Double Whammy: Fed Policy and the U.S.-China Trade War

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

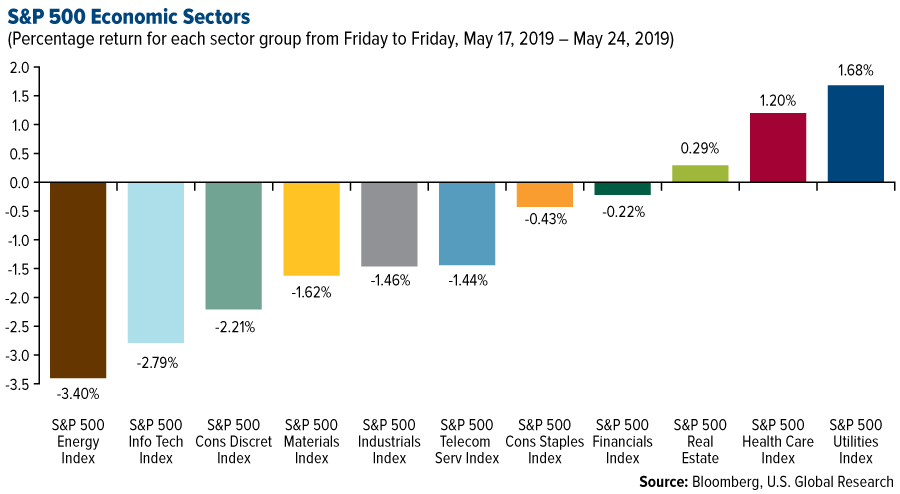

Markets were decisively in “risk-off” mode this week. Following weak manufacturing news on Thursday, the yield on the 10-year Treasury sunk to its lowest level since October 2017. The spread between the 10-year yield and three-month yield, in fact, inverted once again, with the shorter-term bond yield higher by 6 basis points. As such, the “boring” yet mostly reliable utilities sector has rotated to the top.

I’m not going to use the R-word here. All I’m going to say is that it might be time for investors to brace for a significant correction—especially with debt at record levels and the Federal Reserve left with very little firepower to combat a full-blown crisis.

Let’s take a look at what the smart money is doing.

Many successful, ultra high-net-wealth individuals (UHNWIs) favor municipal bonds, not only because they’re tax-free at the federal and often state and local levels, but also because they’ve managed to perform well even during equity bear markets. According to the first-quarter asset allocation report for Tiger 21, a peer-to-peer network for UHNWIs, members had an average weighting of 9 percent in fixed income, which includes muni bonds.

As many of you know, U.S. Global Investors has been known for gold and natural resource investing, but we also have longstanding experience in muni bond investing.

Speaking of gold, Ray Dalio said back in 2015 that “if you don’t own gold… there is no sensible reason other than you don’t know history or you don’t know the economics of it.” Time hasn’t changed Dalio’s mind. The billionaire hedge fund manager, the most profitable in U.S. history, just added to his gold holdings in the first quarter, according to SEC filings.

If you’re not doing the same, why not? The U.S. economy looks rock-solid with a strong jobs market, but there are some worrisome signs lurking under the surface.

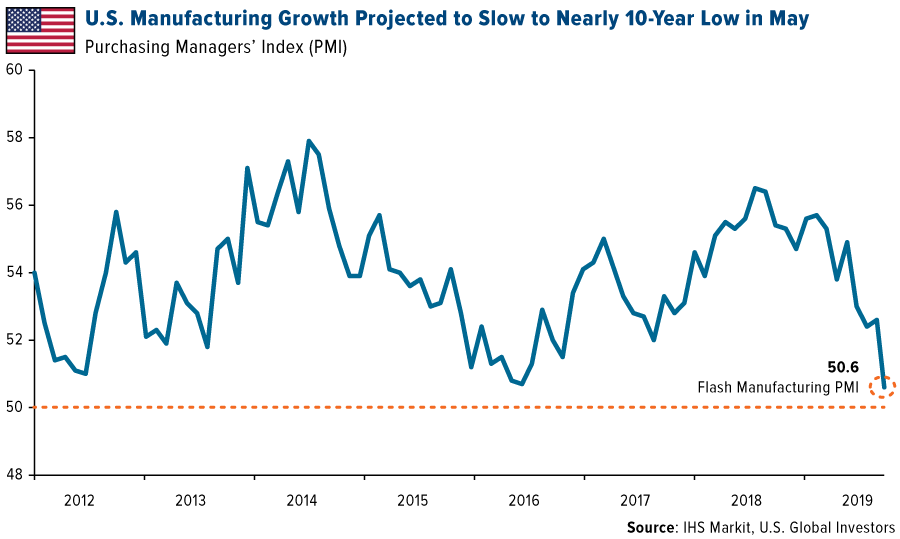

Could U.S. Manufacturers Contract in 2019?

Case in point: May’s “flash” index of U.S. manufacturers registered a sharp decline to 50.6, down from 52.6 in April. This is only a preliminary reading, but if it turns out to be accurate—we’ll know early next month—it would mark the slowest growth in the domestic manufacturing industry since September 2009, according to IHS Markit. Then again, it could fall below 50.0, which would indicate contraction.

Nearly all of the underlying economic data weakened from the previous month, including output, employment and inventories. New orders actually fell in May for the first time since August 2009, meaning U.S. manufacturers had a net negative number of orders. Business expectations sunk to a seven-year low.

As I’ve explained many times before, we see the manufacturing PMI as a leading indicator of future demand for energy and raw materials. But it also has obvious implications for earnings per share (EPS) growth and gross domestic product (GDP) growth.

IHS Markit’s report doesn’t comment on why manufacturers are in this position right now, but two big culprits jump to mind: the Federal Reserve and the U.S.-China trade war.

The Historical Fallout of Tightening Credit

Earlier in the month I shared a chart with you showing that every major slowdown in the U.S. manufacturing industry going back to the 1950s was preceded by a Fed tightening cycle. The way things are headed, this cycle looks to be no different. Fed Chair Jerome Powell has hinted that there will be no more interest rate hikes in 2019, but the “damage” has already been done, so to speak.

In a recent report, analysts at research firm Cornerstone Macro wrote that they believe the U.S. manufacturing index “will eventually break below 50.0 in 2019 as it HAS AFTER EVERY FED TIGHTENING CYCLE.”

| Tightening Cycle Began In: | U.S. Manufacturing PMI Fell Below 50 | EPS Recession | GDP Recession |

|---|---|---|---|

| 1954 | YES | YES | YES |

| 1958 | YES | YES | YES |

| 1961 | YES | YES | NO |

| 1967 | YES | YES | YES |

| 1972 | YES | YES | YES |

| 1977 | YES | YES | YES |

| 1980 | YES | YES | YES |

| 1983 | YES | YES | NO |

| 1988 | YES | YES | YES |

| 1994 | YES | NO | NO |

| 1999 | YES | YES | YES |

| 2004 | YES | YES | YES |

| Hit Rates | 100% | 92% | 75% |

| Source: Cornerstone Macro, U.S. Global Investors | |||

This is significant because it’s one of the final things to happen in nearly every business cycle of the past several decades. After the index dips below 50.0, we start to see employment weaken. (We’re already starting to see some of this. Ford alone has cut some 7,000 positions, with many more expected.) Around 92 percent of the time, an EPS recession followed manufacturing pullbacks, according to Cornerstone. After that, a GDP recession has occurred three quarters of the time.

China Digging In for the Long Haul

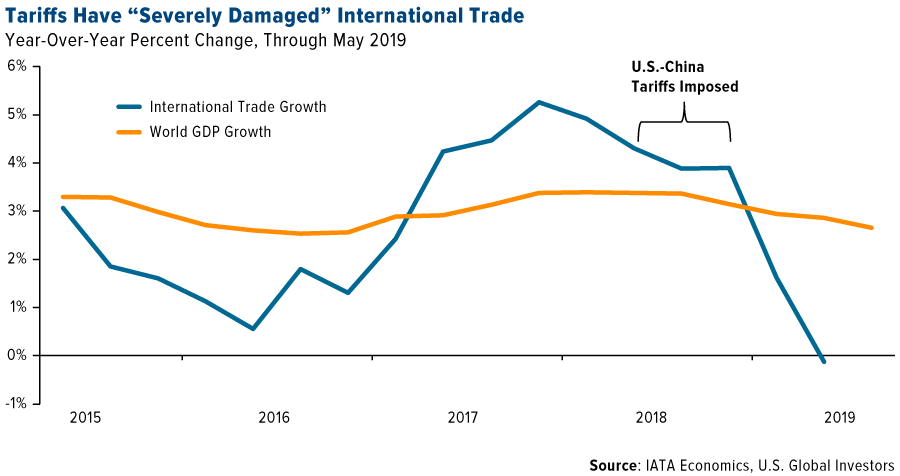

And then there’s the U.S.-China trade war, an end to which might still be some time away. This week Chinese president Xi Jinping told crowds that the country was “now embarking on a new Long March,” a sign that he could be preparing for a protracted engagement.

The skirmish has already “severely damaged” international trade volumes, according to the International Air Transport Association (IATA). Air cargo was down 2 percent in the first quarter of 2019 compared to the same period a year ago, while air freight rates between Hong Kong and North America have spiked.

Tariffs are hurting the competitiveness of American companies operating in China, a survey conducted earlier this month has found. Responding to the American Chamber of Commerce in the People’s Republic of China (AmCham), as much as 75 percent of China-based U.S. firms, and 81.5 percent of U.S. manufacturers, said that tariffs were having a negative impact on their business. More than 40 percent indicated they planned on relocating outside of China to avoid tariffs, but of those, only 6 percent said they were considering returning to the U.S.

But conditions here in the U.S. can be just as constricting for some companies, thanks to higher tariffs. In a report this week, UBS estimated that as many as 12,000 U.S. stores could close this year in response to tariffs, putting some $40 billion of sales at risk. The U.S. is already “over-stored,” according to the report, but so many store closures in a single year would be a major squeeze on the broader economy with mass job losses.

Goldman Sachs: Inflation Will Surge

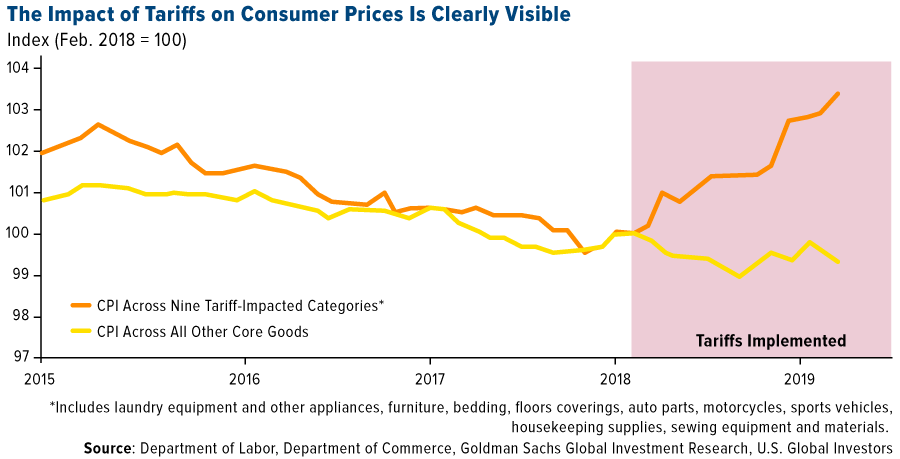

What I have my eye on most, though, is inflation. Tariffs and other trade restrictions are naturally inflationary.

In a recent note to investors, analysts at Goldman Sachs revised up their estimates of the impact tariffs might have on U.S. inflation. Look at the chart below. Although prices for total consumer goods—as measured by the consumer price index (CPI)—have declined over the past few years, prices for as many as nine separate categories hardest hit by tariffs have surged since the U.S.-China trade war began in early 2018.

Earlier this month, Trump raised tariffs from 10 percent to 25 percent on $200 billion worth of Chinese imports. If tariffs were imposed on an additional $300 billion, which Trump has threatened to do, inflation would rise “noticeably” above 2 percent next year, Goldman says. This would “slightly increase the likelihood” that the Fed would hike interest rates.

It should be pointed out that such tariffs are not generally paid by Chinese exporters. Instead, they are paid by U.S.-based importers, which often pass the extra expense on to the end consumer.

Cornerstone Macro weighed in on the subject in a note dated May 21, writing that tariffs are just one part of the inflation story right now—the other being rising fuel costs.

“Tariffs, coupled with rising gasoline prices, represent a double whammy for U.S. consumers,” the firm writes. It projects prices for gas and consumer goods to be up some 5 percent year-over-year in the second half of 2019.

Higher Inflation Has Historically Meant Higher Gold Prices

The good news in all this is that higher inflation has historically been supportive of the price of gold. In the years when inflation was 3 percent or higher, annual gold returns were 15 percent on average, according to the World Gold Council (WGC).

When gold hit its all-time high of $1,900 an ounce in August 2011, consumer prices were up nearly 4 percent from the same time the previous year. The two-year Treasury yield, meanwhile, averaged only 0.21 percent, meaning the T-note was delivering a negative real yield and investors were paying the U.S. government to hang on to their money. This created a favorable climate for gold, as investors sought a safe haven asset that would at least beat inflation. Go gold!

Happy Memorial Day!

Before I leave you, on behalf of everyone at U.S. Global Investors, I wish to thank all of the brave men and women who served and continue to serve this great country. Your bravery, dedication and sacrifice will always be remembered. Happy Memorial Day!

Finally, if you’re hitting the road this weekend, you’ll be in good company. The American Automotive Association (AAA) projects that an incredible 43 million Americans will be traveling this Memorial Day weekend, a 3.6 percent increase from last year and the most since 2005. Happy travels, and be safe!

Gold Market

This week spot gold closed at $1284.75, up $7.20 per ounce, or 0.56 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.71 percent. The S&P/TSX Venture Index came in off just 0.24 percent. The U.S. Trade-Weighted Dollar fell 0.40 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| May-23 | Initial Jobless Claims | 215k | 211k | 212k |

| May-23 | New Home Sales | 675k | 673k | 723k |

| May-24 | Durable Goods Orders | -2.0% | -2.1% | 1.7% |

| May-27 | Hong Kong Exports YoY | -0.8% | -- | -1.2% |

| May-28 | Conf. Board Consumer Confidence | 130.0 | -- | 129.2 |

| May-30 | GDP Annualized QoQ | 3.1% | -- | 3.2% |

| May-30 | Initial Jobless Claims | 215k | -- | 212k |

| May-31 | Germany CPI YoY | 1.6% | -- | 2.0% |

Strengths

- The best performing metal this week was palladium, up 1.49 percent as UBS published a report outlining its positive view on the precious metal; hedge funds raised their net long position in the metal after touching an eight-week low. Gold traders and analysts were neutral on their outlook for gold as a stronger U.S. dollar offset potential haven appeal, according to the weekly Bloomberg survey. UBS’s Joni Teves wrote that gold demand in India is supported by more wedding dates this year. Imports to the world’s second largest consumer of gold were up 60 percent year-over-year in April and 15 percent higher than the long-term average. More physical gold buying could be on its way from hedge funds and ETF investors. Bloomberg reports that positioning by money managers turned net long late in April and has been growing ever since, while holdings in ETFs have risen since May 13.

- Gold buying this year has so far largely come from the world’s central banks. Turkey’s gold reserves rose $63 million from the previous week, according to the central bank’s weekly figures. Kazakhstan increased its gold holdings in March to 11.79 million ounces. Russia, who is one of the biggest gold buyers, saw its first quarter gold output rise 13 percent year-over-year to 58.12 tons.

- Another two countries that want to up their gold intake? Serbia and the Philippines. The Serbian President told its central bank governor that it wants to start buying gold as a safety measure and boost reserves by 10 tons this year. The Philippines passed a law exempting gold sales by small-scale miners to the central bank from excise and income taxes, reports Reuters.

Weaknesses

- The worst performing metal this week was platinum, down 1.64 percent. Platinum fell to a three-month low this week as declining auto sales deter investors, reports Bloomberg. Audi signaled it plans to offer more than 30 electrified cars by 2035, replacing diesel vehicles. Sentiment for the metal reversed sharply this year as holdings in ETFs backed by platinum have slipped and the net-long position has fallen.

- Gold investors are getting tired of the lack of momentum in the metal’s trading. Ole Hansen, head of commodity strategy at Saxo Bank, told Bloomberg that “potential gold investors are being left frustrated and sidelined by the yellow metal’s lack of momentum despite an escalating trade war, heightened concern about stability in the Middle East, recent stock market gyrations and the decline of bond yields.”

- Zimbabwe, facing hyperinflation and shortages of foreign currency, fuel, medicine and more, has secured a $500 million loan by pledging an undeveloped mine to creditors. Bloomberg writes that the loan will be paid over four years when production of the mine starts and is backed by a mine that Great Dyke Investments owns – a venture between Russian investors and the Zimbabwean military.

Opportunities

- According to JPMorgan, traditional hedges like gold and the yen have not done well since the beginning of the U.S.-China trade war, but that could soon reverse due to a more dovish monetary backdrop. Bloomberg reports that strategists including John Normand wrote in a note last week that the combination of a Federal Reserve that has stopped tightening policy and investor positioning that suggests the two assets are under-owned and could see their performance as hedges improve in the rest of 2019 and 2020.

- On Wednesday gold futures rebounded from a two-week low as equities fell and copper continued to fall. What does the falling price of copper relative to gold have to do with anything? Bloomberg’s Eddie van der Walt writes that the ratio is a useful gauge of sentiment because it measures the price of a key industrial input (copper) against that of a perceived haven against economic turmoil (gold). The ratio is heading for a fifth straight weekly drop, which is the longest run since early 2018.

- Citi upgraded Newmont Goldcorp to a buy and said that it offers “superior value” versus its peers in a challenging market, reports Bloomberg. The bank also downgraded Barrick to neutral. Giant Barrick Gold Corp. is proposing it buys the shares of Acacia Mining Plc that it doesn’t already own at a discount. The proposal implies a valuation of $787 for the entirety of Acacia, which is well below current market capitalization of $832 million. Barrick’s last no premium offer for Newmont back in February was withdrawn after just 17 days, as investors thumbed their nose at the offer. Will a discounted offer win the day? Not likely.

Threats

- Diamond sellers continue to struggle. De Beer’s diamond sales plunged to the lowest since 2017 and dropped 25 percent from a year earlier. Bloomberg’s Thomas Biesheuval reports that diamond miners are facing challenges across the board and especially those producing cheaper and smaller gems where there is too much supply. A weaker rupee has made diamonds more expensive for Indian manufacturers who cut or polish nearly 90 percent of the global supply.

- Are Indians falling out of love with gold? The answer is potentially yes, according to younger consumers. About one third of Indians are aged 18 to 35 and they often prefer to spend their money on electronic gadgets with monthly installments rather than jewelry. Some say that gold is no longer a sign of wealth, but rather it is simply fashion. Another factor that could hurt gold buying is that mutual funds have returned 12.5 percent annually in the last decade, reports the Economist, and that during the same period gold prices increased by just 7 percent.

- This week we had an unsolicited call from a U.S.-listed company making a pitch on the merits of investing in their gold mining operation. We listened; you never know what is being presented until you hear the pitch. Unfortunately, these early stage investments are risky and one has to be a bit cautious. After all, you are handing your hard earned money over to someone in exchange for a piece of paper attached to a vision of future wealth creation. Often times retail investors might not know the right questions to ask in order to make an informed decision. This company is just starting to produce gold, thus they should have a resource statement (so there is reasonable disclosure of what assets the company is going to mine). There wasn’t one. The good news about the point we are making here, is that we have seen a lot of these promotions, but they don’t tend to surface as often, unless we are in a bull market for gold.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.69 percent. The S&P 500 Stock Index fell 1.17 percent, while the Nasdaq Composite fell 2.29 percent. The Russell 2000 small capitalization index lost 1.41 percent this week.

- The Hang Seng Composite lost 2.42 percent this week; while Taiwan was down 0.54 percent and the KOSPI fell 0.51percent.

- The 10-year Treasury bond yield fell 7 basis points to 2.32 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector of the week, increasing 1.68 percent, compared to an overall decrease of 1.12 percent for the S&P 500 Index.

- Target was the best performing stock for the week, increasing 15.07 percent.

- Avengers: Endgame is now the second-highest grossing movie in U.S. box office history. Disney's superhero team-up film has raked in more than $781 million in total domestic sales since its opening four weeks ago.

Weaknesses

- Energy was the worst performing sector for the week, decreasing 3.40 percent compared to an overall decrease of 1.12 percent for the S&P 500.

- Kohl’s was the worst performing stock for the week, falling 19.61 percent.

- Boeing reportedly didn't receive a single order for the 737 Max last month. The plane maker last month also didn't receive orders for other popular aircraft such as the 787 Dreamliner or the 777, CNN says.

Opportunities

- On Thursday, JPMorgan analyst Christopher Horvers upgraded Target to overweight from neutral, and added $19 to his price target, to $100. He argues that the shares are undervalued and could surpass consensus estimates. “We believe it should revalue towards the best-in-class Amazon-safe bucket,” he wrote.

- Analysts at Goldman Sachs upgraded General Dynamics to buy. With General Dynamics down 19 percent in the 52-week period, Goldman argues that any headwinds still opposing the stock are now priced into the shares, which currently trade at the low-end of historical ranges.

- Slack is getting ready to go public. The buzzy workplace-chat platform last valued at over $7 billion filed paperwork to publicly list its shares through a direct listing. It could go public on the Nasdaq this month or in June.

Threats

- If you’re an investor who believes, as many do, that the U.S.-China spat will be resolved mostly because any alternative would be catastrophic, the recent history of international trade rifts is probably not something you want to think too hard about, writes Bloomberg News’ Sarah Ponczek. While parallels between the Trump-Xi showdown and Britain’s secession drama are imperfect and the forces not quite a match, equity bulls pinning their hopes on common sense and mutual self-interest should take heed. Just because something should be resolved doesn’t mean it will. “The logic is that it has to, because it’s so bad on both ends if we don’t. But my only concern is we used that exact same logic with Brexit numerous times,” said Samantha Azzarello, global market strategist for JPMorgan ETFs. “When there’s group-think and everybody is thinking this, the repercussions, at least in the shorter-run, can be even more magnified for market reaction. Both the US and China have strong incentives to reach a deal and we do not expect a complete breakdown in negotiations.” To that, it might be observed: neither did the U.K. and the European Union (EU). The reality has been different. After spending years deluded into a belief British voters would never elect to leave, investors gasped when they did. In the three years since, virtually every hope pinned on cooler heads has unraveled. Politics has proved too fickle a force to model.

- The private-equity boom is supercharging a major risk to the stock market. "There's not much inventory in many of these asset classes, as we know," said Mark Machin, the CEO of the Canada Pension Plan Investment Board, at the Milken Institute Global Conference. "We saw the behavior — the gapping in December — in a number of these markets, and I think you're going to find that risk models could blow up very quickly on the public side and trigger more events. So I think people need to be super careful."

- MoviePass' parent company had a brutal 2018. Helios & Matheson lost $288 million last year, according to a "preliminary evaluation" filed with the Securities and Exchange Commission (SEC) on Wednesday.

The Economy and Bond Market

Strengths

- The number of people who applied for unemployment benefits in mid-May fell slightly and returned close to a half-century low, signaling that the U.S. jobs market is still going strong. Initial jobless claims, a rough way to measure layoffs, dipped by 1,000 to 211,000 in the seven days ended May 18, the government said Thursday.

- Mortgage applications rose by 2.4 percent on a seasonally-adjusted basis from one week earlier for the week ending May 17, according to the Mortgage Bankers Association’s latest Weekly Mortgage Applications Survey.

- The latest Bloomberg Consumer Comfort Index edged up to 60.3 from the previous 59.9, a marginal improvement.

Weaknesses

- Orders for durable goods tumbled in April due to falling demand for Boeing jets and new cars and trucks. Even more worrisome, business investment continued to weaken in the face of trade tensions with China and a slower U.S. economy. Orders for durable goods dropped 2.1 percent in April. The increase in orders in March was also marked down.

- American businesses grew in May at the slowest pace since before President Trump was elected, a pair of new surveys show. An IHS Markit “flash” survey of U.S. manufacturers fell to a nine-and-a-half year low of 50.6 this month, down from 52.6 in April. The firm’s survey of U.S. service-oriented companies, such as banks and retailers, slipped to a 39-month low of 50.8, down from 52.7. A reading over 50 signifies that companies are growing, but the sharp decline in the indexes this year suggests the U.S. economy could slow in the months ahead, especially if the dispute with China drags on.

- The U.S. housing market continued to soften in April, with the spring selling season so far proving a disappointment despite falling mortgage rates and a strong economy. Existing home sales fell 0.4 percent in April from the previous month to a seasonally adjusted annual rate of 5.19 million, the National Association of Realtors said on Tuesday. Compared with a year earlier, sales in April declined 4.4 percent, which is the 14th straight month of annual declines. The housing market is “underperforming in relation to economic performance, with job creation and [lower] mortgage rates,” said Lawrence Yun, the trade group’s chief economist.

Opportunities

- Personal income growth is anticipated to have accelerated slightly to 0.2 percent month-on-month in April, while personal consumption is forecast to have moderated from 0.9 percent to 0.2 percent month-on-month. More importantly, the core personal consumption expenditures (PCE) price index, which the Fed tracks for its inflation target, is projected to have stayed unchanged at 1.6 percent year-on-year in April.

- The Conference Board’s Consumer Confidence Index due next Tuesday is forecast to edge up from 129.2 to 129.8 in May.

- The MNI Chicago PMI due next Friday is forecast to move up to 54 from 52.6.

Threats

- The rally in Treasuries has gone too far for now, according to Citigroup Inc. Investors should take profits in long 10-year Treasury positions, as a possible double-bottom technical pattern and potential weakening in downside momentum suggests yields could bounce back to 2.6 percent in the short term, strategists including Jeremy Hale wrote in a note. “We are taking profits on our long 10-year position and look to re-enter if yields bounce back,” they said.

- Another spotlight next week will be on the second estimate of GDP growth in the first quarter. The preliminary estimate had shown the U.S. economy expanded by an annualized rate of 3.2 percent in the first quarter. Analysts are predicting a small downward revision to 3.1 percent in the second print.

- Should the core PCE price index fail to head higher over the next few months, or worse, drift further lower, pressure would grow on the Fed to cut rates. The U.S. central bank has so far stuck to its neutral stance even as global risks to growth rise. But even if the Fed did start to signal a move towards a rate cut, the absence of bright spots elsewhere in the world is likely to cast an overall bleak picture.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was coffee, which gained 6.81 percent on concern of pending cold weather in Brazil’s Minas Gerais region that could damage crops. On Friday nickel surged almost $500 in just a few minutes to $12,460 per ton on the London Metals Exchange. Iron ore saw a big jump this week on positive China demand forecasts and upgrades. Both UBS and Goldman Sachs upped their price outlooks for the metal saying that an unexpected rise in Chinese demand for steelmaking is compounding supply shortfalls, reports Bloomberg. Iron ore futures in Singapore spiked above $100 per ton early this week.

- Bloomberg reports that Saudi Arabia and other OPEC producers have signaled their intention to keep oil supplies constrained for the remainder of the year. Russia’s exports of crude to the U.S. are “on steroids” as the world’s largest foreign producer outside of OPEC takes advantage of lost supply from Venezuelan sanctions.

- A Shell-operated carbon capture and storage project in Canada hit a milestone of sequestering 4 million tons of carbon dioxide nearly six months ahead of schedule, and with a lower than estimated cost. Anne Halladay, an advising geophysicist on the project, says that large projects such as this need capital and more regulatory incentives to get built, but that the fast progress from this Shell project could spark more interest from investors.

Weaknesses

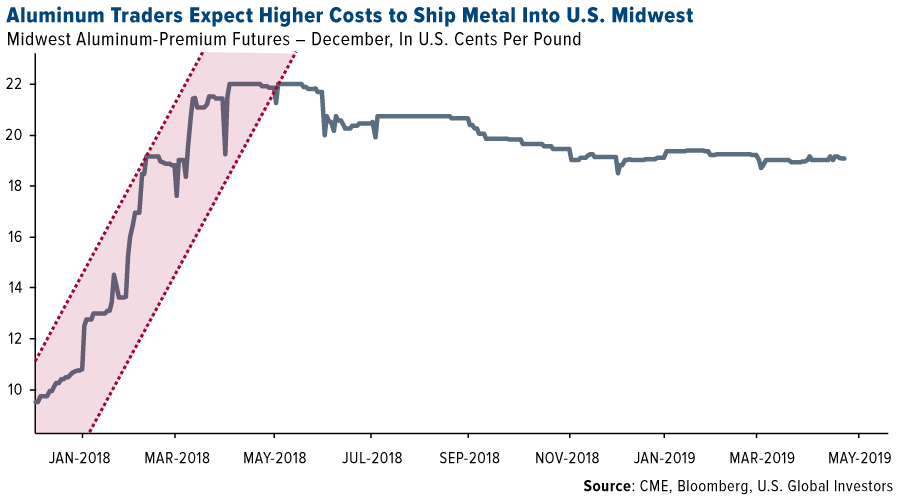

- The worst performing major commodity for the week was crude oil, which fell 6.37 percent on fears regarding how the U.S.-China trade war will hit demand. Crude oil suffered its worst day of 2019 on Thursday as U.S-China trade tensions send investors fleeing from risky assets. Copper is on its worst run in eight months and hit a new four-month low in London this week. Steel manufactures are also taking a hit with the S&P Supercomposite 1500 Steel Index closing 4.3 percent lower on Thursday than it did when President Donald Trump was elected in November 2016, reports Bloomberg. Steelmakers fell after Credit Suisse lowered ratings after Trump ended tariffs on Canadian and Mexican imports of steel. Lastly, aluminum consumers are suffering from the tariffs. Aluminum traders are expecting higher costs to ship the metal into the U.S., which can have a big impact on the beer industry – a big consumer of aluminum. The industry is blaming tariffs for 40,000 job losses.

- British Steel was put into liquidation by the U.K. high court this week as the company failed to stay profitable during its three year run. This will put 5,000 jobs at risk and is another big hit to the nation’s steel industry, which has long struggled to be profitable in the face of high energy and labor costs, reports Bloomberg.

- Zambia is once again taking steps to nationalize copper mining. The nation is planning to takeover Vedanta Resources’ mining assets after allegedly lying about expansion plans and cheating on taxes. Zambia’s Eurobond yields rose to record highs after the news broke, up to 19.68 percent. Bloomberg reports that no other nation, apart from Venezuela, has yields that high, which is a signal that assets are well into distressed territory.

Opportunities

- Glencore signed a battery materials pact with First Cobalt that could help restart the only North America refinery focused on cobalt, which is used in electric vehicle batteries, reports Bloomberg. The supply agreement is for Glencore to provide feedstock for the facility that is expected to produce as much as 2,500 metric tons of cobalt in sulfate.

- Fortum is building a 90 megawatt wind park in Finland with Vestas Turbines. The project will consist of 21 wind turbines and construction is set to begin this summer.

- A new development in solar nears commercial production. Oxford Photovoltaics, which is a U.K. company developing solar cells, announced that it had achieved a 28 percent conversion efficiency for its new tandem perovskite-based solar cell. This is higher than the 22 percent efficiency for the average silicon cell, reports BloombergNEF.

Threats

- Rare earths could soon become a big part of the growing U.S-China trade war. China is the dominant global supplier of rare earths, and the U.S. relies on China for about 80 percent of its supply for use in software and semiconductor products. Chinese President Xi Jinping visited a rare earths facility this week, which raised speculation that the materials could be weaponized in negotiations. China Rare Earth Holdings rose as much as 95 percent in response to President Xi’s plans to boost innovation in the sector.

- The world’s biggest maker of liquid fuel from coal, Sasol, was hit with downgrades from Citi, JPMorgan, Macquarie and RenCap after the company said the cost of its Lake Charles project will rise 50 percent more than initially planned, reports Bloomberg. The ballooning costs for this Louisiana project is a big setback for the South African company’s international expansion plans.

- A $2 billion infrastructure spending plan, a cause both sides of the aisle in the U.S. were supposed to be in agreement on, might be far from moving forward. In a meeting this week with Democratic leaders, President Trump stormed out after saying that he won’t work with them until the investigations into him and his administration end.

