Global Economic Outlook - April 2019

Expanding Ailments

The incoming data so far this year have not been encouraging. Trade struggles and the market’s fourth-quarter correction are weighing on economic activity.

Against this backdrop, we have revised down our 2019 growth projections for major advanced economies. We are still cautiously optimistic that some of the major uncertainties that affect the outlook will erode over the summer. In our central case, we expect the U.K. to leave Europe with a deal that preserves the present provisions of finance and business. The positive news flow around the U.S.-China trade suggests both sides will find a common ground.

A soft landing of the world economy is most likely, but the possibility of a recession in a few advanced markets cannot be ruled out.

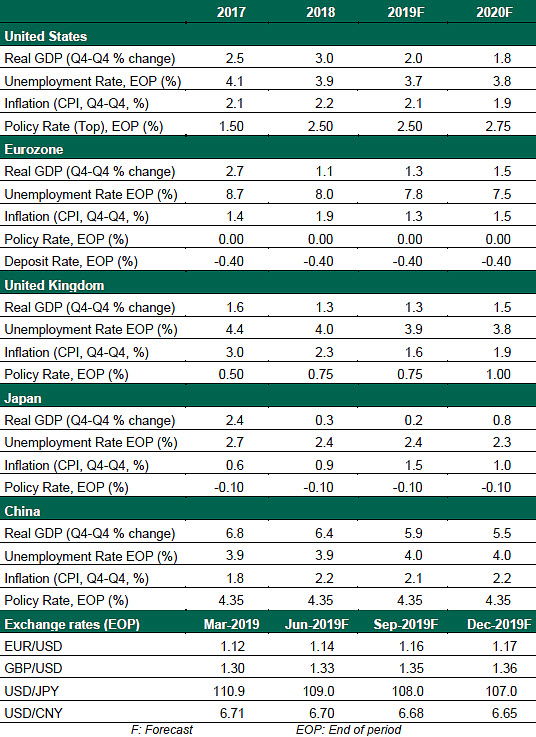

United States

- We have been expecting U.S. growth to moderate as the impact of tax reform recedes. But recent readings on consumption and housing have been tepid, at best. The first quarter of the year is likely to show only modest progress; while we expect the pace of growth to recover, the expansion is not robust. In light of this, we no longer foresee a rate increase from the Federal Reserve in 2019.

- This softer outlook, combined with weaker global data, led to the first 3-month/10-year yield curve inversion since 2007. Though an inversion is not a perfect predictor of a recession, its history of correlation is too frequent to disregard, raising concerns about the outlook. We do not believe a recession is imminent, but downside risks are growing.

Eurozone

The eurozone economy, particularly its manufacturing sector, is struggling. Sentiment and confidence indicators have continued to disappoint. But all hope is not lost. German business confidence rose in March and domestic demand (led by the services sector) remains resilient. This should be sufficient to avoid a recession.

- The impact from some country- and sector-specific woes is anticipated to fade soon. Attention will soon be shifting to the May elections for the European Parliament, which may set the tone for eurozone economic policy in the years ahead. The degree of freedom countries will be granted over their budgets will be central.