The trade truce between China and the United States was short-lived. In a flurry of economic news following a fruitless negotiation round, the United States threatened new tariffs on all imports from China; China cancelled U.S. agriculture orders; China allowed its currency to devalue amid the market volatility; and the U.S. labeled China a currency manipulator. The prospects for a trade deal have diminished, to say the least.

However, our overall outlook for the United States has not changed. The majority of domestic economic activity is driven by consumption; a low dependence on exports makes the U.S. less exposed to the risks of a trade war. Our expectations already reflected slower growth and moderate inflation. While U.S. Treasury yields have fallen amid a flight to quality, we expect that the U.S. economy will continue to show its resilience.

We will discuss the latest setback in global relations in our upcoming Weekly Economic Commentary. In the meantime, factors driving our U.S. outlook to follow.

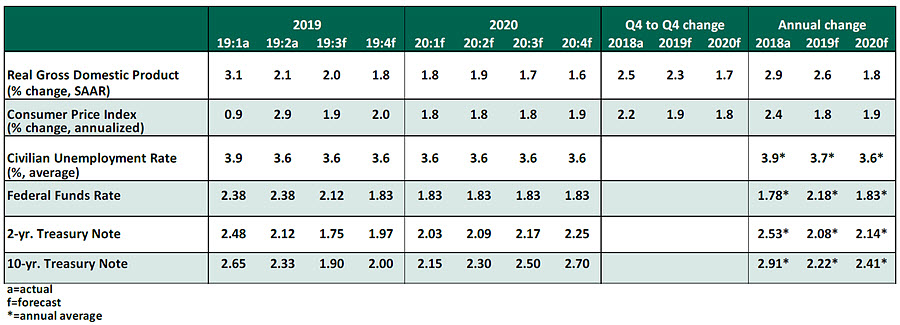

Key Economic Indicators

Influences on the Forecast

- At its July meeting, the Federal Open Market Committee (FOMC) cut the Federal Funds Rate by 0.25%, completing the 180-degree turn in its stance from raising rates as recently as December. In his commentary, Chair Jerome Powell consistently emphasized that the cut was meant to show the Fed’s resolve to protect the economic expansion cycle from the risks of a global slowdown, trade risks and slow inflation.

Markets were unnerved when Powell characterized the cut as a “mid-cycle” adjustment. He clarified that this meant a downward adjustment after a series of hikes, as seen in past growth cycles. He tried to stress that the move was neither the start of a prolonged cutting trend, nor necessarily the only cut to come.

We anticipate one additional rate cut in September, with further reductions only if necessitated by external circumstances. The FOMC seems somewhat divided on the way forward.

- One day after the Fed made its accommodative rate change, President Trump issued a renewed threat to place 10% tariffs on the remaining $300 billion of goods from China not currently subject to tariffs. The market response was swift and negative, diminishing equity markets and the value of the renminbi.

- Amid the market reaction to renewed trade threats, U.S. Treasury rates fell across all tenors. The flight to quality continues to depress U.S. yields. While we expect rates to rise as markets settle, the reset will be gradual, and we have adjusted our rate outlook accordingly.

- The unemployment rate held steady at 3.7% in July. Continuing a long-running trend, new jobs created were roughly matched with a rise in labor force participation. The addition of new workers helped to again constrain wage growth to 3.2% year-over-year. While wages have yet to grow exceptionally, the July reading marked a full year of wage increases of 3% or higher in each month.

- The initial estimate for U.S. gross domestic product (GDP) in the second quarter revealed a mixed picture. Overall growth of 2.1% was fueled by surprisingly strong consumer spending. Despite the accumulation of downside risks, consumers are still working, earning and spending. Business investment declined in the quarter, reflecting elevated uncertainty. We expect the second half to continue a steady return toward potential growth rates below 2%.

- Inflation remains subdued but appears to have stopped its decline. The consumer price index (CPI) increased 1.6% year-over-year in June, while core CPI, excluding food and energy, grew by 2.1%. Personal consumption expenditures showed a similar trend, with the broad measure growing by 1.4% and core by 1.6%. All of these figures are above the lowest levels seen thus far in 2019. We see inflation increasing during the next year, but only gradually.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

More Factor-Based Investing Topics >