What Headwinds? Airlines to Book Their 10th Straight Year of Profitability

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSummary:

- Despite the government shutdown, airlines beat on earnings and offer exciting guidance for 2019.

- Global airlines are expected to log their 10th straight year of profitability—an industry first.

- With incomes expanding worldwide, air travel demand is projected to outpace economic growth for the next couple of decades.

Domestic airlines weren’t exempt from the rout that hit stocks in December, the market’s worst month since the Great Recession. Shares of all four major U.S. carriers—American, Delta, United Continental and Southwest—saw double-digit losses. Delta ended December down 17.8 percent, its worst month since October 2009, when it gave back 20.3 percent.

The losses appeared to extend into the new year when, on January 3, Delta forecast slightly slower revenue growth on concerns of a global economic slowdown, not to mention the partial U.S. government shutdown—which, in its first month, cost the U.S. aviation industry about $105 million, according to consulting firm ICF. Delta’s stock lost almost 9 percent for the January 3 trading day. Shares of the other three major airlines fell as well, though not by as much.

I believe the selloff was overdone, and the market seems to have agreed. Investors who bought the dip were rewarded. From January 3 to January 25, Delta shares recouped about 4.5 percent. Over the same period, the NYSE Arca Airline Index soared about 14.7 percent.

Ancillary Revenues Helped Offset Higher Fuel Costs in 2018

Much of this enthusiasm was driven by better-than-expected full-year and fourth-quarter earnings reports from a number of domestic carriers.

For 2018, United reported an impressive earnings per share (EPS) of $7.70, up 9 percent from 2017. This came even while total fuel costs were 34 percent higher. The carrier is now projecting an EPS of between $10 and $12 this year, based not just on increased demand but also growing ancillary revenue.

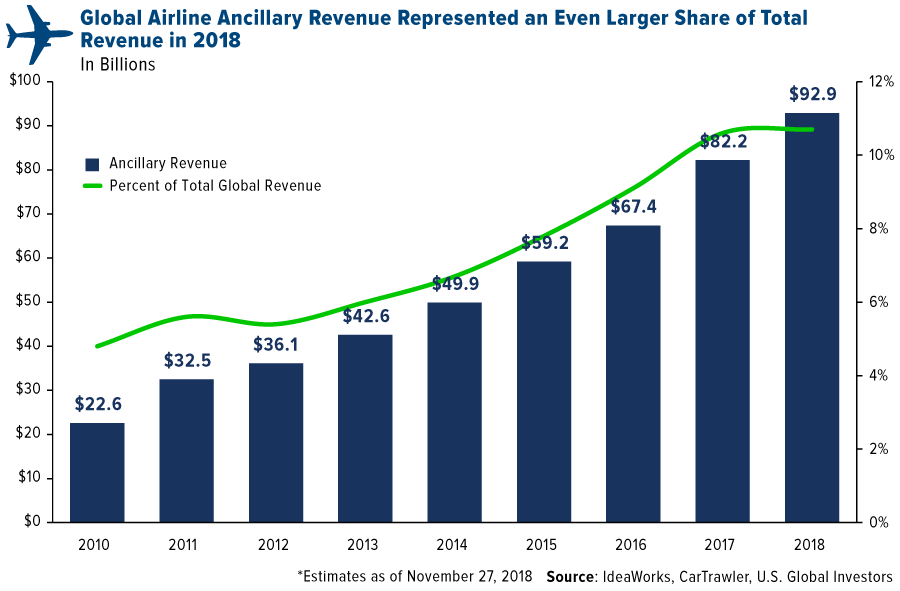

As a reminder, “ancillary revenue” includes all non-ticket items such as baggage fees, assigned seating, credit cards, loyalty programs and more. According to consultancy firm IdeaWorks, such fees on a global scale stood at a mind-boggling $92.9 billion in 2018, an increase of 312 percent since 2010. Of that amount, the “big four” U.S. airlines netted close to $27 billion. Taken together, these additional revenues have helped airlines offset rising fuel and labor costs.

Delta said as much in its own earnings report. For 2018, operating revenue was up 8 percent year-over-year to $44 billion “on an increasingly diverse revenue base, with 52 percent of revenues from premium products and non-ticket sources” (emphasis mine). The Atlanta-based carrier reported $1 billion in profits in the fourth quarter, an unbelievable increase of 240 percent from the same three months in 2017. That amounted to an EPS of $1.49, compared to $0.42 the previous year.

American also reported stellar earnings, and CEO Doug Parker tantalized the market with exciting guidance for this year. “At the midpoint of our guidance, 2019 diluted earnings per share, excluding special items, would increase approximately 40 percent versus 2018,” Parker said. Shares of American popped as much as 6.4 percent on the news.

10th Straight Year of Profitability?

Despite the recent spike in market volatility, I believe the investment case for global airlines looks favorable going forward. I’m not alone. In a press release dated January 23, Moody’s Investors Service stressed that although economic growth could be slowing worldwide, airlines are well-equipped financially for the next 12 to 18 months. The ratings agency writes that “the global passenger airlines industry is stable on steady operating margins, supported by higher passenger volumes, mixed growth in pricing and modestly lower fuel costs.”

If all goes according to plan in 2019, the global airline industry will have achieved something it’s never managed to do—that is, log 10 consecutive years of profitability. In its 2019 outlook, the International Air Transport Association (IATA) believes this will be the case, with net profits estimated at $35.5 billion, slightly ahead of 2018’s $32.3 billion. “An industry first,” the Geneva-based trade group tweeted on December 27. “2019 forecast to be 10th consecutive year of profitability for the global airline industry.”

Long-Term Outlook: Air Travel Demand Could Outpace Economic Growth

Looking ahead even further, 10 to 20 years, I think that airlines could be a profitable way to participate in the expansion of incomes around the world. In about a decade, an estimated 200 million people—many of them concentrated in developing countries such as China and India—are expected to join the middle class and, for the first time, be able to afford the cost of airfare, according to a new report by consulting firm Oliver Wyman.

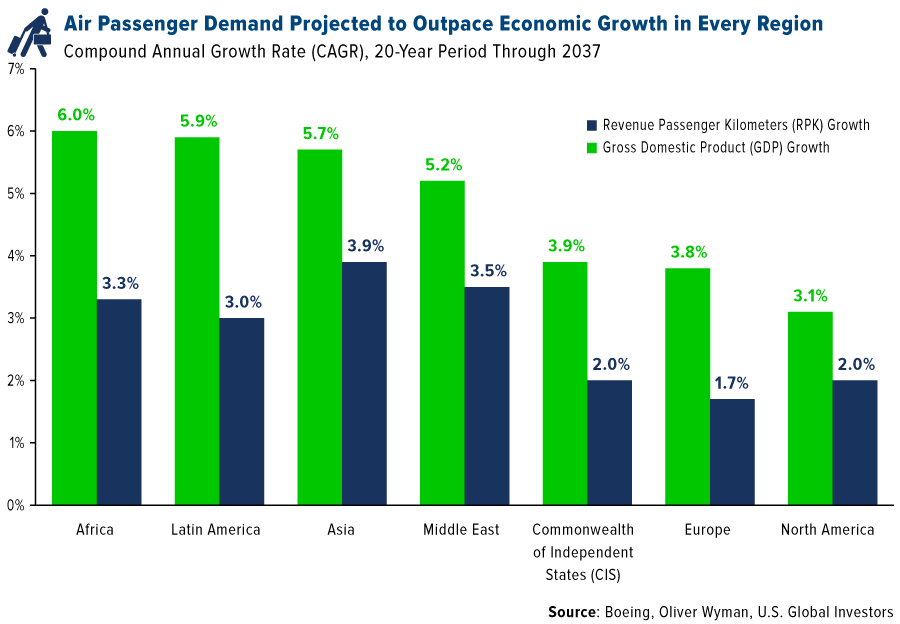

Air travel has historically been tied to change in a country’s or region’s gross domestic product (GDP), but there’s reason to believe that demand will actually outpace economic growth. For the past decade, air passenger traffic growth—as measured in revenue passenger kilometers (RPFs)—has already been faster than GDP growth on an annual basis. Analysts at Boeing now believe this trend will continue for the next 18 years. With a 6 percent compound annual growth rate (CAGR), African countries are projected to undergo the greatest expansion of any other region, followed by Latin America and Asia. Highly developed regions such as Europe and North America will likely see the weakest change year-to-year, but even then, air travel demand growth is expected to be faster than economic growth.

More Than a Billion Indian Passengers by 2040?

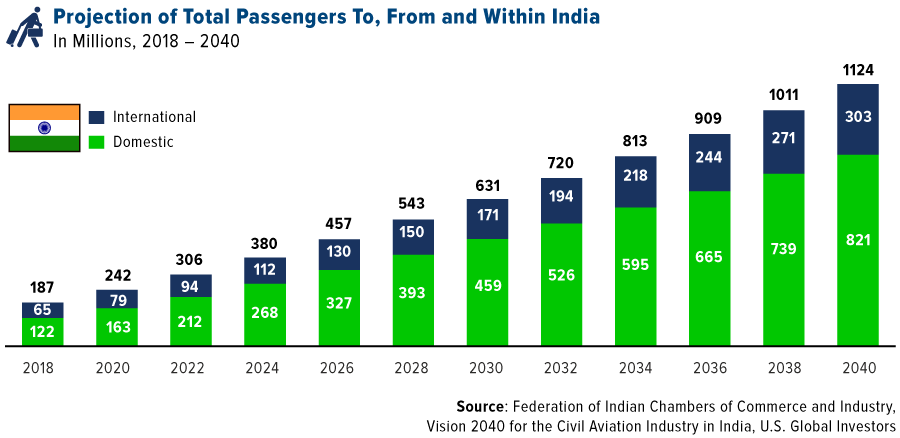

For a moment let’s look just at India, currently the second most populous country on earth. One of the world’s fastest growing regions, it’s expected to replace the U.K. this year as the fifth largest economy. According to the Federation of Indian Chambers of Commerce and Industry (FICCI), which hosted the Global Aviation Summit this month in Mumbai, India today has the world’s seventh largest aviation market with 187 million passengers. By 2022, it could be the third largest.

And if the trend continues, India could very well be the largest aviation market in the world with around 1.12 billion passengers flying to, from and within the South Asian country. That’s an incredible sixfold jump from 2018.

To accommodate so many passengers, the fleet size of scheduled airlines would need to expand dramatically. The FICCI believes the number of aircraft in India could swell from 622 in 2018 to as many as 2,360 by 2040.

This, of course, would benefit manufacturers such as Boeing, which FORTUNE just named as the most admired aerospace company in its annual list of the “World’s Most Admired Companies.”

Boeing Just Unveiled Its Self-Driving Air Taxi

The jet maker recently showed off the progress of its planned self-driving air taxi, which it is building in cooperation with ride-hailing company Uber. “Uber Air,” as it’s called, is a battery-operated, autonomously flying vehicle, with a range of about 50 miles. Morgan Stanley Research estimates that the market for “autonomous urban aircraft” could be as large as $1.5 trillion by 2040. Boeing, which is projected to have a 40 percent market share of all aircraft by 2025, is well-positioned to take the lead in this exciting new technology.

Finally, please take a moment to subscribe to the U.S. Global YouTube page, where we regularly share the latest episodes of Frank Talk Live and Gold Game Film, as well as trading tips and much more. Happy investing!

Gold Market

This week spot gold closed at $1,303.15 up $21.40per ounce, or 1.67 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.38 percent. The S&P/TSX Venture Index came in up 1.52 percent. The U.S. Trade-Weighted Dollar fell 0.54 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-20 | China Retail Sales YoY | 8.1% | 8.2% | 8.1% |

| Jan-22 | Germany ZEW Survey Current Situation | 43.0 | 27.6 | 45.3 |

| Jan-22 | Germany ZEW Survey Expectations | -18.5 | -15.0 | -17.5 |

| Jan-24 | ECB Main Refinancing Rate | 0.000% | 0.000% | 0.000% |

| Jan-28 | Hong Kong Exports YoY | -1.7% | -- | -0.8% |

| Jan-28 - Feb-4 | New Home Sales | 567k | -- | 544k |

| Jan-28 - Feb-4 | Durable Goods Orders | 0.8% | -- | 0.8% |

| Jan-28 - Feb-4 | Housing Starts | 1253k | -- | 1256k |

| Jan-29 | Conf. Board Consumer Confidence | 124.0 | -- | 128.1 |

| Jan-29 - Feb-1 | Durable Goods Orders | 0.8% | -- | 0.8% |

| Jan-29 - Feb-1 | Housing Starts | 1253k | -- | 1256k |

| Jan-30 | Germany CPI YoY | 1.6% | -- | 1.7% |

| Jan-30 | ADP Annualized QoQ | 1.6% | -- | 1.7% |

| Jan-30 | FOMC Rate Decision (Upper Bound) | 2.5% | -- | 2.5% |

| Jan-31 | Initial Jobless Claims | 216k | -- | 199k |

| Jan-31 | Caixin China PMI Mfg | 49.7 | -- | 49.7 |

| Feb-1 | Eurozone CPI Core YoY | 1.0% | -- | 1.0% |

| Feb-1 | Change in Nonfarm Payrolls | 160k | -- | 312k |

| Feb-1 | ISM Manufacturing | 54.3 | -- | 54.1 |

Strengths

- In what has been a rather rare occurrence, silver was the best performing metal this week, up 2.64 percent despite a steady trickle of silver out of the physical metal ETFs on a near daily basis. Gold traders are bullish for an 11th straight week, as surveyed by Bloomberg, on the heels of a declining dollar and speculation of a U.S.-China trade war standoff. Gold briefly rose 1 percent to the $1,300 mark on Friday, a seven-month high, as the dollar fell ahead of the Federal Reserve meeting next week, writes CNBC. The world’s largest ETF backed by gold, SPDR Gold Shares, saw holdings jump to a six-month high. George Gero, managing director of RBC Wealth Management, said that he thinks “the gold rally is going to continue as global worries escalate.”

- Turkey continues to boost its gold reserves. Holdings rose $56 million from the previous week and now totaling $20.4 billion, according to official weekly figures from the central bank in Ankara. Ray Dalio, billionaire investor and founder of Bridgewater Associates, chastised monetary policymakers for an “inappropriate desire” to tighten faster than capital markets could handle, reports Bloomberg.

- Cardinal Resources announced drilling results of 14 meters at 7.0 grams per tonne from just 69 meters from surface at the Ndongo East discovery in Ghana, only 24 kilometers from their 6 million-ounce gold discovery at Namdini. This further enhances the attractiveness of Cardinal’s region land package.

Weaknesses

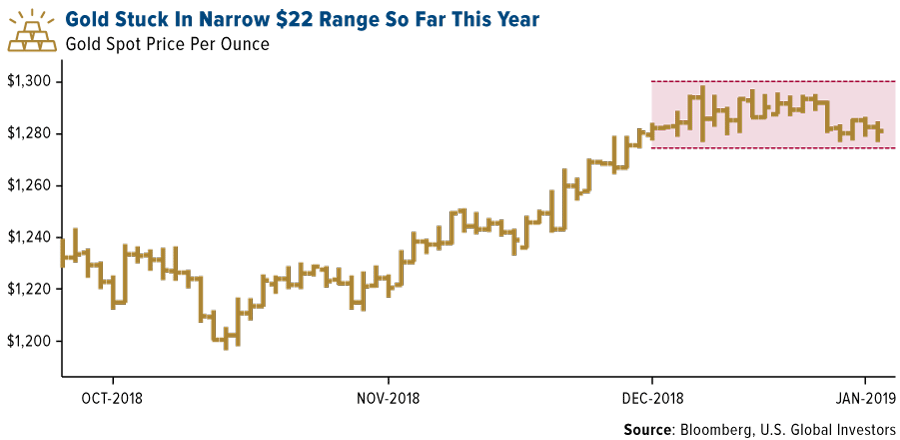

- The worst performing metal this week was palladium, down 1.29 percent . Palladium is set for its biggest weekly loss in two months on concerns that demand might slow, reports Bloomberg. The U.S.-China trade tensions could be worsening, as Secretary of Commerce Wilbur Ross said this week that the two nations remain “miles and miles” apart on trade. Gold has been stuck in a narrow trading range of $22 so far this year, remaining at or below the $1,300 an ounce level.

- Sixteen people died in an explosion at a Shaanzi Mining-operated mine in Ghana this week. The Chinese mining company was carrying out scheduled blasting at the mine. However, a group of people illegally entered the mine before knowing what was going to happen. Shaanzi shut down its operations temporarily.

- Freeport-McMoRan stock fell this week after reporting lower-than-expected profits and rising costs. Goldman Sachs says that traders are less willing to buy and sell long commodity futures because of uncertainty surrounding the trade war and other geopolitical events, writes Bloomberg’s Sebastian Pellejero.

Opportunities

- UBS analysts Giovanni Staunovo and Wayne Gordon wrote in a report this week that gold’s reaction to the stock market volatility in late 2018 has confirmed its role as a safe-haven asset. They write that gold “served investors well as a diversifier… and helped reduce portfolio swings,” and that “these qualities should remain highly relevant for investors this year as the business cycle matures further.” According to SkyBridge Capital, gold could become even more attractive in 2020, as a possible U.S. recession could lead the Fed to loosen monetary policy. Troy Gayseki, senior portfolio manager, told Bloomberg that “it is plausible that the next great monetary easing starts in later 2020, which of course would be very supportive for precious metals.”

- With the recent mega gold miner mergers (Barrick-Randgold and Newmont-Goldcorp), many are speculating what might come next. BMO Capital Markets writes that we could see more mergers to form larger gold miners. Meanwhile, Credit Suisse writes that asset sales are more likely, as Newmont-Goldcorp likely plan to divest non-core assets over the next few years. Additionally, rising gold prices might hinder further gold deals, as this makes valuations less attractive, writes Bloomberg’s Aoyon Ashraf.

- Continuing M&A news, some were speculating that Gold Fields might merge with AngloGold. However, Gold Fields responded a day later saying that news was incorrect. Kinross Gold appears to be open to asset buying opportunities, telling analysts at a conference this week that “we’ll just have to wait and see what comes out” of the two big mergers. JPMorgan wrote this week that it is positive about the recent Newmont-Goldcorp merger, saying that it creates a large “gold miner that should appeal to generalist investors looking for liquid, low drama gold exposure.”

Threats

- Investor Mark Mobius said in a Bloomberg interview this week that he expects gold to stay relatively flat this year due to the Fed potentially raising interest rates. However, Mobius did say that “everybody should have gold, no question about that” and that investors should maybe have “10 percent of their assets in gold.”

- The Bank of England has denied Venezuelan President Nicolas Maduro’s request to pull $1.2 billion worth of gold out of the bank. This comes at a time when the U.K., along with the U.S. and other countries, recognized opposition leader Juan Guaido as the legitimate president of Venezuela. Some are speculating whether or not the bank will eventually allow Guaido to withdraw the gold, as Venezuela’s economy has been struggling.

- Open interest in gold futures reached an over-five-year high on the Multi Commodity Exchange of India, reports Business Standard. Previous years when the open interest ratio hit highs, gold has pulled back, according to data from Seaport Global.

Index Summary

- The major market indices finished mostly up this week. The Dow Jones Industrial Average gained 0.12 percent. The S&P 500 Stock Index fell 0.22 percent, while the Nasdaq Composite climbed 0.11 percent. The Russell 2000 small capitalization index gained 0.02 percent this week.

- The Hang Seng Composite gained 1.83 percent this week; while Taiwan was also up 1.36 percent and the KOSPI rose 2.52 percent.

- The 10-year Treasury bond yield fell 3 basis points to 2.752 percent.

Domestic Equity Market

Strengths

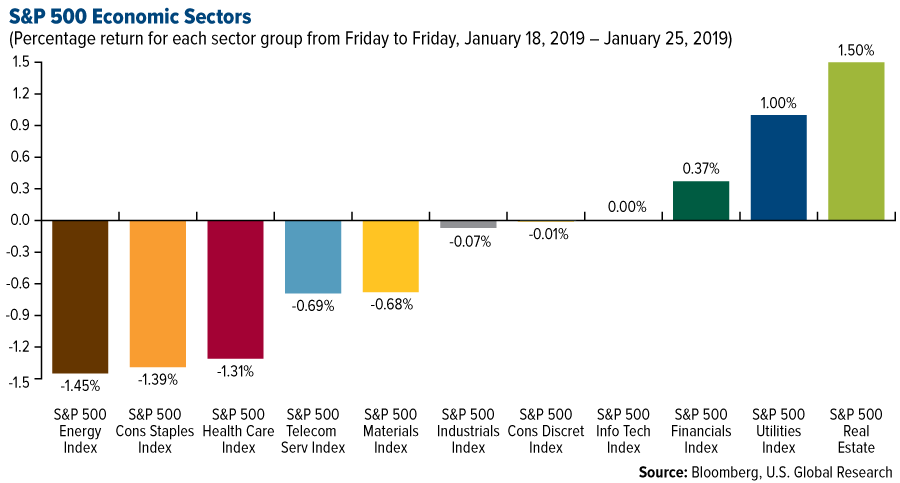

- Real estate was the best performing sector of the week, increasing by 1.5 percent versus an overall decrease of 0.26 percent for the S&P 500.

- Xilinx Inc. was the best performing stock for the week, increasing 17.86 percent.

- January flash Manufacturing PMI for the U.S. rose to 54.9 from 53.8 the previous month. Both output and employment rose from December as well. However, January Services PMI fell to 54.2 from 54.4 in December.

Weaknesses

- Energy was the worst performing sector for the week, decreasing by 1.45 percent versus an overall decrease of 0.26 percent for the S&P 500.

- Resmed Inc. was the worst performing stock for the week, falling 19.93 percent.

- The Conference Board Leading Economic Index, which measures U.S. business trends, fell 0.1 percent in December to 111.7. Economists polled by The Wall Street Journal expected a 0.1 percent decline in the index.

Opportunities

- U.S. jobless claims fell 13,000 to 199,000 last week, the lowest level since 1969, signaling the labor market remains tight even amid the government shutdown.

- U.S. airlines rallied this week as American Airlines Group Inc. and Southwest Airlines Co. predicted strong revenue gains after surpassing Wall Street’s profit estimates late last year.

- Shares of beaten down homebuilders during 2018 have bounced back so far this year, which is a positive sign for the U.S. economy, particularly amid fresh worries over a stagnant housing market and slowing global growth. The National Association of Home Builders’ housing-market index showed a rebound in home builder confidence this month, helped by a gradual decline in mortgage rates, along with strong employment growth.

Threats

- An offer by two Chinese vice-ministers to travel to the United States this week for preparatory trade talks was rejected by the Trump administration, reports the Financial Times. The U.S. turned down the offer due to lack of progress on two important issues. It highlights the difficulty that Washington and Beijing will face in trying to reach an agreement by the March 1 deadline. The stalemate could ultimately derail the higher-level meeting next week between the two countries and cause more worry for financial markets, the article explains.

- The longest government shutdown on record has been blocking the collection and reporting of many key economic numbers, Bloomberg reports. The disruptions are depriving the Federal Reserve of crucial data in particular, as policy makers are feeling their way toward a peak in the rate-hiking cycle — a period when theoretical frameworks are less useful and fresh data become even more important.

- Ray Dalio, founder of the world's biggest hedge fund, warned on Tuesday of a "significant risk" of a U.S. recession in 2020. "It's going to be globally a slow up. It's not just the United States; it's Europe and it's China and Japan," Dalio said in an interview with CNBC.

The Economy and Bond Market

Strengths

- Mutual funds focused on municipal bonds pulled in more than $2.5 billion over the past two weeks, according to Lipper U.S. Fund Flows data, signaling a shift in sentiment among investors who retreated from the market for much of the fourth quarter amid concerns about rising interest rates.

- Wages are growing at the fastest pace since 2008 in the U.K., reports Bloomberg. Average earnings, excluding bonuses, continued to increase an annual 3.3 percent in the three months through November and unemployment fell to 4 percent.

- U.S. households are unlikely to cause the next financial crisis, according to Richard Gluck, author of the Global Investment Strategy blog. Gluck cited a chart of household debt payments to disposable income, based on quarterly data compiled by the Federal Reserve. The third-quarter figure was 9.8 percent, the lowest since at least 1980.

Weaknesses

- The annual economic growth rate in China is now at the slowest pace since 1990, reports the Wall St. Journal. The country reported a 6.6 percent growth rate for 2018 on Monday. The economic slowdown, which has been sharper than Beijing expected, deepened in the last months of 2018, with fourth quarter growth rising 6.4 percent from a year earlier.

- According to a PwC survey released alongside the World Economic Forum (WEF) in Davos, there is a record jump in pessimism among CEOs from world’s leading companies about global growth prospects, reports CNBC. From a survey of over 1,300 CEOs, nearly 30 percent expect global growth to decline in the next 12 months, roughly six times the level of last year.

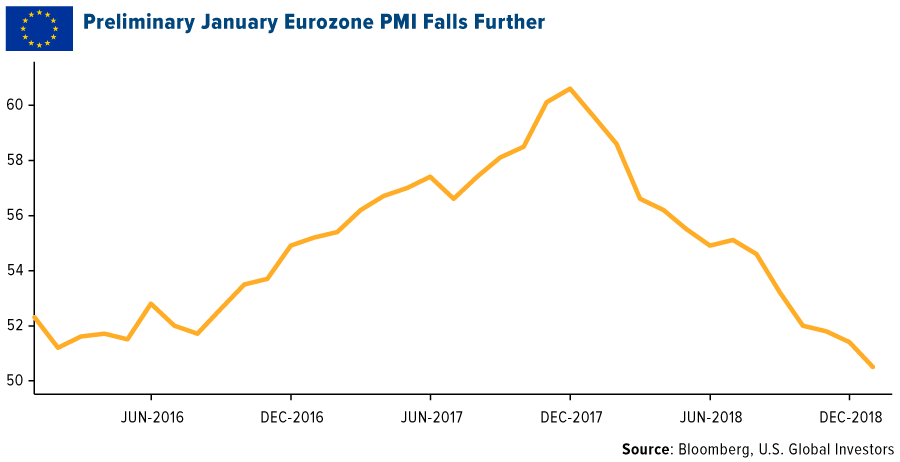

- The flash PMI reading in the euro-area fell to a 66-month low of 50.7 in January from 51.1 in December, below 51.4 consensuses. While Germany’s services PMI expanded, manufacturing PMI fell into contraction. In addition, a further deterioration in the French services PMI to more than offset a rebound in the manufacturing PMI, sending the composite reading to the lowest in four years.

Opportunities

- The PBOC debuted a targeted version of the medium-term lending tool it unveiled last month, offering 257.5 billion yuan ($38 billion) of liquidity to banks. The move, seen as a quasi-rate cut by some analysts, aims to spur lending to small firms and ease cash demand before the Spring Festival. The PBOC's first injection via its targeted medium-term lending facility reflects strong demand from banks for additional funding and suggests lending may have a good start in 2019, Bloomberg Economics said.

- “China’s stimulus measures are seen easing financial stress at the nation’s debt-laden town builders, making them among the top picks for investors this year,” reports Bloomberg, citing data from a Bloomberg survey. Sentiment on LGFVs, typically owned by local governments to carry out infrastructure projects, is turning more positive as China’s targeted easing measures and fiscal support have cut their funding costs.

- Global stocks are gaining momentum, reports Business Insider, with Asian markets hitting their highest level in more than seven weeks. As the article states, renewed enthusiasm for the U.S. technology sector is one reason for this. Several U.S.-based chipmakers reported earnings on Thursday, many delivering better-than-expected results, helping to boost their share prices.

Threats

- The International Monetary Fund has cut its global growth forecast in 2019 to 3.5 percent, down from 3.7 percent forecast in October and 3.9 percent expected in July. The IMF said that global expansion has weakened and the risk of a sharper decline in growth has increased. The update also noted a number of the usual suspects, including trade tensions, financial market stability and politics. Europe is also a key driver of the latest downgrade, while many emerging markets also saw their estimates lowered.

- If President Trump follows through on a threat to impose duties on European Union cars and auto parts, Jean-Luc Demarty, director general for trade in the European Commission, said that the EU is prepared to hit the U.S. with $23 billion in tariffs, reports Fortune. “We shall continue to face a U.S. administration that is content to threaten trade measures even against close allies and partners and, in general, to disrupt the status quo in pursuit of its goals,” Demarty told a European Parliament committee.

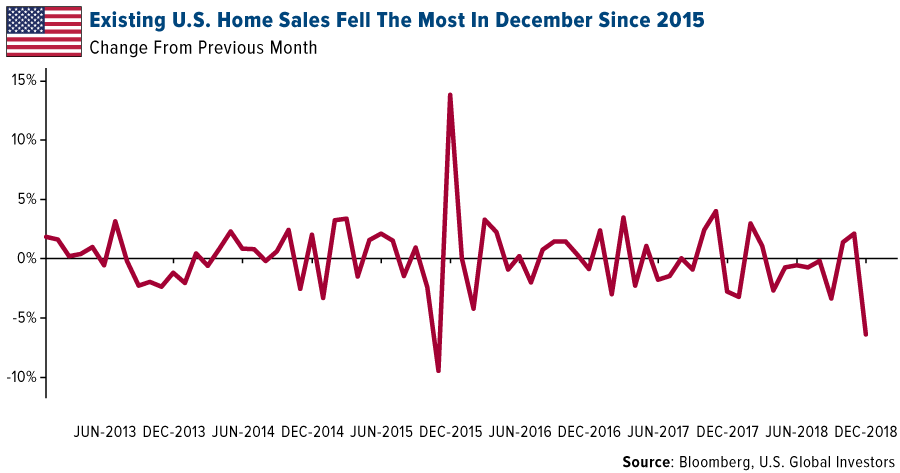

- U.S. existing homes fell to the weakest pace in more than three years, falling short of estimates and indicating the housing market remained in a slowdown as the year ended. Buyers pulled back in the latter half of 2018, as rising mortgage rates, high home prices, a volatile stock market, concerns that prices would start declining and anxiety about the national political situation all caused a number of buyers to hit pause.

Energy and Natural Resources Market

Strengths

- Lumber was the best performing major commodity this week rising 7.66 percent. The commodity rose to a four-month high after supplies heading into the spring building season are sparse, according to industry insiders.

- The best performing sector this week was the NYSE Arca Gold Miners Index. The index rose 3.38 percent after the price of gold rose above $1,300 an ounce, propelled by a drop in the U.S. dollar.

- The best performing stock for the week was Fresnillo. The Mexican precious metals miner rose 6.67 percent after UBS raised its recommendation on the stock to a “Buy” after the company reported record annual silver production.

Weaknesses

- Natural gas was the worst performing commodity this week. The commodity dropped 8.79 percent after buyers backed off as warmer temperatures are forecast across the U.S.

- The worst performing sector this week was oil and gas exploration and development. The group dropped 4.28 percent after an unexpected build in U.S. crude inventories.

- The worst performing stock for the week was Freeport-McMoRan Inc. The U.S. major base metals producer dropped 10.51 percent after the company reported a smaller-than-expected quarterly profit as metal prices fell, and said costs to produce copper will be 62 percent higher this year.

Opportunities

- Bloomberg reported that a Chinese delegation including deputy ministers will arrive in Washington on Monday to prepare for high-level trade talks led by Vice Premier Liu He.

- The International Energy Agency’s (IEA) chief Fatih Birol doesn’t see any signs of oil demand declining despite China’s slowdown. Director Birol also suggested he expects China’s demand to grow by 1 million barrels per day this year.

- Metals and mining stocks are rising after copper, gold and silver outperformed the metals group on weaker U.S. Dollar, as well as optimism for trade talks between U.S.-China.

Threats

- China’s economy cooled in the fourth quarter under pressure from faltering domestic demand and bruising U.S. tariffs, dragging 2018 growth to the lowest in nearly three decades and pressuring Beijing to roll out more stimulus to avert a sharper slowdown. Fourth quarter GDP grew at 6.4 percent, below the 6.5 percent expected.

- The International Monetary Fund (IMF) cut its growth forecast for the world for the second time in three months. Citing a bigger-than-expected slowdown in China-U.S. trade tensions, a possible no “Brexit” deal and weakness in Europe and emerging markets. The IMF expects global growth to decline to 3.5 percent this year.

- European macroeconomic data disappointed again this week. The composite PMI fell to 50.7 this month, below forecasts and the lowest since 2013, with the manufacturing index gauge even worse.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 3.4 percent. Improving global sentiment and reduced geopolitical tension pushed stocks trading on the Istanbul exchange higher for a second week in a row. Year-to-date Turkey is the best performing market in dollar terms, with banks outperforming.

- The Turkish lira was the best relative performing currency this week, gaining 1.2 percent against the U.S. dollar. Fading diplomatic tension between US and Turkey supports the currency appreciation against the dollar, but it could escalate quickly if planned Turkish military offensive in northern Syria results in clashes with the U.S.-allied Kurds.

- The industrial sector was the best performing sector among eastern European markets this week.

Weaknesses

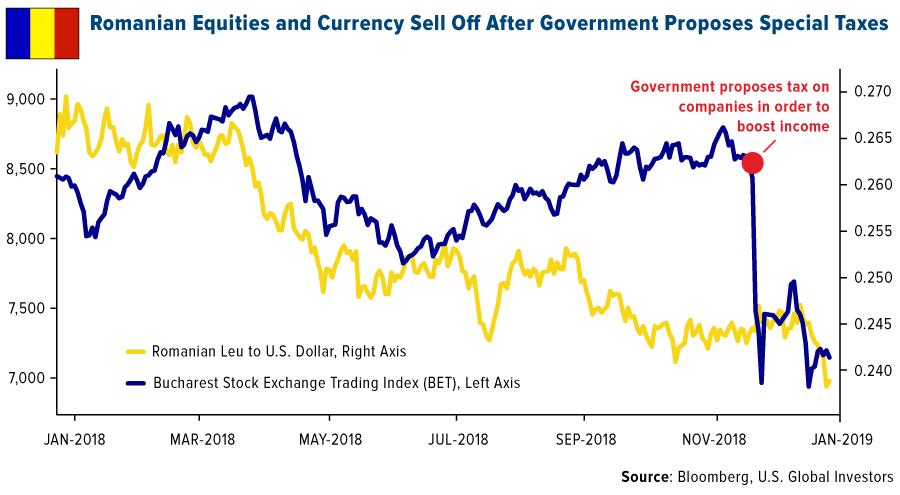

- Romania was the worst performing country this week, losing 2 percent. Banks continue to underperform after the government introduced a tax on banks’ assets in order to increase revenue and avoid breaching 3 percent of the GDP budget deficit.

- The Romanian leu was the worst performing currency this week, losing 1 percent against the U.S. dollar. The currency sold off on concerns among investors that the governing Social Democrats may propose more controversial policies to boost income after imposing tax on banks’ assets.

- Health care was the worst performing sector among eastern European markets this week.

Opportunities

- The president of European Central Bank Mario Draghi issued a darker outlook for the region’s economy; however, he said that the bank is ready to act if the slowdown takes a turn for the worse. As expected, the bank kept all rates unchanged this week. The first interest rate hikes could come in 2020, rather than later this year.

- Poland opened its first Polish House during the World Economic Forum in Davos where politicians and enterprises met to seek closer ties with the Polish economy. Interest in the largest central emerging Europe country was high in Davos and investors were impressed with the country’s strong macroeconomic performance, including around 5 percent GDP in 2018.

- Momentum in emerging markets is likely to pick up as adverse global factors are already at least partly priced in, says Valentijn van Nieuwenhuijzen, the global CIO for NN Investment Partners in Warsaw. He sees Poland among preferred emerging market countries, citing a solid domestic macro picture.

Threats

- A report published by Bloomberg this week, says the Federal Reserve is looking into whether Deutsche Bank’s U.S. arm was involved in moving suspicious funds out of the Estonian branch of Danske Bank. Danske Bank is already being investigated in Denmark, Estonia, the U.K. and the U.S. over 200 billion euros worth of suspicious payments through its Estonian branch between 2007 and 2015. Deutsche Bank is the largest bank in Germany, with a large presence in Europe.

- The International Monetary Fund downgraded its 2019 euro-area gross domestic product to 1.6 percent from 1.8 percent in 2018. It highlighted weakness in Germany and public debt problems in Italy. Projected growth in Italy this year is the lowest among individually listed nations at 0.6 percent.

- Eurozone January Manufacturing PMI fell to 50.7 from 51.1 in December, the lowest reading in 66 months, but it remains above the 50 mark that separates growth from contraction. Ongoing automobile sector weakness, Brexit worries, trade war fears and protests in France were the main factors contributing to this economic slowdown.

China Region

Strengths

- Korea’s KOSPI jumped 2.52 percent for the week, matched by Thailand’s SET Index, which also climbed 2.52 percent. South Korea’s fourth quarter GDP print came in stronger than expected, at 3.1 percent year-over-year growth.

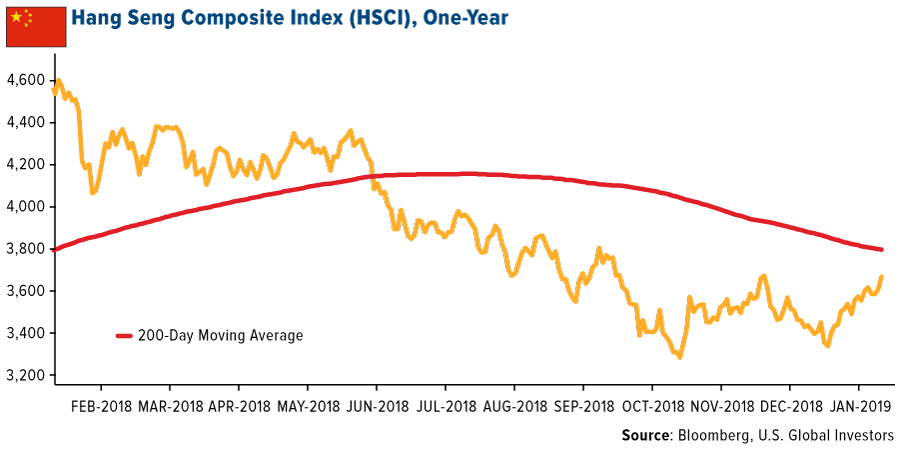

- The industrials sector was the top performer in Hong Kong’s Hang Seng Composite Index for the week.

- The Hang Seng Composite Index is bumping up right on its early December 2018 highs and approaching new multi-month highs.

Weaknesses

- Singapore and India finished down for the week, with the Straits Times Total Return Index declining by 69 basis points as the SENSEX and NIFTY Indices in India dropped by 99 and 112 basis points, respectively.

- The materials sector was the only one in Hong Kong’s HSCI Index to close out the week in the red, dropping 75 basis points.

- We received a few notable GDP prints as well. China’s fourth quarter GDP reading came in at 6.4 percent, dropping down into the range of 6-6.5 percent suggested for the state for the current year’s outlook and rounding out last year’s growth rate at about 6.6 percent overall. The Philippines’ fourth quarter GDP clocked in at 6.1 percent—definitely not too shabby, but below analysts’ expectations nonetheless—analysts were looking for a 6.3 percent print. On the bright side, the prior quarter’s print was revised up by 0.1 percent.

Opportunities

- The Nikkei Asian Review this week highlighted a recent report by New York-based research firm eMarketer that China “is expected to overtake the U.S. to become the world’s largest consumer of goods this year despite a slowdown in the economy and retail sales.” The forecast, the article went on, is based on estimates of retail sales growth of some 7.5 percent for China and 3.3 percent for the United States. Monica Peart, the senor forecasting director at eMarketer, explained, “The rising incomes of Chinese over the past years have catapulted millions into a middle class that has experienced a marked expansion in purchasing power.”

- Late last week Bloomberg News reported that Indonesia’s e-commerce marketplace unicorn PT Bukalapak.com is preparing to complete a new round of fundraising. CEO Achmad Zaky stated last year that the company had already breached a valuation of more than $1 billion. Southeast Asia’s largest economy is becoming a hotly-contested e-commerce market, and Bukalapak.com is now the second most-visited site after PT Tokopedia. Bukalapak’s investors, the article continues, include Singapore’s sovereign wealth fund, China’s Ant Financial, and Indonesia’s Emtek, while Tokopedia’s backers include Alibaba and Softbank.

- Mark Mobius, the veteran emerging markets investor, suggested from Singapore on Friday to Bloomberg News that now is the time to buy developing nations’ equities, and noted he particularly liked India.

Threats

- The trade war resumption/escalation threat continues, even as markets demonstrated a touch of optimism heading into the trade talks next week. U.S. Commerce Secretary Wilbur Ross suggested that China and the United States remain “miles and miles from getting a resolution,” while HK CEO Carrie Lam indicated that it seems unlikely—in her opinion, presumably—that all issues will be resolved in a timely fashion. All eyes will be watching for reports of progress or lack thereof from the talks next week.

- The port of Hong Kong fell in the rankings to the seventh-busiest in the world, in what may well be a sign of the slowdown and tariff concerns with respect to the mainland Chinese economy.

- The New York Times reported this week that Philippine legislators are weighing a law that would consider children as young as nine years of age criminally responsible for their actions. The previous juvenile justice law, passed in 2006, had set the minimum age for criminal liability at age 15.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended January 25 was Delphy, up 141.90 percent.

- Enterprise blockchain startup Symbiont closed a $20 million Series-B funding round led by Nasdaq Ventures, writes Coindesk. The firm previously raised a combined $15.4 million from a seed round in 2014 and Series A in 2017, but has kept a low profile as market movements have overshadowed the enterprise sector, the article continues. Now, as part of the investment, Nasdaq Financial Framework will integrate Symbiont’s Assembly smart contracts platform to explore new avenues involving tokenization.

- On Thursday, the New York Department of Financial Services (NYDFS) announced that it is granting stock trading startup Robinhood and bitcoin ATM provider LibertyX virtual currency licenses for their latest subsidiaries – as well as a money transmission license for Robinhood. In a statement by NYDFS superintendent Maria Vullo, she commented that New York has a “flourishing financial technology sector” thanks in part to its regulatory regime. Around 16 different companies now hold this virtual currency license, Coindesk reports, which NYDFS launched in 2015.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended January 25 was Kambria, down 57.31 percent.

- The company behind the $60 million blockchain project known as Nebulas, is laying off 60 percent of its workforce, reports Coindesk. A spokesperson for the company said that one main reason for the layoffs was that the market price kept going down. There have already been a series of layoffs that have seen peripheral elements of its roadmap shelved, the article continues, at least pending a recovery in the market for Nebulas’ NAS token.

- The CBOE pulled the proposal for the VanEck/SolidX physically backed, institutional style bitcoin ETF this week, reports MarketWatch. The chief executive of VanEck told CNBC the reason for pulling the filing was a combination of the government shutdown and market concerns. Surprisingly, on Thursday, the price of bitcoin was still holding firm despite the news.

Opportunities

- According to the GTI Global Strength Technical Indicator for bitcoin, the digital currency is nearing oversold levels, reports Bloomberg, clocking in at 35.6. That makes this the lowest level since December, with the price stabilizing around $3,500. Looking at the chart below, this could mean bitcoin is gearing up for a short-term rally.

- MarketWatch reports that in this day and age, digital estate planning is becoming more and more serious. The article specifically dives into three ways that investors can ensure their loved ones can easily access their bitcoin or other digital assets once they are gone. Step one is to create an inventory of all digital assets and accounts. Step two is to organize your credentials – making sure all logins are recorded in a single and secure place. Step three is to name a digital fiduciary or executor in your will.

- IBM is being joined by Aetna, PNC Bank, Anthem and others in the health care space to improve the way sensitive data is shared and to make health claims and transactions more efficient, reports Coindesk. The driving force behind these improvements, intended for close to 100 million health care plans, is a “blockchain-based ecosystem,” according to IBM.

Threats

- According to the Bank of International Settlements (BIS), bitcoin’s sustainability might be at risk. Raphael Auer, principal economist in the monetary and economic department at the BIS, believes that drawbacks with the digital currency’s proof-of-work concept uncover significant economic problems, reports Market Watch. “If the incentives of potential attackers are analyzed, it is clear that the cost of economic payment finality is extreme,” Auer says. He also believes that as mining income deteriorates, more people will leave the proof-of-work system, resulting in the deterioration of liquidity.

- CNN reported that the hacker known as “ExploitDOT” was attempting to sell know-your-customer (KYC) data from leading cryptocurrency exchanges on the dark web. The hacker then confirmed that they were in fact trying to sell the data in an attempt to clear their name from crypto news outlets claiming the news was fake.

- According to analysts at JPMorgan Chase & Co., the production-weighted cash cost to mine one bitcoin averaged around $4,000 globally in the fourth quarter of 2018, writes Bloomberg. Bitcoin has been trading around $3,600 or lower recently, which demonstrates that many miners are losing money mining each coin. There are some miners with lower costs, such as Chinese miners at $2,400 per coin, who leverage direct power purchasing agreements with electricity generations who are selling excess power generation

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits