SUMMARY

- Reflections from Budapest

Hungary, perhaps more than most nations, is no stranger to regime change.

The settled history of the region dates to Roman times. A number of tribes inhabited the area during the first centuries after Christ; the Magyars arrived shortly before the end of the first millennium. The Magyars were overrun by the Mongols in the 1200s, and the Ottomans arrived in the 1500s. The Habsburgs took over from the Ottomans, ultimately founding the Austro-Hungarian Empire. The Empire dissolved after the First World War, and its territory was partitioned.

The Second World War began a long, challenging period for Hungary. First the Nazis and then the communists installed their versions of totalitarian rule, creating terribly unfortunate outcomes for Hungary’s people and its economy. It was scant compensation, but Hungary was allowed to begin experimenting with capitalism a bit earlier than other Eastern European states, chartering what was called “Goulash Communism” after Soviet tanks crushed the 1956 revolution.

As a result, Hungary was well-positioned to take advantage of the fall of the Berlin Wall. The Third Republic was established in 1989, and Hungary became one of the most dynamic markets in Europe. The long series of regime changes has ultimately resulted in an eclectic and resilient culture that attracts visitors and capital alike.

The term “regime change” unifies the range of topics that our group of economists explored together. On many fronts, dramatic breaks from past patterns are challenging our models and our sensibilities. As Hungary’s history shows us, our success at collectively acclimating to these changing times will determine our prosperity.

The group’s consensus outlook was the first sign of change. Since last year’s survey, growth prospects have been downgraded and recession probabilities upgraded. Policy postures seen last year as too easy are now viewed as about right. Our current collective concerns center on nationalism and protectionism, the populist movement’s economic manifesto. Just as countries are becoming more aggressive, international authorities are losing traction. A particularly troubling development is the influence of the World Trade Organization declining just as its caseload is rising.

The populist agenda has undermined the roles of domestic and international institutions around the developed world. This was a common refrain during our review of the major economies.

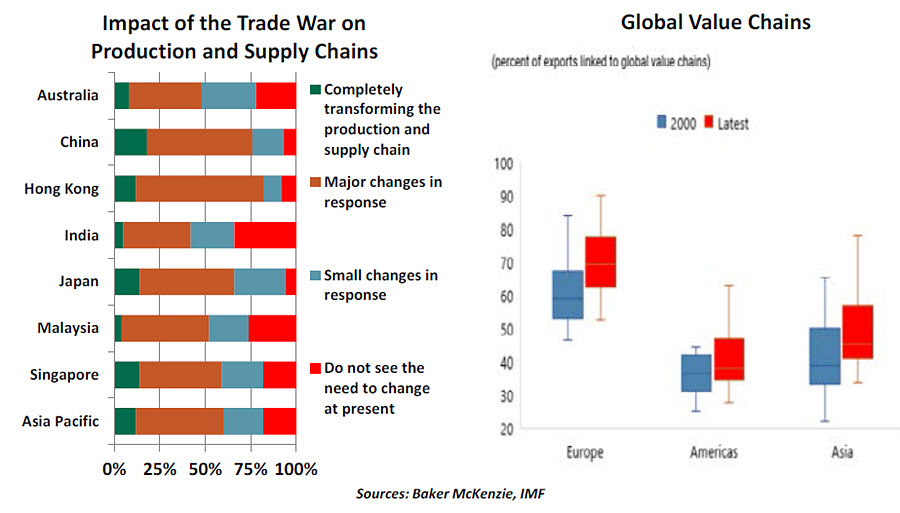

“Carefully-constructed global supply chains are fracturing.”

- In the United States, we have witnessed the decline of fiscal discipline and the advance of attacks on monetary discipline. The inward turn of politics has led to trade actions that continue to move abruptly: both forward and backward, and from side to side. The resulting uncertainty has hindered confidence in the U.S. economy and forms the core of the “external factors” weighing down the outlooks for a series of other countries.

- Gravity has already begun to assert itself on the economies of China and Europe. Official Chinese results are misleadingly smooth, but there is considerable churn beneath the surface. The battle over trade is disrupting the global value chains that China has profited from so handsomely during the last two decades. Re-engineering these systems is an extensive and expensive process. Once gone, the chains don’t look back.

- The eurozone has proven exceptionally sensitive to the contraction in trade, and to the uncertainty surrounding political regimes within and across countries in the European Union. A fractured Europe will lose competitive traction with the rest of the world.

- As Brexit preparations enter their fourth year, the same could be said of the United Kingdom. While politics on the both sides of the Channel flirt with dysfunction, the frighteningly short timeline left for negotiation cannot possibly suffice. The best case outcome may be limbo; the worst, a disorderly divorce.

- It is clear that the battle of the elephants is trampling others in the jungle. From Southeast Asia all the way down to Australia, Pacific Rim countries find themselves caught in the middle of the trade crossfire. Some will prosper from the migration of supply chains, but the case of Vietnam illustrates the risk that the United States will turn its ire toward those who benefit.

- Demographics are playing a significant role in the finances and politics of Japan, just as they will soon do for other countries. Getting old can be painful, individually and collectively. The implications of collective aging for potential growth, asset returns and a range of economic policies are substantial.

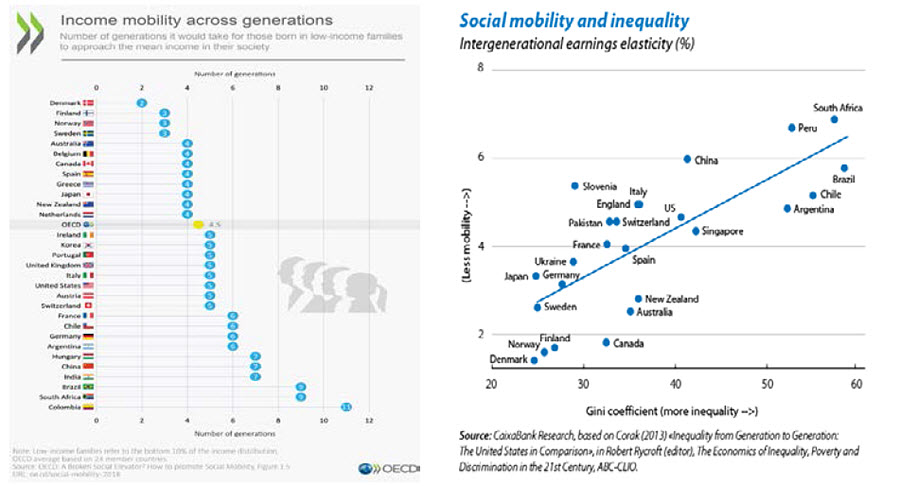

Breaking the cycle of populism will require addressing the roots of discontent. Increasing economic mobility and reducing income inequality will require retraining and other forms of transitional support.

Environmental change is not just a figurative term when applied to the economy. The social and economic damage that could be wrought by climate change in the years ahead is frightening. To be fair, there is still debate over the extent, or even the existence of, a climate problem. But many smart people have concluded that climate change poses a huge risk to humankind, and central banks are making an issue of it. It is therefore a topic that financial companies cannot ignore.

“Populism won’t recede until its root causes are addressed.”

In other regions, regime change is occurring in its literal form. Government instability is both a result and a cause of economic underperformance. New leadership is starting promisingly in some places, but new optimism can quickly give way to old realities. A conference delegate from Latin America suggested his continent has endured a lost decade; while new leaders have arrived in several countries, endemic problems have overtaken them. Corruption, nature and religion continue to complicate matters in the Middle East and Africa. At the conclusion of our review of emerging markets, I circled Argentina and Turkey as two countries of particular concern in the year ahead.

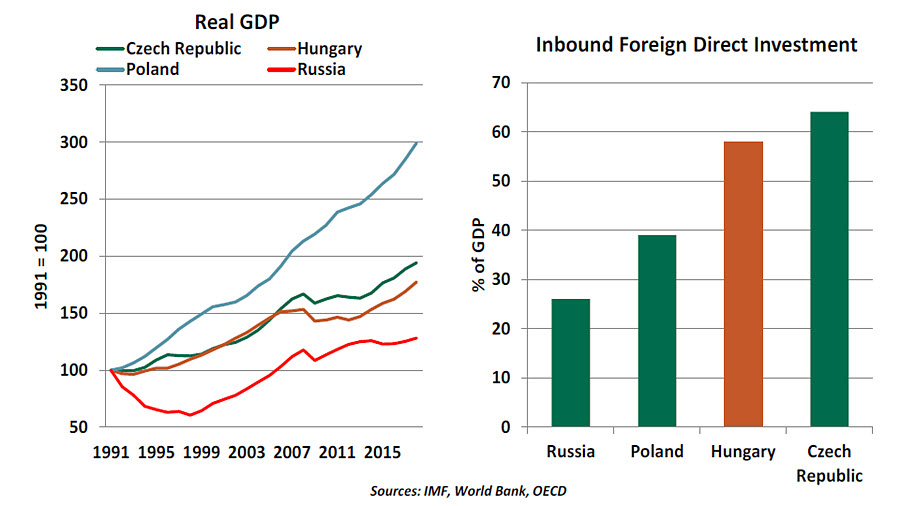

The experience of Eastern Europe suggests the long-held “Washington consensus,” a set of policy prescriptions for emerging markets, is in need of re-evaluation. The central question is whether that approach, and the institutions it relies upon, should be the subject of a mid-course correction or a wholesale re-engineering.

Regime change is also threatening the world’s monetary authorities. The relationship between economic activity and inflation, the bedrock of models used to inform policy, appears to have fractured. We economists all attempted to explain why inflation remains low, despite low unemployment. We were able to find some links between costs and wages, but we conceded these links are vulnerable to e-commerce and advanced analytics. This regime change in pricing dynamics places inflation targets further out of reach.

The failure of growth to kindle inflation during the current cycle has rendered central bank tools much less effective. The struggle of central banks to fulfill their missions has provided a fertile field for those seeking to alter those missions. Fiscal authorities who are deeply indebted, traders that want puts on market prices, and nationalists who want to weaponize exchange rates in a trade war have all moved to press their agendas with global central banks. Everyone, it seems, wants lower interest rates.

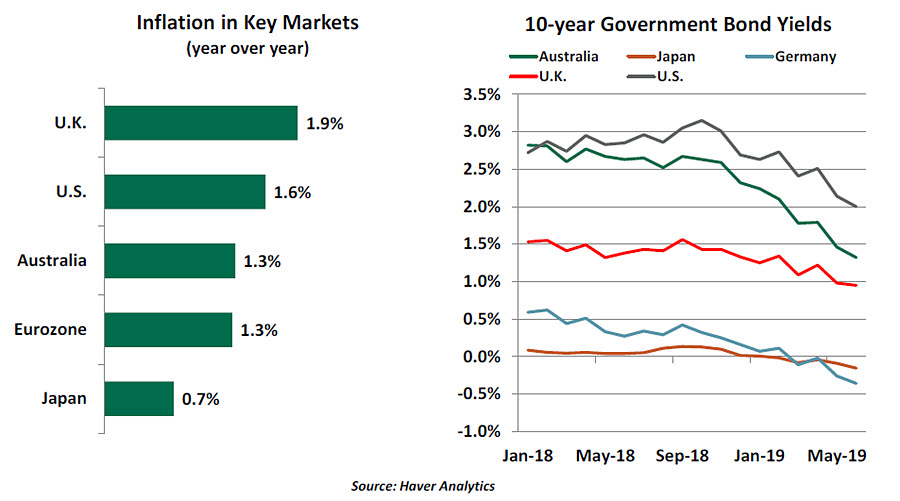

This pressure may be one reason for the collapse in term premiums and the inversion of yield curves. The phenomenon is still not well understood and has the potential to reverse, creating uncertainty in global fixed income markets.

The model offered by the Hungarian central bank, the Magyar Nemzeti, is certainly an illustration of the new monetary doctrines that are arising. The bank is taking a more direct role in allocating credit, fostering capital market development and helping set and achieve national economic objectives. To some, this is a logical response to competition from countries where political and monetary integration is further along.

To others, it is a dangerous violation of the integrity of a critical economic institution, and raises the risk of undesirable long-term outcomes. Risks to financial stability and other unintended consequences of “lower for longer” (or in the case of some markets, lower forever) are elevated.

Monetary policy works with long and variable lags, and several presenters suggested those lags are getting longer and more variable. To some, that recommends that we not be overly concerned about easy money. But we should be careful not to confuse long lags with the absence of consequences.

“Central bank missions and mandates are under broad review.”

Modern Monetary Theory (MMT) is an extreme expression of the reformulation of economic policy. It is marketed as monetary policy, but in fact, its prescriptions include elements more commonly the responsibility of the legislative branch. Some believe MMT should only be applied in case of emergency. For others, it has become business as usual.

Regime change is also apparent in industrial policy. On one hand, there seems to be a trend toward supporting national champions in key industries; on another, there are renewed efforts in some parts of the world to call out anti-competitive behavior. The romantic vision that small and medium-sized entities (SMEs) are the key to development is coming under useful question, and technology is rapidly changing who provides competition, and how.

History tells us that times change, and regimes change. Change can threaten, but it can also create opportunity if we adapt successfully. So we must try to remain open-minded as paradigms shift.

“Adapting to change is essential, but some things should stay the same.”

But are there certain immutable principles and institutions that should not shift with the prevailing tides? And how can we define and enable them in an increasingly fragmented world economy? These were the main questions that challenged the group this year.

Towering above Buda Castle is a statue of the Turul. This bird of prey plays a central role in Magyar mythology; it appeared in a dream to the princess Emese while she was pregnant with prince Álmos. According to legend, a Turul was dispatched with a sword in its talons to seek a suitable settling place for the Magyars; the bird dropped the sword on the hills above the Danube River. Prince Álmos led his people to settle on that spot, founding the Hungarian kingdom in Buda.

Our recent discussions helped the membership put stakes in the ground to separate the timeless from the transitory. Through our work and through our networks, our community is positioned to help confront some of the more troubling forces in the world today. We all agreed to pursue that objective vigorously.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

Read more commentaries by Northern Trust