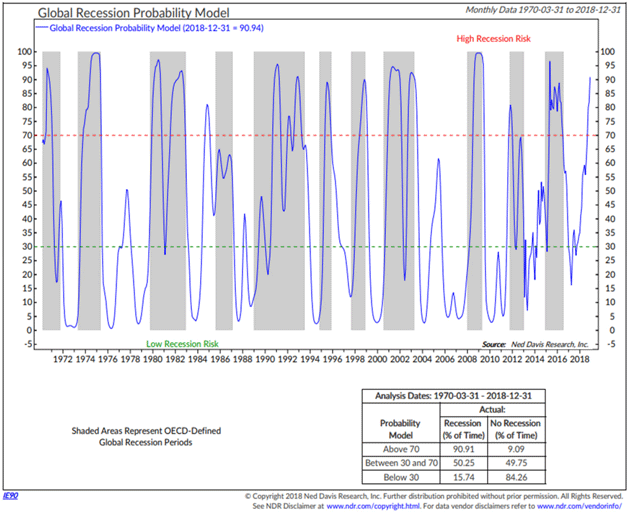

Steve watches an indicator from Ned Davis Research called the Global Recession Probability Model. I want to thank them for letting us use this.

Source: CMG Capital Management

This model measures leading indicators across 35 countries, things like money supply, yield curve, building permits, consumer and business sentiment, share prices, and manufacturing production. It’s done a good job at calling recessions, shown in the gray bars. Any reading above that red dotted line of 70 is the danger zone. When that’s occurred, over 90% of the time we’ve been in recession.

On the webinar, I pointed out that on this very useful chart, the indicator doesn’t just indicate a coming global recession. It says we’re in one. Economists identify them in hindsight. We only know we’re in a recession when we look back over the past data. So, the gray bars don’t appear in real time. They get added later.

There was a point in 2000 that we were in a recession for just one quarter. It was three years later they tell us this. Now, it didn’t change anybody’s trading when they announced it and few noticed because it was three-year-old news. But it illustrates that economists are pretty bad at actually recognizing recessions in real time. We could find out in late 2019 that a recession began sometime the prior spring.

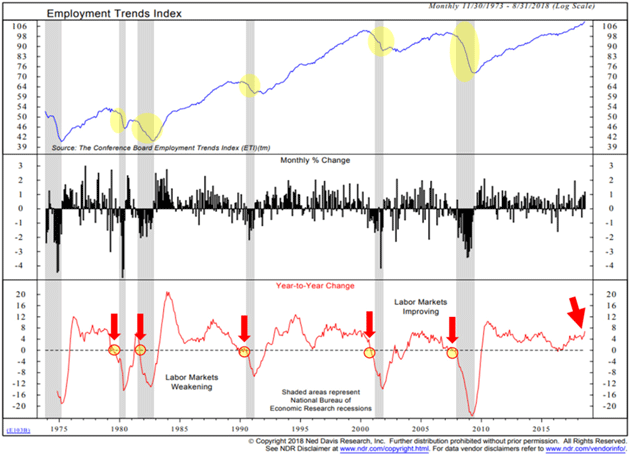

However, that NDR index is global, and we know the US economy is doing better than most. This next chart is US-specific and the lower section shows the year-to-year rate of change in their Employment Trends index. Note how when employment trends have declined, recession (gray bars) followed. So, recession risk is highest when this index’s yearly change is below zero. Conditions are currently favorable, with low recession risk.

Source: CMG Capital Management

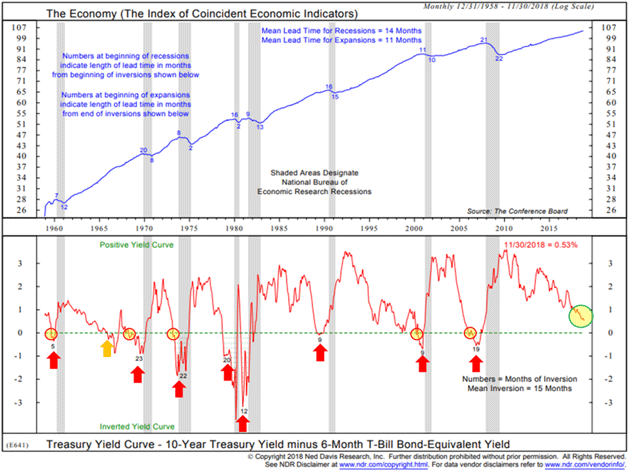

Next, let’s look at the yield curve. I explained last week that it’s flattening but not yet inverted, which would signal recession 9–15 months later. Ned Davis looks at the difference between the six-month Treasury bill and the 10-year Treasury note. We’ve highlighted inversion periods in yellow circles. Typically, it’s anywhere from 9 to 15 months between the inversion and the beginning of a recession. Presently we are not there yet (“Yet” being the operative word.)

Source: CMG Capital Management

As you’ll notice, the yield curve nearly always turns positive before we actually go into recession. I know this from painful experience. As I related last week, I called the last recession after the yield curve inverted and the markets promptly went up 20% more.

As of now, portions of the yield curve are flattening. It looks like the beginning of an inversion. The Fed seems aware of it, too, as we learned this week.

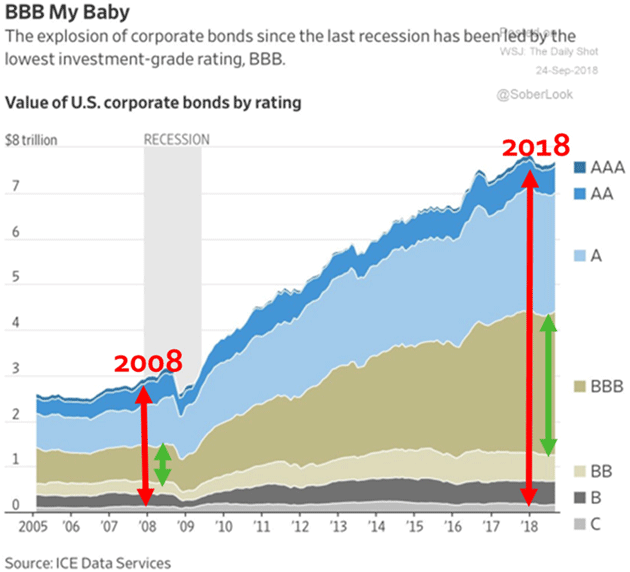

Bond Boom

Unfortunately, recession isn’t the only risk we face for 2019. I’ve talked several times this year about corporate debt and it just keeps growing. The corporate bond market is roughly three times bigger than it was in 2008. Worse, quality is dropping as quantity increases. In 2008, the US had about $3 trillion in corporate bonds outstanding. Now we have far more than that just in the BBB ratings or below.

Source: CMG Capital Management

This might be tolerable if corporations were, as a group, highly capitalized with fortress-like balance sheets. Some are, but a dangerously high number are not. Yield-hungry investors have been throwing money at companies, which they naturally accept but don’t necessarily use wisely. Some large companies live on borrowed money and don’t have the reserves to survive long without it.

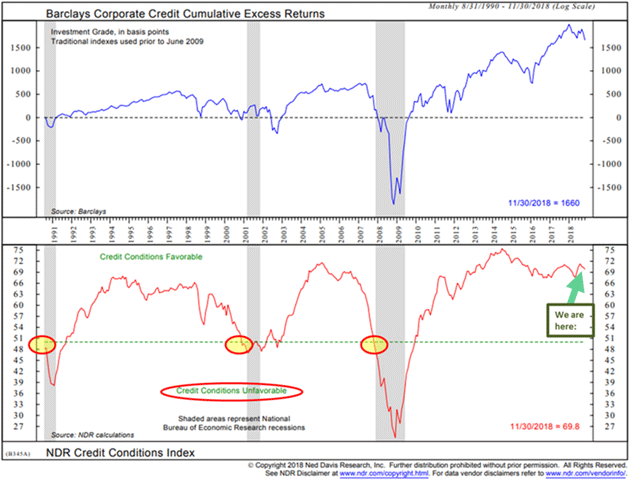

Having said that, such problems are not widespread yet and won’t necessarily become so in 2019. Here is another Ned Davis chart. Look at the lower portion, their Credit Conditions Index.

Source: CMG Capital Management

A dip below the green dotted line signals the kind of unfavorable credit conditions that would mean trouble for leveraged companies. As Warren Buffett famously said, that’s when the tide goes out and you see who’s swimming naked. The last three times happened near the beginning of recessions. Presently we are far from that point.

On the other hand, notice how fast the index fell right before the last recession. It could change considerably by this time next year if the Fed tightens too much, or federal deficits “crowd out” capital from the corporate markets, or some other stressful event occurs. So, while this looks okay for now, it is important to watch, which Steve does.

Priced to Sell

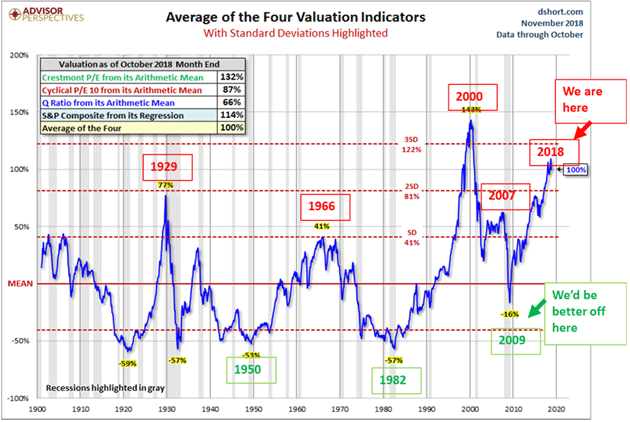

Finally, let’s get to what is most important for investors. Are your stocks safe? The quick answer is stocks are never safe. If safety is the priority, you should probably consider something else. Stocks are a “risk” asset. The real question is whether the gains adequately pay you for the risk you are taking. The higher the valuation, the less you are being paid. That makes this next chart disturbing if you’re long stocks.

Source: CMG Capital Management

We see here four popular valuation measures, the average of which crunch to the second-highest stock valuations since 1900. The highest was in 2000. We are much higher now than in 2007, which led to a 55% peak-to-trough decline.

That kind of decline won’t necessarily happen next year, but it’s all but certain within ten years. So this may not be a “sell” signal, but it sure looks like a “don’t buy” signal. And even with the recent drop, I would not bring a “buy the dip” mentality to my investment selection today.

Note the bottom section of the chart where it says, “We’d be better off here.” That’s what a buying opportunity looks like. Buying opportunities happen at the bottom of the cycle when everybody is scared. That’s true for stocks, high yields, real estate, and everything else.

When people say they’re worried about holding cash, I remind them cash is an option on the future. It’s not earning very much right now but could potentially earn a lot more when you buy at the bottom. I’m not looking at this and panicking at all. I’m rubbing my hands at the coming chance to buy solid assets cheap.

Have Yourself a Merry Little Christmas

It’s time to hit the send button. I will follow up this letter next week with my final year-end thoughts as we look to a brand-new 2019. Between now and then, my best to you and your families and friends, and here’s wishing you the best of the holiday season. The best gift I get is the time you graciously spend reading Thoughts from the Frontline. Thank you so very, very much.

Let me give you a small gift that may help lift your spirits as well. My favorite version of the famous Christmas song, Have Yourself a Merry Little Christmas, was done by Frank Sinatra, who, as Judy Garland did before him, asked the original songwriter to make the lyrics more upbeat. Judy Garland used Sinatra’s version of the lyrics later she did her TV special. You can watch the Chairman of the Board himself sing that song here.

For nostalgia buffs, look at the personalities in the audience. And if you really like nostalgia, go to the 1:54 mark in this video for Bing Crosby, later joined by Sinatra, singing I’m Dreaming of a White Christmas like nobody else has ever done. It really will make your heart a little lighter.

“Faithful friends who have been dear to us, will be near to us once more….”

Your dreaming of a new Fed policy analyst,

John Mauldin

© Mauldin Economics

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All