‘CEO/CFO Board Behaviors’

Corporate Bond spreads (additional yield over comparable US Treasury) have done a near full reversal from the wides reached in January (+147*). Today (+104*) we are very close to the tight spreads reached last year (+99*). The reversal brings our 2019 Theme #5 “CEO/CFO Board Behaviors” into play again.

We highlighted in our ‘7 Themes for 2019’ paper at the beginning of the year, the critical importance of capital structures and management teams’ focus on reducing leverage.

We believe there will be significant winners and downright losers in the capital structure management process, resulting in more significant dispersion within the credit market. We highlighted our belief that many management teams and Corporate Boards will be challenged in 2019.

We have seen early signs of deleveraging - dividends cuts, businesses sold with proceeds earmarked for debt paydown and new found verbal commitments of free cash flow finding its way toward debt reduction. In addition, some management teams have extended their debt maturities, allowing for greater financial flexibility. Other management teams are ignoring the warning signs.

We highlighted that we will learn a lot about the character and discipline of management teams and the fortitude of Corporate Boards. We will once again be reminded of the importance of leadership and the ability to adapt.

In the write-up that follows, we highlight our views on CEO/CFO behaviors around debt and the search for the perfect capital structure.

As an integral part of assuring the future health of their business, management teams must be effective capital allocators. Typically, the best run businesses have management teams that are very good, long-term capital allocators. Essentially, this responsibility is the prudent allocation of cash flows toward: reinvesting in the business in the form of capital expenditures (CapEx), managing debt profiles, engaging in Mergers & Acquisitions (M&A), and returning cash to shareholders via buybacks and/or dividends.

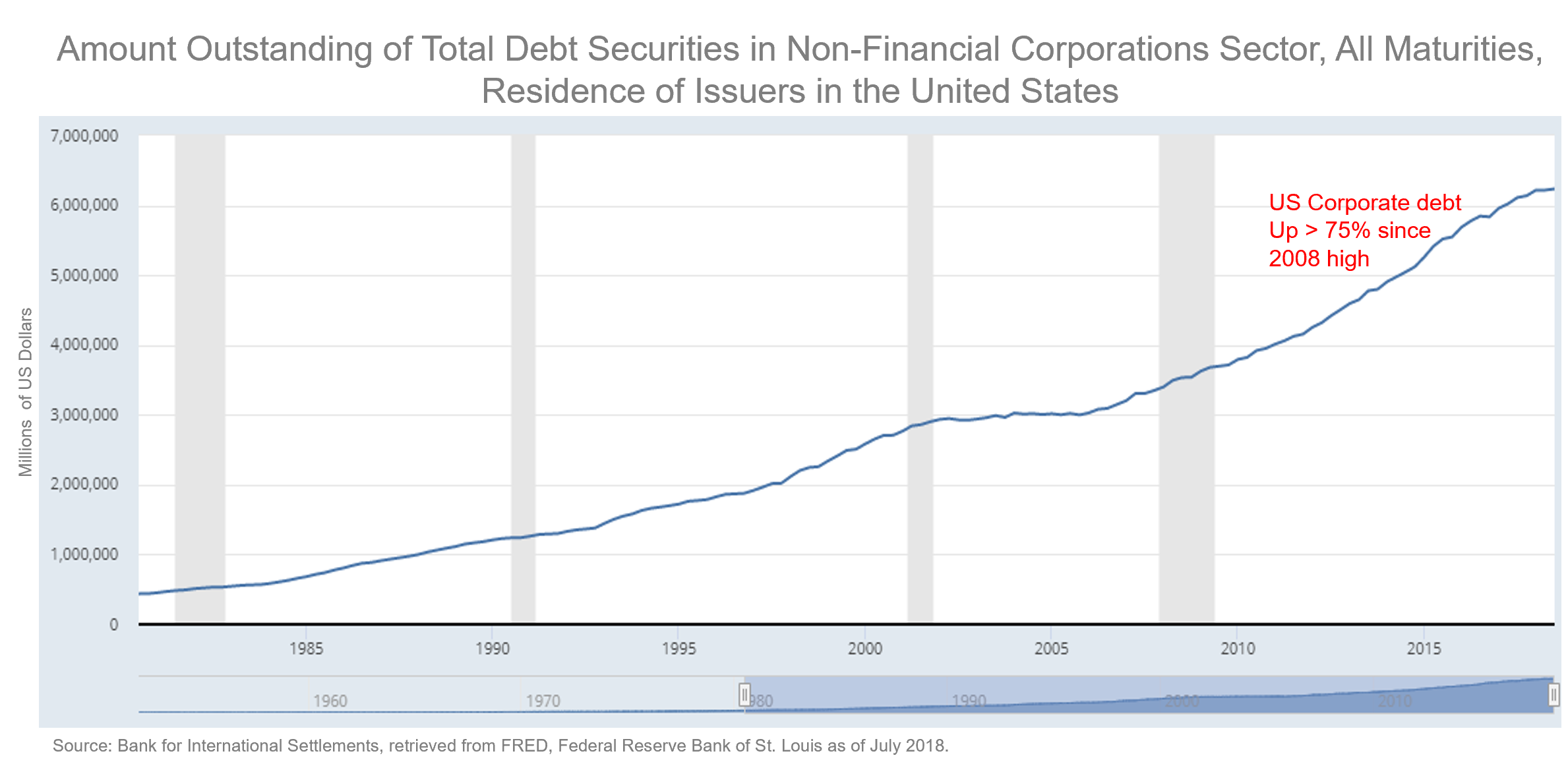

Low-interest rates and tight credit spreads often lure management teams into accelerating many of the aforementioned actions through the use of debt. Said another way, given attractive rates, we’ve seen an increasing appetite for corporations to use debt as an accelerant to “maximize shareholder value”. Furthermore, to our concern, management teams can become more complacent capital allocators and consequently increase the probability of putting their companies in a less resilient position for an unknown future.

This discussion of capital allocation would not be complete without talking about how complacent buyers of credit (also capital allocators—of their clients' money) have fueled and/or enabled more aggressive behaviors by management teams in boardrooms across America.

“If creditors are going to lend me money at that rate, why wouldn’t I borrow more?”

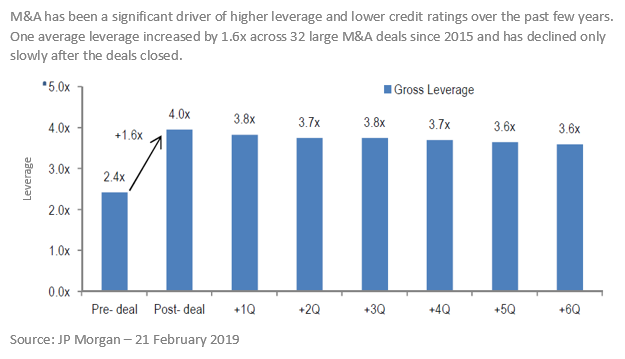

Across the credit markets, we have witnessed management teams materially increase leverage with the promise to quickly deleverage. Unfortunately, many of these deleveraging stories appear good on the surface to creditors but actually, have very narrow margins for disruption—either self-inflicted, market inflicted, or otherwise. Often, to our dismay but unsurprisingly, we see many of these less-than-thoroughly-vetted deleveraging stories get gobbled up by credit investors. This demand leads to spread tightening; giving the companies the benefit for deleveraging before any material de-risking of their balance sheets have even occurred. Note the actual pace of deleveraging across a swath of large M&A deals dating back to 2015—it has been glacially slow and certainly not in-line with the compression of spreads that these issuers have experienced over the same time period.

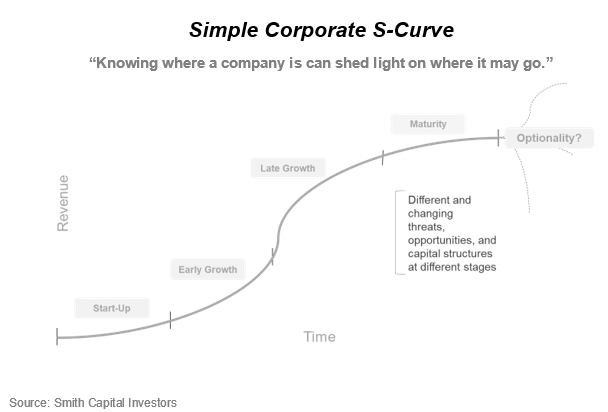

On managing capital structures, as relevant to both investors and management teams, it is crucial to know where you stand. When thinking about the life-cycle of a company as an S-curve (or hopefully a series of S-curves) it is imperative to know that optimal capital structures and capital allocation decisions should, and really must, change over the course of this lifecycle.

It can result in significant future consequences by complacently setting up a capital structure and making capital allocation decisions optimized for the current environment. When both companies and investors become “offsides”, as a result of a changing environment, therein can lay great opportunity for those that have more appropriately positioned for the future. This is not to say a management team or investor can predict the future but rather taking such an approach can put those practitioners in a more resilient, opportunistic position where they are able to adapt to a wider array of possible outcomes.

We believe the recent mini cycle is a great representation of the need for investors to be very present around fundamentals and valuations.

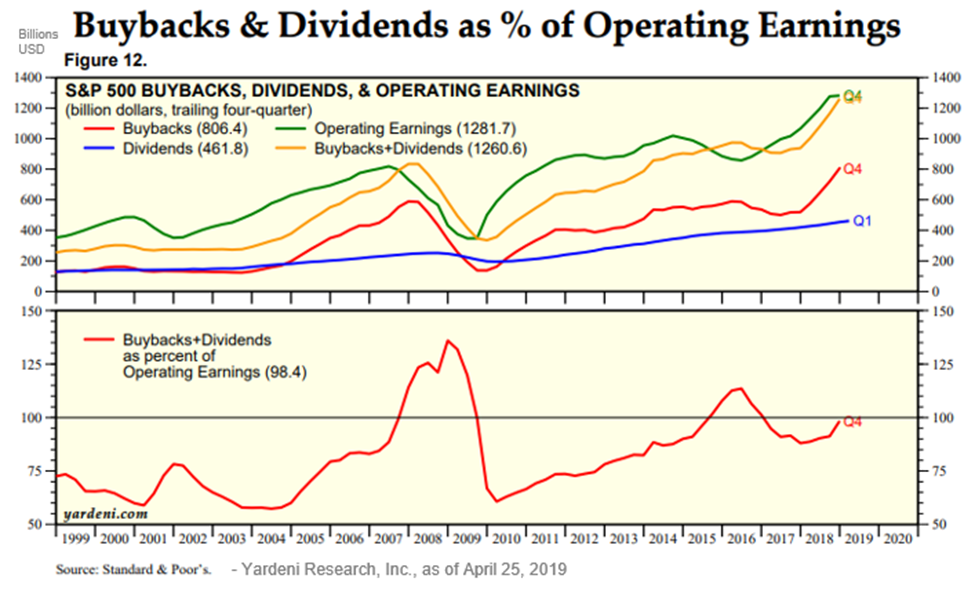

On capital allocation, it is no secret that corporations have been amongst the biggest buyers of their own stock. Shareholder buybacks have been an essential ingredient in fueling the rise of equities as companies have taken advantage of increasing earnings and cheap debt. Commitments to dividends and buybacks now account for almost the entirety of the average use of an S&P 500 company’s operating earnings. The chart below illustrates this.

What happens, however, when future earnings disappoint? On this, we believe we need not look any further than the current environment. Earnings growth expectations for 2019 have swiftly moved from 12% down to 5% since September of last year! What happens when earnings deteriorate and cash to support Earnings Per Share (EPS) growth via share buybacks also dwindles? That is a double whammy!

Will companies be able to issue additional debt at attractive rates when they’ve already ‘optimized’ their capital structures for the current environment? It seems to us that many management teams have traded better earnings and “shareholder friendly” actions in the current “good times” for less flexibility when the inevitable “not so good times” come.

Can companies adjust their balance sheets fast enough to adapt to a changing environment? Some will be able to, some will not, and others will only be able to do so by materially changing the way they allocate capital. This, in effect, reverses much of the aforementioned accelerated “maximization of shareholder value”.

In our decades of observing businesses, we have concluded that management teams who optimize for the current environment are often guilty of making overly narrow predictions about the future. Namely, they make a prediction that the future will play out much like the present. Conversely, we’ve observed that management teams that place a premium on the ability to adapt, tend to preserve optionality. This gives them the ability to adapt to a wide range of future outcomes, many of which are likely materially different than the current environment. This behavior often looks sub-optimal in the near term but prescient over the long-term. One needs to look no further than Berkshire Hathaway’s enviable track record and prodigious balance sheet to observe this statement in action.

On the other end of the spectrum, we have observed “bullet-proof” companies such as Kraft Heinz, L Brands, and PG&E, to name only a few, who have recently had to cut dividends and address their less-than-prescient capital allocation elections. These previously-thought “unimaginable” scenarios now clash with the future sustainability of their businesses.

We contend that it is management’s job to acknowledge their inability to accurately project the future and thus should manage their capital structure with this “uncertainty” embedded in their decision-making process. Furthermore, as investors, recognize those businesses and management teams that are AND those that are not positioning themselves, their shareholders, creditors, and other constituents in a position of resiliency.

It is instructive to continue with the themes that emerge from the three companies referenced above; however, lack of imagination with regard to future disruption, unsustainable capital return, or the tail risk posed by suppressing capex, are by no means unique to only these three companies.

We would argue these and other risks are rising after a prolonged period of low volatility.

First, we know that disruption risk sits at an all-time high as legacy companies make the jump into the digital age, even while fending off the threat of digital natives. The epic clash of Amazon and Walmart springs to mind, but the reader can pick their own comparison.

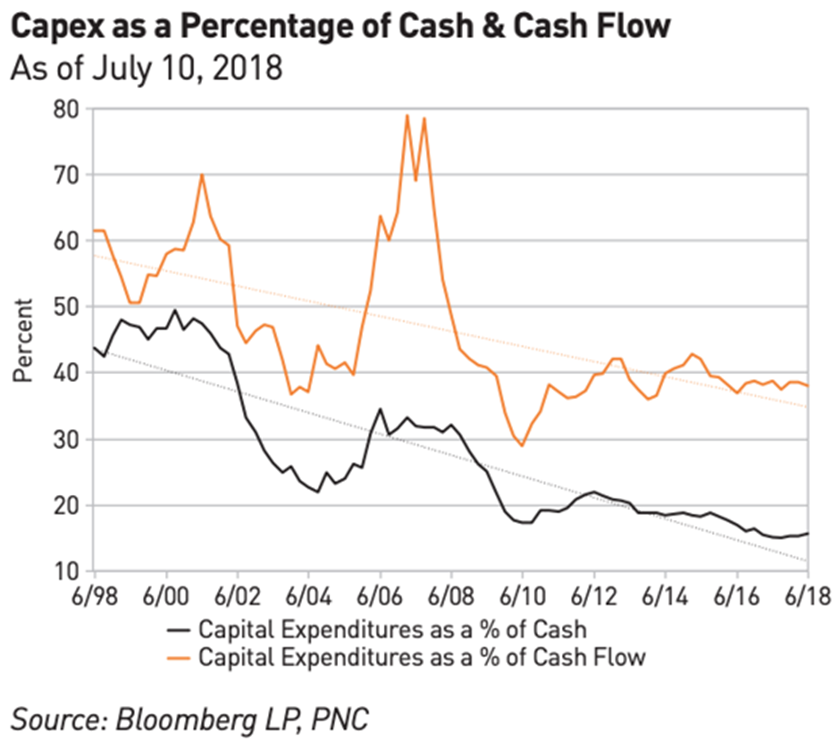

Second and third, unsustainable capital return in a swiftly changing macro environment and, furthermore, holding capex rates down in the face of disruption threats can create an unsavory cocktail for both management teams and investors. These trends can be particularly alarming – even deadly – with companies that operate aging infrastructure (such as, say, PG&E).

We fear that by using close to 100% (or in many cases, more than 100%) of free cash flow to buy back stock and pay dividends, combined with leveraging the balance sheet to fund such actions and engaging in M&A while holding capex low, management teams have painted themselves into a very dangerous corner if challenging times come.

As the liquidity tide reverses and growth slows, more and more cases of vulnerable capital structures may be revealed.

A strong balance sheet, substantial cash flows, and a well-positioned business for the future offer real and valuable options to create both share and bondholder value.

As we look to the future, we wouldn’t be surprised to see humbled leadership teams and business school case studies revealing regret and long-term value destruction as they more thoroughly look back on the massive amounts of capital committed to share repo and some of the M&A deals of the current and not too distant time periods.

As we hunt for opportunities in the credit market, we continue to place a premium on management teams that exhibit long-term thinking, foster a culture of innovation, and avoid narrow predictions about the future while preserving the ability to adapt and evolve to changing environments. We are digging beyond ratings and company-adjusted metrics to buy debt that makes sense from management teams acting as stewards for the long-term health of their businesses. Business models that have retained a margin of safety versus redlining their financial profile should be rewarded in even a mildly slowing economic environment.

The opinions and views expressed are as of the date published and are subject to change without notice. Information presented herein is for discussion and illustrative purposes only and should not be used or construed as financial, legal, or tax advice, and is not a recommendation or an offer or solicitation to buy, sell or hold any security, investment strategy, or market sector. No forecasts can be guaranteed. Any investment or management recommendation in this document is not meant to be impartial investment advice or advice in a fiduciary capacity and is not tailored to the investment needs of any specific individual or category of individuals. If you are an individual retirement investor, contact your financial advisor or other fiduciary unrelated to Smith Capital Investors about whether any given investment idea, strategy, product or service described herein may be appropriate for you. Opinions and examples are meant as an illustration of themes, are not an indication of trading intent, and are subject to change at any time due to changes in the market or economic conditions. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio.

Past performance is not a guarantee or a reliable indicator of future results. Investing in a bond market is subject to risks, including market, interest rate, issuer, credit, inflation, default, and liquidity risk. The bond market is volatile. The value of most bonds and bond strategies are impacted by changes in interest rates. Bond investments may be worth more or less than the original cost when redeemed. The return of principal is not guaranteed, and prices may decline if, among other things, an issuer fails to make timely payments or its credit strength weakens. High yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

There is no guarantee that any particular investment strategy will work under all market conditions or are suitable for all investors. Investors should consult their investment professional prior to making an investment decision. All indices are unmanaged. You cannot invest directly in an index. Index or benchmark performance presented in this document does not reflect the deduction of advisory fees, transaction charges, and other expenses, which would reduce performance.

This material may not be reproduced in whole or in part in any form, or referred to in any other publication, without express written permission from Smith Capital Investors. Smith Capital Investors, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission.

ALPS Portfolio Solutions Distributor, Inc., FINRA Member Firm.

© Smith Capital Investors

More ETF Topics >