Europe Flirts With Recession

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- Europe At Risk For Recession

- Will Germany Open Its Wallet?

- Government Debt Goes Long

The city of Biarritz is part of the pays de Basque, which spans southwestern France and north-central Spain. The Basques’ unique cultural identity has often led to separatist sentiment. One of the symbols of the Basque region is the piment d’Espelette, a spicy pepper used in the local cuisine.

Last weekend, Biarritz played host to the latest leadership meeting of the Group of Seven (G7) countries. The G7 membership is taken from the largest Western-style economies: the United States, Japan, Germany, France, Canada, the United Kingdom and Italy. (Delegates from the European Union are also in attendance.) Its intent is to foster discussion and diplomacy among member nations, which together account for almost half of the world’s economic output.

Unfortunately, this year’s gathering of G7 leaders produced lots of separatist sentiment, and lots of spicy plot twists. European delegates returned to their homes without a coordinated commitment to re-open global trade, leaving the Old World to face the end of its economic expansion.

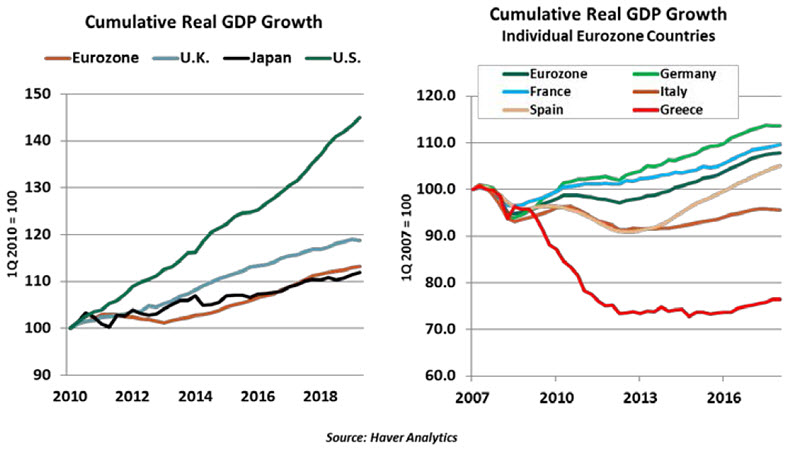

Europe emerged more slowly than other regions from the 2008 recession, and its expansion has been modest and uneven. In 2012 it was forced to cope with a sovereign debt crisis, and budget rules within the eurozone prevented the kind of fiscal stimulus that was applied in other jurisdictions. Regulators in Europe were less forceful in recapitalizing the region’s banks, which limited the flow of credit to firms and individuals.

But starting in 2014, the eurozone economy found its footing. Growth rebounded, confidence recovered, and markets performed well. The unemployment rate in the region is almost 5% below its post-crisis peak, and several of the weaker countries in the area have regained strength.

The European Central Bank (ECB) deserves considerable credit for engineering the turnaround. Seven years ago, ECB President Mario Draghi initiated a series of forceful actions. Confidence was restored, and economic progress followed.

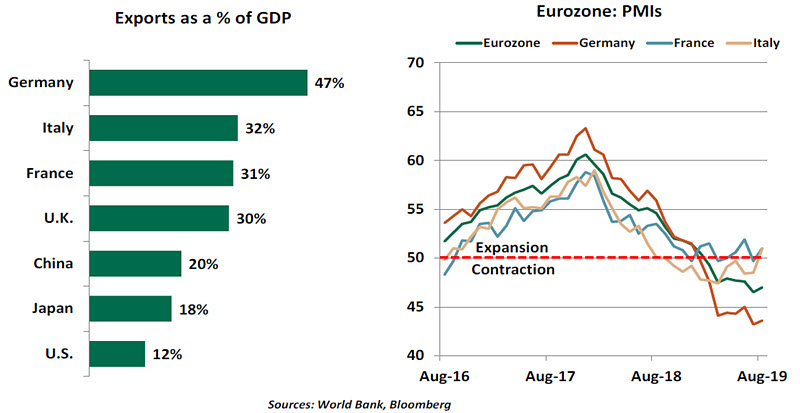

The eurozone also benefitted from strong growth in overseas markets. The U.S. and China are both important clients for European companies, and both implemented substantial amounts of post-crisis stimulus. European exports surged.

“Europe’s economy depends far more on trade than other regions do.”

Just as the outlook for Europe seemed brightest, however, the tone surrounding global trade turned negative. Difficulties between China and the United States have been the most prominent, but not the only, example of retreat from free trade principles. Tariffs and other trade restrictions are proliferating around the world, the products of economic inequality and the nationalist sentiment it has engendered.

While Europe hasn’t been Washington’s primary focus, the American administration has threatened action against industries including Europe’s auto and aircraft makers. Even if these actions are ultimately averted, the uncertainty the threats create is inimical to economic growth.

Europe’s export dependence, and its central role in global supply chains, has left it especially vulnerable to the narrowing of trade channels. As we detailed earlier this year, Germany has been especially hard-hit. Surveys of business confidence in that country have plummeted. German gross domestic product (GDP) contracted in the second quarter of the year, and is not expected to recover much during the balance of 2019.

With its main engine sputtering, the broader eurozone economy has slowed to a near crawl. Inflation and inflation expectations in the region have fallen sharply, and stand well below the ECB target. Some observers warn that Europe is at renewed risk for “Japanification,” a long period of stagnation that policy struggles to address.

Five thousand miles from Biarritz, in Jackson Hole, Wyoming, the world’s central bankers spent last weekend assessing the current situation and debating their options. Those assembled expressed a collective concern that monetary policy was not well-suited to offset restrictive trade policy. The tools available work subtly and over long time horizons.

Mario Draghi did not make the trip to Jackson Hole this year. He and his colleagues are deeply engaged in determining how they might avoid a worst-case outcome. (See the following article.) This is certainly not the valedictory Mr. Draghi was hoping for in the final two months of his tenure.

Using fiscal policy to address the advancing malaise will be complicated by Europe’s governance structure. The eurozone is not a perfect union: countries share a common currency and a common monetary policy, but spending initiatives remain the province of local legislatures. Budgets for member states are subject to review from the European Commission in Brussels, a process that has become increasingly stressful.

“Politics in Europe will complicate efforts to avoid recession.”

The volatile political landscape in Europe has complicated policy making of all kinds. Italy’s government fell last week, Angela Merkel’s tenure as German chancellor will soon end, “Euroskeptic” parties are gaining ground, and the Brexit deadline is only two months away. Weak leadership and rising uncertainty make it difficult to reach decisive policy decisions.

The silver lining in all of this may be that Germany’s struggles could lead it to be more supportive of stimulus. In recent years, Germany thrived while others struggled; German policy makers consequently took a hard line on monetary and fiscal policy. Facing problems at home, Berlin may be forced to open its purse strings and allow other European capitals to do the same.

Biarritz is known for its beaches and its massive casino, which attract people from all over Europe who come to relax during the summer. Unfortunately, the European leaders assembled for the G-7 meeting received little relief from the heat created by faltering economic conditions. The odds of recession in Europe are rising.

Not So Easy

Just last December, the European Central Bank (ECB) ended its €2.6 trillion ($3 trillion) stimulus program, a step seen as the first step toward “normalization” of monetary policy. But the bad news that has accumulated from mid-2018 through today is pushing the ECB to reverse its course. Outgoing ECB President Mario Draghi has set the stage for more easing in September.

Market participants are expecting the ECB to move its deposit rate deeper into negative territory (with the introduction of a tiering system) and resume its bond-buying program. New, targeted longer-term refinancing operations are also likely to support lending conditions. These measures, while a step in the right direction, will not be enough.

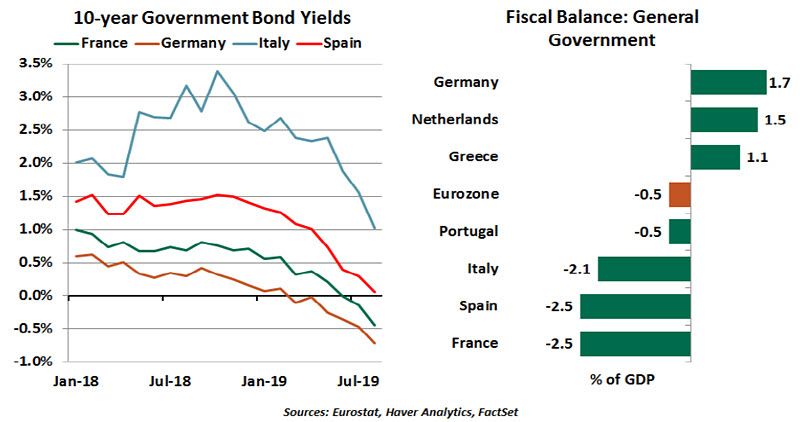

Low interest rates, coupled with the ECB’s large program of asset purchases, have pushed government bond yields lower, even into negative territory. With rates languishing at historic lows, further cuts are unlikely to yield any additional benefit. At last week’s Jackson Hole symposium, U.S. Federal Reserve Chair Jerome Powell stated that monetary policy “cannot provide a settled rulebook in international trade,” implying monetary policy is the wrong tool for balancing protectionist trade policies.

A rate cut could push the euro’s exchange rate lower, potentially benefiting European exporters. But with other central banks following suit, any benefits would be short-lived. Deeper negative rates would also dent the profitability of banks, particularly the weaker ones. According to a recent study by the ECB’s staff, “healthy” eurozone banks are able to pass on negative rates to their depositors more than other banks. For this reason, there is talk of introducing a tiered system in which reserves below a defined threshold will not be subject to negative rates. (Negative rates, if continued over longer period of time, can discourage savings and distort asset prices as well.)

Quantitative easing is nearing the ECB’s limit of owning more than a third of each country’s debt (especially in Germany, Finland and the Netherlands). There are political barriers as well. Northern states like Germany, with higher inflation and growth rates until recently, aren’t big fans of easing, perceiving it as a bailout of less-disciplined European nations funded by German taxpayers. Recently, the Bundesbank’s president, Jens Weidmann, announced his opposition to easing, asserting that he was “particularly cautious about government bond purchases,” as they distort the line between monetary and fiscal policy.

Considering the constraints and concerns around further easing, a coordinated fiscal boost is needed. As a whole, the eurozone is running a nearly balanced fiscal account, with a deficit of only -0.5% of gross domestic product (GDP). Its public debt has fallen from recent highs, suggesting some space for an expansionary fiscal stance. Low or negative financing rates provide further support for budget expansion. Reports suggest Germany is willing to embrace this approach.

“Striking a balance between monetary and fiscal easing won’t be easy.”

Core markets like France, Italy and Spain are struggling to manage their economies and public finances. At times, their public spending has not been applied in the ways most accretive to economic growth. Allowing them additional budget room would have to be accompanied by monitoring of how the money is being invested. Further, the fiscal expansion must be undertaken in a way that does not significantly undermine the debt and deficit rules set out in the Maastricht Treaty, which were designed to make the euro a strong and credible currency.

In 2012, Mario Draghi vowed that the ECB would to do “whatever it takes” to support the eurozone economy. If Europe is to sustain its expansion, other policy makers in the region will have to make and deliver on the same promise.

Long Time No See

Ryan reports on the rising popularity of very long-term bonds.

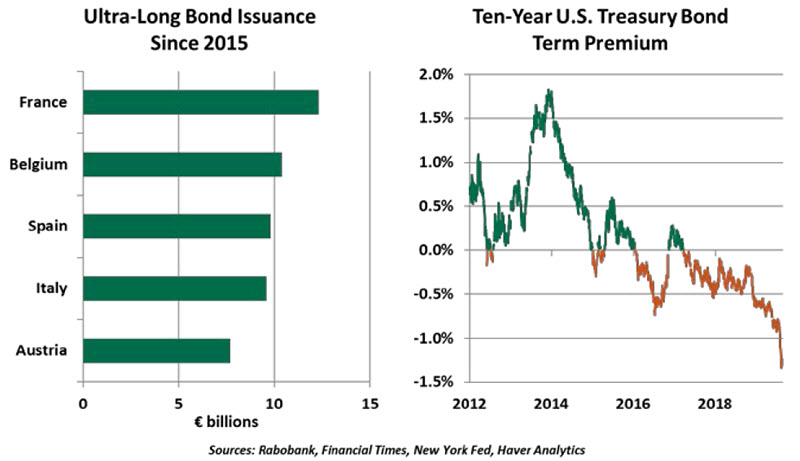

This week, my parents celebrated 50 years of marriage. It’s hard for most of us to conceive of a bond lasting that long. But in another arena, governments are floating debt with maturities as long as 100 years. These “ultra-long” bonds” are becoming more common and more popular.

This summer, Austria successfully auctioned a €1 billion 100-year bond to public buyers, following on their €3.5 billion century offering in 2017. Countries including Belgium, Ireland, Argentina and Mexico have sold century bonds, while others have issued debt carrying maturities of 40 or 50 years.

The U.S. has recently contemplated extending terms beyond 30 years. In 2017 and again this summer, the Treasury Department surveyed its primary dealers as to the demand and expected premium for ultra-long U.S. bonds, but met a cool reception. The case to issue seems strong: Yields are low, term premiums are negative and demand is high, an ideal time for the Treasury to lock in low rates. But dealers were uncertain of the demand and liquidity in a new market.

Buyers of European ultra-long bonds have had a winning year. As capital flows into fixed income instruments, their prices have been bid up. The longer the note’s duration, the greater the gain has been for the bond’s holders. Of course, the risk runs in both directions; a selloff would hurt holders of ultra-long bonds most. But it is also likely that the bond buyers may not be price-sensitive. Ultra-long buyers are often pension funds and insurers seeking to match their long-dated liabilities with assets of similarly long durations. The current pricing volatility is an afterthought; the safe and steady coupon payment is sufficient for their needs.

“In volatile times, the certainty of a long-dated bond has appeal.”

Government bonds and marital bonds have little in common, but both are based on an expectation of positive future returns. At a celebration among family this past weekend, my mother reflected on her long union with my father: “Of course we had ups and downs, but there were more ups than downs.” We wish the same fortune for holders of ultra-long securities.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All