Global Economic Outlook - January 2019

In the old days (and by old, we mean twenty years ago), markets would start to quiet down in early December. Traders and portfolio managers would curtail their activity weeks before year-end, allowing them to get their minds out of the markets and into holiday parties. And yes, there were still a number of corporate holiday celebrations back then…

Policy makers were also reluctant to spoil the spirit of the season by making big news as the new year approached. All of this allowed business economists to enjoy a welcome respite and to prepare their annual outlooks in quiet repose.

2018, however, closed with a bang. (And it was not a celebratory bang from a fireworks show.) Markets were unsteady throughout December, amid signs of economic moderation, ongoing trade frictions, concern over monetary policy and renewed dysfunction in Washington. Declining and volatile asset prices reflected heightened uncertainty over the outlook.

Yet as we separate noise from signal, we arrive at the conclusion that 2019 should be a successful year for the global economy. Growth may not match the levels seen last year, but that is to be expected; the effects of U.S. tax reform are fading and the impact of trade restrictions is rising.

To achieve a favorable outcome, tension surrounding four situations will have to de-escalate.

- East-West Trade Relations. Our expectation is that both China and the United States will retreat from their harsh rhetoric and find ways forward. China is anxious to avoid further economic deterioration and credit stress; the U.S. administration is seeking to avoid further market upset.

- Brexit. A disorderly “no-deal” separation has been rising in likelihood, but our most-likely case is an extension of current deadlines. An agreement leaving current patterns of commerce and finance largely in place should follow.

- Political Dissonance. An opposition House has been seated in Washington, and European parliamentary elections may find extreme parties making gains. Markets have handled populism in stride up to this point, but may soon find their patience challenged.

- Monetary Policy Misgivings. The world’s central banks are, rightfully, becoming less accommodative. Some see a disconnect between the market’s expectations and those of the U.S. Federal Reserve, the European Central Bank, and the Bank of England. Furthermore, stress between governments monetary authorities is rising. Care must be taken to reach sound decisions on policy, and to communicate them effectively.

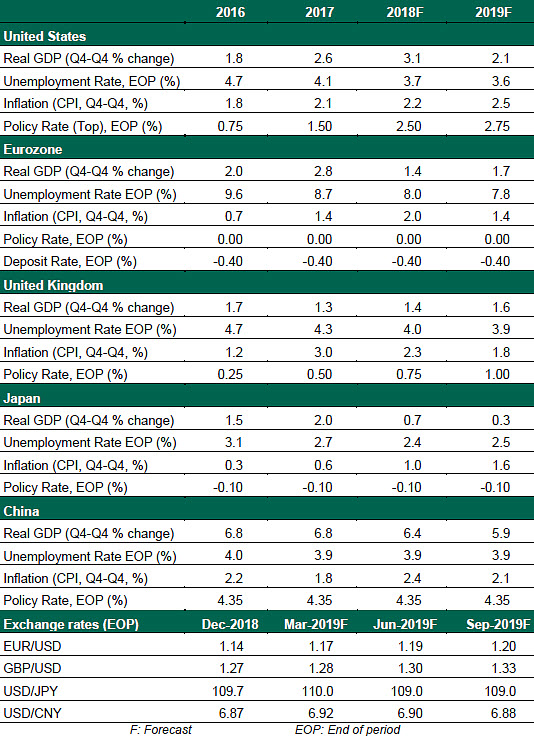

United States

- In the year ahead, the U.S. economy will likely grow at a steady but slower rate than the high levels seen in 2018, as the short-term stimulus provided by tax reform tapers. But slower growth is still growth: employment will remain strong, and inflation will continue to firm. These are the conditions under which we would expect further tightening by the Federal Reserve.

- There is upside potential, if the increased business investment envisioned by the authors of tax reform comes to fruition. And productive trade negotiations would support growth, make its benefits more wide-spread, and reduce the international tensions that characterized 2018.

- Though it remains a low probability, we cannot rule out a recession. Risks are legion: The federal government is starting the year shut down; if prolonged, a fiscal cliff scenario would have severe effects. Unsteady markets could destroy consumer and business confidence, while a rising dollar could stall exports. The current expansion has proven durable and resilient, but rising uncertainty is reflected in rising volatility.