The year to date has run hot and cold. Trade tensions, the growth outlook, employment and asset prices have all been volatile. The past month offered several reasons for cheer, but we have become conditioned to bracing ourselves for the next wave to come.

The agreement between Presidents Trump and Xi to resume trade negotiations, defer threatened tariffs and resume purchases of U.S. agricultural exports was a positive step. Trade escalations will hopefully stay out of the headlines for a while, but a lasting deal is far from complete. In the interim, U.S. companies still find themselves in limbo as they attempt to invest and manage their supply chains.

This does not provide the firmest ground for a constructive outlook on the economy. There is no recession in our forecast, which includes our first look at 2020. But downside risks still predominate.

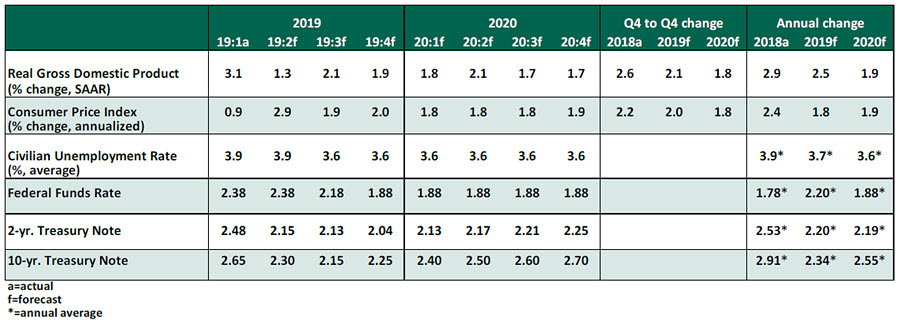

Key Economic Indicators

Influences on the Forecast

-

- In June, the U.S. economy added 224,000 jobs. The report ended concerns that the weak job creation observed in May was the start of a trend. The unemployment rate increased slightly to 3.7%, driven by a positive force: an increase in labor force participation. Wages continued their steady climb, growing by 3% year-over-year.

- Initial jobless claims are holding at a four-week moving average of around 220,000, a low level not seen in 50 years. The labor market is often an early indicator of economic trouble, and it is not yet giving cause for alarm.

- Inflation continues to fall short of targeted levels. The consumer price index (CPI) and producer price index (PPI) in May both grew by 1.8% year-over-year. The deflator on personal consumption expenditures (PCE) excluding food and energy has risen by just 1.6% during the past 12 months. We expect that the short-term price pressure from the higher tariff rate applied to Chinese goods in May, combined with easing by the Fed, will set the stage for higher inflation in the balance of the year.

- Interest rates have fallen and cannot get up. Even as equity markets have set record highs, inflows into U.S. Treasuries have kept yields low, continuing the 3 month-10 year inversion that began a month ago. As signs of a global slowdown become more apparent throughout Europe and Asia, the low risk and relatively high yields offered by Treasuries are maintaining strong global demand, keeping their prices high. We expect international markets to stabilize and risk assets to continue to appreciate, which should reduce demand for Treasuries and allow rates to normalize.

- Despite low rates, the housing market has remained sluggish. Housing starts in May declined to a pace of 1.26 million units at a seasonally adjusted annual rate, a level that reflects no growth year-over-year. The supply of homes for sale fell to a post-crisis low in the first quarter. House price indices continue to climb in many markets, with the S&P/Case-Shiller National Home Price Index increasing by 3.6% year-over-year in April. Strong employment, low rates and appreciating home values lead us to expect better from the housing sector.

- The manufacturing Purchasing Managers’ Index (PMI) fell to 51.7 in June, its lowest reading since 2016, though still a level narrowly indicating expansion. Falling PMIs have been a consistent story across the globe, reflecting slower industrial activity. While the U.S. industrial production index recovered to 2.1% growth year-over-year from a sluggish 0.9% in April, signs of sustained business investment have been slow to emerge.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

More ETF Topics >