The Etrade commercial aired during Super Bowl XLI in 2007. The following year, the financial crisis set in, markets plunged, and investors lost 50%, or more, of their wealth.

However, this wasn’t the first time it happened.

The same thing happened in late 1999. This commercial was aired 2-months shy of the beginning of the “Dot.com” bust as investors once again believed “investing was as easy as 1-2-3.”

Why this trip down memory lane? (Other than the fact the commercials are hilarious to watch.)

Because this is typical of the mindset seen at the end of extremely long “cyclical” bull market cycles.

Investing is simple. Just throw you money in the market and it goes up. Its so easy a “baby can do it.”

Here is something else you see at the end of bull market cycles:

How did they make this happen? Shen and Leung, who was also a computer engineer, are part of the FIRE movement — which stands for Financial Independence, Retire Early — where the goal is to save a lot so you can retire early. The couple retired at 31 with roughly $1 million in the bank. They’re currently withdrawing 3.5% a year from that nest egg, and say they can easily travel the world on that money — as they’ve got lots of practice being frugal.”

First, I want to give the couple a “fanatical thumbs up” for saving $1 million by their 30’s. That is an amazing feat which deserves respect and acknowledgment.

Secondly, they are very budget conscious and willing to sacrifice the luxuries most people long for to live their dream.

Another “thumbs up.”

However, the rise of the “F.I.R.E.” movement is symptomatic of a late stage bull market advance. More importantly, we can also predict how things will turn out for Shen and Leung.

For this discussion I want to use the data provided by Shen and Leung to build our examples.

Invested asset value: $1 million

Annualized withdrawal rate: 3.5%

Annualized return rate: 6% (Not specified but a reasonable estimate)

Living needs: $35,000 annually.

Life expectency: 85-years of age.

With these assumptions in place we can begin to do some forecasting about how things eventually turn out. However, we also have to assume:

The couple never has children

Never requires serious medical care (hopefully)

Never considers buying a house

Has no major life events, etc.

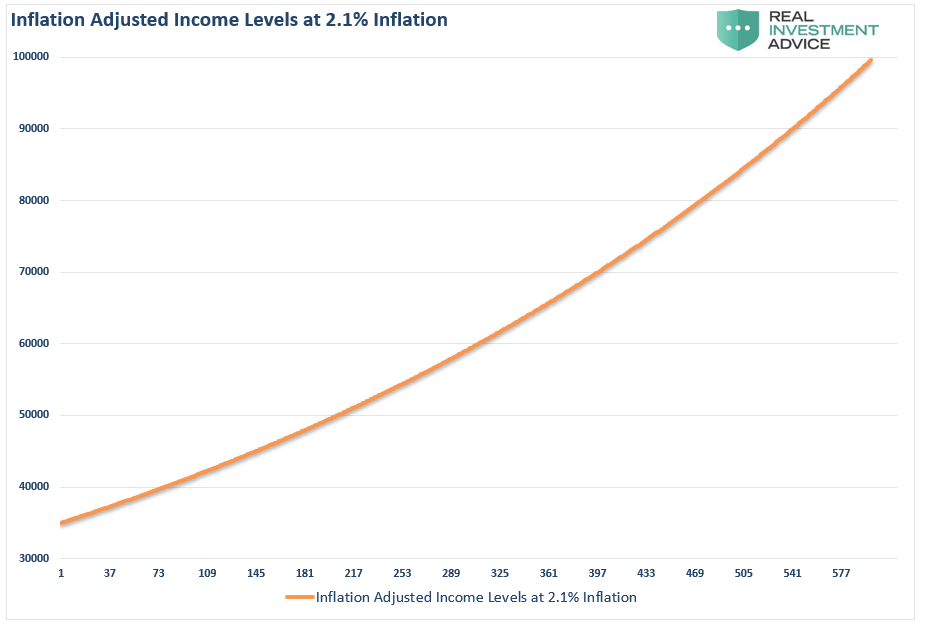

First, we need to start with the cost of living. As I showed recently in Part 1 of “Everything You’ve Been Told About Savings & Investing Is Wrong” is that the cost of living rises over time due to inflation. However, for most the increase in living costs rises dramatically more as needs for housing, children, education, travel, insurance, and health care occur through stages of life.

For this exercise, we will assume our example couple never changes their lifestyle so only inflation is a factor. We will use the historical average of 2.1% and project it out for 50-years.

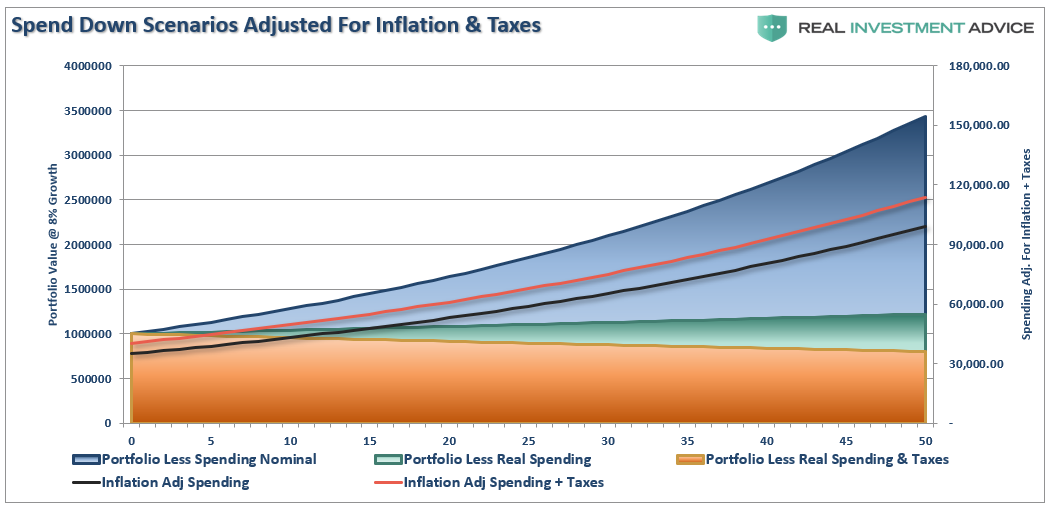

Understanding this, we can now take their $1 million, compound it at 6% annually (the preferred mainstream method), and deduct 3.5% annually adjusted for inflation over their 50-year time horizon.

We need to assume that since our couple is in their 30’s, the investable assets are in taxable accounts. Also, if this is the case, and they are not touching the principal, then we need to adjust the annual withdrawals for capital gains tax. The bottom two area charts adjust for 2.1% annual inflation and inflation plus a 15% tax on withdrawals.(Tax is paid on the gains taken to fund the withdrawal and the dividends paid in on an annual basis)

Not surprisingly, if our couple can indeed live on $35,000 a year, even when adjusting for inflation and taxation, a $1 million portfolio growing at 6% annually can indeed support them for their entire lifespan.

Reality Is Different

In Part 3 of our recent series on “saving and investing,”we laid out the issue, and importance, of variable rates of return. To wit:

“When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what happened to their money is substantial over long-term time frames.”

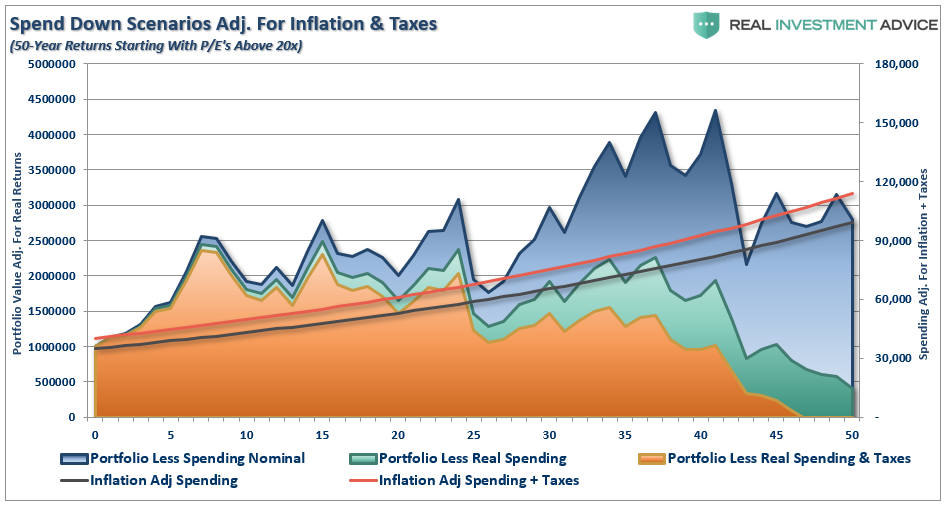

The chart below is exactly the same as above, however, this time we have used the average annual 50-year returns from previous periods in history where starting valuations were greater than 20x earnings as they are today. (High starting valuations beget lower future returns historically speaking.)

Over a 50-years, our couple will get the benefit of complete valuation and market cycles. In this case, since they are starting with high valuations at the outset, the first 30-years contains a long-period of lower returns, but that last 20-years receives the benefit of higher returns due to valuation reversion.

Due to market volatility and periods of negative growth, the original $1 million portfolio only grows to $3 million when including nominal spending. However, when accounting for volatility, inflation, and taxes, the survival rate of the portfolio diminishes sharply due to two reasons:

Down years reduce the growth rate of the portfolio over the given time frame.

Withdrawals in down years exacerbate the decline in the portfolio. (i.e. Portfolio declines by $65,000 plus the $35,000 annual withdrawal increases the 6.5% decline to 10%.)

Obviously, not accounting for volatility when planning to retire early can have severe future consequences. In this case they will run out of money in year 47.

The Big Bad Bear

As I said at the beginning of this missive, the “F.I.R.E.” movement is the result of a decade-long bull market cycle.

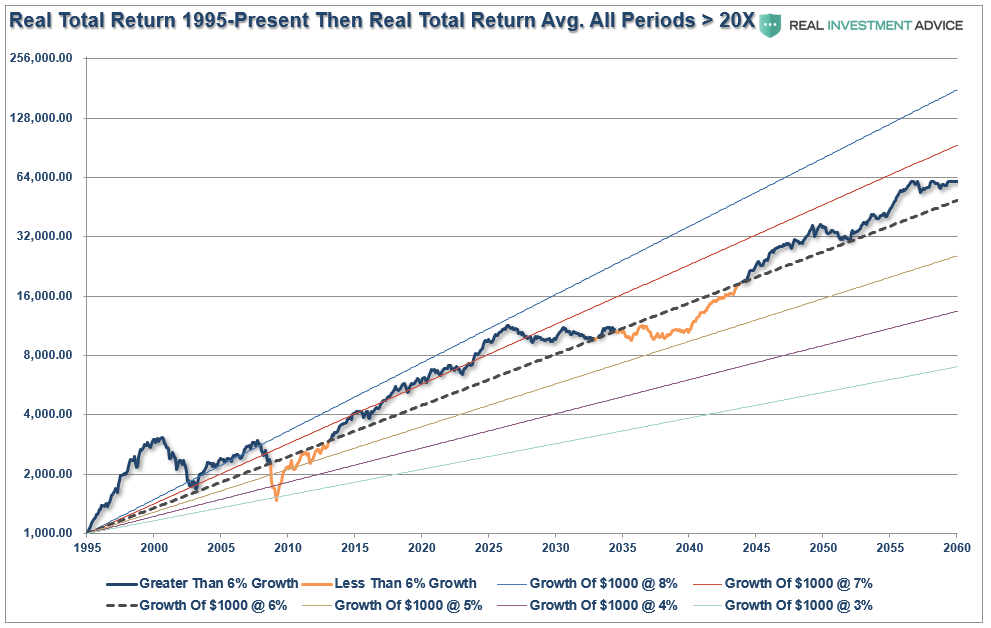

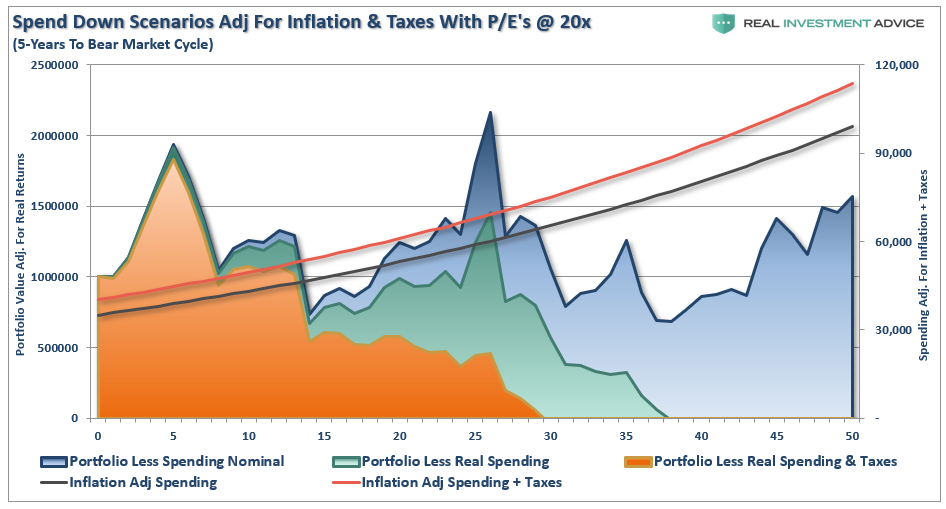

Most likely, our young couple will be met with a “bear market” sooner, rather than later, in their early retirement. If we use the return model from our recent article on “investors and pension funds,” we see a rather dramatic shift in life-expectancy of the portfolio.

“The chart below is the S&P 500 TOTAL REAL return from 1995 to present. I have projected an average return of every period in history where the market peaked following P/E’s exceeding 20x earnings. This provides for variable rates of market returns with cycling bull and bear markets out to 2060. I have also projected ‘average’ returns from 3% to 8% from 1995 to 2060. (The average real total return for the entire period is 6.56% which is likely higher than what current valuation and demographic trends suggest it should be.)”

The benefit of this model is that it shows the impact to portfolio returns when bear markets are “front-loaded,” as will likely be the case for most the “F.I.R.E.” followers.(Note, in the return model above the “bear market” is 5-years into the future)

The reason for the dramatic short-fall is that a major, “rip your face off,” bear market will cut asset values by 50% very early on. All of a sudden, the annual withdrawal rate of 3.5% becomes 7%, which outpaces the ability of the portfolio to grow fast enough to catch up with the withdrawal rate and the loss of principal. In this more realistic example, our couple will run out of money in 30 years.

This is the exact problem “pension funds” face currently.

The Other Problems From “Playing With F.I.R.E.”

While we have mainly addressed the issues surrounding assumptions being used by the ‘F.I.R.E.” movement in having enough assets to retire, there are some other important issues which should be considered.

Loss of your skill set. In retirement it is probable your skill set erodes and becomes outdated over time. New technologies, trends, innovations, etc. are running at a faster pace than ever.

Becoming unemployable. One of the things seen following the financial crisis was employers preferring to hire individuals who were already employed rather than hiring those out of work. The reasoning was that if you were good enough to keep your job during the recession, you obviously have a valuable skill set. Once you are out of the “labor force” for a while, it becomes more difficult to regain employment as employers tend to prefer those with a very steady work history, a growing career, and relevant skill sets.

Life. Besides simply running out of money sooner than you planned because of a bear market, a rising cost of living more than you counted on, or higher taxes (all of which are very likely in the near future) there is also just “life.” It doesn’t matter how carefully you plan; “S*** Happens!” More importantly, it always happens when you least expect it and at the worst possible time. These things cost money and impact our best laid spending and saving plans. The problem with “retiring early,” is that it leaves plenty of time for things to go wrong.

Unplanned Accident/Medical Problem.Young people suffer from an “invincibility syndrome.” They tend to not carry insurance, due to the cost, because they “never get sick.” While we certainly hope it never happens, a major accident or health issue can extract tens to hundreds of thousands of dollars of capital critically impairing retirement plans.

Too Old To Do Anything About It. The biggest problem for “F.I.R.E.” practitioners is that running out of money late in life leaves VERY few options for the rest of your retirement years. If our math above is even close to correct, which history suggests it is, then our young couple will be faced with going back to work in the 70’s. That is not exactly the retirement most are hoping for.

As I stated in our previous series, retiring early is far more expensive than most realize. Furthermore, not accounting for variable rates of returns, lower forward returns due to high valuations, and not adjusting for inflation and taxes will leave most far short of their goals.

While it sounds like I am bashing the “F.I.R.E. Movement,” I am not. I am for ANY program or system that gets young people to save more, stay out of debt, and invest cautiously. The movement is a good thing and it should be embraced.

But, it is also a symptom of a decade-long period of making “easy money” in the financial markets.

These periods ALWAYS end badly and the next “bear market” will quickly “extinguish the F.I.R.E.” as losses mount and dreams have to be put on hold.

It will happen. It always appears easiest at the top.

And, given one of E*Trade’s latest commercials, the next bear market may be coming sooner than we expect.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube