We entered the year wondering if the economic tides had turned. Risk appetite fell and volatility spiked amid a strong negative market reaction to the Federal Reserve’s rate increase in December. But markets caught their breath in January: Equity values recovered much of their losses, and economic data, though delayed by the government shutdown, has remained strong.

One year has passed since volatility re-emerged in February 2018. Investors have now been thoroughly reminded that markets can move both up and down. Amid this context, we anticipate a year of continued but slower economic growth, and a patient Fed unlikely to undertake many rate actions.

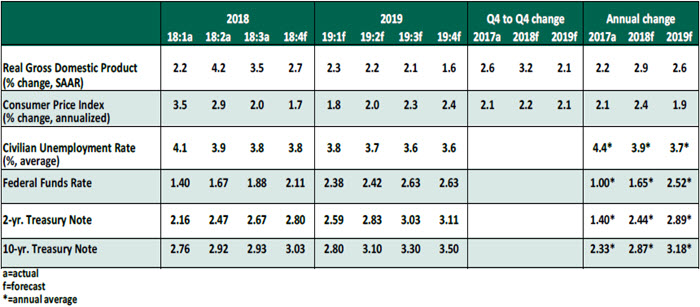

Key Economic Indicators

Influences on the Forecast

- In a press conference following the January 29 and 30 meeting of the Federal Open Market Committee (FOMC), Fed Chair Jerome Powell struck a substantially more dovish tone than we heard after the December meeting. Powell emphasized that the Fed will be patient and data-driven, holding off on rate actions until actual results demonstrate the need to change course. We maintain our expectation of one additional rate increase in mid-2019, likely ending the cycle.

- Starting in 2019, the FOMC considers every meeting to be “live,” with a press conference to follow each meeting. This is a change from the custom of making rate actions only at meetings that coincided with quarterly press conferences. While conditions were not in place for a rate hike in January, this additional flexibility sets the stage for the Fed to change course more rapidly.

- The U.S. federal government shutdown ended in January after a record-setting 35-day run. We expect that belt-tightening by government employees and contractors will weigh on economic growth in both fourth quarter 2018 and first quarter 2019, though some of that loss will be recouped over the course of the year ahead. Government statistical agencies whose workers were furloughed are back at work, catching up and publishing data releases that had been postponed.

- The threat of another shutdown lingers, but we do not believe it will occur. The political cost (to both sides) could be substantial. However, increasing partisanship sets the stage for rancorous fiscal debates as the debt limit is reinstated in March. A budget for fiscal year 2020 must be established by September 30.

- The January employment report contained generally good news. The unemployment rate rose to 4.0% as more workers re-entered the workforce and as furloughed government workers were categorized as temporarily laid off. The payroll report of 304,000 jobs created was well beyond expectations, but was accompanied by a downward revision to prior months. We take this as a validation of a fundamentally strong labor market.