Black Hole Investing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsRealistic Forecasts

Profound Technological Change

Income Challenges

Crazy Numbers

New York and Houston

Scientists say the rules change in a cosmic “black hole” at what astrophysicists call the event horizon. How do they know that? Not by observation, since what happens in there is, by definition, un-seeable. They infer it from the surroundings, which say that the mathematics of the universe as we understand them change at the event horizon.

Or maybe not. One theory says we are all inside a black hole right now. That could possibly explain a few things about central bank policy.

Last week I showed you Ray Dalio’s latest Three Big Issues article. To recap, Ray says we are now in a world where…

- Central banks have limited ability to stimulate growth as we approach the end of a long-term debt cycle.

- Wealth and political polarity are producing internal conflict between the rich and poor as well as between capitalists and socialist.

- There is also external conflict between a rising power (China) and the existing world leader (the USA).

The world last saw this combination in the 1930s, which is not comforting, to say the least. But as I said, we can get through this together if we approach it wisely. That’s a big “if,” given the ways some investors behave at cyclical peaks, but people will do what they do. We can only control our own actions, and today I want to talk about some we can take.

We are approaching the black hole, which means we can’t rely on previously reliable strategies. Let’s start with a jolt of reality.

Realistic Forecasts

As investors we have to make assumptions about the future. We know they will likely prove wrong, but something has to guide our asset allocation decisions.

Many long-term investors assume stocks will give them 6–8% real annual returns if they simply buy and hold long enough. Pension fund trustees hire consultants to reassure them of this “fact,” along with similar interest rate and bond forecasts, and then make investment and benefit decisions.

Those reassurances are increasingly hollow, thanks to both low rates and inflated stock valuations, yet people running massive piles of money behave as if they are unquestionably correct.

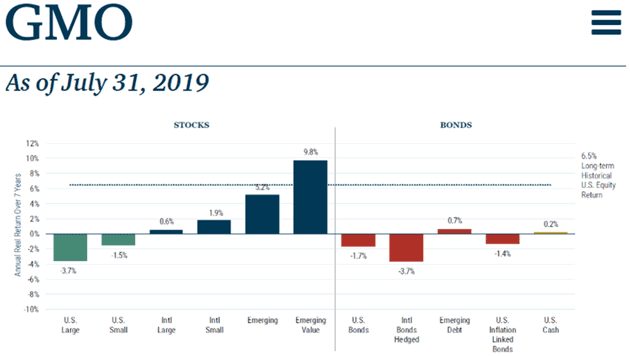

You can, however, find more realistic forecasts from reliable, conflict-free sources. One of my favorites is Grantham Mayo Van Otterloo, or GMO. Here are their latest 7-year asset class forecasts, as of July 31, 2019.

Source: GMO

These are bleak numbers if you hope to earn any positive return at all, much less 6% or more. If GMO is right, the only answer is a large allocation to emerging markets which, because they are emerging, are also riskier. The more typical 60/40 domestic stock/bond portfolio is a certain loss, according to GMO. (Note these are all “real” returns, which means the amount by which they exceed the inflation rate).

Others like my friends at Research Affiliates (Rob Arnott), Crestmont Research (Ed Easterling), or John Hussman (Hussman Funds) have similar forecasts. They differ in their methodologies but the basic direction is the same. The point is that returns in the next 7 or 10 years will not look anything like the past.

If you think these are reasonable forecasts (I do), then one reaction is to keep most of your assets in cash for at least a fractionally positive, low-risk return. That’s simple to do. But it probably won’t get you to your financial goals.

Remember, though, this forecast is what GMO expects if you buy and hold those asset classes for the next seven years. Nothing requires most of us to do that. We are free to move between them and use other asset classes, too… which is exactly what I think we should do.

Profound Technological Change

I mentioned last week that technology will bring profound changes. I’m expounding on that in my book. It has major investment implications. Companies small and large, all over the world, are right now inventing new technologies that are going to change our lives.

I’ve used this example before, but think of the now-ubiquitous smartphone. Apple launched that category with the iPhone in 2007. Many who saw them as expensive toys at first now can’t live without them. That shows you how fast, and how deeply, a technology we didn’t even know we needed can change everyday life. Not always for the better, but the change is real.

The iPhone ecosystem around it spawned other successful companies. The productivity gains it gave users led to growth in seemingly unrelated fields. We have a radically different (and, on balance, better) economy now than we would have without it.

Note also, the iPhone launched just months before the Great Recession began, and proved indispensable anyway. So our macro challenges, serious though they may be, won’t necessarily stop progress. They may even accelerate it.

I expect to see fortunes made in biotechnology, and particularly life extension and age reversal drugs, but that will only be the beginning. Autonomous vehicle technology is going to restructure our cities and enhance our productivity as we put those traffic jam hours to better use. AI and Big Data will enable quantum leaps in many fields.

I could go on with more examples, but here’s the point: Innovation will continue in almost any economic scenario you can imagine. Recession will, at most, delay it a bit. Not every innovative company will succeed but some will, and the rewards will be huge. If you want capital gains, the opportunities will be there… but not in a passive index strategy. You will need active management and expert managers.

Owning index funds won’t help much because by definition most of these companies will start out small and not have meaningful presence in the indexes. By the time they are big enough to be meaningful, the really massive gains will have already been made. That means you will want to find active managers who focus on particular fields and allocate them some of your risk (not core!) capital. These will not be sure things.

Income Challenges

Now, capital gains aren’t (and shouldn’t be) everyone’s goal. Many of my Baby Boomer peers have assets but need current income, which is scarce and getting scarcer in this low-yield world. The way central banks are going, conventional debt instruments probably won’t do it.

This week the ECB lowered its base rate to -0.50% and announced it will stay there for a long time. I think it is increasingly obvious we are headed back to the zero bound on short-term US government debt. That will drag down interest rates on most fixed income instruments.

Here again, I think the market will provide solutions but they won’t be what once was thought of as “normal.” Our parents and grandparents could count on 5% or better yields in safe, predictable CDs and Treasury bills. That’s fantasy now. So, what do you do?

The first thing, if you’re not already fully retired, is to maximize your job income and increase your savings. Watch your spending, too. Now is not the time for frivolity. Be the ant, not the grasshopper.

That still won’t be enough for most income-seeking investors. We will need higher yields from our portfolios. Right now, this is more than a minor challenge unless you want to take significant principal risk. Government bonds yield nothing (or less) and corporate bonds are headed that way. High-yield bonds indeed have higher yields but also higher risk. What to do?

I think interest rates are going lower and will stay lower for a very long time, just as I and my fellow Boomers are hitting retirement age. (I’ll start getting Social Security when I turn 70 next month. I remember reading somewhere that I’ll earn something like 1 to 2% compound returns on my Social Security “investment.” Ouch.)

The good news is that markets eventually respond to demand. More and more companies will concentrate on returning investor capital. As businesses stabilize into steady cash flow, they will be able to pay increasingly higher dividends, and may find it is a good way to maintain their share prices. In addition, I think many old-fashioned value companies are getting ready to come back into favor as their steady dividends become attractive to a retiring generation.

Remember, there are different ways to slice this pie. It doesn’t have to be standard dividends. I expect innovative structures will emerge to offer yield with controlled risk—new kinds of preferred shares, convertible securities, etc. Some exist right now, but legal barriers restrict them only to the wealthiest investors. Here again, if the demand exists, elected officials will respond by relaxing those barriers.

Higher yields come with higher risk, of course. That’s why you should spread your capital across more than one and not risk too much on any one strategy. A strategy I have seen used with great success is simple high-yield bond timing. While those trading algorithms can be complex, even simple ones can sometimes yield above-market returns over a full cycle.

As my dad would tell me when I was growing up, “Son, betteth not thy whole wad on one horse.” That was as close to biblical language as he could get.

Central banks and politicians are the problem, not the solution. Last week President Trump openly told the Federal Reserve to reduce interest rates to zero or lower.

Seriously? What business activity will that encourage? The latest National Federation of Independent Business survey (by my good friend Bill “Dunk” Dunkelberg) clearly shows that small businesses aren’t worried about interest rates. What they need is more customers and predictable government policies. In a world of trade wars and potential currency wars brought on by central bank manipulation, predictable is not a word that comes to mind.

Further, do the president and his economic advisors understand the realities facing the average retiree? In this zero-interest-rate world, exactly how are retirees supposed to survive without taking much more risk than they should?

The financial repression emanating from central banks all over the world borders on criminal, and that they think they are “helping” us is risible. They are on the verge of destroying a generation come the next recession. They have encouraged retirees to seek yield and riskier investments precisely when they should not be.

They are robbing savers and asking us to say thank you because they are so wise.

Crazy Numbers

Many financial advisors, apparently unaware the event horizon is near, continue to recommend old solutions like the “60/40” portfolio. That strategy does have a compelling history. Those who adopted and actually stuck with it (which is very hard) had several good decades. That doesn’t guarantee them several more, though. I believe times have changed.

But those decades basically started in the late 40s and went up until 2000. After 2000, the stock market (the S&P 500) has basically doubled, mostly in the last few years, which is less than a 4% return. When (not if) we have a recession and the stock market drops 40% or more, index investors will have spent 20 years with a less than 1% compound annual return. A 50% drop, which could certainly happen in a recession, would wipe out all their gains, even without inflation.

And yes, there have been historical periods where stock market returns have been negative for 20 years. 1930s anyone? Yes, it is an uncomfortable parallel.

The “logic” of 60/40 is that it gives you diversification. The bonds should perform well when the stocks run into difficulty, and vice versa. You might even get lucky and have both components rise together. But you can also be unlucky and see them both fall, an outcome I think increasingly likely. Louis Gave wrote about this last week.

Historically, the optimized portfolio of choice, and the one beloved of quant analysts everywhere, has been a balanced portfolio comprising 60% growth stocks and 40% long-dated bonds. Yet recently, this has come to look less and less like an optimized portfolio, and more and more like a “dumbbell portfolio,” in which investors hedge overvalued growth stocks with overvalued bonds.

At current valuations, such a portfolio no longer offers diversification. Instead, it is a portfolio betting outright on continued central bank intervention and ever-lower interest rates. Given some of the rhetoric coming from central bankers recently, this is a bet which could now be getting increasingly dangerous.

(Over My Shoulder members can read Louis Gave’s full “Dumbbell Portfolio” article with a summary and key points. Not a member? Click here to join us.)

We are rapidly approaching the event horizon where central bank intervention and ever-lower interest rates will not help your bond portfolio. That is already the case in Europe and Japan. Stocks are at historically high valuations and subject to a severe bear market brought on by a recession.

“Diversification” is not simply owning different asset classes. They have to be uncorrelated to each other and, more important, stay uncorrelated. That was a problem in 2008 when lots of previously disconnected categories suddenly started moving in lockstep.

For the moment, I still think long-term yields will keep falling, helping the bond side of a 60/40 portfolio. Meanwhile, negative or nearly negative yields will push more money into stocks, driving up that side of the ledger. So 60/40 could keep firing on all cylinders for a while. But it won’t do so forever, and the ending will probably be sudden and spectacular.

Which brings us to my final point. The primary investment goal as we approach the black hole should be “Hold on to what you have.” Or, in other words, capital preservation. But you may not realize that capital preservation can be better than growth, if the growth comes with too much risk. Here’s the math.

- Recovering from a 20% loss requires a 25% gain

- Recovering from a 30% loss requires a 43% gain

- Recovering from a 40% loss requires a 67% gain

- Recovering from a 50% loss requires a 100% gain

- Recovering from a 60% loss requires a 150% gain

If you fall in one of these deep holes you will spend valuable time just getting out of it before you can even start booking any gains. Once you start to fall, the black hole won’t let go. Far better not to get too close.

Friends don’t let friends buy and hold. I can’t say that strongly enough. You must have a well thought out hedging strategy if you’re going to be long the stock market. If your investment advisor simply has you in a 60/40 portfolio and tells you that “we are invested for the long term and the market will come back,” pick up your capital and walk away. I can’t be any more blunt than that.

Every investment advisor, including me, uses these words in their disclosure documents: Past Performance Is Not Indicative of Future Results. I think that has never been more true than for the coming decade. The 2020s will be more volatile and difficult for the typical buy-and-hold index fund investor than anything we have seen in my lifetime.

Active investment management is not particularly popular right now since passive strategies have outperformed. But I think that is getting ready to change. You should start, if you’re not already, investigating active management and more proactive investment styles. You will be much happier if you do.

Personally, I am still happily invested in a number of hedge funds but the strategies I select are limited, as many hedge fund styles have seen great challenges in producing acceptable risk/reward returns.

That is getting ready to change. I believe some hedge fund styles like the distressed debt, fixed income and event driven spaces are going to be very attractive. Who knows? Maybe even long/short funds will eventually find their former mojo.

At the economic event horizon, we all need to become black hole investors. Relying on past performance as the tectonic plates shift underneath us, as the central bank black holes begin to suck historical performance into their maws, we must look forward rather than backwards to design our portfolios.

At the event horizon, as the Jefferson Airplane song of my youth says, logic and proportion are fallen sloppy dead. You better feed your head with much more forward-looking strategies.

New York and Houston

Sunday I will fly to New York, meeting with old friends and new, and researching some management styles and managers, along with a few new biotech investments. Yes, my own personal focus is on biotech, and I do have a larger position of my personal portfolio in biotech stocks than I do in other areas. I should probably take a more holistic approach, but I actually give money to other managers who focus on different parts of the market, and spend more of my personal portfolio time on biotech. Ask me in 10 years if that was a good decision.

Tuesday night I get to be with Danielle DiMartino Booth on her birthday in New York, celebrating it with a number of our mutual friends. Danielle was Richard Fisher’s personal researcher at the Dallas Fed and now writes the must-read Daily Feather newsletter.

In one of the early Batman movies, the Joker says, “Where does he get all those wonderful toys?” I read The Daily Feather and I ask myself, “Where does she get all those wonderful stories and analogies?” And the data is truly a marvel.

I’ll be back in Puerto Rico on Wednesday afternoon, with meetings in San Juan before returning home to Dorado. Then the next Monday I will fly to Houston in the early evening. I will spend the next day with my partners at SMH (Sanders, Morris, Harris) going over strategies for clients and meeting with companies (yes, one might be biotech) and hopefully Texas barbecue for dinner. Then up early the next morning to go back to Puerto Rico.

Theoretically, I have no travel scheduled for the next month after that. But past performance suggests that something will happen to keep me from staying home for 30 days straight. We’ll see…

And with that, I will hit the send button. You have a great week and I hope you get to spend it with good friends and great conversation. It’s hard to get any better than that combination.

Your trying to figure out how I got old enough to get Social Security analyst,

John Mauldin

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits