This past weekend, we discussed the breakout of the markets to all-time highs.

The question I asked this past weekend was simply;

“The bull market is back, but can it stay?”

When I was growing up my father, probably much like yours, had pearls of wisdom that he would drop along the way. It wasn’t until much later in life that I learned that such knowledge did not come from books, but through experience. One of my favorite pieces of “wisdom” was:

“Exactly how many warnings do need before you figure out that something bad is about to happen?”

Of course, back then, he was mostly referring to warnings he issued for me “not” to do something I was determined to do. Generally, it involved something like jumping off the roof with a queen-sized bedsheet convinced it was a parachute.

My argument was always that “everyone else is doing it.”

After I had broken my wrist, I understood what he meant.

(What’s funny is that I am having the same conversations with my son today, and he is determined to figure out things the hard way simply because “everyone else is doing it.” Now, I truly understand what I put my Father through.)

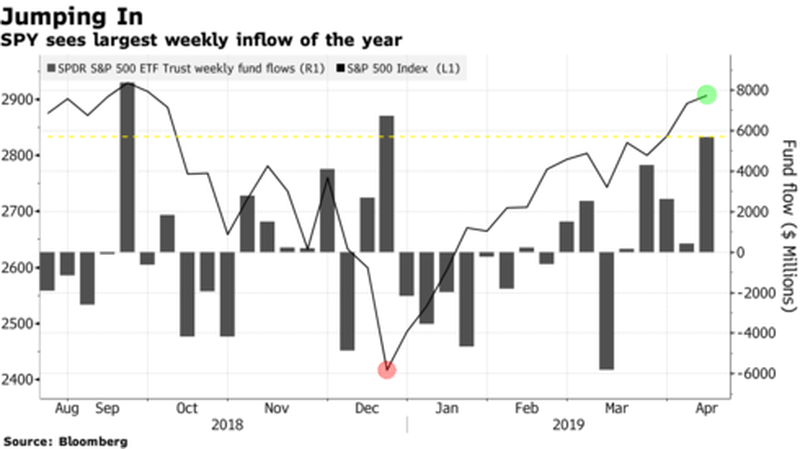

Likewise, investors are currently rushing to get back into the market, after bailing out in December, with a near reckless disregard for the consequences.

Simply because “everyone else is doing it.”

So, before you go “jumping off the roof with a bed sheet for a parachute”, there are some warning signs to consider before taking that leap.

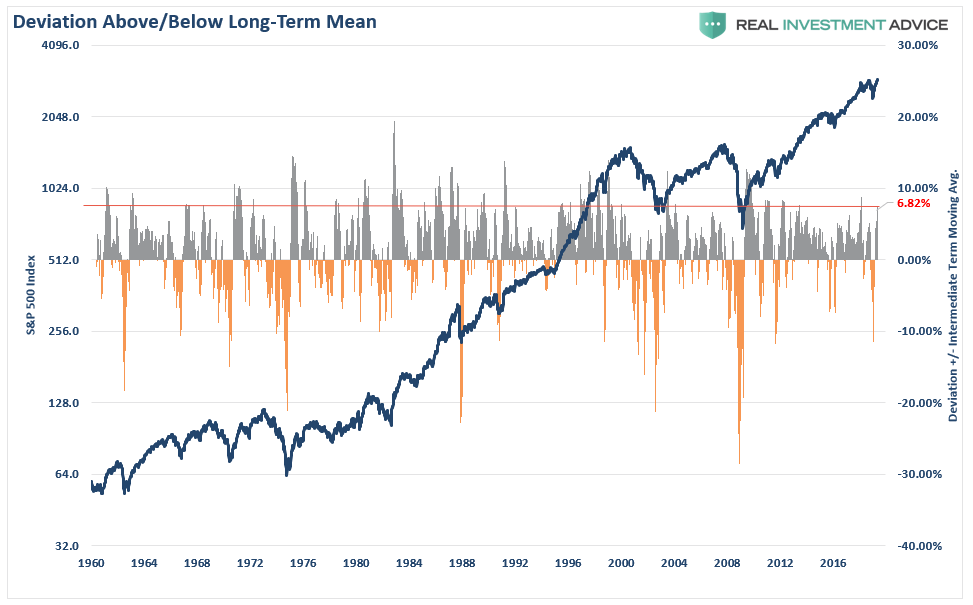

Warning 1: Deviations From The Mean

There is a funny story about a “defensive driving” class where the instructor asks the class how many thought they were “above average drivers.” About 80% of the class raised their hands. The funny thing is that all of them were in the class because of traffic violations or accidents. But more to the point, 80% of drivers cannot be above average. It is mathematically impossible.

Likewise, in investing, prices must be both above and below the “average price” over a set period of time for there to be an average. To many degrees “price” is bound by the laws of physics, the farther from the “average price” the current price becomes, the greater the pull back to, and generally beyond, the average. This is shown in the daily chart below.

Currently, the market is more than 8% above its longer-term daily average price. These more extreme deviations tend not to last an extraordinarily long time. Furthermore, reversions from these more extreme deviations tend to be rather quick.

If we step out to a weekly basis, we see the same warning.

At almost 7% above the long-term weekly moving average, the market is currently pushing the upper end of historical deviations.

The important point to take away from this data is that “mean reverting” events are commonplace within the context of annual market movements.

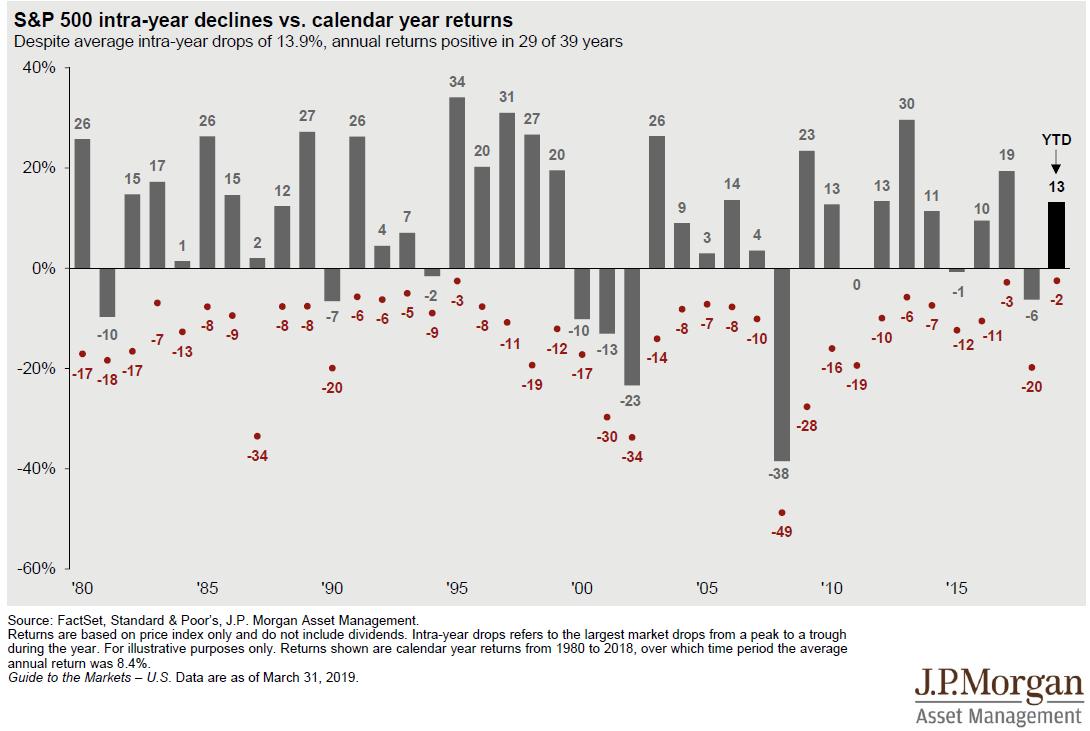

Currently, investors have become extremely complacent with the rally from the beginning of the year and are quick extrapolating current gains through the end of 2019.

As shown in the chart below this is a dangerous bet. In every given year there are drawdowns which have historically wiped out some, most, or all of the previous gains. While the market has ended the year, more often than not, the declines have often shaken out many an investor along the way.

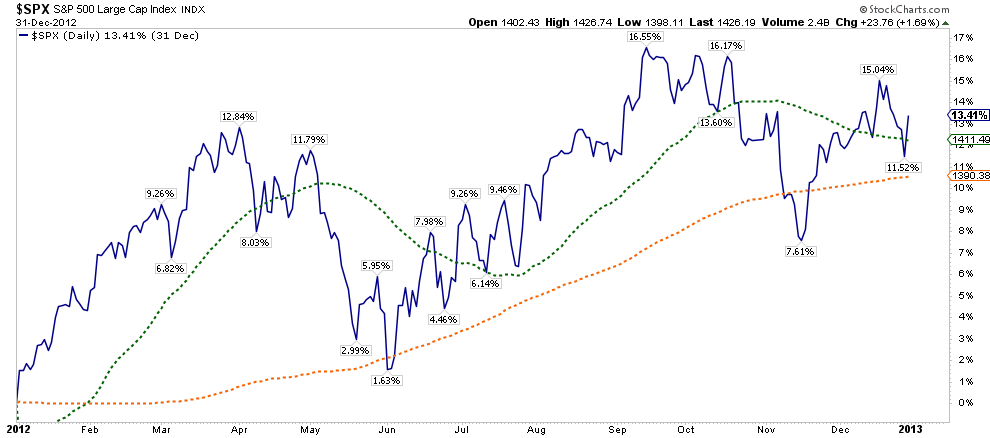

Let’s take a look at what happened the last time the market started out the year up 13% in 2012.

So far, it looks a whole lot like this year.

From a portfolio management standpoint, the reality is that markets are very extended currently and a decline over the next couple of months is highly likely. While, it is quite likely the year will end on a positive, particularly after last year’s loss, taking some profits now, rebalancing risks, and using the coming correction to add exposure as needed will yield a better result than chasing markets now.

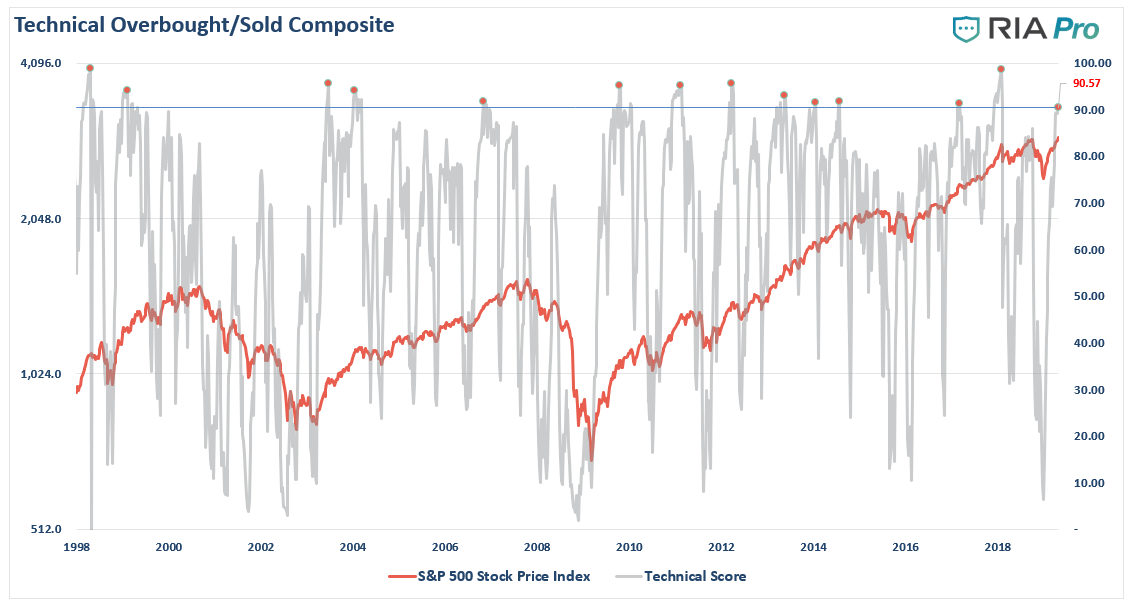

Warning 2 – Technical Warnings

The technical warnings also confirm our concerns about a near-term correction.

Each week, we post the chart below for our RIA PRO subscribers which is a composite index of our weekly technical measures including RSI, Williams %R, Stochastics, etc. Currently, the overbought condition of the market is near points which have denoted more significant corrections.

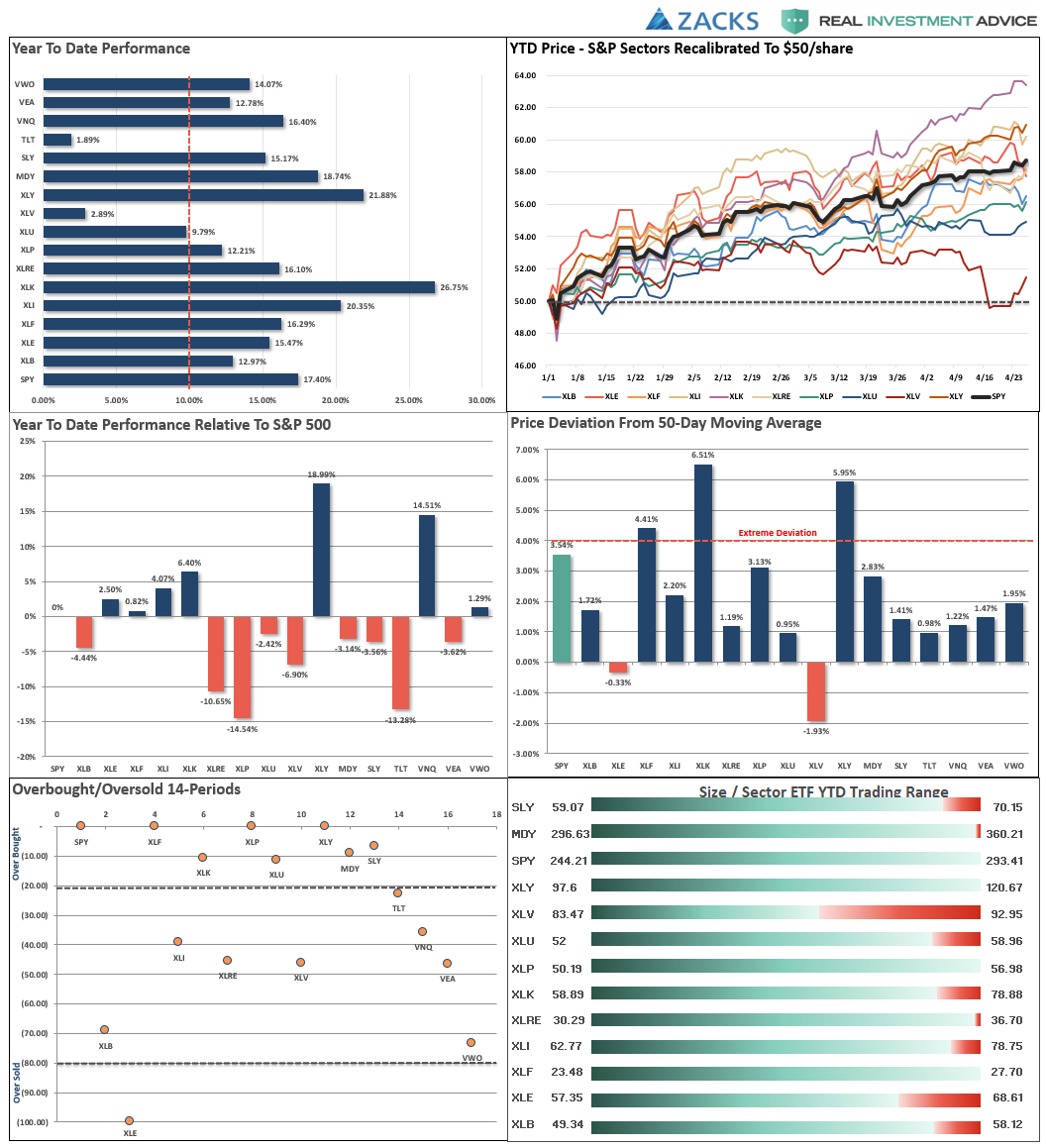

The market/sector analysis, which is also exclusive to RIA PRO members, shows the rather extreme price deviation in Technology, Discretionary, and Financials. Also, relative performance shows that it has primarily been Technology and Real Estate providing a bulk of the “alpha” year-to-date.

These are abnormalities that tend not to last long in isolation and rotations tend to occur rather quickly.

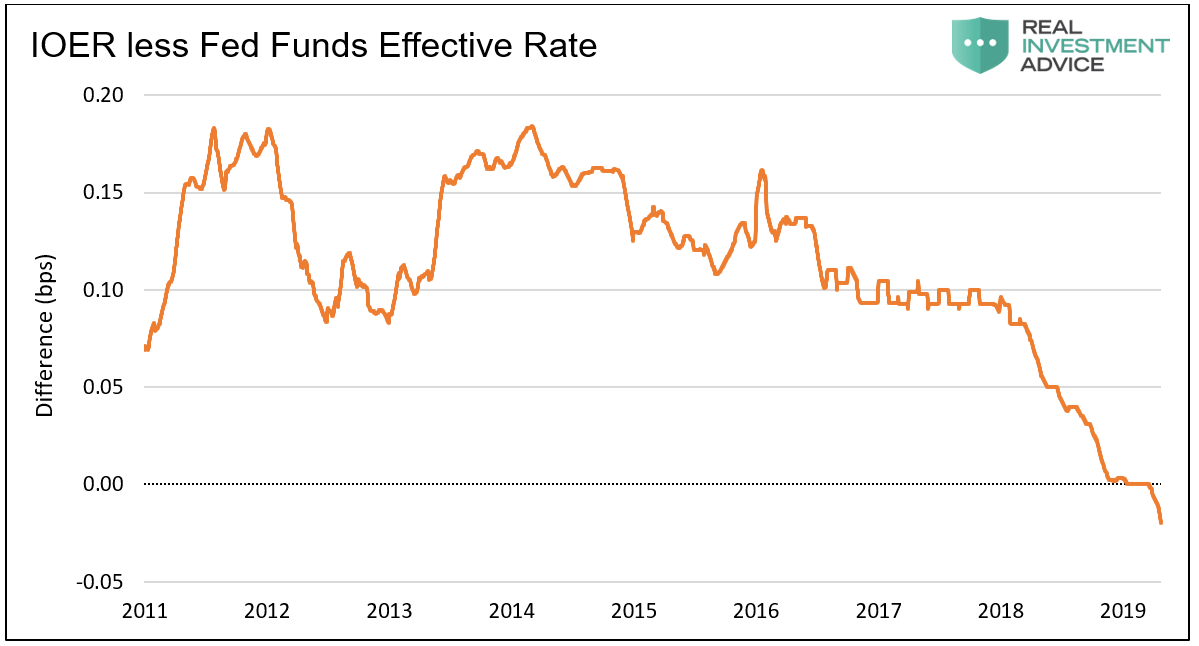

Warning 3 – Dollar Surge/Shortage

One of the lesser known issues with the markets currently was addressed by my co-portfolio manager, Michael Lebowitz, CFA:

When the Fed embarked on QE, they wanted to ensure that the money created to buy Treasuries and mortgages was being held by the banks as excess reserves and not being used to form loans. They also knew that controlling the Fed Funds rate would become problematic given the sharp increase in potential banking reserves. To help them keep the money on the sidelines and better control the Fed Funds rate, the Fed decided to pay banks interest on excess reserves (IOER). The IOER rate was set above the Fed Funds rate (the rate banks lend reserves to other banks on an overnight basis). The thought being that banks would rather collect a higher interest rate and take no risk than lend out money to other banks at a lower interest rate. On the flip side, if Fed Funds rose to the IOER rate, the banks would lend their reserves which should, in theory, provide a cap for Fed Funds.

The IOER premium over Fed Funds served its purpose in keeping excess reserves constant and in capping the Fed Funds rate from 2011 to 2017. However, as shown below, its effectiveness started eroding with the advent of QT in October of 2017

We believe the liquidity drain associated with QT created a shortage of dollars among foreign banks. Given this liquidity shortfall, foreign banks are likely being forced to pay higher interest rates for overnight funding. The Fed Funds rate is now higher than the IOER rate. That was not supposed to happen. Domestic banks either do not have the liquidity to lend or are being precautionary. Regardless of the reasons, a dollar shortage can become a dollar crisis if not addressed.

It is quite possible this situation will cause the Fed to stop QT before the scheduled September 30th end date. More importantly, it also raises the specter that QE, which injects liquidity into the banking system, is not as far off as we think. Watch the IOER/Fed Funds rate differential and the dollar for clues of further liquidity problems.

Warning 4 – Earnings

Lastly, as I discussed in this past weekend’s missive, earnings are not currently as “stellar” as the media makes them out to be. To wit:

“One of the reasons given for the push to new highs, and something we had previously said was highly probable, were the “better than expected” earnings reports coming in.

As noted by FactSet:

“Percentage of Companies Beating EPS Estimates (78%) is Above 5-Year Average

Overall, 15% of the companies in the S&P 500 have reported earnings to date for the first quarter. Of these companies, 78% have reported actual EPS above the mean EPS estimate, 5% have reported actual EPS equal to the mean EPS estimate, and 17% have reported actual EPS below the mean EPS estimate. The percentage of companies reporting EPS above the mean EPS estimate is above the 1-year (76%) average and above the 5-year (72%) average.”

Wow…that’s impressive and certainly would seem to be the reason behind surging asset prices.

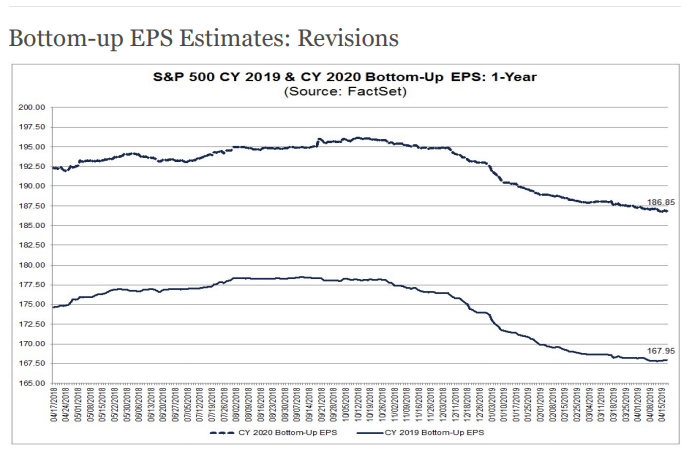

The problem is that “beat rate” was simply due to the consistent “lowering of the bar” as shown in the chart below:”

“As shown, beginning in mid-October last year, estimates for both 2019 and 2020 crashed.

This is why I call it ‘Millennial Soccer.’

Earnings season is now a “game” where scores aren’t kept, the media cheers, and everyone gets a “participation trophy” just for showing up.”

Importantly, the issue of buybacks continues to obscure the issue.

Not surprisingly, stock buybacks create an illusion of profitability.

Once that impact is removed the “soft underbelly” of actual earnings is fully exposed. The risk investors are taking is ultimately paying far too much for every dollar’s worth of earnings given that much of it is manufactured. While it may not matter now, it ultimately will matter.

If They Don’t “Buy & Hold” – Why Should You?

Here is the market for you year to date (via David Rosenberg):

- Alphabet +23%

- Microsoft +28%

- Apple +30%

- Amazon +30%

- Facebook +46%

(Disclosure: We are long Apple and Microsoft in our equity portfolio.)

These “warning signs” are just that. None them suggest the markets, or the economy, are immediately plunging into the next recession-driven market reversion.

But as David noted:

“The equity market stopped being a leading indicator, or an economic barometer, a long time ago. Central banks looked after that. This entire cycle saw the weakest economic growth of all time couple the mother of all bull markets.”

There will be payback for that misalignment of funds.

Past experience suggests that future returns will be far less than historical averages suggest. Furthermore, there is a dramatic difference between investing for 30-years, and whatever time you personally have left to your financial goals.

While much of the mainstream media suggests that you “invest for the long-term” and “buy and hold” regardless of what the market brings, that is not what professional investors are doing.

The point here is simple. No professional, or successful investor, every bought and held for the long-term without regard, or respect, for the risks that are undertaken. If the professionals are looking at “risk,” and planning on how to protect their capital from losses when things go wrong, then why aren’t you?

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

© Real Investment Advice

© Real Investment Advice

More Alternative Investments Topics >