SUMMARY

- Slowing growth and downside risks set the stage for two rate cuts this year.

- Trade restrictions are damaging, as is uncertainty over trade policy.

- The Fed will have to look past politics and focus on its mission.

It’s been a tough year for the Federal Reserve…and it’s only June! Berated in some corners for pushing up interest rates late last year, the Fed changed its tone in January and seemed set for a long, comfortable pause. Then came a barrage of criticism from the White House and an unexpected escalation of global trade tensions. The outlook has become murkier and riskier, leading the markets to cry out for easier monetary policy.

We think the Fed will be forced to acquiesce. Probably not at this month’s meeting; there hasn’t been enough time to send the proper signals to the markets. But lower rates are coming. Here is our take on the likely content of next week’s conversations.

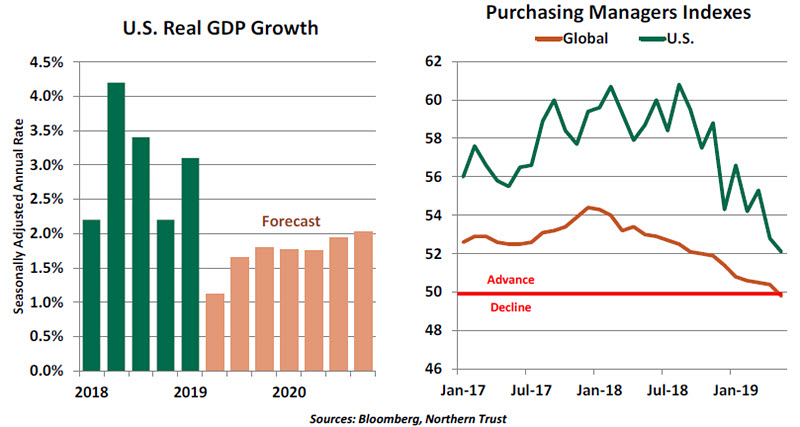

We are not forecasting a recession, but the odds of one are rising. Trade-sensitive sectors have been impaired, and targeted retaliation by China against U.S. companies and industries will further the damage. Policy uncertainty is hindering business investment. And as discussed below, the outlook for American consumers may not be as bright as it was a few months ago.

The weakness of the Phillips Curve relationship between unemployment and inflation has occupied the attention of economists for several years now. The first leg of that relationship, the one between unemployment and wages, still holds; wage growth has risen steadily over the past five years, but is nowhere near the heights achieved during the last expansion.

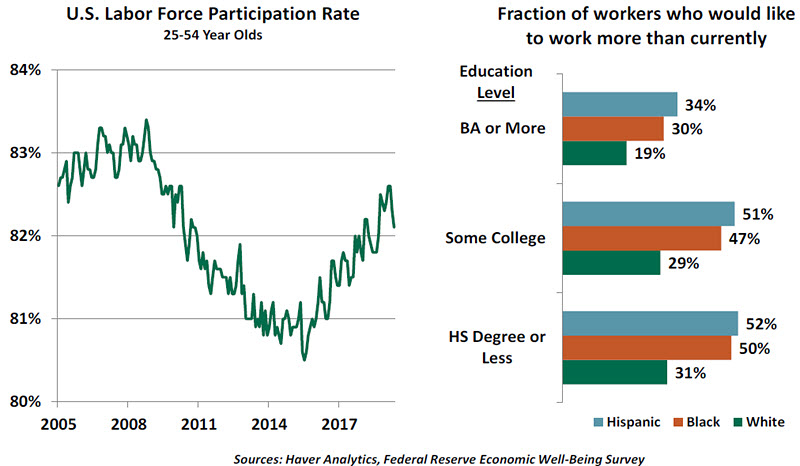

One potential explanation is that more slack remains in U.S. labor markets than meets the eye. Labor force participation for prime-aged workers is still below the peak of the past cycle. And the Federal Reserve’s recently released Report on the Economic Well-Being of U.S. Households challenges the notion that America is at full employment. A large fraction of workers want to work more than they are, and almost half of U.S. workers did not receive a raise last year.

To be sure, labor markets are tight in some areas. But in others, progress has been slower. Former Fed Chair Janet Yellen was a proponent of allowing the economy to run “hot” as a way to provide expanded opportunity; many on the current FOMC share that orientation.

One month does not a trend make, so it is premature to call a turning point on the U.S. job front. But persistent trade battles will put employment at risk in the months ahead.

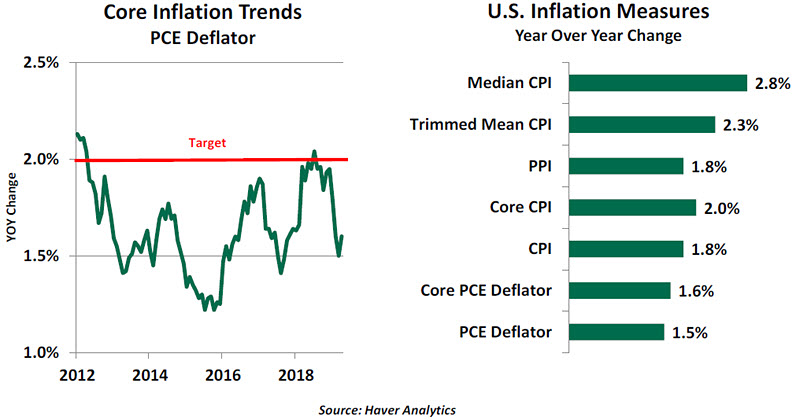

For several years now, the Fed’s models of inflation have suggested an impending return to 2%. But more educated consumers and more efficient corporations have held inflation down.

To be fair, many prominent inflation measures are close to or above 2%. Fed Chair Jerome Powell, among others, has suggested that transitory factors are skewing results for the core PCE deflator. But worry over low inflation has been spreading.

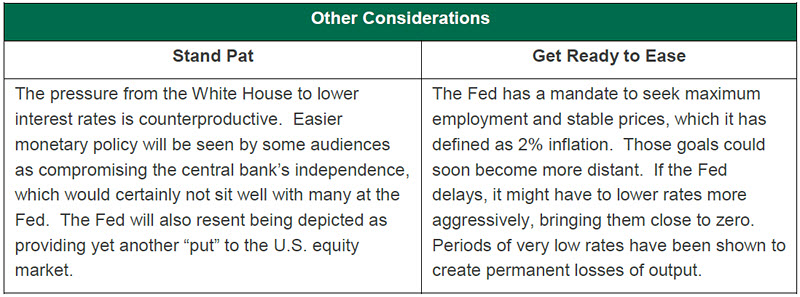

Prior to May’s breakdown of talks between the U.S. and China, the Fed was primarily focused on its inflation-targeting regime. A series of town halls have evaluated structural changes, and Fed officials have debated whether it would cut rates if disinflation persisted amid an otherwise healthy expansion. Our view is that any alterations to the Fed’s targeting system are some ways off, and are likely to be fairly flexible. And while very low inflation should prompt central bankers to act, U.S. inflation has not yet descended to a level that calls for an urgent response.

Heightened trade frictions change the picture. As we discussed in a recent note, tariffs increase prices of the products involved, but can become disinflationary if they dampen economic activity. We think we have arrived at that second phase, and inflation is likely to moderate further from here.

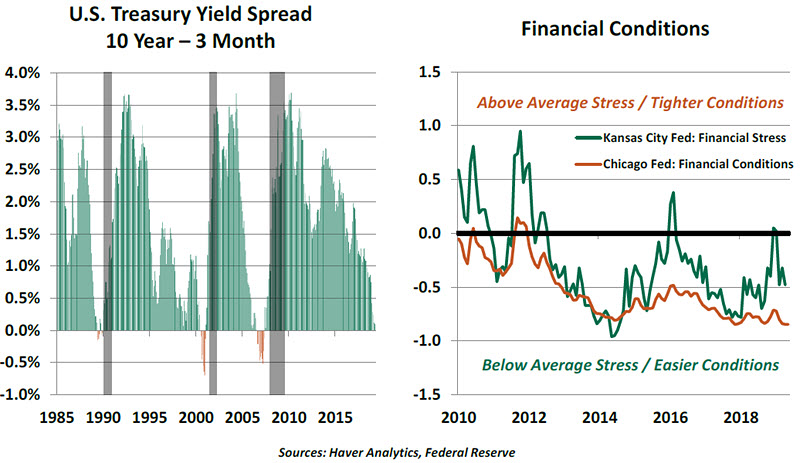

Interpreting the yield curve has become more complicated as central banks, commercial banks,

and foreign investors have become bigger owners of long-term Treasury securities. But it is nonetheless a signal that we ignore out our own peril. And while the Fed’s recent Financial Stability Report highlights a handful of concerns about asset prices, none could be considered proximate threats to the financial system. With risks to the business cycle rising, concern about market excesses should not be a primary concern.

Members of the Federal Reserve community will certainly want to avoid the appearance of bowing to escalating pressure from the White House. But Alan Greenspan reportedly advised Jay Powell to “put earmuffs on” and focus on the outlook. That is what we think the Fed will ultimately do.

Summary

A darkening outlook and increasing downside risks will eventually force the Fed to respond. Next week’s meeting will likely be too soon; the blackout period for FOMC participants commenced just after the disappointing job report came out. But the statements and forecasts that emerge next Wednesday afternoon will highlight increased uncertainty and a willingness to react.

The Fed will be evaluating incoming economic data carefully, and will watch the G-20 meeting at the end of June anxiously. Presidents Trump and Xi might certainly find enough common ground in Osaka to call a temporary halt to economic hostilities and restart negotiations. But recent provocations from both sides have gone so far that retreat is going to be difficult.

The Fed probably wishes it had accumulated more dry powder by raising interest rates a bit further as the expansion continued. And some FOMC members may be tempted to reserve capacity until absolutely necessary. But if modest rate reductions now can head off a worst-case outcome later, there is no compelling reason to wait.

Some analysts are calling for a more sudden or substantial program from the Fed. (The market currently expects three 25 basis point cuts during the balance of the year.) Given what we know today, two reductions should be enough to provide sufficient insurance and stability. Economists inside and outside of the Fed will be monitoring events through the summer and will update expectations if conditions warrant.

We’ll be offering immediate reflections on the FOMC meeting via social media. And we’ll undoubtedly have much more on the Fed in this space in the weeks ahead.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

More Factor-Based Investing Topics >