2019 – The Year of Volatility and a Year to Stay Active – Interest Rates

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsInterest Rates - A Topic That Needs No Introduction

The direction of interest rates and the shape of the yield curve are key determinants of returns in the fixed income markets. This will be no different in 2019. The interest rate volatility experienced in 2018 will likely be repeated in 2019 as markets determine the right balance of risk and insurance/protection. While historical correlations between rates and equities showed signs of breaking down, we see a risk of an even higher correlation in 2019. The implications of stocks and bonds moving in tandem have significant implications around the preservation of capital. Many investors will ask the question, “Where is the best place to hide?” We think they should be asking the question “Where is the best place to be?”

With a flat interest rate curve, there are consequences for both interest rates and fixed income risk assets.

Investors will need to consider the drawdown risk associated with limited yield pick up as they move out the curve. Similar to 2018, we believe that the front end offers some of the most compelling risk-adjusted returns. The long end should be monitored closely for opportunities.

We believe the marketplace will once again default back to focusing on real rates and inflation expectations. The inflation outlook will prove to be challenging for many investors as the inflation rebasing effects come into play in the back half of this year. We will also be fighting headlines of rising wages, input costs, and other direct components of inflation. The complacency around inflation that has been built over the years surrounding the ‘disruption’ theme and deflationary ‘demographics’ will be challenged this year.

Ultimately, the economic outlook and the health of the consumer will garner the greatest focus and be the key driver of risk assets. Growth may prove to be on more solid footing than many expect. At Smith Capital Investors, we expect a sequence of the events – stable economy, stirring of inflation and the Fed forcing the market to come up to their now moderate 3% projection - to occur in September 2019, causing interest rates to move higher into the end of the year and allowing the Fed to get another rate hike pushed through the market. Complacency will not be an investor’s friend in this environment; it’s time to know your fixed income manager and know how they invest.

A. The economy and the consumer

Interest rates serve as a proxy for the health of the economy. In the US, approximately 70% of the economy is driven by the consumer…and we believe that the consumer is still very much in the game for 2019. The first round of 2019 data reinforced that the foundations of economic growth are intact. Credit conditions are supportive, employment is strong, and wages are increasing. While we are in an adjustment phase, with growth potentially slowing to a 2% pace, we are not throwing in the towel. Our conviction around sustainable growth has been confirmed by the recent economic data as well as 4Q 2018 company earnings. Thus far, in our view, companies are adjusting to an expected slower pace of growth but are still focused on hiring and are delivering higher wages. Corporate outlooks are cautious, but not pessimistic. From our perch, we see many positives on the horizon that will keep the economy from diving into a recession. With this in mind, we recognize that significant changes in sentiment can create a self-fulfilling outcome.

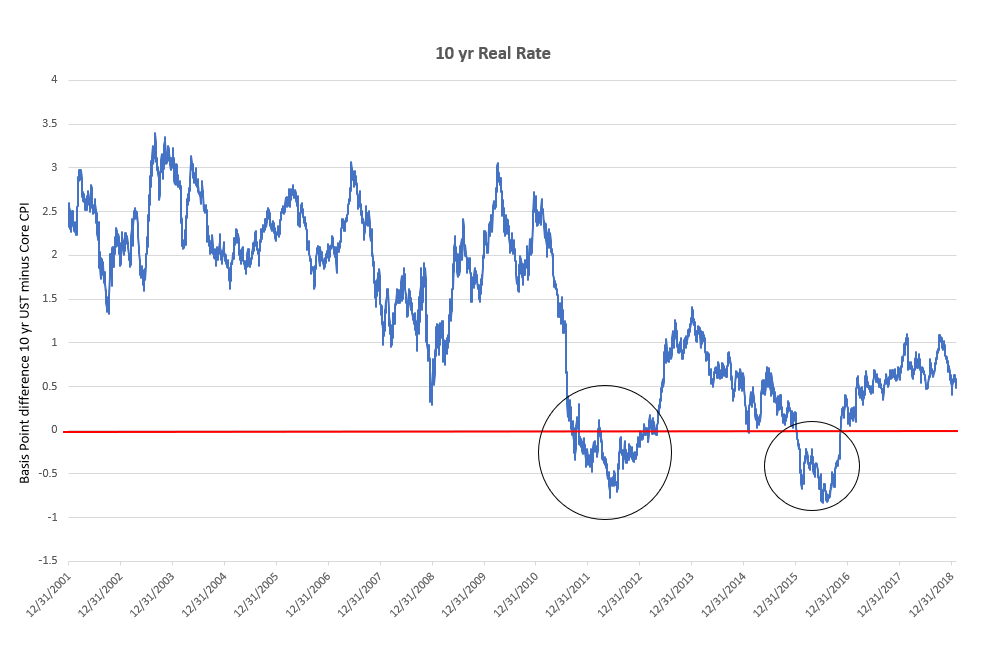

B. Real rates

Historically, real rates have been a key component in fixed income investing. With rates artificially held down throughout the process of Quantitative Easing (QE) AND inflation running below the Fed’s 2% mandate, real rates were in negative territory for two periods post the Great Recession. This period of negative real rates was reinforced by concerns around unstoppable deflation. Thankfully, we have now turned positive as inflation expectations have adjusted higher and bond markets are much more sensitive to positive real rates. This is not only a good sign for the strength of the economy and the consumer’s purchasing power but also for savers. Positive real rates reflect growing expectations of rising inflation. They also provide fixed income investors protection. The U.S. is in positive territory while other G8 counties, specifically the United Kingdom, Germany, and Japan continue to register negative real rates.

Source: Smith Capital Investors, Bloomberg as of January 31, 2019

C. Inflation resets: hard data vs. inflation expectations

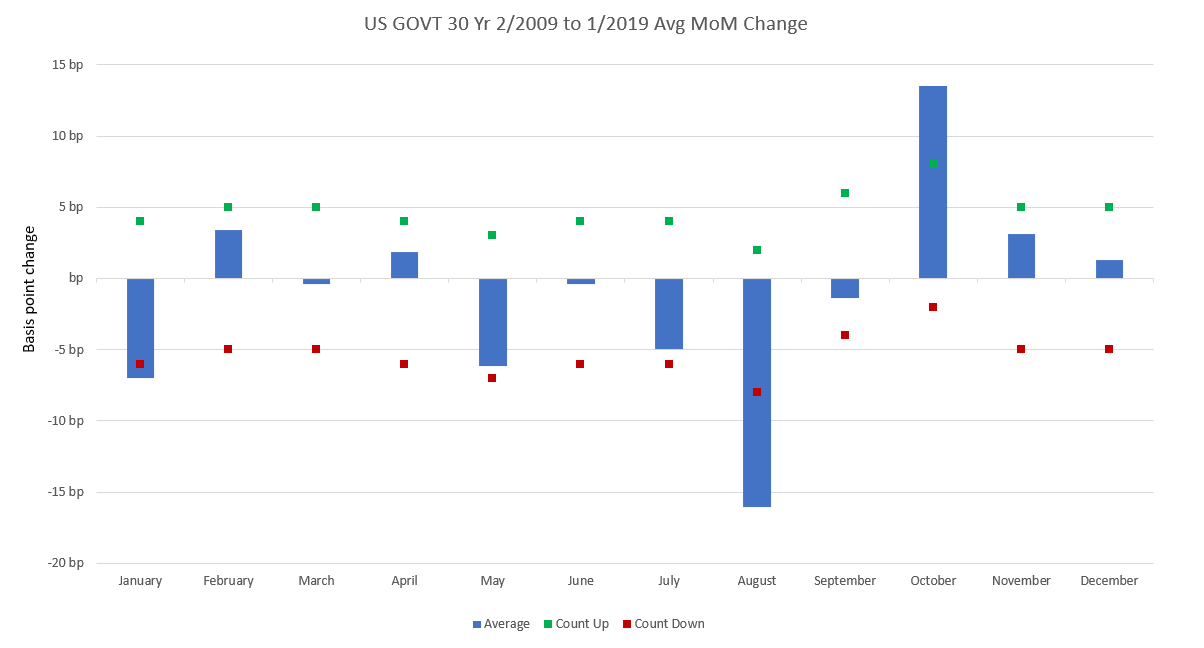

For the past six months we’ve talked about the divergence across inflation data. We believe this will be a big driver of the bond market in 2019. On one side, we have inflation expectations and hard data (Core CPI, Core PCE) signaling very soft inflation (leaning toward soft as compared to stable), while on the other side we have wages and anecdotal data suggesting that inflation is stirring and starting to gather momentum. In 3Q 2019 we will see higher inflation from hard data coincide with strong wages, suggesting that we aren’t actually living in this sub-two-percent inflation world.

The bond market needs to be prepared for this adjustment!

Starting with the “hard data”, the first half of 2018 saw a decent rise in the monthly Core Consumer Price Index (CPI) data. This implies that even stronger monthly data is required in the first half of 2019 to hold Core CPI at levels above 2.2% year-over-year (YoY). We call this the “base effect.” The outcome will cause Core CPI YoY data to look optically lower in the first half of 2019. This effect fades mid-year, resulting in a much easier monthly comp naturally lifting non-seasonally adjusted (NSA) Core CPI YoY. This isn’t necessarily the root of the problem – the market and the Fed are fine with numbers running above 2.0-2.2% YoY. The real problem is that this will collide with 1) a negative seasonal for Treasuries in the month of September (see graph below), 2) wage data that FINALLY starts to reflect the commentary from companies around wage increases in this tight labor market and 3) a Fed that has now slowed the pace of tightening and lowered the terminal rate.

One possible outcome from this collision of hard data and fundamental change is a quick and significant move higher in yields (think taper tantrum) as the market reprices the economic backdrop. Each one of the factors we mention is not enough to reprice the market on its own, but the collision of all three in September 2019 could catch the market by surprise. A market caught unaware could result in quick and volatile move in Treasuries, particularly in the long-end. Caution is warranted on interest rates in this environment.

Source: Smith Capital Investors, Bloomberg as of January 31, 2019

Wages are starting to move higher after employers have exhausted measures of luring new employees and retaining current employees with non-cash benefits, as was the case into the end of 2018. Cash compensation is king in a tight labor market where firms need to pay to acquire and retain talent. Wages are currently running at a healthy 3.2% YoY and we do not see this subsiding.

Anecdotally as we work through earnings season, we are hearing commentary around wages (non-cash perks/benefits turning into one-time bonuses and/or outright pay increases) and higher input costs eating away at margins or being passed along to the consumer. Both situations add to the inflation story.

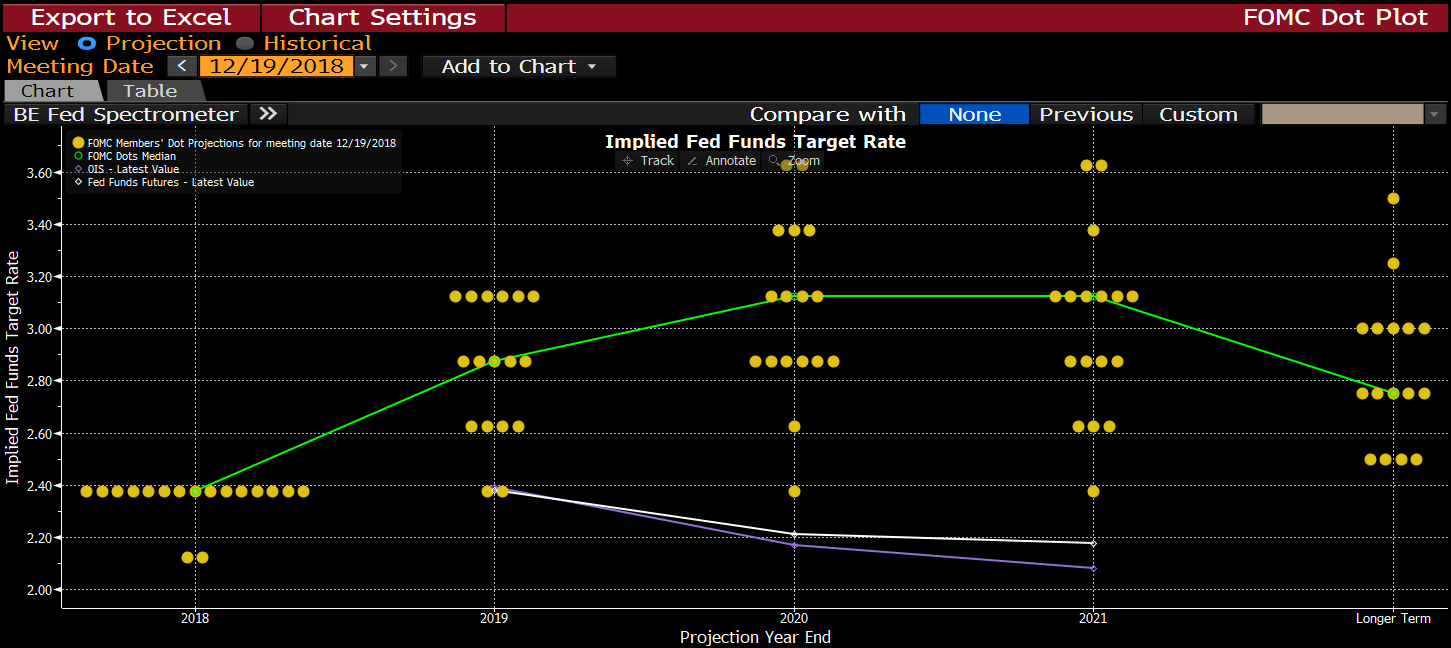

D. Fed expectations vs. reality

With the Fed on hold, we turn our focus to 3Q (September 2019) for the next move by the Fed. We think we have time to work through the market noise while inflation slowly stirs in the background, setting up for what we believe will be two hikes between September and 1Q 2020. This allows the Fed to achieve its earlier target of a 3% terminal Fed Funds rate, a rate that gives the Fed additional bandwidth to weather a future slowdown or market disruption.

That being said, there has been a disconnect between the Fed and the market. In 2018, initially the market moved expectations up to the Fed’s projection until the pivotal turning point: Powell’s “we’re a long way from terminal” comment. Risk assets suffered and inevitably forced the Fed to revise its commentary to bring it closer to market expectations. Powell addressed the market movement with “we are listening to the market” and lowered the terminal rate to 3% from a prior 3.4%, “pausing” for the foreseeable future to assess incoming data. Scoreboard: Fed 1 | Market 1 in 2018.

The market has now repriced the next move as a cut in the Fed Funds rate, not an increase. Based on the information reviewed above, the economy is on solid, though slower, footing. The consumer is strong, inflation is stirring; financial conditions are once again improving. The Fed, led by Powell, will want to get the economy to its terminal rate, providing itself an insurance to combat a market downturn or disruption. While the market is not pricing in a rate hike in the future, we believe the Fed will be given the opportunity to prepare the market for a slow and steady return to a 3% Fed Funds rate which will take Treasuries along for the ride.

Fed Summary of Economic Projections suggesting two hikes, the market is pricing in a cut.

Bloomberg as of Fed meeting December 19, 2018

E. Debt and Deficits

We will cover the topic of Debt, Deficits and Federal leverage when we write more about politics (Theme #6). Although in the interest of a little foreshadowing – complacency is not our friend as it relates to our Federal Debt.

The implication of the growing debt load is real and, in our opinion, continues to be brushed under the rug. The United States thankfully has the benefit of being the global reserve currency and the flight-to-quality bid in the Treasury market. This may not always be the case. There may be a time when our debt creates increased instability and we register a loss of confidence in the system. Low rates have given the government the opportunity to finance/refinance our debt at extremely attractive levels but as rates rise, even marginally, the net interest costs will become a greater burden. According to the Congressional Budget Office (CBO), net interest to service our debt is currently 1% of Gross Domestic Product (GDP), this will rise to more than 6.3% over time. Interest expense will account for more than 50% of the overall spending increase if actions are not taken to balance the budget.

The fiscal side of the equation isn’t the only problem, a potential loss of faith in the U.S financial situation will cause rates to rise as borrowers require a higher coupon to buy the debt. This is NOT an immediate issue but is something we keep on our radar and in our discussions. With total debt currently at $22 trillion dollars (a number most cannot truly comprehend), political discord, polarization, and greater uncertainty on the horizon, we feel it would be foolish to not keep this in focus. More to follow as we dig deeper into politics.

F. Correlations and Relationships

One last consideration for fixed income investors: the correlation between Equities and Treasuries is changing. There is a growing disconnect between the historical relationships and foundations within the market place. We believe that this changing relationship is an unintended consequence of Quantitative Easing (QE) and the Fed’s decision to reverse its unconventional policy position. This has implications for interest rates but a more profound effect on other risk assets, especially credit. We will expand on this in our upcoming writeup on credit. While there are many paths that relationships and correlations can take, we believe the historical risk-off/risk-on relationship is evolving and will have significant implications for capital preservation in a more volatile market. Treasuries have historically served as a safe harbor in difficult times. We have some medium- and long-term concerns that this may not be the case going forward. Like remaining active in managing portfolios, we will consistently challenge the way we think about historical relationships and correlations.

The relationship between interest rates and risk assets is evolving.

Conclusion

Though 4Q 2018 was a healthy reminder of the underlying risks and quick changes in sentiment, fixed income markets have awoken from their high levels of complacency. We believe that rate volatility in 2019 will be ever-present.

Complacency cannot reign when the market is in transition. We believe the market will be forced to recognize the foundations of economic growth are intact. Inflation, though not out of control, is rising and the Fed desires to orchestrate a 3% terminal Fed Funds rate. Underlying our concerns around heightened volatility, we believe that many great opportunities will be created for fixed income and equity investors in 2019. The key is to be present… and stay active.

Our mailing address is:

1430 Blake Street

Denver, CO 80202

303-597-5555

833-577-6484

[email protected]

www.smithcapitalinvestors.com

The opinions and views expressed are as of the date published and are subject to change without notice. Information presented herein is for discussion and illustrative purposes only and should not be used or construed as financial, legal, or tax advice, and is not a recommendation or an offer or solicitation to buy, sell or hold any security, investment strategy, or market sector. No forecasts can be guaranteed. Any investment or management recommendation in this document is not meant to be impartial investment advice or advice in a fiduciary capacity and is not tailored to the investment needs of any specific individual or category of individuals. If you are an individual retirement investor, contact your financial advisor or other fiduciary unrelated to Smith Capital Investors about whether any given investment idea, strategy, product or service described herein may be appropriate for you. Opinions and examples are meant as an illustration of themes, are not an indication of trading intent, and are subject to change at any time due to changes in the market or economic conditions. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio.

Past performance is not a guarantee or a reliable indicator of future results. Investing in a bond market is subject to risks, including market, interest rate, issuer, credit, inflation, default, and liquidity risk. The bond market is volatile. The value of most bonds and bond strategies are impacted by changes in interest rates. Bond investments may be worth more or less than the original cost when redeemed. The return of principal is not guaranteed, and prices may decline if, among other things, an issuer fails to make timely payments or its credit strength weakens. High yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Please consider the charges, risks, expenses and investment objectives carefully before investing. Please see a prospectus, or, if available, a summary prospectus containing this and other information. Read it carefully before you invest or send money. Investing involves risk, including the possible loss of principal and fluctuation of value. There is no guarantee that any particular investment strategy will work under all market conditions or are suitable for all investors. Investors should consult their investment professional prior to making an investment decision. All indices are unmanaged. You cannot invest directly in an index. Index or benchmark performance presented in this document does not reflect the deduction of advisory fees, transaction charges, and other expenses, which would reduce performance.

This material may not be reproduced in whole or in part in any form, or referred to in any other publication, without express written permission from Smith Capital Investors. Smith Capital Investors, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All