In Part 1, we discussed the problems with the “savings” side of the equation as it relates to building wealth. Part 2, covered the issues of counting on average, or compound, returns as it relates to future outcomes.

This final chapter is going to cover some concepts which will destroy the best laid financial plans if they are not accounted for properly.

Just recently, CNBC ran a story discussing the “Magic Number” needed to retire:

“For many people who adhere to the mission, there’s a savings target they want to hit, at which point they will have reached financial independence, as they define it. It’s called their FIRE number, and typically, it’s equal to 25 times a household’s annual spending, invested in low-cost, passive stock funds. Many wannabe-early retirees aim to save between $1 million and $2 million.”

This was the savings level we addressed in part one, which is erroneous because it is based on today’s income-replacement level and not the future inflation-adjusted replacement level, as it requires substantially higher savings levels. To wit:

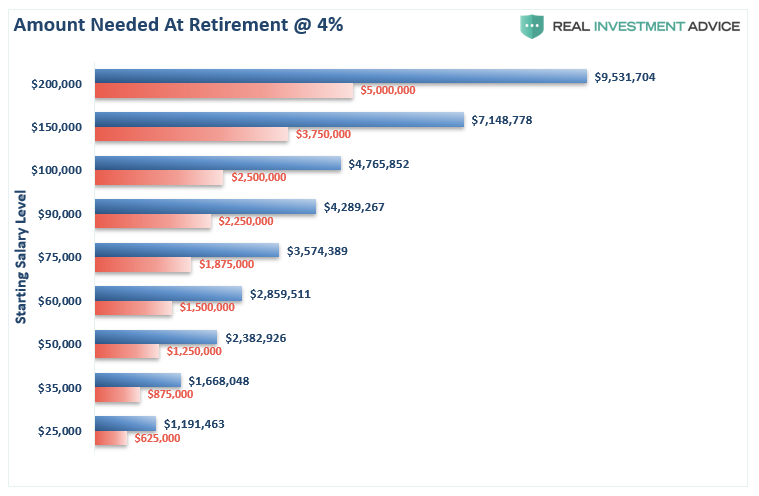

“The chart below takes the inflation-adjusted level of income for each bracket and calculates the asset level necessary to generate that income assuming a 4% withdrawal rate. This is compared to common recommendations of 25x current income.”

“If you need to fund a lifestyle of $100,000 or more today. You are going to need $5 million at retirement in 30-years.

Not accounting for the future cost of living is going to leave most individuals living in tiny houses and eating lots of rice and beans.”

The Cost Of Miscalculation

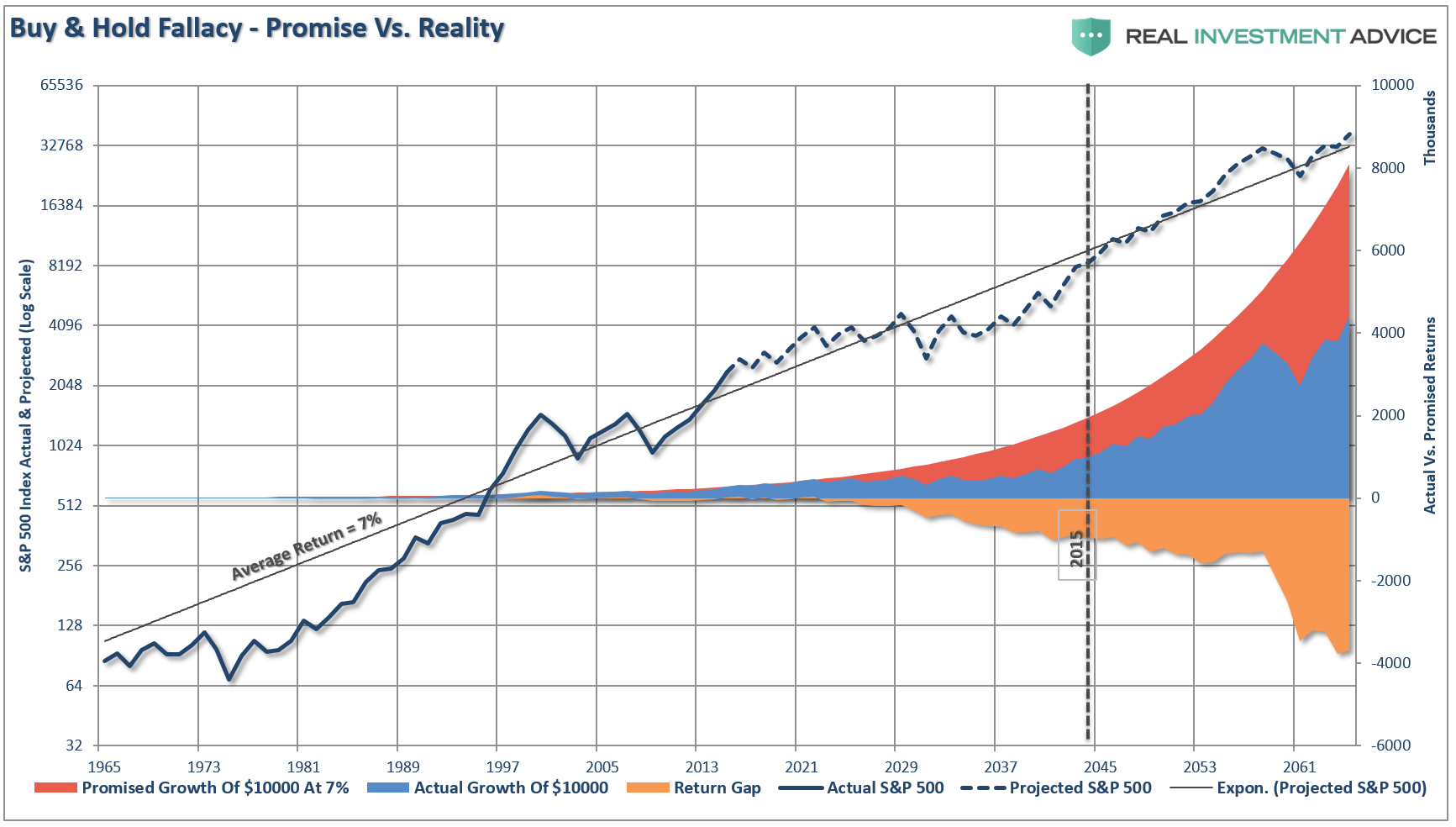

As noted in the CNBC article above, it is recommended that you invest your savings into low-cost index funds. The assumption, of course, is that these funds will average 8% annually. As discussed in Part One, markets don’t operate that way.

“When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over long-term time frames.”

During strongly trending bull markets, investors tend to forget that devastating events happen. Major events such as the “Crash of 1929,” “The Great Depression,” the “1974 Bear Market,” the “Crash of ’87”, the “Dot.com” bust, and the “Financial Crisis,” etc. often written off as “once in a generation” or “1-in-100-year events.” However, these financial shocks have come along much more often than suggested. Importantly, all of these events had a significant negative impact on an individual’s “plan for retirement.”

It doesn’t have to be a “financial crisis” which derails the best laid of financial plans either. An investment gone wrong, an unexpected illness, loss of job, etc. can all have devastating impacts to future retirement plans.

Then there is just “life,” which tends to screw up things without a tragedy occurring.

Making the correct assumptions in your planning is critical to your eventual success.

Your Personal Returns Will Be Less Than An “Index”

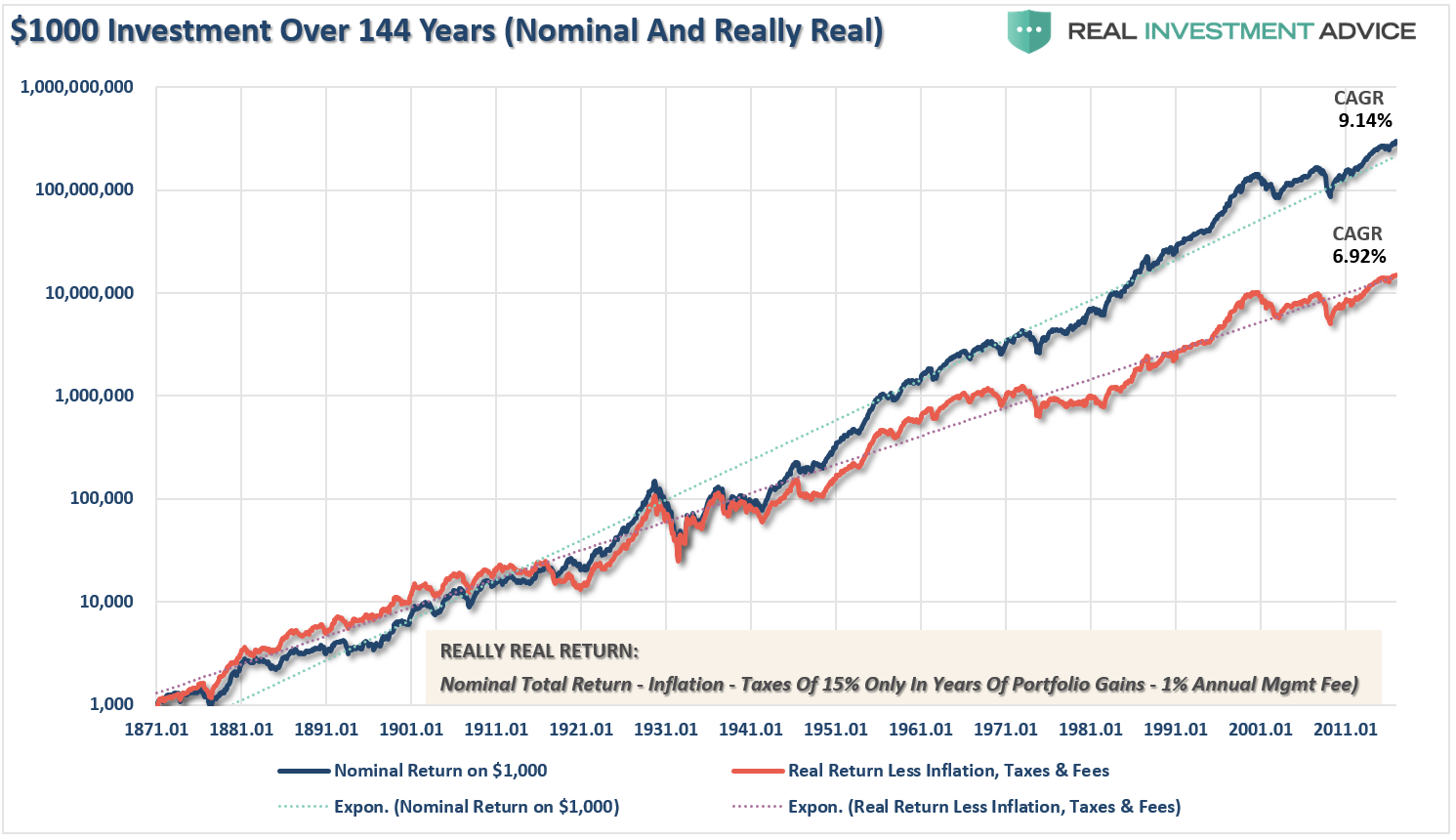

One of the biggest mistakes made is assuming markets will grow at a consistent rate over the given time frame to retirement. As noted, there is a massive difference between compounded returns and real returns as shown above. Furthermore, the shortfall is compounded further when you begin to add in the impact of fees, taxes, and inflation over the given time frame.

The chart below shows what happens to a $1000 investment from 1871 to present, including the effects of inflation, taxes, and fees. (Assumptions: I have used a 15% tax rate on years the portfolio advanced in value, CPI as the benchmark for inflation and a 1% annual expense ratio.)

There are other problems with chasing an “index” also:

- The index contains no cash

- An index has no life expectancy requirements – but you do.

- It doesn’t have to compensate for distributions to meet living requirements – but you do.

- It requires you to take on excess risk (potential for loss) in order to obtain equivalent performance – this is fine on the way up, but not on the way down.

- It has no taxes, costs or other expenses associated with it – but you do.

- It has the ability to substitute at no penalty – but you don’t.

-

It benefits from share buybacks (market capitaliziaton) – but you don’t.

As an individual you have very little in common with a “benchmark index.” Investing is not a “competition” and treating it as such has had disastrous consequences over time.

Financial Planning Gone Wrong

I know, you still don’t believe me. Let’s use CNBC’s example and then break it down.

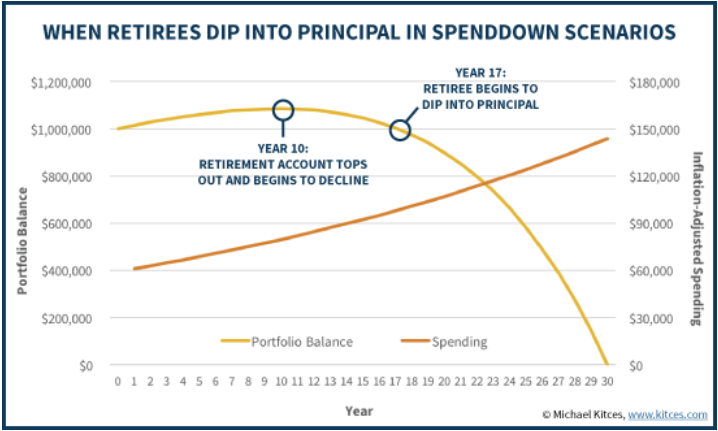

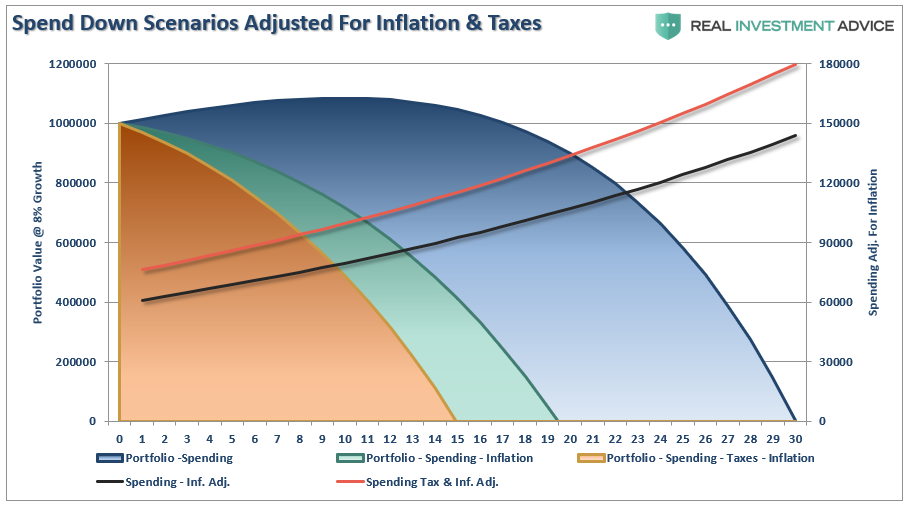

“For instance, imagine a retiree who has a $1,000,000 balanced portfolio, and wants to plan for a 30-year retirement, where inflation averages 3% and the balanced portfolio averages 8% in the long run. To make the money last for the entire time horizon, the retiree would start out by spending $61,000 initially, and then adjust each subsequent year for inflation, spending down the retirement account balance by the end of the 30th year.”

This assumption on expanding inflationary pressures later in retirement is correct, however, it doesn’t take into account the issue of taxation. So, let’s adjust the chart and include not only the impact of inflation-adjusted returns but also taxation. The chart below adjusts the 8% return structure for inflation at 3% and also adjusts the withdrawal rate up for taxation at 25%.

By adjusting the annualized rate of return for the impact of inflation and taxes, the life expectancy of a portfolio grows considerably shorter.

However, we must also consider the impact of variable rates of returns in retirement as well.

The Impact Of Variability

Over the last 120-years, the market has indeed averaged 8-10% annually. Unfortunately, you do NOT have 90, 100, or more years to invest. All that you have is the time between today and when you want to retire to reach your goals. If that stretch of time happens to include a 12-15 year period in which returns are flat, which happens with some regularity, the odds of achieving goals are massively diminished.

But what drives those 12-15 year periods of flat to little return? Valuations.

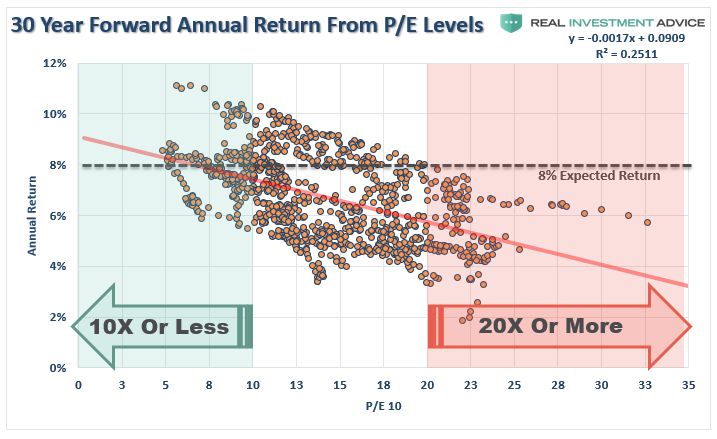

Understanding this, we can use valuations, such as CAPE, to form expectations around risk and return. The graph below shows the actual 30-year annualized returns that accompanied given levels of CAPE.

As evidenced by the graph, as valuations rise future rates of annualized returns fall. This should not be a surprise as simple logic states that if you overpay today for an asset, future returns must, and will, be lower.

Math also proves the same. Capital gains from markets are primarily a function of market capitalization, nominal economic growth plus the dividend yield. Using the Dr. John Hussman’s formula we can mathematically calculate returns over the next 10-year period as follows:

(1+nominal GDP growth)*(normal market cap to GDP ratio / actual market cap to GDP ratio)^(1/10)-1

Therefore, IF we assume that

- GDP maintains, 4% annualized growth indefinitely

- Which means recessions have been eliminated, AND

- Current market cap/GDP stays flat at 1.25, AND

- The current dividend yield remains at 2%:

We would get forward returns of:

(1.04)*(.8/1.25)^(1/30)-1+.02 = 4.5%

These are some “big” assumptions. If we assume inflation remains stagnant at 2%, as the Fed hopes, such would mean a real rate of return of just 2.5%. This is far less than the 8-10% rates of return currently being counted on in many of the financial plans I see regularly.

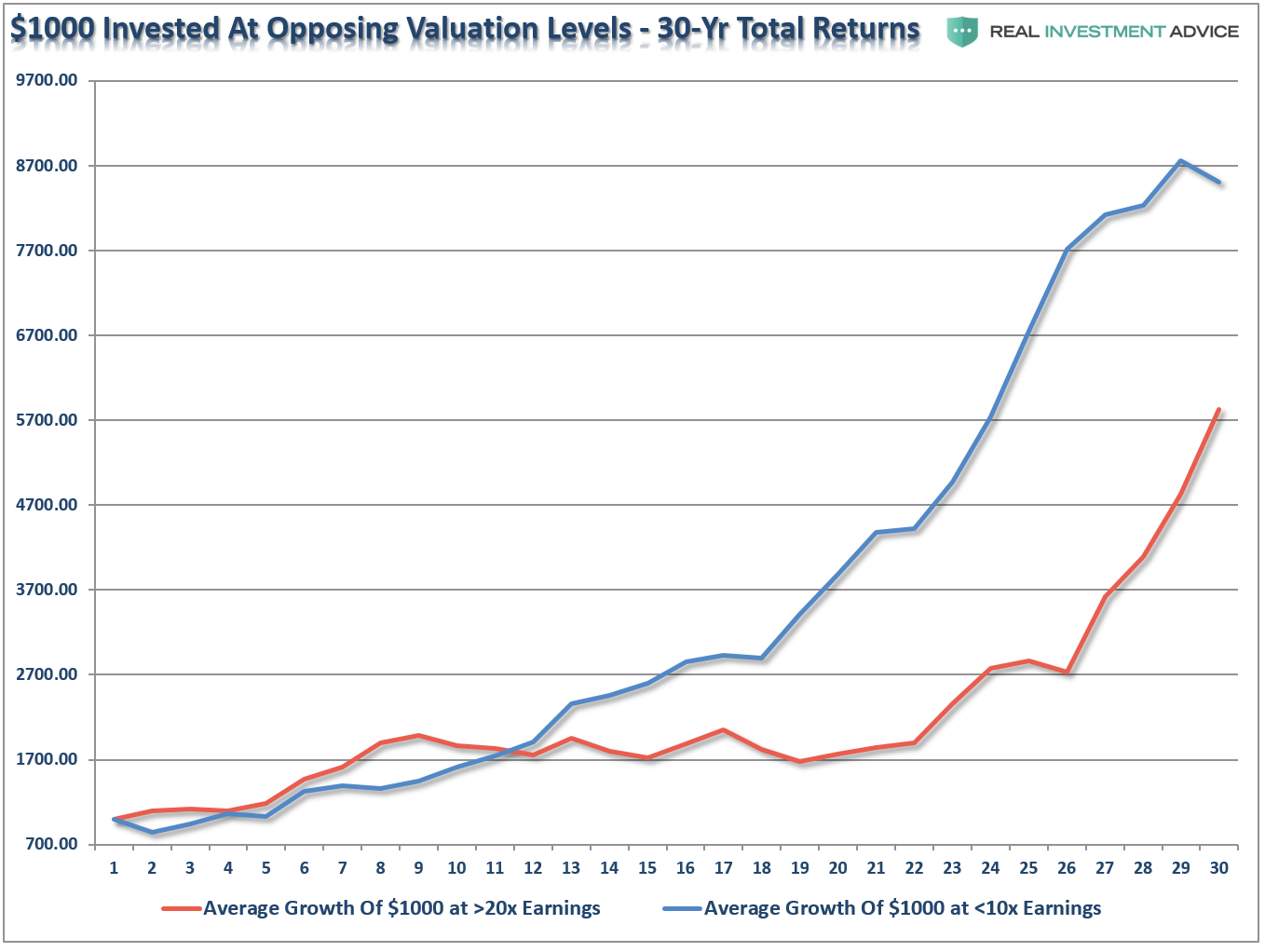

Let’s take this a step further. For the purpose of this article, we went back through history and pulled the 4-periods where trailing 10-year average valuations (Shiller’s CAPE) were either above 20x earnings or below 10x earnings. We then averaged those periods and ran a $1000 investment going forward for 30-years on a total-return, inflation-adjusted, basis.

Not surprisingly, the starting level of valuations has the greatest impact on your future results.

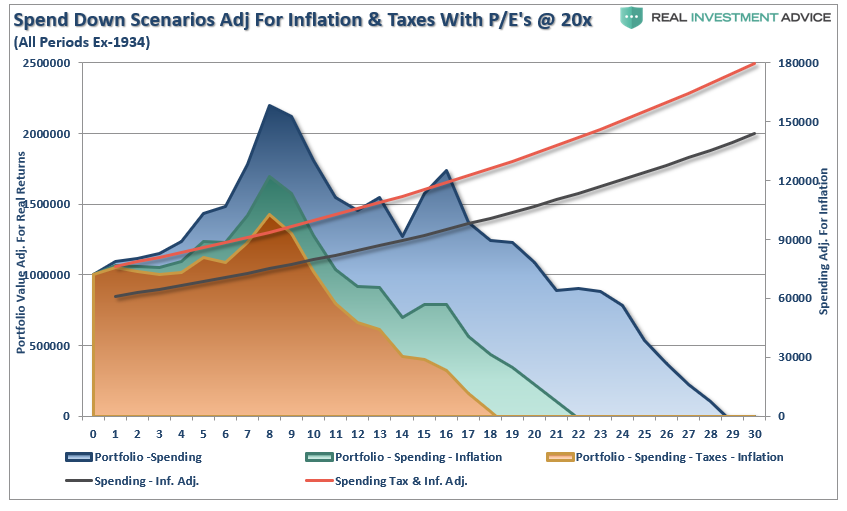

If we apply the math of valuations to our example, a much different, and far less favorable, financial outcome emerges – the retiree runs out of money not in year 30, but in year 18.

With current valuations elevated, and total returns in excess of 300% over the last decade, planning on using the stock market to make up for a savings short-fall may be misguided. This is the same trap that pension funds all across this country have fallen into and are now paying the price for.

What Your Financial Planning Should Consider

The analysis above reveals the important points individuals should consider in their financial planning process:

- Expectations for future returns and withdrawal rates should be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerates the principal bleed. Plans should be made during up years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last 8-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Investing for retirement, no matter what age you are, should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

- Save More And Spend Less: This is the only way to ensure you will be adequately prepared for retirement. It ain’t sexy, or fun, but it will absolutely work.

- You Will Be WRONG. The markets go through cycles, just like the economy. Despite hopes for a never-ending bull market, the reality is “what goes up will eventually come down.”

- RISK does NOT equal return. The further the markets rise, the bigger the correction will be. RISK = How much you will lose when you are wrong, and you will be wrong more often than you think.

- Don’t Be House Rich. A paid off house is great, but if you are going into retirement house rich and cash poor, you will be in trouble. You don’t pay off your house UNTIL your retirement savings are fully in place and secure.

- Have A Huge Wad. Going into retirement have a large cash cushion. You do not want to be forced to draw OUT of a pool of investments during years where the market is declining. This compounds the losses in the portfolio and destroys principal which cannot be replaced.

- Plan for the worst. You should want a happy and secure retirement – so plan for the worst. If you are banking solely on Social Security and pension plans, what would happen if the pension was cut? Corporate bankruptcies happen all the time and to companies that most never expected. By planning for the worst, anything other outcome means you are in great shape.

Most likely whatever retirement planning you have done is most likely overly optimistic.

Change your assumptions, ask questions, and plan for the worst.

The best thing about “planning for the worst” is that all other outcomes are a “win.”

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

© Real Investment Advice

© Real Investment Advice

More Fixed Income Topics >