Brexit, trade tensions, global slowdown: The themes are familiar, but the stakes keep getting higher.

SUMMARY

Instead of a calm end to summer, the past month has brought more downside risks for the global economy. The U.S. and China mutually raised tariffs, while evidence of a slowdown in the eurozone is accumulating. Brexit outcomes have become even more difficult to predict. Civil unrest in Hong Kong and a rebuilt governing coalition in Italy are the latest examples of imbalances seen around the world.

At this juncture, the best we can hope for is no further deterioration of economic conditions. The escalation of U.S. tariffs on goods from China will proceed as threatened this year, but tariffs are reaching their natural limit as a policy threat. Policymakers’ comments during and after the G7 and Jackson Hole conferences failed to offer new insights or reason to expect renewed growth in any region.

The ongoing uncertainties will continue to weigh on economic prospects for the remainder of the year and into 2020. Our outlook for the world’s major economies is cautious.

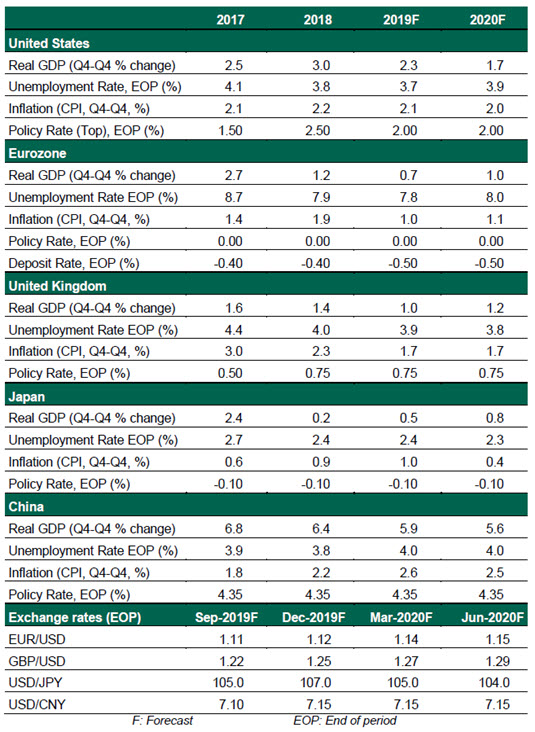

United States

- While parts of the U.S. economy, including business investment, are sluggish, the hale and hearty U.S. consumer is encouraging. Backed by a solid labor market, the Conference Board Consumer Confidence Index reaffirms that consumers are willing to spend. The situation could reverse if more of the cost of U.S.-China trade actions is passed on to consumers. We expect growth to remain near 2% for 2019, but as protectionist measures expand, growth will likely fall below that level in 2020.

Japan

- Yields on Japanese government bonds fell deeper into negative territory as a global flight to this safe-haven currency pushes down yields. The Bank of Japan has not intervened to control the yield curve, and we do not expect it will make any changes to its policy rate.

- Growth prospects for Japan remain dim, with slow growth in exports and capital spending. The consumption tax hike to come later in 2019 will weigh on consumer spending and boost inflation. An overture by the U.S. to strike a trade deal with Japan may not amount to an actual agreement, but the risk of a further slowdown due to tariffs has receded for the moment.

China

- Normally a closely managed currency, the renminbi was allowed to devalue below 7 per U.S. dollar, a symbolic threshold not crossed since 2008. Deteriorating growth conditions in China are the primary driver of the devaluation, but the ability to blunt some of the effects of tariffs is a bonus to China. We expect the value to stay depressed until a trade deal is struck.

- China fought back against the latest U.S. tariffs with retaliatory tariffs of its own, making the possibility of a deal feel more remote. The tariff battle has little remaining scope for further escalation, but we do not expect it to spread into other arenas.

- China reformed its interest rate regime by creating a new loan prime rate, giving the People’s Bank of China closer control over loan rates to encourage bank lending. China will continue to look inward for stimulus measures.

Global Economic Forecast – September 2019

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

© Northern Trust

More Alternative Investments Topics >