As we closed out 2018, a fair amount of our time was spent looking into 2019; discussing the themes that we thought would drive markets. This discussion helped narrow down a list of what we felt commanded focus. Each of the themes has multiple facets and, in some cases, many possible outcomes. Over the next couple of months, we will be expanding on these key themes in greater detail. We welcome your feedback and thoughts.

2019 promises to be another volatile year in the markets. We believe the fixed income markets will experience similar ups and downs as we experienced in 2018, however, with much greater uncertainty and the potential for more severe outcomes. With the greater uncertainty will come significant dispersion and differentiation, especially in the credit markets. Active management that focuses on resiliency and the ability to adapt to the volatility will be required. Our concerns around passive management are more amplified after the moves we saw in 2018. Additionally, many managers with generic over-weights in credit felt significant pain in 2018 and were dealt a friendly reminder of the importance of security selection and security avoidance – both crucial components of active management. We are definitively moving into a bond picker’s market.

The core of our thesis around heightened volatility in 2019 rests on the view that we are coming off a period of money being priced below its natural rate. The artificial rate environment created capital market distortions and, in many places, poor investment of capital in the economy. The mispricing of money also resulted in behaviors and actions by individuals that created some unhealthy imbalances in the markets. We believe we will continue to contend with these imbalances and the re-pricing of risk throughout 2019.

The intended and unintended consequences of the great monetary experiment (QE) are still widely felt in the economy and markets—some positive and some very negative. We believe that as money is repriced to a natural/neutral rate, the residual outcome is (and will be) a significant repricing of the excesses created by the cheap money. Some of these show up in our themes for 2019.

Many of us were raised with the mantra to ‘not fight the Fed’. We believe this is a healthy reminder and one that should be heeded again. Central Banks around the globe are scrambling to reverse the great monetary policy experiment to prepare for the next rescue. The importance of reversing course is increased by the recent tension in global relationships. The Fed has raised rates nine times while starting the reduction of its balance sheet. Other Central Banks are following suit. With these ongoing changes will come heightened volatility and uncertainty but, most importantly, new valuations and repricing of risk.

Here’s the list of our 7 themes and focuses for 2019:

1. Interest Rates - A Topic That Needs No Introduction

The direction of interest rates and the shape of the yield curve are key determinants of returns in the fixed income markets. This will not be different in 2019. The interest rate volatility experienced in 2018 will likely be repeated in 2019 as markets determine the right balance of risk and insurance/protection. While historical correlations between rates and equities showed signs of breaking down, we see a risk of an even higher correlation in 2019. The implications of stocks and bonds moving in tandem have significant implications around preservation of capital. Many investors will ask the question, “Where is the best place to hide?” but should be asking the question “Where is the best place to be?”

With a flat interest rate curve (theme #4), there are consequences for both interest rates and fixed income risk assets.

Investors will need to consider the drawdown risk associated with limited yield pick up as they move out the curve. Similar to 2018, we believe that the front end offers some of the most compelling risk-adjusted returns. The long end should be monitored closely for opportunities.

We believe the marketplace will once again default back to focusing on real rates and inflation expectations. The inflation outlook will prove to be challenging for many investors as the inflation rebasing effects come into play in the back half of this year. We will also be fighting headlines of rising wages, input costs, and other direct components of inflation. The complacency around inflation that has been built over the years surrounding the ‘disruption’ theme and deflationary ‘demographics’ will be challenged this year.

Ultimately the economic outlook and the health of the consumer will garner the greatest focus and be the key drivers of risk assets. Growth may prove to be on more solid footing than many expect.

2. The Fed – All I Need Is a Little Help from My Friends

The Fed will prove to be a source of calm this year in our opinion due to their focus on more transparent communication. The marketplace will embrace Powell as an excellent leader, great communicator, and someone who is fully aware of the Fed’s non-mandated role in engineering less volatility in the markets. The marketplace will realize that the Fed is strongly committed to its core mandates – price stability and full employment. With that in mind, the Fed is going to have to make some difficult decisions around changing inflation expectations in 2019 but they’ve learned that communication is key. Stay tuned!

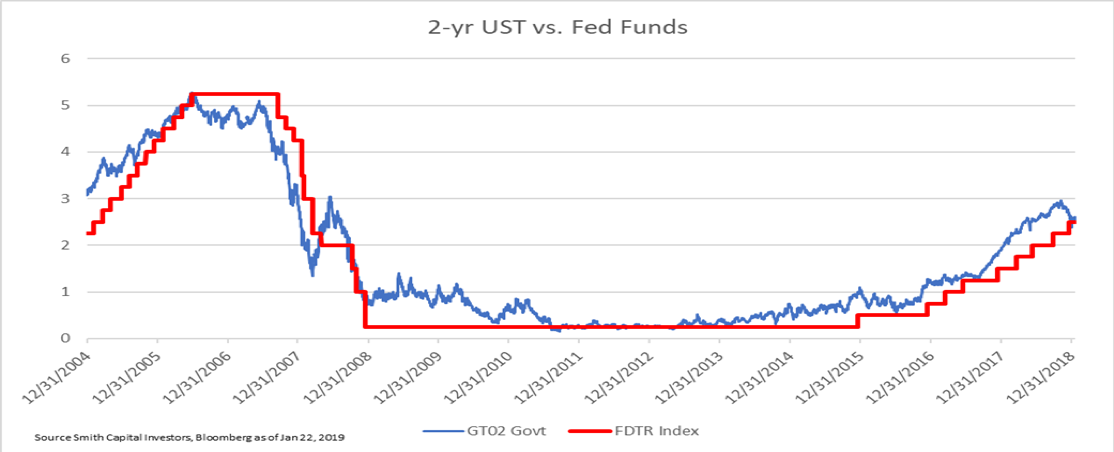

We are watching spread relationships very closely to gauge market sentiment and consensus views. The relationship between 2yr Treasuries and target Fed Funds tells us a lot about future expectations for the Fed. We expect there to be opportunities around this spread relationship throughout 2019.

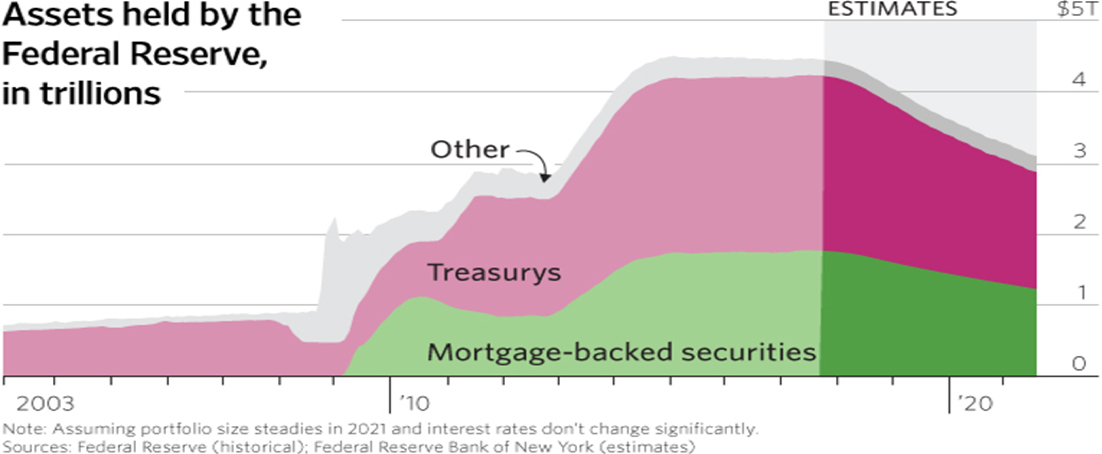

Furthermore, we cannot lose sight of the balance sheet reduction and what that means for the markets. The Fed has issued a commitment to clear communication around this but did not issue a termination of its commitment to actually shrinking the balance sheet.

3. Credit – The Year of Dispersion and Differentiation

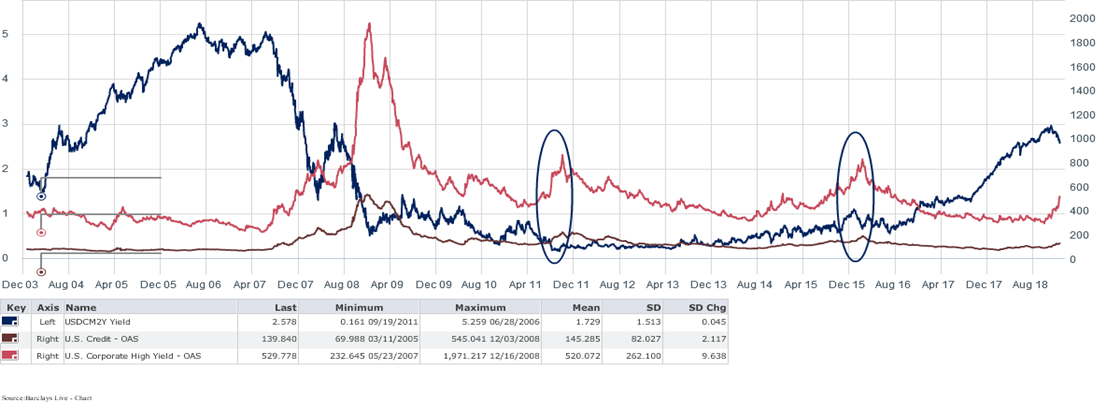

The credit markets have grown in size and depth. Management teams have taken advantage of the opportunity to leverage profits, capital structures, and the scale of their businesses. Shareholder-friendly and merger and acquisition activity have been key drivers of the growth in the credit markets. Flows into fixed income have helped facilitate lower, stable rates and thus the re-levering of Corporate America. With this re-levering we have seen an explosion in the quantity of credit and, furthermore, a deterioration of quality. The insatiable hunt for yield has been a key driver in keeping valuations rich and in many cases driving excessive valuations. This will be a key theme for 2019.

In 2018 we received a first-hand example of what happens when the complacent yield-seeker is awoken by uncertainty and volatility. We expect there to be many bouts of this type of volatility on the horizon. The unintended consequence of the volatility and the repricing of credit will trigger a newfound focus on corporate balance sheets and liquidity by investors as well as CEOs, CFOs and boards (see Theme #5). We would not be surprised to see a series of downgrades and acceleration of defaults in the credit markets in 2019. There are going to be some great winners in the credit space and some unbelievable losers. Differentiation and dispersion should increase significantly. Many management teams will be effective in navigating these times and others will fail. We will once again be reminded of the importance of leadership and the ability to adapt (Theme #5 again).

We strongly believe we are in a bond picker’s market. Yield hogs in the late stages of a credit cycle will be dealt with frequent reminders of the importance of valuation and risk management. Buyer beware.

Investment Grade:

High Yield:

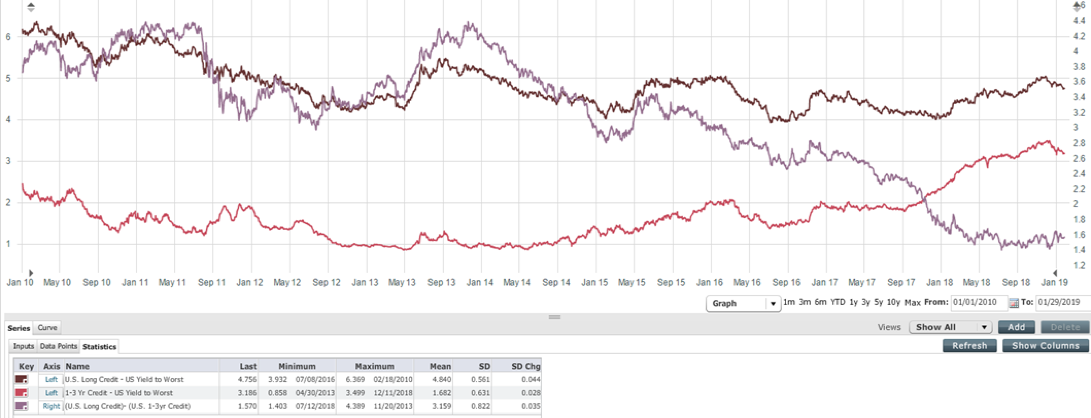

4. Curves: Credit and Rates - “The Earth Is Flat” …and So Is The Curve

When thinking about curves, both interest rate and credit curves, we are drawn to the consideration of risk and return. How much risk is one willing to take per unit of expected return? We raise this issue on every security that enters the portfolios we manage irrespective of the prescribed weights in the index. Flat curves require a different perspective on risk and reward.

We remind ourselves daily that there have been long periods of time where curves flattened and remained flat. These periods of time have important considerations for fixed income investors. Yield-seekers must be very mindful of the drawdown risk during periods of flat curves. Minimal yield pickup for extending in either Treasuries or credit comes from very diverse future expectations. One comes with a view on slowing economic growth and fragility and the other comes from a view of very strong corporate credit profiles, however currently the market seems to be indicating towards both of these scenarios. Downside risk becomes an even more important consideration during these periods.

2 / 10 / 30

Long / Short Credit:

5. CEO/CFO, Board behaviors – Can Firms Deliver and De-Lever? Adapt or Face the Consequences as Firms Search for the Perfect Capital Structure

This will be the year of the haves and the have-nots in Corporate America. Complacent buyers of credit have fueled more aggressive behaviors by management teams and great complacency in boardrooms across America. A turn-of-leverage-here, a turn-of-leverage-there and next thing you know you have a levered balance sheet and a vulnerable capital structure. Many management teams and boards will be challenged in 2019. Some will see the light and realize the power and resiliency of a strong balance sheet in 2019 (and some were forced to already!). Management teams will also be reminded that the best values are found when others are seeking ways to shore up their capital structure. A strong balance sheet and substantial cash flows offer real and valuable options to create shareholder value.

We also believe that many leadership teams will look back on the massive amounts of capital committed to share repo and some of the M&A deals they have done with regret - and most likely a lot of revisionist history around shareholder value creation. 2019 will be the start of a new focus on de-levering and adjusting capital structures in our opinion. Over time these behaviors will accrete to equity holders as bondholders benefit from disciplined moves to reduce leverage.

We will learn a lot about the character and discipline of management teams as well as the fortitude of corporate boards.

6. The Trump, Pelosi and Schumer Reports – Please Tweet Me to Less Volatility

What can we say about politics? The incredible polarization and dysfunction of politics have become commonplace in Washington and, moreover, spread throughout the nation. In many cases the banter between the two parties is viewed as a comedy. We find little to laugh about with the growing deficits, outstanding debt, leveraging of the country (tax payer) and political dysfunction. The implications of the growing debt load in our great country concern us and create increased instability and possibly lower levels of confidence in the system. We take little comfort that other countries have greater debt issues and believe it’s time for a reset in mindset around federal deficits and debt load. A trillion is a big number; twenty trillion is an even harder number to comprehend. Imagine what happens to society when politicians are finally forced to address the entitlement and retirement problems that plague the system versus focusing on less important tasks. Or, what happens when politicians wake up to the fact that larger amounts of the budget will have to be focused simply on debt service. This promises to be an interesting year – one where politics probably rattle markets more than concerns around economic conditions do. Truth be told, we are going to learn the two are very intertwined in 2019.

7. Active Verse Passive in Fixed Income - I Am so Passive I Am Starting to Feel Bashfully Complacent

The active/passive debate in fixed income will take on greater intensity after the volatility of 2018. The sell-off in rates early in 2018 validated concerns around the interest rate sensitivity of the index. Furthermore, the rally in rates in Q4 2018 coupled with the spread widening in credit showed the impact of overall credit growth in the market. While biased in our statement, we believe investors will continue to see the importance and value of active fixed income management—particularly as it relates to capital preservation.

Lastly, we have talked a lot about the risks and unintended consequences of the indices as well as the perils of ‘going passive’ in fixed income. We think these risks could be amplified in 2019 and investors will be reminded of the very asymmetric nature of many segments of the fixed income markets. There are significant drawdown risks in the market place today that offer limited room for error (or yield).

We will save the shadow indexing discussion for later.

Summary:

We expect 2019 to be a year of heightened volatility and uncertainty. We are focused on:

- Interest Rates

- The Fed

- Credit

- Curves

- CEO/CFO Behavior

- Washington

- Active vs. Passive

We are confident that there will be other themes that emerge as time passes. Our goal over the next several weeks is to provide our partners and investors greater detail and depth around these themes while highlighting our thought process and research. Please contact us at [email protected] and let us know if you are interested in receiving the details.

The opinions and views expressed are as of the date published and are subject to change without notice. Information presented herein is for discussion and illustrative purposes only and should not be used or construed as financial, legal, or tax advice, and is not a recommendation or an offer or solicitation to buy, sell or hold any security, investment strategy, or market sector. No forecasts can be guaranteed. Any investment or management recommendation in this document is not meant to be impartial investment advice or advice in a fiduciary capacity, and is not tailored to the investment needs of any specific individual or category of individuals. If you are an individual retirement investor, contact your financial advisor or other fiduciary unrelated to Smith Capital Investors about whether any given investment idea, strategy, product or service described herein may be appropriate for you. Opinions and examples are meant as an illustration of themes, are not an indication of trading intent, and are subject to change at any time due to changes in market or economic conditions. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio.

Past performance is not a guarantee or a reliable indicator of future results. Investing in a bond market is subject to risks, including market, interest rate, issuer, credit, inflation, default, and liquidity risk. The bond market is volatile. The value of most bonds and bond strategies are impacted by changes in interest rates. Bond investments may be worth more or less than the original cost when redeemed. The return of principal is not guaranteed, and prices may decline if, among other things, an issuer fails to make timely payments or its credit strength weakens. High yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Please consider the charges, risks, expenses and investment objectives carefully before investing. Please see a prospectus, or, if available, a summary prospectus containing this and other information. Read it carefully before you invest or send money. Investing involves risk, including the possible loss of principal and fluctuation of value. There is no guarantee that any particular investment strategy will work under all market conditions or are suitable for all investors. Investors should consult their investment professional prior to making an investment decision. All indices are unmanaged. You cannot invest directly in an index. Index or benchmark performance presented in this document does not reflect the deduction of advisory fees, transaction charges, and other expenses, which would reduce performance.

This material may not be reproduced in whole or in part in any form, or referred to in any other publication, without express written permission from Smith Capital Investors. Smith Capital Investors, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission.

© Smith Capital Investors

Read more commentaries by Smith Capital Investors