What Ballooning Corporate Debt Means for Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThis week I’m writing to you from Delray Beach, Florida, where I’m presenting at Money Map Press’ Black Diamond Conference.

What I love about this event, and others like it, is that it gives investors a chance not only to hear from market experts but also speak with them face-to-face on a wide range of topics, from metals and mining to bitcoin, and so much more. Among the most sought-after presenters this year are early-stage tech investor Michael Robinson, who I interviewed last year; Money Map Chief Investment Strategist Keith Fitz-Gerald; and Sprott CEO Rick Rule.

In case you didn’t get the chance to attend, I’ll be sure to cover the highlights in the coming days.

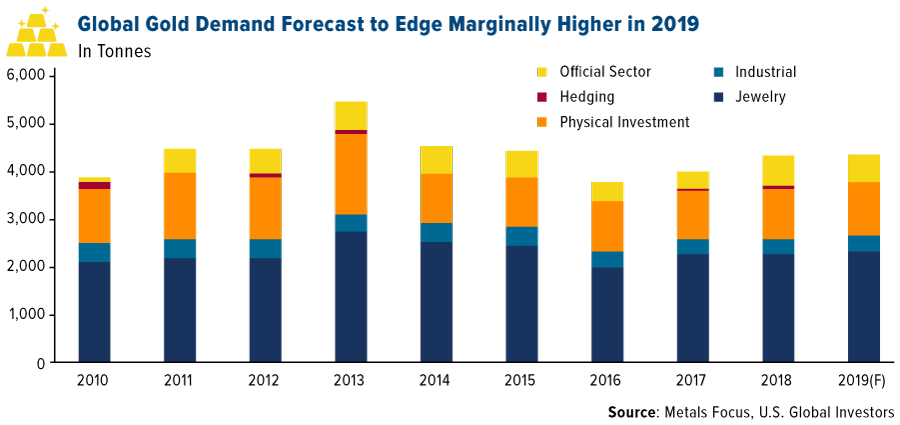

Right now I want to share with you the latest from Metals Focus. The London-based commodities research group just released the 2019 edition of its widely-read Gold Focus report, and the big news is that global gold demand will climb to its highest level in four years. The uptick is expected to be driven by an increase in jewelry fabrication, with India, China and Italy leading consumption higher.

Interest in gold jewelry has indeed improved in recent years, a phenomenon we’ve noticed with the success of such companies as Men?. Late last year, Google inquiries for “gold jewelry” hit an 11-year high.

But there’s more to the story than the Love Trade. Metals Focus analysts see gold also benefiting from a more dovish Federal Reserve and fears of a global economic slowdown.

“We expect U.S. real gross domestic product (GDP) to slow in 2019 and 2020,” comments Metals Focus Director Nikos Kavalis. “This reflects a natural tapering, following two very strong years, the fading of windfall gains from the late-2017 tax reforms and, eventually, also the impact of trade wars on U.S. consumer spending.”

Are We Headed for Another Recession?

Few people know the risks in today’s economy and marketplace as much as David Rosenberg, chief economist and strategist at Canadian wealth management firm Gluskin Sheff & Associates. For years he’s educated investors with his popular “Breakfast with Dave” newsletter, which you can subscribe to here. He’s also a regular contributor to the Globe and Mail and the Financial Post.

Considered by many to be a Wall Street permabear, Rosenberg successfully predicted the 2007-2008 financial crisis.

Now he’s predicting another recession to make landfall as soon as the second half of this year. Why? In short, the Fed has been too aggressive tightening liquidity at a time when corporate debt is at an all-time high. What’s more, the Trump administration has already enacted fiscal stimulus in the form of tax reform, which has historically been reserved for times of economic turmoil, not expansion.

“How are we going to stimulate fiscal policy [in the event of a recession]?” he asked recently on CNBC’s Trading Nation. “We already did that at the peak of the cycle. We don’t have the fiscal ammunition.”

Corporate Debt Nearing Half of U.S. GDP

Last week Rosenberg spoke at the CFA Societies Texas Investor Summit in San Antonio, U.S. Global Investors’ hometown, where he laid out his thought process.

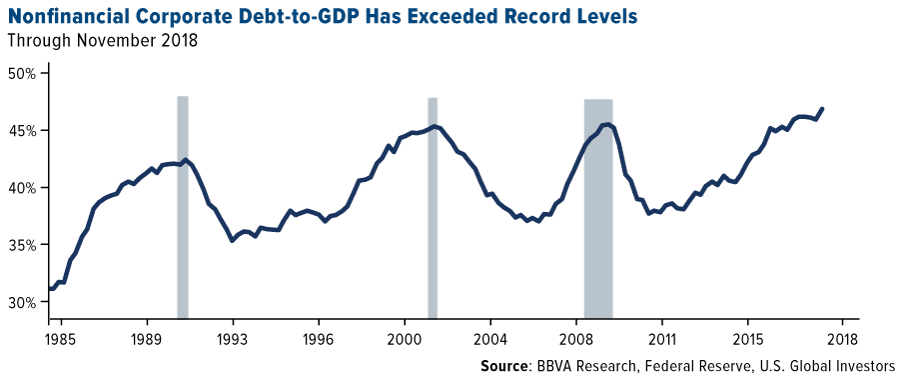

Since the last recession, nonfinancial corporate debt has ballooned to more than $9 trillion as of November 2018, which is nearly half of U.S. GDP. As you can see below, each recession going back to the mid-1980s coincided with elevated debt-to-GDP levels—most notably the 2007-2008 financial crisis, the 2000 dotcom bubble and the early 90s slowdown.

Through 2023, as much as $4.88 trillion of this debt is scheduled to mature. And because of higher rates, many companies are increasingly having difficulty making interest payments on their debt, which is growing faster than the U.S. economy, according to the Institute of International Finance (IIF).

On top of that, the very fastest-growing type of debt is riskier BBB-rated bonds—just one step up from “junk.” This is literally the junkiest corporate bond environment we’ve ever seen.

Combine this with tighter monetary policy, and it could be a recipe for trouble in the coming months.

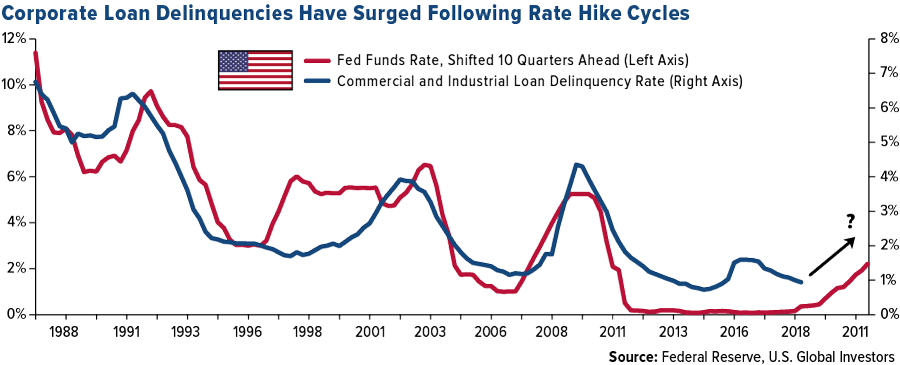

During his presentation, Rosenberg reiterated the saying that business cycles don’t die of old age, but rather they’re killed by the Fed. Take a look at the chart below. It shows commercial and industrial loan delinquency rates, overlaid by fed fund rates shifted 10 quarters ahead. What it suggests is that roughly 10 quarters after the Fed began to tighten, loan delinquencies surged.

The good news is that it’s been more than 10 quarters since the Fed started lifting rates in December 2015, and so far we haven’t seen a noticeable increase in delinquencies.

Could this be because the rate hikes this cycle have been small relative to those in past cycles? Not likely, says Rosenberg. According to him, it’s not the amount that matters so much as the change. Whether rates go up 2.50 percent or only 0.25 percent, it can still be a shock on the financial system.

To be clear, I’m not predicting a recession any time soon, only passing along Rosenberg’s expert opinion.

But if his position makes sense to you, it might be time to consider your options on how to prepare. Rosenberg recommends overweighting fixed-income and REITs (real estate investment trusts).

I would add gold to that mix, as it’s performed well as a store of value during economic pullbacks. As always, I recommend a 10 percent weight in gold, with 5 percent in gold bars, coins and jewelry, and 5 percent in gold stocks, mutual funds and ETFs.

Concerned about Brexit? Read my thoughts on how it could impact gold prices by clicking here!

Gold Market

This week spot gold closed at $1,291.55 down $0.75 per ounce, or 0.06 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week slightly higher by 0.12 percent. The S&P/TSX Venture Index came in up 0.47 percent. The U.S. Trade-Weighted Dollar rose 0.11 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-31 | Caixin China PMI Mfg | 50.0 | 50.8 | 49.9 |

| Apr-1 | Eurozone CPI Core YoY | 0.9% | 0.8% | 1.0% |

| Apr-1 | ISM Manufacturing | 54.5 | 55.3 | 54.2 |

| Apr-2 | Durable Goods Orders | -1.8% | -1.6% | 0.1% |

| Apr-3 | ADP Employment Change | 175k | 129k | 197k |

| Apr-4 | Initial Jobless Claims | 215k | 202k | 212k |

| Apr-5 | Change in Nonfarm Payrolls | 177k | 196k | 33k |

| Apr-8 | Durable Goods Orders | -- | -- | -1.6% |

| Apr-10 | ECB Main Refinancing Rate | 0.000% | -- | 0.000% |

| Apr-10 | CPI YoY | 1.8% | -- | 1.5% |

| Apr-11 | Germany CPI YoY | 1.3% | -- | 1.3% |

| Apr-11 | PPI Final Demand YoY | 1.9% | -- | 1.9% |

| Apr-11 | Initial Jobless Claims | 210k | -- | 202k |

Strengths

- The best performing metal this week was platinum, up 6.07 percent. Platinum is set for its biggest weekly advance in two years, as its wide discount to sister metal palladium creates interest for the metal. Bloomberg writes that traders are also weighing the potential for labor disruptions in South Africa, the world’s largest producer of the metal. Platinum fell 14 percent in 2018, but is starting to see a rebound this year. Gold traders switch to being neutral on the yellow metal this week after being bullish for three previous weeks, according to the weekly Bloomberg survey. The Perth Mint reports that gold coin and bars sales rose to 32,757 ounces in March, which is up from 19,524 ounces in February. BullionVault’s gold index measuring the balance of buyers against sellers rose to 54.5 in March, up from 52.2 in February, indicating that there are more buyers on the market for gold.

- Gold held steady this week, down just 0.06 percent, as investors await the outcome of the latest round of trade talks between the U.S. and China and as negative economic data was released. The World Trade Organization cut its global trade growth projection for 2019 and orders placed with U.S. factories for business equipment fell in February for the third time in four months, reports Bloomberg.

- Retail investors are also taking notice of platinum. U.S. Mint data shows that first quarter sales of platinum coins surpassed the amount sold in all of 2018. Prices for the metal have climbed more than 13 percent so far this year.

Weaknesses

- The worst performing metal this week was palladium, down just 1.02 percent, as hedge funds cut bullish positioning to a 5-month low. Turkey’s gold reserves fell $154 million from the previous week, with total reserves now worth $20.8 billion, according to central bank data in Ankara. U.S. Mint data shows that American Eagle gold coin sales fell 8 percent in March, marking two straight months of declines after reaching a two-year high in January.

- Improving global growth and surging stocks are luring investors away from gold and into riskier assets, writes Bloomberg’s Vildana Hajric. Outflows from U.S.-listed commodity ETFs totaled $1.25 billion in the week ended April 4, which is a big drop from deposits of $128 million the previous week. Precious metals ETFs saw outflows of $943 for the week. Data compiled by Bloomberg shows that ETFs cut 379,577 troy ounces of gold from their holdings on Tuesday, which is the biggest one-day decrease in at least 12 months.

- Mongolia’s central bank reported on Monday that its purchases of gold in the first quarter declined by 71.6 percent year-over-year. The decline is due to the expiration of the effective period of low royalty taxes on gold. The discount of 2.5 percent ended on January 1 and since then there has been a 5 to 10 percent royalty tax on gold miners. A bank spokesperson told Xinhua, a news agency, that “miners are less willing to sell their gold to the central bank due to this factor.”

Opportunities

- Ronald-Peter Stoeferle, managing partner at Incrementum AG, says that gold is poised to rally to $1,450 to $1,500 per ounce by year end if it breaks through the $1,360 to $1,380 per ounce resistance level. Stoeferle says that one of the drivers will be demand from pension funds, high-net worth individuals and wealth managers. Bloomberg writes that Stoeferle also cities his fund’s own inflation indicator to support his bullish gold view, which is currently showing increasing momentum. Goldman Sachs is also bullish on the yellow metals as it expects a rebound in ETF holdings to continue due to late-cycle worries and negative German 10-year real rates.

- More bullish views of platinum ahead. Bloomberg’s Rupert Rowling writes that the precious metal is set to climb above the $900 per ounce level on speculation of strikes at South Africa mines. Demand is also being driven by platinum being considered as a substitute for palladium for use in autocatalysts. Bloomberg’s Mike McGlone writes that platinum is likely in the early days of its recovery, based on the palladium versus platinum ratio.

- China’s second largest, publicly-listed gold producer, Shandong Gold, is looking to make an acquisition by the end of this year. Chairman Li Guohong said in a briefing in Shanghai that “we are more optimistic on gold prices this year than last year” and that other mergers and acquisitions in the sector are proof of bullish consensus on gold prices. Wesdome Gold Mines Ltd. rose 9.72 percent for the week after announcing that its gold production was up 6 percent year-over-year, producing 19,010 ounces. Higher grades were delivered to the mill and the company maintains a strong cash position.

Threats

- The Eastern Shore community in Nova Scotia is rallying against Atlantic Gold’s proposed open-pit gold mine in the area. The community opposes the project strongly because it could damage a river that has been heavily protected for over 40 years. The Atlantic Gold project would also only operate for six years, but impact the environment significantly for many years after.

- Senators in Italy voted in favor of a parliamentary motion calling on the government to clarify the legal status of the Bank of Italy’s gold reserves, reports Bloomberg. The motion also asks the government to obtain detailed information about the status of the central bank’s gold held abroad. It is unclear what the government is trying to do with the country’s gold. A separate motion by the opposition party that called for the repatriation of gold held abroad was rejected.

- Palladium fell this week after President Donald Trump threatened to close the border between the U.S. and Mexico. A border closing would be negative for the U.S. economy and the auto industry in particular, which is the largest consumer of palladium.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.91 percent. The S&P 500 Stock Index rose 2.04, while the Nasdaq Composite climbed 2.71 percent. The Russell 2000 small capitalization index gained 2.77 percent this week.

- The Hang Seng Composite gained 2.93 percent this week; while Taiwan was up 0.60 percent and the KOSPI rose 3.22 percent.

- The 10-year Treasury bond yield rose 9 basis points to 2.498 percent.

Domestic Equity Market

Strengths

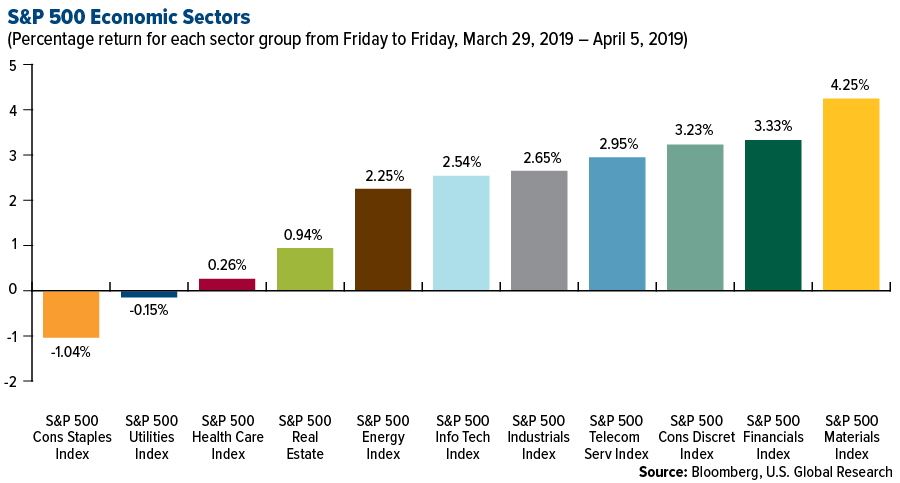

- Materials was the best performing sector of the week, increasing by 4.25 percent versus an overall increase of 1.98 percent for the S&P 500.

- Wynn Resorts was the best performing stock for the week, increasing 18.12 percent.

- Tradeweb soared in its trading debut. The financial data provider closed at $35.81 a share on Thursday — up 32.6 percent from the $27 where its initial public offering priced the prior evening.

Weaknesses

- Consumer staples was the worst performing sector for the week, decreasing by 1.04 percent versus an overall increase of 1.98 percent for the S&P 500.

- Walgreens Boots Alliance was the worst performing stock for the week, falling 13.56 percent.

- Shares of Walgreens Boots Alliance were down 12.1 percent on Tuesday after the drugstore chain announced disappointing results for its fiscal 2019 second quarter. Adjusted earnings per share declined 5.4 percent to $1.64. Analysts, on average, had been forecasting higher earnings of $1.74 per share.

Opportunities

- Slack is reportedly aiming for a direct listing on the New York Stock Exchange. The workplace messaging platform is said to be planning an NYSE debut in June or July, according to The Wall Street Journal.

- One of Africa's first unicorns is about to go public on the New York Stock Exchange. Jumia, the Alibaba of Africa, last week set the price range for its initial public offering at between $13 and $16 a share. It will trade under the ticker JMIA.

- Housing stocks are roaring back. The S&P homebuilders exchange-traded fund has surged 20 percent since December, despite some lackluster underlying housing data.

Threats

- According to Morgan Stanley, tech stocks are headed for a rude awakening. "Despite a higher rate of companies missing EBIT margin estimates in Q4 amid slowing demand, management teams have remained positive," said Mike Wilson, Morgan Stanley's U.S. equity strategist. "It would seem to us that management teams are not yet acknowledging a rising risk of margins disappointing.”

- Tesla deliveries dropped sharply in the first quarter of this year. The electric car maker delivered 63,000 vehicles, according to a press release out Thursday evening, which is a 31 percent drop from the fourth quarter of 2018.

- GameStop sank after missing on earnings. Shares fell more than 7 percent after the video game retailer reported disappointing top- and bottom-line results for the fourth quarter and said it wouldn't give annual earnings-per-share results at this time because it recently named a new CEO and launched a cost-savings initiative.

The Economy and Bond Market

Strengths

- Nonfarm payrolls expanded by 196,000 in March, better than the 175,000 Dow Jones estimate. It is also good news on the heels of February numbers that had economists wondering whether the decade-old economic expansion was nearing an end.

- Unemployment held steady at 3.8 percent, the Bureau of Labor Statistics reported Friday, meeting economist’s expectations.

- The number of Americans filing applications for unemployment benefits dropped to a more than 49-year low last week, pointing to sustained labor market strength despite slowing economic growth. Initial claims for state unemployment benefits declined 10,000 to a seasonally adjusted 202,000 for the week ended March 30, the lowest level since early December 1969.

Weaknesses

- The U.S. dollar once again lost some of its appeal as a reserve currency in the fourth quarter. Central banks around the globe held 61.7 percent of their allocated currency reserves in the greenback at the end of December, paring back for a third straight quarter and approaching a five-year low, the International Monetary Fund said in a report Friday. The dollar’s share dropped from 61.9 percent at the end of September, as the euro, Japanese yen and the Chinese yuan all gained ground.

- U.S. retail sales unexpectedly eased in February on declines in grocery stores and building materials, which could potentially reflect cooler weather, though also may signal further headwinds for the economy in the first quarter. The value of overall sales fell 0.2 percent, according to Commerce Department figures released Monday. The median forecast of economists surveyed by Bloomberg called for a 0.2 percent gain.

- New orders for key U.S.-made capital goods unexpectedly fell in February as well. The Commerce Department said on Tuesday that orders for non-defense capital goods excluding aircraft, a closely watched proxy for business spending plans, slipped 0.1 percent, pulled down by declining demand for machinery and computers and electronic products. Overall orders for durable goods fell 1.6 percent in February.

Opportunities

- Next Wednesday, attention will shift to the FOMC minutes of the March meeting and on inflation as the CPI report is released. Headline inflation is expected to have accelerated to 1.8 percent year-over-year in March from 1.5 percent before, while the core rate is forecast to have held steady at 2.1 percent year-over-year. The Fed will probably reinforce its neutral stance in its March meeting minutes when FOMC members signaled they’re not planning to raise rates at all in 2019.

- The University of Michigan’s preliminary reading of the consumer sentiment index for April will also be on the radar next week.

- Trade talks appear to be making progress. China’s Vice Premier said the U.S. and China had "reached new consensus on such important issues as the text," according to the state-run news agency Xinhua.

Threats

- After managing small growth of 0.1 percent month-on-month in December and January, factory orders are forecast to have reversed course in February to decrease by 0.6 percent.

- It's time to play 'defense' in the bond market. "We think it's a time to start to move up in credit quality and keep the duration short," Darrell Cronk, chief investment officer of Wells Fargo's wealth and investment management unit, told Business Insider.

- A housing slowdown is taking hold in some Florida markets, where a growing share of properties are sold only after the seller cuts the asking price. Miami leads the nation in both the size and frequency of such deals. In Miami, hurt by a pullback of South American buyers, about 88 percent of single-family home sales in the first quarter came after a reduction, according to an analysis by Knock, a startup that helps buyers trade up into their next homes.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was palm oil, which gained 6.40 percent. Inventories showed a drop and markets turned optimistic that strong demand and higher biodiesel use will further reduce stockpiles. Oil in New York is set for the longest weekly winning streak since November 2017, as crises from Venezuela to Libya threatened supplies and optimism over the U.S.-China trade talks boosted the outlook for demand, writes Bloomberg. WTI was up 3.3 percent this week and is poised for a fifth weekly advance. On Monday Saudi Arabia’s giant oil company, Aramco, finally opened its books and revealed that it generated over $111 billion in net income in 2018. This makes it likely the world’s most profitable company.

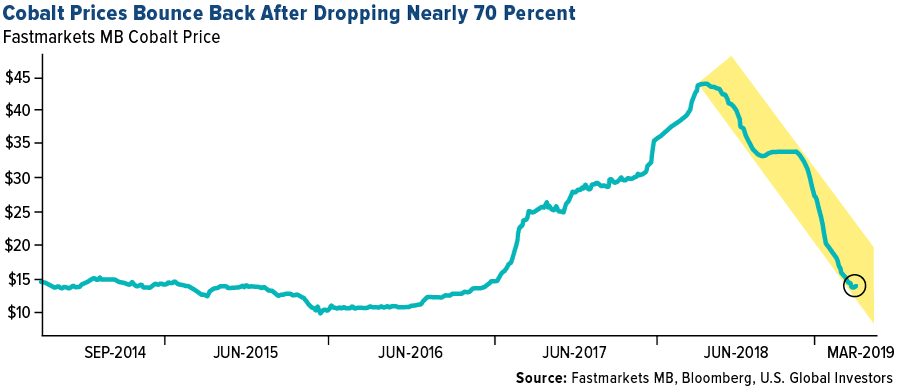

- Uniper SE is now planning a floating LNG terminal on the North Sea coast as the collapse of Asian LNG prices has helped Europe become the most important gas market in the world. The company’s chief commercial officer Keith Martin said in an interview this week that there is much interest in the project from several companies. Eurasian Resources Group (ERG), a top cobalt miner, says that the price of cobalt is set to rebound after a 12-month collapse in prices. CEO Benedikt Sobotka expects a revival for the metal due to growing electric vehicle sales. After falling 70 percent since last April due to oversupply, cobalt prices climbed this week for the first time in five months.

- In a big week for wind power, BloombergNEF reports that offshore wind power costs dropped 22 percent in the last six months alone, according to the global levelized cost of energy benchmark. The Global Wind Energy Council estimates that wind power may jump 50 percent in the next five years led by installations in China, the U.S. and new Southeast Asia markets. Norway could see greater adoption of the technologies too as the Norwegian Water Resources and Energy Directorate has presented a framework report to the government proposing 13 new areas for onshore wind-power projects. Lastly, Bloomberg reports that Enel SpA has acquired U.S. renewables developer Tradewind Energy Inc., expanding its wind project pipeline by 37 percent, and marking the Italian utility’s second acquisition of U.S. renewable projects this month.

Weaknesses

- The worst performing major commodity for the week was lumber, which fell 2.33 percent as wood stockpiles in China reached near full capacity in March. Even as U.S.-China trade optimism boosted base metals early this week, most are set for a weekly loss due to demand concerns. On Thursday LME copper stockpiles rose 18 percent to the highest level in six months. China’s stainless steel stockpiles are near a record-high, which could endanger nickel’s surge of 25 percent so far this year. Morgan Stanley wrote in a report, citing Chilean customs data, that prices for lithium produced in Chile saw the largest decline on record in February falling 22 percent from the previous month. Coal fell for a fifth day on Tuesday in Europe to the lowest since June 2017.

- Positive for consumers and negative for producers, natural gas in West Texas plunged into negative territory due to overproduction. Bloomberg reports that drillers must now pay customers to take away gas, a byproduct of crude production, as pipeline constraints keep supply trapped in the region. With nowhere to send it, some producers are burning the excess gas (although it is frowned upon by regulators). Additionally, the rise of wind power in Texas is threatening to erode the long-standing correlation between the price of natural gas and the cost of electricity, writes Bloomberg’s Christopher Martin. Wind has become so powerful that electricity prices surged this week even as gas was at negative 34 cents on Monday.

- Factory orders in Germany plunged the most in a decade in the month of February, led by a drop in exports of 6 percent, as China and the global slowdown took a toll, writes Bloomberg. Orders fell 4.2 percent in February from the month prior and are down 8.4 percent from a year earlier. The SEC says that mining giant Rio Tinto Group has failed to produce 25,000 documents linked to fraud charges stemming from a troubled $3.7 billion coal deal. London-based Rio is facing an SEC lawsuit over inflating the value of Mozambique coal assets acquired in 2011.

Opportunities

- Iron ore prices ended a crazy week above $90 a ton as supply shocks spurred gains, writes Bloomberg’s Krystal Chia. Futures rose 7.5 percent in Singapore due to continued supply concerns from the Vale SA dam burst and supply losses in Australia due to Cyclone Veronica. Rio Tinto Group warned that it might lose 14 million tons of iron output in 2019 due to the cyclone and a fire. Australia’s big four miners, including Rio, all experienced on-year drop in exports of iron due to the cyclone that impacted a week of shipping. According to UBS Group AG, production dropped 12 percent month-over-month and 16 percent year-over-year.

- According to JPMorgan Chase & Co., U.S. energy stocks are poised to gain after underperforming both oil and the rest of the stock market. Strategists led by Dubravko Lakos-Bujas wrote in a report that “energy currently offers the best risk-reward” and the valuation for the sector is at a multi-decade low. Bloomberg’s Joanna Ossinger writes that energy is outperforming the S&P 500 this year by gaining 16 percent, versus 15 percent, and that oil has risen about 37 percent. South Korea has enacted tax reform that reduces tax on LNG by 75 percent, which should be positive for demand.

- Norway’s $1 trillion sovereign wealth fund will be adding a new asset class for the first time in nine years. After previous rejections, the government is now allowing the fund to be invested in unlisted renewable energy infrastructure, which is a step forward in diversifying away from mostly oil and gas production. In battery news, Total SA is teaming up with China’s Tianneng Group to build lithium-ion cells for electric vehicles and energy storage equipment. BloombergNEF finds that the cost of storing energy using utility-scale batteries of four-hour duration is down 76 percent since 2012.

Threats

- Canada says that it will not ratify the new USMCA trade deal unless the U.S. lifts its tariffs on steel and aluminum. Canada’s foreign minister issued a warning this week that the country will only move forward with ratification when other countries do so as well. The deal, which was agreed upon in November, has yet to be signed into law by the U.S., Canada or Mexico.

- Drillers in Colorado, the nation’s number five oil producing state, are now facing toughing rules. The state’s legislature passed an overhaul of oil and natural gas laws that gives local governments more power to regulate drilling. Bloomberg’s Catherine Traywick writes that explorers such as Anadarko Petroleum Corp. and Noble Energy Inc. could face new levels of oversight, which would be able to regulate the siting of surface infrastructure and impose other rules around drilling.

- Bloomberg reports that LNG supply will swell this year and that the rankings of the biggest exporters will change and create an unprecedented race for market share. Australia might topple Qatar to become the biggest exporter and the U.S. could become the third-largest exporter. Mel Ydreos, from lobby group International Gas Union, says that “in the next five years 75 percent of the additional LNG supply will come from the U.S.”. He adds that it’s a “pretty big shift and of course we are seeing the competition respond.”

Emerging Europe

Strengths

- Turkey was the best performing country this week gaining 5.3 percent. The S&P said Turkey’s credit rating is not at risk of being downgraded, but did warn that another fall in the lira could be very bad news. Currently the S&P ranks Turkey’s credit rating at B+ (junk level) with a stable outlook.

- The Czech koruna was the best performing currency this week, gaining 70 basis points against the U.S. dollar. According to a Reuters’ poll of analysts, the koruna is expected to strengthen by 2 percent versus the euro in the coming year if the Czech central bank continues to increase rates to fight inflation.

- Industrial service was the best performing sector among eastern European markets this week.

Weaknesses

- Hungary was the worst relative performing country this week, gaining 40 basis points. The nation’s Manufacturing PMI was reported weaker in March at 52.4 versus an estimated 54.3, and well below February’s reading of 55.7.

- The Turkish lira was the worst performing currency this week, losing 1.3 percent against the U.S. dollar. The lira has been highly volatile the past few weeks. According to unofficial results from last weekends’ municipal elections, President Erdogan and his leading AKP party lost the majority in the capital city of Ankara and also in Istanbul. In Istanbul, the nation’s largest city, the AKP and opposition both claimed victory, so the votes are being recounted.

- Utilities was the worst performing sector among eastern European markets this week.

Opportunities

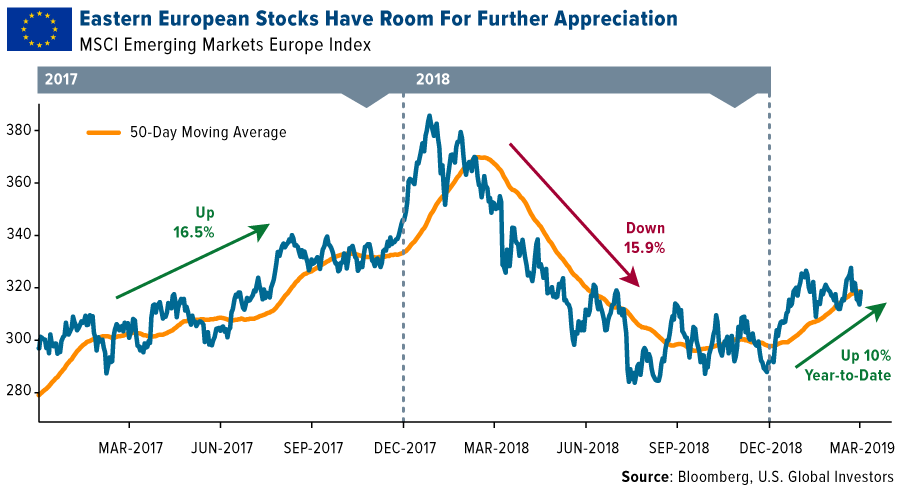

- Looking at a technical price performance chart of the MSCI Emerging Europe Index, we can see that stocks may have more room for further price appreciation. 2017 was a strong year for the region with stocks gaining 16.5 percent. Then in 2018, equites lost 15.9 percent. Year-to-date Eastern Europe has gained 10 percent. The index has crossed above its 50-day moving average, which suggests the upward trend will continue.

- U.K. lawmakers made some progress on Brexit this week by agreeing on a bill that rules out a no-deal exit from the European Union. In the case of no agreement by April 12, the government will seek an extension to the Brexit deadline. Donald Tusk, President of the European Council, favors a one-year extension, but some EU members are opposed to such a long extension.

- Eurozone finance ministers agreed to disburse 1 billion euros to Greece as part of a post-bailout program of monitoring reforms. The payment was conditional on Athens respecting its reform commitments. The money will boost Greece’s cash buffer and could allow the country to borrow at more favorable rates.

Threats

- The EU launched another procedure against Poland for rule-of-law violations. Poland is already facing EU infringement proceedings regarding mandatory retirement ages for judges. New proceedings will look at legislation that allows the decisions of ordinary court judges to be subject to probe. In addition, the commission will look into the independence of the Polish Supreme Court, noting all of its members are new and appointed by the parliament. Poland has two months to respond to the EU’s concerns.

- Germany’s manufacturing PMI is falling faster than feared, according to estimates published a week ago. Final Manufacturing PMI reading for March was reported at 44.1, below the estimated 44.7, and below February’s reading of 47.6. For the whole Eurozone area, the Manufacturing PMI was reported lower as well, at 47.5. However, Service PMI for the EU jumped to 53.3 from 52.7, keeping the Composite PMI above the 50 level that separates growth from contraction.

- Low-cost European airlines may suffer from Brexit. EasyJet is turning more negative on its second half of 2019 outlook. Overcapacity combined with slower growth was among the key arguments for its negative outlook. A strong U.S. dollar along with higher oil prices are not helping the airline either.

China Region

Strengths

- The Shanghai Composite jumped 5.04 percent this week and it even took Friday off! Hong Kong’s Hang Seng Composite climbed 2.93 percent, and Hong Kong took Friday off, too! Korea had a good week as well, with the KOSPI rising 3.22 percent, and Singapore’s Straits Times Total Return climbed 3.42 on the week.

- Materials was the top performing sector for the Hang Seng this week, jumping 6.60 percent.

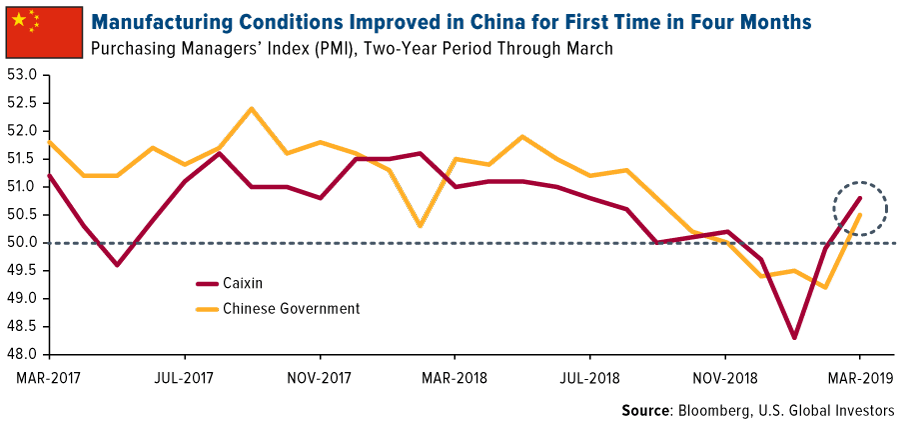

- China’s manufacturing sector just returned to growth for the first time in four months, a sign that its government’s economic stimulus appears to be working. Both the private Caixin and official Chinese government purchasing managers’ indices (PMI) beat consensus by rising sharply above 50.0 in March, indicating factory expansion.

Weaknesses

- Malaysia’s FTSE Bursa Malaysia Kuala Lumpur Composite dropped by 11 basis points on the week, while the Philippines’ PCOMP fell by 48 basis points.

- Amid a relatively risk-on week for Hong Kong and China, utilities was the worst performing sector in the HSCI since last Friday.

- South Korea’s exports dropped again for the March measurement period, falling by 8.2 percent year-over-year and coming up short of expectations for a 7.0 percent decline. Imports also missed, dropping by a year-over-year 6.7 percent, below expectations for only a 5.3 percent drop.

Opportunities

- The U.S.-China trade talks continue, as China’s Vice Premier Liu He returned to Washington this week, where negotiations went on and during which Liu also met with U.S. President Donald Trump. While Trump administration officials continue to preach patience and caution, the administration has also said it remains possible for a summit even within the next four weeks and President Trump said the deal could be “monumental.” China’s Liu hailed a “new consensus” amid the terms and for the text of the trade talks, which sounds an awful lot like progress. (Although, as President Trump cautioned when pressed about a summit, “If we have a deal, we’ll have a summit.”) This round of high level talks appears to have been geared toward approving a text and a set of terms that may be close enough to a done deal to get both sides on board for a summit and finalization of deal terms.

- Inflation in the Philippines continues to drop, falling for a fifth month running and now down to a 3.3 percent year-over-year print, beating expectations for a 3.5 percent print and a far cry from latter 2018’s high prints of 6.7 percent.

- While March revenue for Macau casinos was expected to drop by some 3 percent, it only ticked down by 0.4 percent, outperforming expectations, and taken in tandem with better PMI numbers, it may be indicative of more resilience than thought in the Chinese economy at present. Of course, Chinese stocks have been recovering over the past quarter as well, and all of this is nice to see amid what is technically still a trade war between the U.S. and China.

Threats

- U.S.-China trade talks remain ongoing and tariffs remain delayed in implementation; a collapse of the former or the commencement of the latter remain a collective threat until resolution one way or the other amid the dispute. This week there were promising signs—a new consensus, if you will—but it ain’t over ‘till it’s over.

- Higher energy prices could burden some of the region’s major importers: Brent is back over $70 at the moment.

- The U.S. dollar remains strong. To be sure, some resolution on Brexit or a pickup in the Eurozone might aid sterling or the euro, for example, but in general, out of the world’s big reserve currencies the U.S. dollar remains strongest, which could weigh on or spook emerging markets at some point. The dollar has not yet broken out to new 52-week highs, and the Fed remains on pause, but the U.S. has not yet ruled out further hikes, and the dollar remains strong in the meantime.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended April 5 was ICOBID, up 647.56 percent.

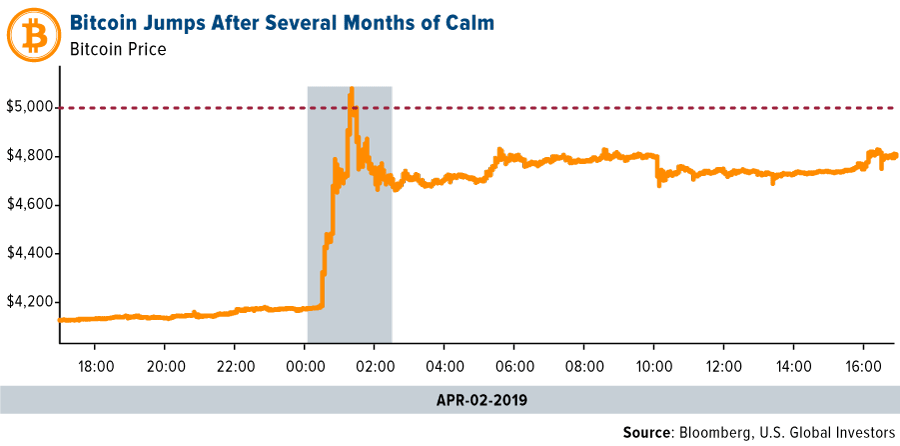

- On Monday, bitcoin advanced to the highest level of 2019, writes Bloomberg, rising as much as 1.6 percent to $4,135.60. Then on Tuesday morning, the digital currency surged even higher, rising as much as 20 percent and trading above $5,000 for the first time since last November. According to MarketWatch, the market value of all cryptocurrencies rose more than $15 billion in less than 90 minutes on Tuesday.

- Four exchange-traded products (ETPs) from XBT Provider that are tied to the prices of XRP and litecoin, went live this week on the Nordic Growth Market, a subsidiary of the Borse Stuttgart exchange. Ryan Radloff, CEO of XBT Provider parent company CoinShares, said in a statement that “this is another important step in the professionalization of the infrastructure around this asset class.”

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended April 5 was Expanse, down 79.70 percent.

- Despite bitcoin’s jump above $5,000 earlier this week, Bloomberg reporter Leonid Bershidsky writes that investors should have no fear of missing out because whatever the explanation, there’s no good reason to turn bullish on crypto. “Without the hype that often accompanies cryptocurrency spikes, more of the questionable ‘coins’ would die out faster, more dodgy exchanges would fail, and more scammers would move on,” Bershidsky explains. “Meanwhile, work could continue on ironing out the underlying blockchain technology’s kinks and finding some real-world applications.”

- Hut 8, a Canadian bitcoin mining firm, has laid off employees at its facilities in Alberta, according to the Canadian Broadcasting Corporation (CBC). A former employee told CBC that they were laid off along with two dozen other colleagues due to the 2018 bear market in cryptos and increased electricity costs. CoinTelegraph writes that Hut 8, which has mined 7,300 bitcoin to date, reported third quarter 2018 revenue of $13.5 million, but also had a net operating loss of $8.3 million.

Opportunities

- According to a recent job posting, the U.S. Securities and Exchange Commission (SEC) is seeking to hire a “crypto securities” advisor, reports CoinDesk. The posting outlines one of the key responsibilities of the new hire as applying their “knowledge of federal securities laws to digital asset securities and crypto matters, i.e., broker-dealer, exchange, clearing agency and transfer registrations, exchange product applications, sales and trading practices, etc.”

- PayPal announced earlier this week that it is making its first-ever investment in a blockchain technology company. The online payments giant has joined the extension of a Series A funding round in Cambridge Blockchain, writes CoinDesk, a startup that helps financial institutions and other companies manage sensitive data using shared ledgers.

- On Wednesday the SEC published new regulatory guidance for token issuers, nearly six months after it was announced that it was being developed. The new “plain English” guidance includes examples of both networks and tokens that fall under securities laws, as well as a project which does not, writes CoinDesk. Although there are still many unanswered questions about regulations, the guidance is a step forward for the industry.

Threats

- Police have frozen the assets owned by the founders of blockchain services company Vanbex, reports CoinDesk, as part of a fraud investigation into a 2017 initial coin offering (ICO) that raised $22 million. The company raised $30 million CAD (around $22 million) worth of fiat and cryptocurrency through the sale of a token called FUEL, which was supposed to be usable in a forthcoming smart contract system. However, Vanbex “developed no usable products,” and its founders “did not intend to develop the products they were marketing,” the article goes on to explain.

- Cryptocurrency uncertainty will continue in India. The nation’s Supreme Court postponed a case involving crypto exchanges and the Reserve Bank of India (RBI) until July. The RBI has a ban on crypto services and it has been hurting related businesses in the country for nine months now.

- The largest cryptocurrency exchange in South Korea, Bithumb, has reportedly lost $19 million in a cyber-attack. The exchange confirmed that no customer funds were lost, but that at least 20 million XRP tokens worth approximately $6.2 million disappeared.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits