The trade war between the world’s two largest economies entered its 18th month in September with the U.S. imposing fresh 15 percent tariffs on $125 billion worth of goods imported from China. China retaliated in kind, but a breakthrough could happen sooner rather than later. According to reports, trade representatives from both countries have agreed to hold new talks in early October, and there’s optimism that this could be “the one.”

“China and the U.S. announced new round of trade talks and will work to make substantial progress,” Hu Xijin, editor-in-chief of the Global Times, tweeted on Thursday. “Personally I think the U.S., worn out by the trade war, may no longer hope for crushing China’s will. There’s more possibility of a breakthrough between the two sides.”

CNBC writes that Hu has been spot on with past developments in the ongoing trade war. Many Wall Street traders follow him for insight on what could happen next.

One thing Hu is right about—the trade spat is wearing on the U.S. economy, especially manufacturers. The ISM manufacturing purchasing manager’s index (PMI), an important forward-looking gauge of economic activity, has been declining steadily for months now, and in August, it shrank for the first time in three years. The PMI stood at 49.1, down from 51.2 a month earlier, its lowest reading since March 2016.

click to enlarge

Among 11 factors that the Institute for Supply Management (ISM) measures every month, only supply deliveries was still in expansion mode in August. All other factors, from new orders to employment to exports, were below the 50.0 threshold, indicating contraction.

Comments made by manufacturing executives “reflect a notable decrease in business confidence,” the report says.

This may not bode well for the domestic stock market, especially if the manufacturing sector continues to cool. In the chart above, you can see that the S&P 500 has been trading in tandem with the PMI. In August, the year-over-year percent change fell below 1 percent.

China Manufacturing Recovers, Back in Expansion Mode

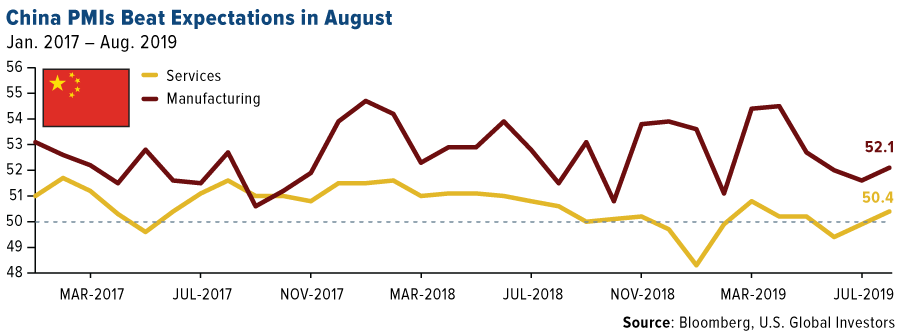

Looking across the Pacific, the trade war hasn’t been as impactful on Chinese factories as it’s been on those in the U.S. In fact, the Chinese manufacturing sector improved in August, with the PMI rising to 50.4 from 49.9 a month earlier. This is not only above consensus but also the strongest month-to-month improvement since March, according to Caixin, the private firm that produces the monthly report.

“China’s manufacturing sector showed a recovery in August, mainly due to improved production activity,” says Zhengsheng Zhong, director of macroeconomic analysis at CEBM Group. He adds, however, that “overall demand didn’t improve, and foreign demand declined notably, leading product inventories to grow.”

click to enlarge

China’s service industry also surprised to the upside in August, ticking up to 52.1.

Markets welcomed the news. The Shanghai Stock Exchange Composite Index traded up close to 1 percent on Thursday, its fourth straight day of positive gains.

China’s resilience is particularly good news for commodities and raw materials. The Asian giant represents a huge percent of global demand for commodities such as oil, iron ore, copper and many more.

Also good news is the proposed addition of new free trade zones (FTZs). As I told you earlier in the week, China recently announced that it would be creating new FTZs in as many as six provinces, making them more attractive to high-quality manufacturers.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

The Manufacturing ISM Report On Business is based on data compiled from purchasing and supply executives nationwide. The Caixin China General Services PMI is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 companies. The Caixin China Report on General Manufacturing is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 500 manufacturing companies.

The S&P 500 Indexor the Standard & Poor's 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. The SSE Composite, which is short for the Shanghai Stock Exchange Composite Index, is a market composite made up of all the A-shares and B-shares that trade on the Shanghai Stock Exchange.

© U.S. Global Investors

© U.S. Global Investors

More Alternative Investments Topics >