European equity markets have been caught in the middle of opposing forces, mainly growing tensions around global trade and increasingly dovish central banks. This has pushed European government bond yields to fresh lows and caused bond-sensitive sectors to climb higher, further stretching valuations. In this environment, it is becoming increasingly important for investors to be discerning, to focus on fundamentals and not short-term macro drivers, particularly as sentiment is vulnerable to rapid shifts.

The yield on 10-year German government bonds moved into negative territory during the second quarter for the first time since 2016, adding to the relative appeal of equities. Indeed, equities have outperformed all other key asset classes so far this year, despite softer-than-expected global economic data and concerns over US-China trade relations and its spillover effects. Political progress between the two economic powerhouses has been far from linear and it is difficult to anticipate how developments will continue to unfold over the coming months and what their impact might be.

Concerns that the trade spat between the United States and China would have a knock-on effect to the European economy grew, reflected by a softening in forward-looking indicators such as consumer confidence and business surveys focused on the outlook for the business climate, employment, and inventory levels. The outlook for the autos sector also continued to be clouded by the US-China dispute. Sales in China dropped for the first time since 1990 as consumers held back on purchases, creating expected ripple effects to European manufacturers alongside the ongoing threat of an import tax being applied by the United States on cars shipped from Europe. For now, however, European auto sales have held up, supported by a recent recovery in Germany, which helped to counteract the weakness in the United Kingdom created by Brexit uncertainty.

With UK Prime Minister Theresa May resigning as Conservative party leader, a conclusion to the Brexit negotiations seems unlikely for some time. May’s resignation has set in motion a leadership race that potentially opens the way for a more Eurosceptic successor who is prepared to take a tougher negotiating stance with the European Union (EU) and, as such, the odds of a no-deal Brexit has risen. Tensions were also evident between the European Commission and Italy during the quarter. While both sides edged towards an agreement over Italy’s 2019 fiscal budget figures, projections for 2020 did not go far enough to address the country’s structural budget deficit. This could result in the euro zone’s third-largest economy being subject to a fine of up to €3.5 billion as part of an official infringement procedure, which places the country under EU scrutiny for years. This could continue to feed into anti-EU sentiment at the national level although, for now, this threat appears to be relatively contained as populist and Eurosceptic parties gained fewer seats than expected at the European Parliament elections in May. Furthermore, political tensions in France have eased materially since the start of the year when the "gilets jaunes”, or yellow vests, protests were at their height, removing a significant overhang.

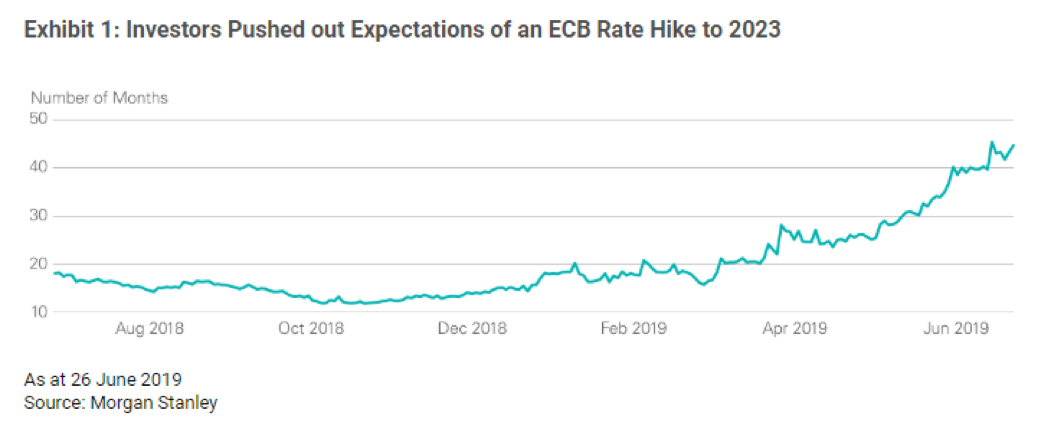

The European Central Bank (ECB) noted that it saw the potential for lingering softness in euro zone economic growth over the short term because of geopolitical tensions and ongoing trade disputes that have weighed on the European manufacturing sector and exports. However, the ECB assured it had the policy tools available to stimulate growth if the economic situation deteriorated over the coming months, either by cutting interest rates again or by engaging in further asset purchases. The ECB said it did not anticipate its first post-crisis rate hike until mid-2020. However, market participants are not expecting a rate hike until much later, at least not until March 2023 (see Exhibit).

The preceding is an excerpt from our Outlook on Europe. Read the full paper.

Important Information

Certain information included herein is derived by Lazard in part from an MSCI index or indices (the "Index Data”). However, MSCI has not reviewed this product or report, and does not endorse or express any opinion regarding this product or report or any analysis or other information contained herein or the author or source of any such information or analysis. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any Index Data or data derived therefrom.

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

Information and opinions presented have been obtained or derived from sources believed by Lazard to be reliable. Lazard makes no representation as to their accuracy or completeness. Any views expressed herein are subject to change. There is no guarantee that any projection, forecast, or opinion in this material will be realised.

This document is provided by Lazard Asset Management LLC or its affiliates ("Lazard”) for informational purposes only. Nothing herein constitutes investment advice or a recommendation relating to any security, commodity, derivative, investment management service, or investment product. Investments in securities, derivatives, and commodities involve risk, will fluctuate in price, and may result in losses. Certain assets held in Lazard’s investment portfolios, in particular alternative investment portfolios, can involve high degrees of risk and volatility when compared to other assets. Similarly, certain assets held in Lazard’s investment portfolios may trade in less liquid or efficient markets, which can affect investment performance. Past performance does not guarantee future results.

This content represents the views of the author(s), and its conclusions may vary from those held elsewhere within Lazard Asset Management. Lazard is committed to giving our investment professionals the autonomy to develop their own investment views, which are informed by a robust exchange of ideas throughout the firm.

This document reflects the views of Lazard Asset Management LLC or its affiliates ("Lazard”) based upon information believed to be reliable as of the publication date. There is no guarantee that any forecast or opinion will be realized. This document is provided by Lazard Asset Management LLC or its affiliates ("Lazard”) for informational purposes only. Nothing herein constitutes investment advice or a recommendation relating to any security, commodity, derivative, investment management service, or investment product. Investments in securities, derivatives, and commodities involve risk, will fluctuate in price, and may result in losses. Certain assets held in Lazard’s investment portfolios, in particular alternative investment portfolios, can involve high degrees of risk and volatility when compared to other assets. Similarly, certain assets held in Lazard’s investment portfolios may trade in less liquid or efficient markets, which can affect investment performance. Past performance does not guarantee future results. The views expressed herein are subject to change, and may differ from the views of other Lazard investment professionals.

This document is only intended for persons resident in jurisdictions where its distribution or availability is consistent with local laws or regulations. Please visit www.lazardassetmanagement.com/global-disclosure for the specific Lazard entities that have issued this document and the scope of their authorized activities.