SUMMARY

- Bumpy Road Ahead For The U.S. Auto Industry

- Germany’s Motor Is Sputtering

- Chinese Auto Sales Are Stuck in Reverse

Recent hot weather made me daydream of a once-familiar summer sight: the unlucky driver pulled over with steam pouring out of the car’s radiator. Happily, we don’t see scenes like that much anymore. Vehicle reliability has come a long way, even in my own lifetime. When I learned to drive just 20 years ago, checking fluids and changing a flat tire were essential lessons. Now, I can’t remember the last time I needed jumper cables.

Much like the products it produces, the American automotive market has entered a state of maturity and stability. Vehicles have never been safer or more efficient, and financing has allowed more buyers to obtain better vehicles. But changing market circumstances will put sustained pressure on the automotive sector, which may need jumper cables of its own in the years ahead.

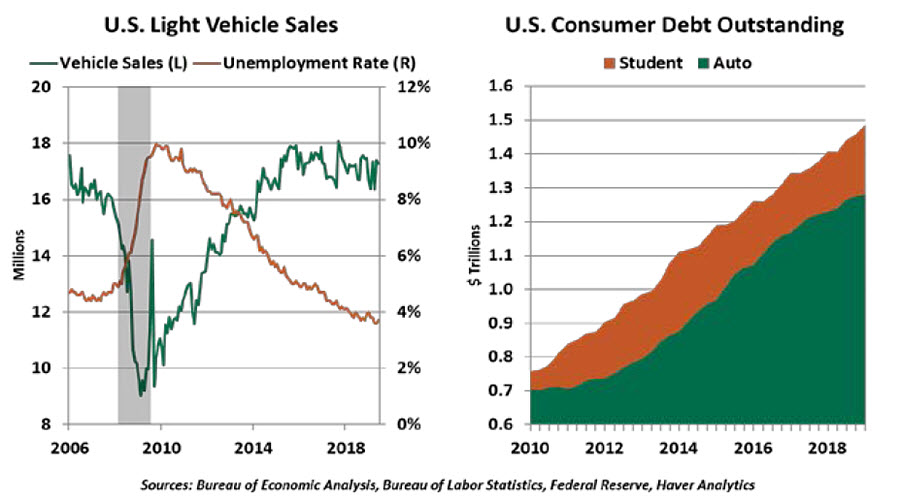

The macro economy has been as good as it gets for the automotive industry. Through 2010, U.S. unemployment was close to 10%, but it now stands at a 50-year low. More workers are re-entering the labor force. These people need vehicles to get to their jobs, and their jobs give them incomes to afford cars. Auto sales have consequently grown steadily during the current expansion.

Easier financing conditions have contributed to this performance. Automotive lending is an attractive market for banks and finance companies: All loans pledge a valuable asset as collateral, and in lean times, people tend to prioritize their car payments over other obligations. In the aftermath of the financial crisis, the delinquency rate on auto loans held lower than that of mortgages. Cars and homeownership may both be pieces of the American dream, but when the chips were down, we learned that Americans who possessed both assets would sooner keep their cars than their houses.

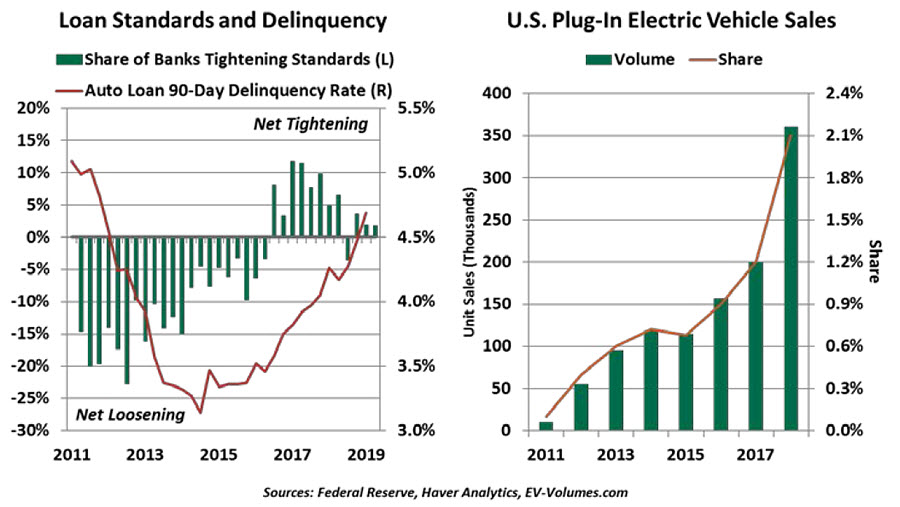

“Years of easy credit have caught up with auto lenders.”

Ample credit gave consumers access to loans and leases for the vehicles they wanted, but now, many are overextended. The loose standards of past years are manifesting as higher delinquency rates today, with the 90-day past due rate of 4.7% of balances in first quarter 2019 within sight of the crisis peak of 5.3%. Lenders are at risk of greater losses as vehicles are recovered with little equity. While interest rates remain relatively low, lenders are tightening standards and manufacturers are curtailing interest-free financing to draw buyers into dealerships.

Consumers are stretched by their other obligations, as well. The student debt burden cannot be ignored, with about 45 million Americans carrying student loans on their credit files. Meanwhile, rents and house prices continue to rise nationwide, crowding out car payments in consumers’ budgets. These factors have contributed to a flattening of demand for cars seen recently.

Automakers will also have to adapt to changing consumer preferences. Auto purchases have shifted away from cars and into light trucks, including sport-utility vehicles and pickups. At the time, low oil prices made these heavier vehicles more affordable. But higher gasoline prices and rising environmental consciousness have increased the popularity of electric vehicles (EVs). EVs produce no tailpipe emissions but are not just for environmentalists: they also incur low operating costs, and cover increasing distances on a single charge.

Meeting the growing demand for EVs will be a massive effort for carmakers, who will have to scrap a hundred years of experience perfecting internal combustion engines. They must now engineer new drivetrains, create marketing plans for these new vehicles, and train their dealers and mechanics to support them. Even when successful, these foundational changes are costly.

The greatest demand shift, however, will alter the industry fundamentally: the appeal of car ownership may be on the decline. Ride-sharing apps have turned transportation into an on-demand service at the fingertips of the majority of Americans. Getting by without a car, or with a single car in a multiple-driver household, has gotten easier.

Autonomous vehicles are not yet in commercial service, but if perfected, they would further weaken the case for private car ownership. And those who own cars now have options to rent out their vehicles on a short-term basis. These platforms each address an irrationality that had worked to carmakers’ benefit: Consumers spent heavily on an asset that would spend most of its life parked. These new platforms allow for better utilization of the nation’s auto fleet.

A shift in preferences toward urban living also works against carmakers. Owning a car is a burden in dense cities; parking is scarce or expensive, and traffic is perpetual. Those who do not need a car daily may find they are better served with ride-sharing and occasional rentals.

“For an increasing number of consumers, car ownership is no longer mandatory.”

Automakers are bracing for challenges on the supply side, as well. The uncertainty around global trade continues to cast fear on the industry. Repealing NAFTA or imposing tariffs would throw the industry into disarray. Automakers are leaders at creating international supply chains, integrating components sourced from wherever manufacturing is most cost-effective. Any changes to these complex supply chains will eat into margins. And protectionism could disrupt an industry in which the U.S. runs a trade surplus with China.

None of this is to say the auto industry will fade away. Not everyone will crowd into city living, and rideshare drivers will still need to buy cars. Manufacturers have committed to ambitious plans to retire their fossil fuel engines over the medium term. Today’s shoppers will find a vehicle assortment that has never been more reliable, more efficient, safer or cleaner. But tomorrow’s car buyers will be fewer in number and will expect a different ownership experience.

Those who drove older vehicles will recall the sinking feeling of a breakdown: An odd noise from under the hood, dashboard warning lights illuminating and the engine losing power. Carmakers see the warnings clearly and are doing all they can to retool.

Off The Autobahn

U.S. car makers aren’t the only ones bracing for a difficult road ahead. Their European counterparts are already reeling from challenges that came from several directions. The past year has been especially difficult for the German car industry. A main engine of the eurozone economy is struggling.

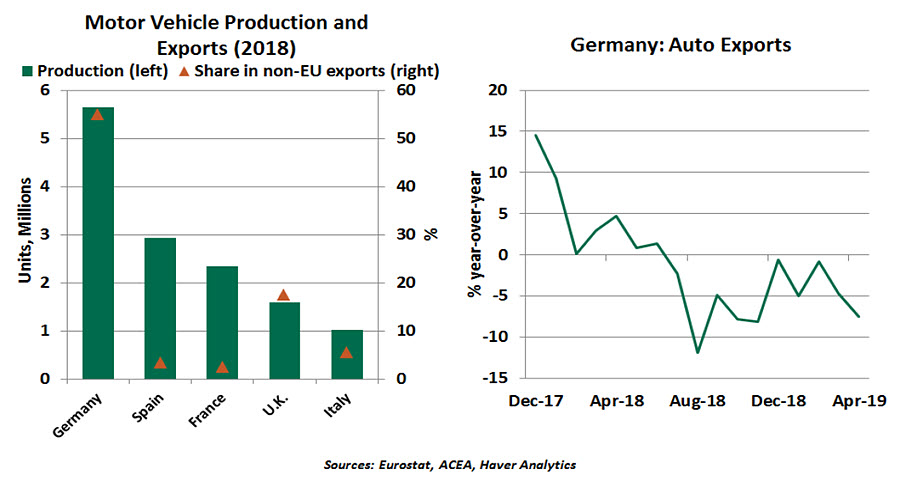

Germany is not only the second-largest export economy in the world, but also the top exporter of cars globally, with the vehicle industry employing more than 870,000 of its residents. Unfortunately, the German automotive sector has been contracting since July 2018. Within the European Union (EU), German car exports to the U.K. (its biggest EU market) fell by 9.9%, and exports to Italy are down by 7.8%.

Regional sales have been dented by an advancing economic slowdown that has hit Europe particularly hard. Looming risks of a no-deal Brexit, a slowing Chinese economy and the impact of U.S.-China trade tensions on European supply chains have weighed on business sentiment and industrial activity.

Europe is an important market for German carmakers, but Germany’s market is global. German output accounts for 55% of car exports from the EU to other countries, and 13% of Germany’s total exports outside of the EU. The U.S. and China are the top consumers of German vehicles; car exports to the U.S. declined by 5% in 2018, and as discussed in the following article, vehicle sales in China have slumped.

German automakers have a significant presence in the U.S. market, with four large car factories employing more than 100,000 Americans. According to the German Association of the Automotive Industry, German car manufacturers produced 750,000 vehicles at their American plants in 2018, with more than half exported to Europe and China. Around 95,000 German light vehicles were shipped from the U.S. to China last year, compared to 150,000 in 2017. So the malaise in sales of German brands has hit the United States, as well as Germany.

Adding insult to injury is the treat of U.S. tariffs against European auto makers. The tariffs would apply to vehicle components as well as completed vehicles. In the short run, this would challenge the competitiveness of German cars, but in the long run, it could prompt production to leave the United States (and potentially end up in Asia, closer to Chinese consumers).

According to the IFO Institute for Economic Research, a 25% tariff from the U.S. could reduce German car exports to the U.S. by 50%, directly reducing German real gross domestic product (GDP) growth by 0.14%. Oxford Economics forecasts a more severe loss of 0.3% of German GDP by 2021. Given the inter-linkages of auto manufacturers and their suppliers, the near-term impact of increased protectionism could be much bigger.

“New economic and ecological challenges are sending ripples through the German auto industry.”

Regulatory changes stemming from environmental concerns have also been difficult for German manufacturers. New emissions rules required a wholesale retooling that slowed production in the middle of last year. Other sector-specific challenges like electric mobility, autonomous driving and car sharing are only adding to the pressure. China recently decided to impose quotas on carmakers, requiring them to either sell a fraction of hybrid and all-electric vehicles, or face heavy fines.

German automakers are responding by placing bets on new products (developing electric and self-driving cars), allocating huge investments in new technology and even forming new forms of cooperation with rivals. This is a step in the right direction but may not be enough to return to the fast lane.

Backing Up

Americans first saw televised images of China during Richard Nixon’s visit to the country in 1972. At that time, the masses moved about largely by bicycle, in armadas that filled the broadest avenues in Beijing.

As a recent visitor to Beijing, I can tell you that transportation has changed a lot since then. The bicycles are still there, but they compete for pavement with armadas of motor vehicles. Traffic rules are somewhat fluid, making transit an exciting proposition for all modes of transportation.

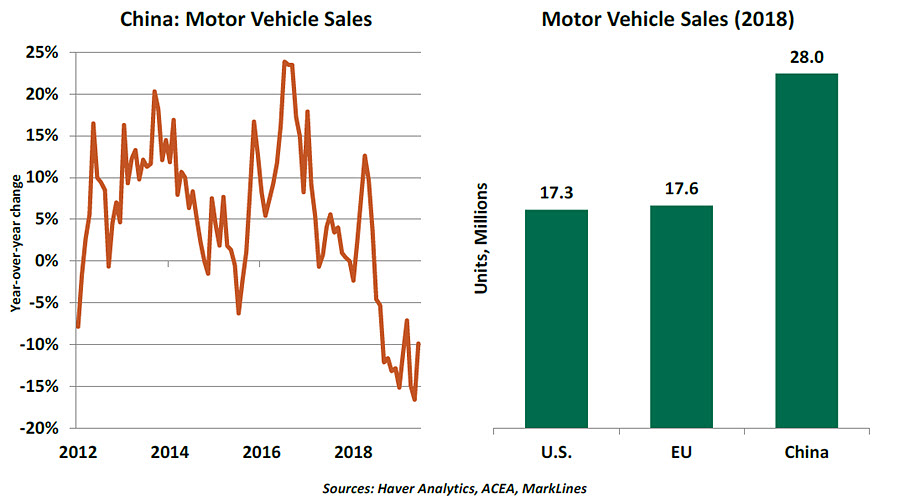

Automobile ownership is a milestone for both motorists and nations. It is a sign of economic progress, reflecting a growing middle class. For China, increasing car sales have signaled its arrival as a middle income country in which domestic consumption is reducing reliance on exports for economic growth. Chinese vehicle purchases surpassed those in the United States in 2010 and have more than doubled in the last decade.

“Flagging car sales in China are hurting producers all over the world.”

But car buying in China has stalled, with sales down sharply over the past twelve months. There are a series of reasons for this: tighter terms for vehicle financing, the increased popularity of ride-sharing and a heightened environmental sensibility. But a more tenuous economic outlook is also at play. No matter the country, households don’t extend themselves when the future is uncertain.

While China has ramped up efforts to produce motor vehicles, about 60% of the cars purchased by Chinese drivers come from overseas. Soft Chinese demand is hitting Japanese, Korean, American and European automakers hard. In this manner, trade action initiated in the West is harming some of the producers it is ostensibly designed to help. This is one of many unintended side effects of the ongoing trade conflict.

If there is a silver lining to all of this, the decline of vehicle sales means I might be able to cross the street more safely during my next visit to Beijing.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust