We have consistently forecasted a slower year of U.S. economic growth in 2019. Last year’s stimulus measures are losing momentum, and downside risks are accumulating. The transition to a slower rate of growth is underway, and it is yielding economic indicators that can seem contradictory.

While certain measures have begun to cool, the economy is fundamentally sound. The job market is still performing well, inflation is steady and a patient Fed will leave interest rates alone for an extended period. These circumstances will support continued growth.

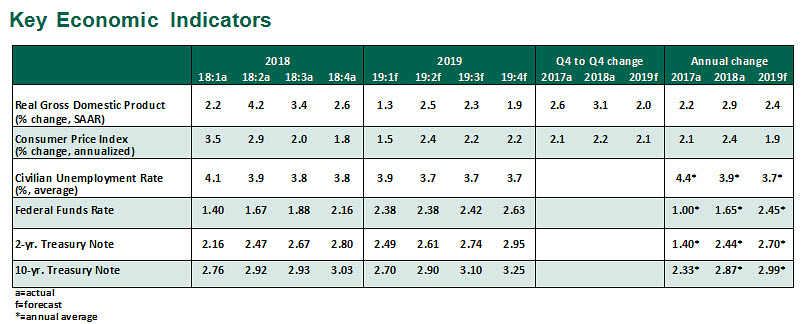

Influences on the Forecast

- Real gross domestic product (GDP) for fourth quarter 2018 grew at an annualized pace of 2.6%, the start of a slower trend. For the full year, the economy grew at 3.1% after adjusting for inflation, in line with forecasts made by the administration when it introduced tax reform and deregulation measures. Those forecasts, however, projected a persistent pace of better than 3%, which we do not think will be realized.

- The unemployment rate recovered to 3.8% in February after briefly reaching 4%. Job gains have been volatile, with merely 20,000 jobs created in February after a blowout of 311,000 in January. We would caution against overreacting to the most recent figure; weather played a role, as did the government shutdown earlier this year.

- Inflation remains muted, with the Consumer Price Index (CPI) rising by only 1.6% year-over-year. Much of this was driven by the fall in energy prices; excluding food and energy, core CPI increased by 2.2%. The personal consumption price index showed a similar trend, growing at a headline rate of 1.8% and a core rate of 1.9%. Wage growth is strong, rising 3.4% year-over-year in February, but it has not flowed through to broader inflation measures.

- After a few months in search of a consistent message, the public comments by Federal Reserve officials now emphasize the patient, data-driven approach they will apply to any upcoming interest rate increases.

- In light of the sluggish data releases starting the year and the Fed’s contemplation of alternate approaches to inflation targeting, we expect to see no rate action until the September meeting of the Federal Open Market Committee (FOMC). Continued growth and the resolution of trade uncertainties will create the conditions for one last hike.

- After the FOMC meeting on March 19-20, we expect to receive guidance as to the targeted level of the Fed’s balance sheet, the timeline over which this level will be reached, and the composition of assets the Fed will hold going forward. The path of quantitative tightening has been well-communicated thus far, and its end does not factor into our forecast.

- As of March 2, the debt ceiling limit on payments is back in force. The Treasury will not face a material risk of running out of money for several months, but a limit increase will eventually be required to continue funding the government through the end of the fiscal year.

- Trade negotiations with China showed sufficient progress to defer the threatened hike in tariff rates on March 1. While the rumored trade deal is unlikely to resolve all tensions with China, it would serve to reduce downside risks to the outlook.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust