After two years of solid growth, a synchronized global slowdown is underway. The U.S. economy appears to have lost momentum, growth has been falling in the eurozone, China is struggling to sustain economic momentum and lingering Brexit-related uncertainty continues to take a toll on the British economy. This has raised concerns about the longevity of the current expansion.

Though growth rates may not match recent performances, we do not anticipate a recession anytime soon. The U.S. economy will downshift naturally as the impact of fiscal stimulus from tax reform wanes and monetary policy normalization continues. Even though we envisage a gradual decline in U.S.-China trade tensions, the Chinese economy should continue to moderate amid weaker external demand and internal rebalancing. European growth should recover from the recent soft patch as favorable domestic drivers are still in place. And we continue to expect a “soft” Brexit that broadly maintains strong commercial ties with the European Union.

The key downside risks to this outlook are an escalation or broadening of the U.S.-China trade war, a disorderly Brexit and another rise in populist sentiment.

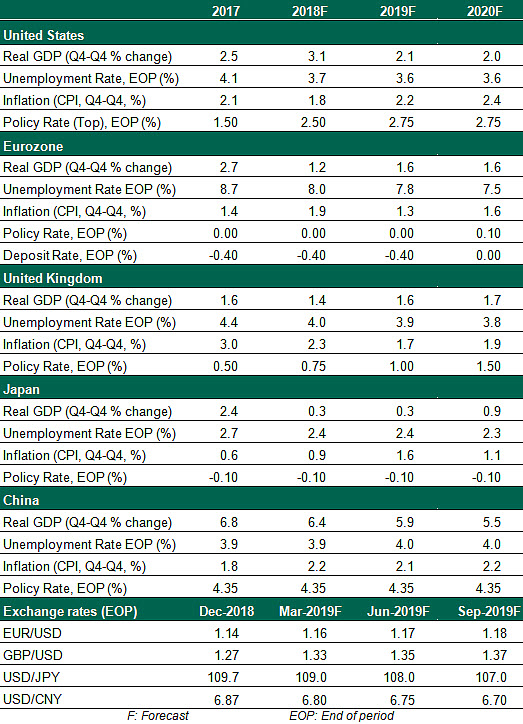

United States

- The federal government has reopened after a record-setting shutdown. We expect that leaders on both sides share a distaste for further standoffs and will find ways to agreements that keep the economy running smoothly. Reduced spending by furloughed workers and suspended contractors will weigh on first-quarter economic growth, but the impasse does not significantly impair our full-year outlook.

- U.S. consumers and businesses alike have benefitted from lower energy prices, which have stabilized after a steady descent in the fourth quarter. This fall will contain the growth of headline inflation. The combination of below-target inflation and delayed data releases from the shutdown gives us confidence that the Federal Reserve will undertake no rate actions until mid-year. We expect one rate increase later in the year to conclude the rising cycle. Upcoming Federal Reserve meetings should give us greater clarity into the timing and terminal level of its balance sheet holdings.

Eurozone

- Owing to both transitory and fundamental factors, growth in the eurozone continues to disappoint . Exports, which were a key contributor to growth over the past few quarters, will prove to be a drag amid a slowing global landscape, but domestic fundamentals will continue to underpin the economy. Consumption should remain strong in 2019 as unemployment continues to trend lower, inflation has moderated due to falling oil prices, wages should continue to rise and monetary policy will likely remain supportive. A less austere fiscal stance will also support growth.

United Kingdom

- An expected defeat in the U.K. parliament of the proposed Brexit deal has thrown the process into further disarray. The persistent uncertainty is taking a toll on the economy: production is falling and talent is moving out of the country. The likelihood of a disorderly “no-deal” Brexit is still elevated, but in our base case, we expect an extension of deadlines followed by a “Brexit in name only” agreement (keeping existing arrangements of business and finance in place).

- A looser fiscal stance coupled with an “orderly” Brexit would put the U.K. economy back on track. Firmer wages will support consumption, the impact will be partially mitigated from the benefits freeze and higher interest rates (we predict one hike in 2019 and two in 2020 of 25 basis points each). The support to net exports from strong global growth and a weaker pound should continue to fade.

Japan

- Consumption and investment are likely to be the engines of growth this year and next, as moderating global growth and rising protectionist sentiment weigh on exports. A healthy labor market will provide impetus to consumption, while investments will remain firm in preparation for the 2020 Tokyo Olympics. We expect the government to stick to the October 2019 timeline for the implementation of a consumption tax hike. However, there is a risk that further deterioration in economic conditions could lead to yet another delay in implementation.

The Bank of Japan will continue to remain in a highly accommodative mode (no hikes expected) through 2019 and 2020, as the 2% inflation target remains elusive.

China

- The Chinese government’s drive to scale back leveraging along with the current trade frictions with the U.S. are the key challenges currently faced by the Chinese economy. China’s full-year growth of 6.6% in 2018 was its slowest pace since 1990. Chinese households are also holding off their spending amid heightened uncertainties.

- We expect the economy to continue to slow further this year and next with the growth rate falling below 6.0% year-over-year. Policymakers will likely continue to deploy easing measures to support the economy, effectively indicating a retreat from financial reforms. China will be cautious in using their currency as a tool in combating the slowdown, as a notable fall in the Chinese yuan would draw the attention of the U.S. administration. On the trade front, we expect both China and the U.S. to retreat from punitive stances and find ways forward.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Global Economic Forecast – February 2019

© Northern Trust

Read more commentaries by Northern Trust