8-Reasons To Hold Some Extra Cash

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOver the past few months, we have been writing a series of articles that highlight our concerns of increasing market risk. Here is a sampling of some of our more recent newsletters on the issue.

- Never Hurts To Ring The Cash Register

- Looking For A Sellable Rally

- Bull vs. Bear Case

- Don’t Fear A Bear Market

- Risk Happens Fast

The common thread among these articles was to encourage our readers to use rallies to reduce risk as the “bull case” was being eroded by slower economic growth, weaker earnings, trade wars, and the end of the stimulus from tax cuts and natural disasters. To wit:

These “warning signs” are just that. None of them suggest the markets, or the economy, are immediately plunging into the next recession-driven market reversion.

However, The equity market stopped being a leading indicator, or an economic barometer, a long time ago. Central banks looked after that. This entire cycle saw the weakest economic growth of all time couple the mother of all bull markets.

There will be payback for that misalignment of funds.“

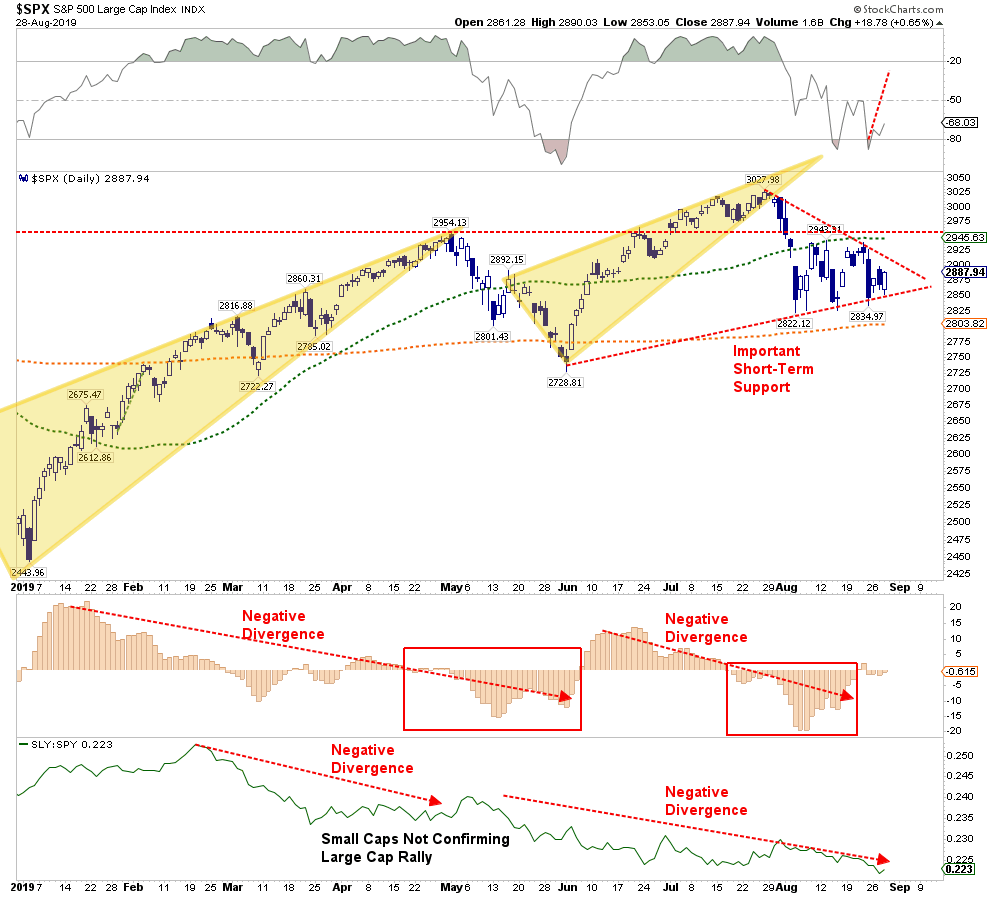

As I noted on Tuesday, the divergences between large-caps and almost every other equity index strongly suggest that something is not quite right. As shown in the chart below, that negative divergence is something we should not discount.

However, this is where it gets difficult for investors.

- The “bulls” are hoping for a break to the upside which would logically lead to a retest of old highs.

- The “bears” are concerned about a downside break which would likely lead to a retest of last December’s lows.

- Which way will it break? Nobody really knows.

This is why we have been suggesting raising cash on rallies, and rebalancing risk until the path forward becomes clear. Importantly:

“The reason we suggest selling any rally is because, until the pattern changes, the market is exhibiting all traits of a ‘topping process.’ As the saying goes, a market-top is not an event; it’s a process.”

With no trade deal in sight, slowing global growth, a Fed that doesn’t appear to want to cut rates aggressively, and weakness in markets continuing to spread, it is now time to take some actions.

Time To Take Some Action

Investors tend to make to critical mistakes in managing their portfolios.

- Investors are slow to react to new information (they anchor), which initially leads to under-reaction but eventually shifts to over-reaction during late-cycle stages.

- Investors are ultimately driven by the “herding” effect. A rising market leads to “justifications” to explain over-valued holdings. In other words, buying begets more buying.

- Lastly, as the markets turn, the “disposition” effect takes hold and winners are sold to protect gains, but losers are held in the hopes of better prices later.

The last point is relevant to today’s discussion. Investors tend to identify very “specific” price targets to take action. For example, in the chart above, the 50-dma, our previous target, currently resides at roughly at 2950.

The mistake is only taking action if a specific target is met. If the price target isn’t precisely reached, no action is taken. As prices begin to fall, investors start hoping for a “second shot” at the price target to get out. More often than not, investors wind up disappointed.

As Maxwell Smart used to say: “Missed it by that much.”

In our own portfolio management practice, technical analysis is a critical component of the overall process, and carries just as much weight as the fundamental analysis. As I have often stated:

“Fundamentals tell us WHAT to buy or sell, Technicals tell us WHEN to do it.”

In our methodology, technical price points are “neighborhoods” rather than “specific houses.” While a buy/sell target is always identified BEFORE a transaction is made, we will execute when we get into the general “neighborhood.”

We are now in the “neighborhood” given both the recent struggles of the market, the deteriorating technical backdrop, and our outlook over the next several months for further acceleration of the trade war.

This all suggests that we reduce equity risk modestly, and further increase our cash hedge, until such time as there is more “clarity” with respect to where markets are heading next.

This brings me to the most important point.

8-Reasons To Hold Cash

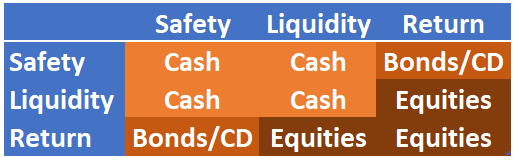

In portfolio management, you can ONLY have 2-of-3 components of any investment or asset class: Safety, Liquidity & Return. The table below is the matrix of your options.

The takeaway is that cash is the only asset class that provides safety and liquidity. Obviously, this comes at the cost of return. This is basic. But what about other options?

- Fixed Annuities (Indexed) – safety and return, no liquidity.

- ETF’s – liquidity and return, no safety.

- Mutual Funds – liquidity and return, no safety.

- Real Estate – safety and return, no liquidity.

- Traded REIT’s – liquidity and return, no safety.

- Commodities – liquidity and return, no safety.

- Gold – liquidity and return, no safety.

You get the idea. No matter what you chose to invest in – you can only have 2 of the 3 components. This is an important, and often overlooked, consideration when determining portfolio construction and allocation. The important thing to understand, and what the mainstream media doesn’t tell you, is that “Liquidity” gives you options.

I learned a long time ago that while a “rising tide lifts all boats,” eventually the “tide recedes.” I made one simple adjustment to my portfolio management over the years which has served me well. When risks begin to outweigh the potential for reward, I raise cash.

The great thing about holding extra cash is that if I’m wrong, I simply make the proper adjustments to increase the risk in my portfolios. However, if I am right, I protect investment capital from destruction and spend far less time “getting back to even” and spend more time working towards my long-term investment goals.

Here are my reasons why having cash is important.

1) We are not investors, we are speculators. We are buying pieces of paper at one price with an endeavor to eventually sell them at a higher price. This is speculation at its purest form. Therefore, when probabilities outweigh the possibilities, I raise cash.

2) 80% of stocks move in the direction of the market. In other words, if the market is moving in a downtrend, it doesn’t matter how good the company is as most likely it will decline with the overall market.

3) The best traders understand the value of cash. From Jesse Livermore to Gerald Loeb they all believed one thing – “Buy low and Sell High.” If you “Sell High” then you have raised cash. According to Harvard Business Review, since 1886, the US economy has been in a recession or depression 61% of the time. I realize that the stock market does not equal the economy, but they are highly correlated.

4) Roughly 90% of what we’re taught about the stock market is flat out wrong: dollar-cost averaging, buy and hold, buy cheap stocks, always be in the market. The last point has certainly been proven wrong as we have seen two declines of over -50%…just in the last 19-years. Keep in mind, it takes a +100% gain to recover a -50% decline.

5) 80% of individual traders lose money over ANY 10-year period. Why? Investor psychology, emotional biases, lack of capital, etc. Repeated studies by Dalbar prove this over and over again.

6) Raising cash is often a better hedge than shorting. While shorting the market, or a position, to hedge risk in a portfolio is reasonable, it also merely transfers the “risk of being wrong” from one side of the ledger to the other. Cash protects capital. Period. When a new trend, either bullish or bearish, is evident then appropriate investments can be made. In a “bull trend” you should only be neutral or long, and in a “bear trend” only neutral or short. When the trend is not evident – cash is the best solution.

7) You can’t “buy low” if you don’t have anything to “buy with.” While the media chastises individuals for holding cash, it should be somewhat evident that by not “selling rich” you do not have the capital with which to “buy cheap.”

8) Cash protects against forced liquidations. One of the biggest problems for Americans currently, according to repeated surveys, is a lack of cash to meet emergencies. Having a cash cushion allows for working with life’s nasty little curves it throws at us from time to time without being forced to liquidate investments at the most inopportune times. Layoffs, employment changes, etc. which are economically driven tend to occur with downturns which coincide with market losses. Having cash allows you to weather the storms.

Importantly, I want to stress that I am not talking about being 100% in cash.

I am suggesting that holding higher levels of cash during periods of uncertainty provides both stability and opportunity.

With the political, fundamental, and economic backdrop becoming much more hostile toward investors in the intermediate term, understanding the value of cash as a “hedge” against loss becomes much more important.

Given the length of the current market advance, deteriorating internals, high valuations, and weak economic backdrop; reviewing cash as an asset class in your allocation may make some sense. Chasing yield at any cost has typically not ended well for most.

Of course, since Wall Street does not make fees on investors holding cash, maybe there is another reason they are so adamant that you remain invested all the time.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All