Emerging Europe

Strengths

- Russia was the best relative performing country this week, gaining 1.6 percent. Stocks trading on the Moscow exchange reached a new, one-year high this week. Wages in Russia unexpectedly grew in March and April as inflation began to retreat from its spike. The central bank may resume cutting rates in June.

- The Polish zloty was the best performing currency this week, gaining 79 basis points against the U.S. dollar. The currency was supported by strong retail sales, which came in at a seven-year high. Economic growth is expected to remain at 4 to 5 percent this year.

- Energy was the best performing sector among eastern European markets this week.

Weaknesses

- Austria was the worst performing country this week, losing 3.4 percent. A political corruption scandal weighed on equities trading on the Vienna exchange. Snap elections will take place in September following the collapse of the coalition government.

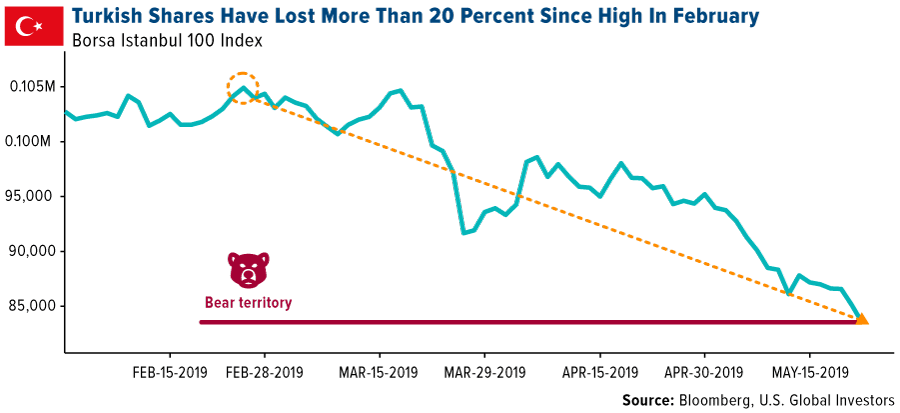

- The Turkish lira was the worst performing currency this week, losing 33 basis points against the U.S. dollar. Domestic and international tensions weighed on the country’s currency. Turkey claimed to stop taking delivery of oil from Iran in respect of the U.S. demands. However, the country is still on track to take delivery of the S-400 missiles from Russia, opening the door to new sanctions from the United States.

- Industrials was the worst performing sector among eastern European markets this week.

Opportunities

- Previously, Russia agreed to reduce the country’s oil output by 228,000 barrels a day, but now it may not want to extend the deal any longer. Former economy minister said that Russia recorded slower growth in the first quarter because the country produced less oil, its main source of revenue. If OPEC members extend further their curbs on oil production, but Russia backs out of it, the country will benefit from higher oil prices and stronger production volume.

- The Prime Minister of the United Kingdom Theresa May will step down on June 7. After years of her unsuccessful Brexit trade negotiations, the incoming prime minster may bring new tactics to the trade negations on the domestic and international front. The new prime minister will be placed before July 20. The market reacted positively to this news.

- JPMorgan, in its “EM Dividends Nobles – Looking for Shelter in Volatile Times” report, listed stocks that consistently increased their dividends per share over the past five years. Out of a sample set of 1,135 companies within the MSCI Emerging Market Index, JPMorgan created a list of 64 stocks. While Chinese and Taiwanese companies represented a majority of the list, Russian equites made up 7.8 percent, with steel producers like Severstal and Novolipetsk in the top two spots. Sberbank and Lukoil were placed not too far behind.

Threats

- Eurozone preliminary manufacturing PMI data for May came out at 47.7 versus the prior reading of 47.9 and expected 48.1. However, the service sector remains strong, keeping the composite PMI above the 50 level that separates expansion from contraction. The EU’s service PMI was reported at 51.6 versus the prior reading of 51.5 and expected 51.7.

- The Istanbul exchange has declined more than 20 percent since its peak in February, entering a bear market. Domestic and international political pressures as well as a weakening lira against the dollar may put further pressure on Turkish equites.

- The elections to the EU parliament are taking place this week. Europe’s traditional political parties – the center-right European People’s Party and the center-left Socialists and Democrats -- will likely lose some seats in parliament, while the nationalist and far-right parties will gain more power. The Europe of nations and Freedom group (far-right) is predicted to win 62 seats, compared to 37 currently.

China Region

Strengths

- India was the best performing country in the region this week, up 3.96 percent. Indian equities climbed and key gauges rose to records, capping their best weekly gains in nearly seven months, as Prime Minister Narendra Modi cruised to his second successive victory.

- The best performing sector in Hong Kong’s Hang Seng Composite Index for the week was utilities, up 1.70 percent.

- Taiwan’s year-over-year export orders for the April measurement period declined by less than expected, dropping only 3.7 percent, much slower than the previous reading and ahead of analysts’ estimates for a 6.5 percent decline.

Weaknesses

- Hong Kong was the worst performing country in the region this week, down 2.12 percent.

- The worst performing sector in Hong Kong’s Hang Seng Composite Index for the week was information technology, down 6.96 percent.

- Singapore’s first quarter 2019 year-over-year GDP growth clocked in at only 1.2 percent, below analysts’ estimates for a 1.4 percent print and down from the prior reading of 1.3.

Opportunities

- India’s incumbent Prime Minister Narendra Modi now appears to have a decisive—and historic—reelection, even as the BJP garners enough votes for a single party majority.

- As has been the custom lately—and because any new reader should also be aware—we will reiterate that the possibility of some kind of trade deal with China has still not been ruled out. Only time will tell. But if indeed a trade deal is reached, or if we get any positive confirmation on the future of tariffs between the two economic juggernauts, those developments may well present opportunities for rebounding sentiment and possibly markets as well. President Trump indicated late this week that there remains a “good chance” (to be sure, words we’ve heard before, so there is no change in substance at this point) of a trade deal with China, and President Trump and President Xi are still reportedly scheduled to meet at the upcoming G20 summit.

- And to keep up the finalizing of election results, Indonesia’s incumbent Joko Widodo has also been declared the official winner this week in the country’s recent election, and JokoWi has already begun to put out ambitious new plans for the new term, which include continuation of infrastructure development and the target of 7 percent GDP growth.

Threats

- The threat of trade war escalation and Huawei fallout continues for global investors. There does remain a possibility for improved sentiment and some kind of positive developments toward a trade deal as we wait for the reported Osaka G20 sit-down between Presidents Trump and Xi, but just remember, “It ain’t over ‘till it’s over …”

- The Chinese yuan stabilized somewhat in the sense of ceasing declines, but remains elevated (weak) and therefore a threat. This week the PBOC asserted it maintains the tools to stabilize the yuan as needed.

- The U.S. dollar, on the other hand, put in new 52-week highs this week, and remains strong relative to the rest of the world’s major currencies, which could equally serve as a threat to EM sentiment.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 24 was ShareX, up 832.42 percent. AT&T announced on Thursday that it will now accept bill payments in the form of cryptocurrency by way of BitPay, reports CoinDesk. “We have customers who use cryptocurrency, and we are happy we can offer them a way to pay their bills with the method they prefer,” said Kevin McDorman, vice president at AT&T.

- After last Friday’s sudden drop in the price of bitcoin to $6,178, the start of a new week brought with it renewed upward price movement. On Monday, the popular digital currency jumped as much as 17 percent, briefly breaching the $8,000 level, writes Bloomberg. Bitcoin has now logged double-digit gains for three consecutive weeks.

- After receiving secondary-market trading approval, Grayscale Investments LLC announced that its investment vehicle that holds Ether will open soon to mom-and-pop buyers, writes Bloomberg. Previously, the minimum purchase for the Grayscale Ethereum Trust had been $25,000 for accredited and institutional investors, but now small investors will be able to buy shares in the trust in over-the-counter markets, after gaining FINRA approval.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended May 24 was Soma, down 77.93 percent.

- The U.S. Securities and Exchange Commission (SEC) has delayed its decision on another bitcoin ETF proposal, reports CoinDesk. On Monday, a document was filed with the SEC instituting proceedings on whether or not to approve a proposed rule change that would allow the VanEck SolidX Bitcoin Trust to issue and list its shares. The regulator invited comments from the public, and a new deadline for the SEC to make a decision is August 19. The SEC has delayed making any decision on two proposals so far this year, the article continues, with the latest delay on Bitwise’s proposal coming on May 14.

- Bitcoin “dived out of a narrowing price range on Wednesday,” reports CoinDesk, opening the doors for a deeper drop to $7,200. The fall confirmed a downside break of what is known as a contracting triangle pattern, which is a series of higher lows and lower highs created in the first two trading days of the week. As the article explains, as a result bitcoin could continue to lose altitude in the short term.

Opportunities

-

The U.S. Internal Revenue Service (IRS) is working to release its first tax guidance for cryptocurrency since 2014, reports CoinDesk. The agency’s commissioner Charles P. Rettig outlined a non-specific plan to release the in-depth guidance in response to a request on reporting the digital currencies. “I share your belief that taxpayers deserve clarity on basic issues related to the taxation of virtual currency transactions and have made it a priority of the IRS to issue guidance,” Rettig wrote.

- This week the U.S. Copyright Office awarded Craig Wright the registration for the whitepaper on bitcoin, along with the computer code underlying the original cryptocurrency, reports Bloomberg. This was done under the pseudonym Satoshi Nakamoto. The news gave bitcoin SV a bump earlier in the week, despite the fact the Copyright Office has clarified that it does not “officially recognize” anyone as the inventor of bitcoin.

- After a minister in Russia once proclaimed that the country would never make cryptocurrencies legal, now the Russian Central Bank is considering the use of a gold-backed digital currency, reports CoinDesk. On Thursday, Elvira Nabiullina, governor of the Bank of Russia, announced that her institution will review a proposal for the development of the cryptocurrency, however, she added that “in my opinion, it is more important to develop settlements in national currencies,” the article continues.

Threats

- The Australian Federal Police (AFP) announced in a media release Tuesday that a 33-year-old government employee has been charged after he was caught mining cryptocurrency at work. The release alleged that the IT contractor had modified government computer systems to mine cryptocurrency worth over AU$9,000 for his own gain, CoinDesk details. The charges carry a maximum penalty of 10 years imprisonment and two years’ imprisonment, respectively.

- Circle, a cryptocurrency startup which owns the USDC stablecoin in partnership with Coinbase, has laid off 10 percent of its staff, reports CoinDesk. “We made these changes in response to new market conditions, most importantly, an increasingly restrictive regulatory climate in the United States,” CircleCEO Jeremy Allaire said. The cuts primarily affect Circle’s Boston headquarters.

- Changpeng Zhao, Binance founder and CEO, is taking a unit of Sequoia Capital back to court after the VC investor’s case against him was dismissed, reports CoinDesk. Zhao says Sequoia Capital China hurt his reputation and prevented him from raising money at favorable valuations. In a filing submitted on May 20 to the High Court in Hong Kong, Zhao has sent an application via his attorneys for a hearing before the court chambers on an order for “immediate summary of assessment of damages,” the article explains.

© US Global

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits