Summary

- Central Banks Address Climate Change

- Clean Power Generates A Buzz

- Catastrophe Bonds in Demand

Mark Carney has a lot on his mind. As Governor of the Bank of England, Carney has to steer the British economy through the Brexit transition. With the terms and timing of Brexit still very much a mystery, setting an appropriate monetary course is a difficult task. As if that weren’t enough, Carney’s tenure at the Bank of England concludes in January 2020, so (unless his term is extended again) he’ll soon need to prepare a transition for his successor.

Across the pond, Robert Kaplan is president and CEO of the Federal Reserve Bank of Dallas. As a contributor to the Federal Open Market Committee, Kaplan helps determine the course of U.S. monetary policy. With the terms and timing of an agreement between the U.S. and China still unclear, this is no easy task. And if that weren’t enough, Kaplan’s district includes much of the American oil industry, which has had its highs and lows over the past several years.

Yet despite these full plates, both Carney and Kaplan have recently weighed in on an issue that might not immediately appear central to central banking: climate change. To some, this is an overreach; to others, it is directly on point.

We’ve written about climate change in the past. It remains a controversial topic; a recent YouGov poll revealed that segments of the world’s population do not accept the premise that the global climate is changing. Others acknowledge change, but are doubtful that human beings are responsible.

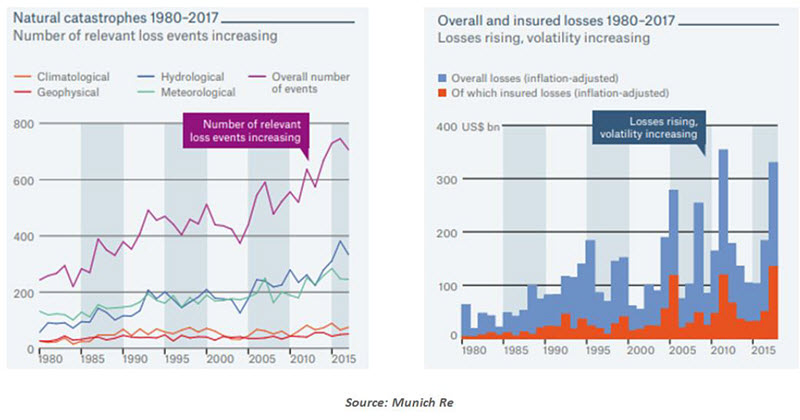

What is not in question is the steady increase in frequency of natural disasters over the past 40 years. Storms, floods and droughts have all increased in number and severity. The costs to insurers have escalated, as have the costs to society.

Catastrophic climatic events have changed the physical and commercial landscapes of the affected areas. As a result, the viability of residency and commerce in certain parts of the world has come under question. This, in turn, will have an impact on asset values and financial markets. That is why meteorological developments have become a concern for central banks, many of which view climate change as a threat to economic and financial stability.

“Climate change creates risks for the global economy and the global financial system.”

In the short run, losses created by natural disasters can affect credit quality and stress the reserves maintained by banks and insurance companies. Even if these losses can be absorbed, there may be a reluctance to provide credit and renew insurance policies to support the rebuilding process. Once bitten, twice shy.

As an example, mortgage analysts have called into question the wisdom of making thirty-year home loans along America’s Gulf Coast. The U.S. National Flood Insurance Program is pending renewal in Congress, with some legislators calling for an end to the government’s subsidy for loss-making flood insurance policies. And climate change has many countries rethinking the traditional practice of replacing and rebuilding in exactly the same spots.

Longer-term, the transition to a lower-carbon economy will diminish some industries and regions while promoting others. Storm threats will move people and production to higher ground. Inhospitable temperatures or a lack of potable water will also affect the geography of business operations. Global companies will have to place a premium on resiliency and location strategy.

These were the topics covered in Kaplan’s June research note. Just over two years ago, Texas was struck by Hurricane Harvey, one of the costliest storms in history. (Sadly, Tropical Depression Imelda is presently dumping immense amounts of rain on some of the same areas hit by Harvey.) Texas is also the locus not just of energy production but energy refining in North America, and those facilities are vulnerable to severe weather and rising sea levels. Longer-term, the lifeblood of the Texas economy (and other oil-producing regions) may need to change as the world strives to reduce reliance on fossil fuels.

These very tangible consequences are the entry point for central bank involvement. Central banks don’t have to take a position on whether climate change is a fact; the mere risk that global temperatures will continue upward should be factored into assessments of financial stability.

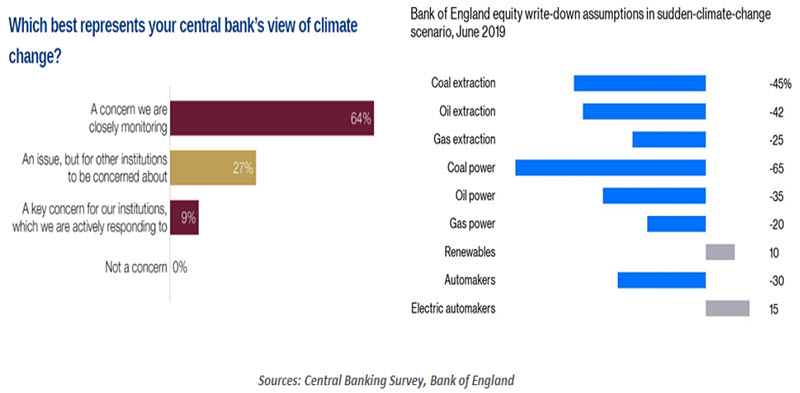

In an attempt to get out in front of potential consequences, a group of 34 central banks have formed the Network for Greening the Financial System (NGFS), which issued “A Call For Action” earlier this year. Among the recommendations forwarded were:

- Asking financial companies to assess, and stress test, their exposures to the short- and long-term consequences of climate change.

- Having central banks incorporate sustainability factors into the management of assets under their control.

- Facilitating the collection of data on climate-related risks.

- Broadening understanding of climate issues through research and conferences.

Mark Carney has been in the vanguard on this issue. In 2015, he gave a speech entitled “Breaking the Tragedy of the Horizon” that warned of the economic consequences of climate change. The Bank of England’s website has a whole section devoted to the topic. (By contrast, the European Central Bank and the U.S. Federal Reserve have been more measured in their approaches.)

“It is right and proper for central banks to engage on climate change.”

Carney’s focus on the topic has earned him no small measure of scorn. The Telegraph asked “Who Put Mark Carney in Charge of Our Climate Policy?” The Financial Times accused him of straying too far from the Bank of England’s mandate.

But the world is facing a rising risk of tail events, the costs of which could be immense. In similar low probability/high consequence situations, making an intelligent assessment and taking out insurance are routine. For that reason, central banks are justified in turning up the temperature on the topic of climate change.

Cleaning Up Our Act

While policymakers continue to debate climate change and energy policy, the markets are not waiting. Traditional economic incentives have promoted the adoption of more efficient fuels and technologies that are transforming the American power industry. On this front, the movement to a lower-carbon future is truly electric.

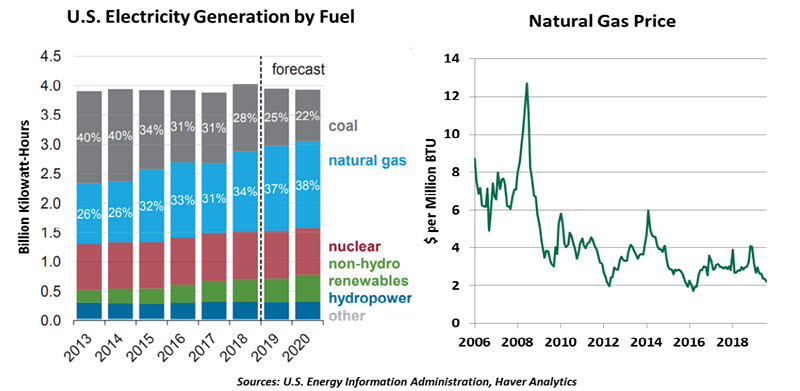

Coal is past its heyday. Though it is a polluting fuel, the move away from coal has been driven by economics more than environmentalism. Falling prices of natural gas and alternative energy technologies have made coal relatively expensive. The market is quickly moving away from coal, from 40% of U.S. electricity generation in 2013 to 28% in 2018, with further declines likely.

Natural gas is taking coal’s place in the near term. It is a byproduct of the hydraulic fracturing process that has changed the landscape of oil production in North America, leading to a supply glut that has kept its cost low. It can be moved through pipelines, a more efficient means than rail cars full of coal. Coal-burning plants are being converted to gas. Gas also burns more cleanly than coal, but it should not be considered a clean source of energy. Methane from oil wells and gas leaks is a potent greenhouse gas, while explosions and fires in the distribution network can be fatal.

Nuclear power carries many advantages: It runs at high capacity regardless of weather, and it produces no carbon emissions. However, nuclear plants are expensive to build and maintain. Spent nuclear fuel is small in volume but persistent in its danger. Nuclear plant development has slowed worldwide in response to fears of accidents and price competition from alternative energy sources. While fourth-generation plants have been proposed that would be safer and more economical, the appetite for building new plants is unlikely to return, leading to stasis in nuclear’s contribution to the U.S. energy mix.

Wind and solar are the greatest sources of energy capacity growth. They are maturing rapidly, and the cost of generating power from them is falling by the year. However, their ability to scale is not yet proven. Buildings with rooftop solar panels can meet most of their own electric needs during sunny days, but still rely on the electric grid at night and during cloudy weather. Wind farms work day and night but are only as powerful as the weather allows. Storage systems like batteries and pumped water reservoirs can help smooth the supply of power, but they are difficult to build at scale, and battery production brings its own environmental challenges. Open lands ripe for solar field and wind farm development are far from the urban centers that consume most electricity, requiring more investment in the power grid.

A further advantage of alternative energy sources is their higher efficiency. Two-thirds of the potential energy of conventional fuels is wasted as heat in the combustion process that turns motors and turbines. Alternative energy sources that do not produce heat are more efficient. In addition, much energy is expended to produce and transport fuels: mining and moving coal, digging oil and gas wells, refining crude oil, delivering gasoline. Moving to low-carbon electricity sources permits a reduction in the energy expended to bring energy to its final consumer.

“Market forces are helping to reduce pollution from energy generation.”

While the forms of electricity generation are shifting rapidly, we will not witness the end of the use of petroleum fuels. Batteries cannot rival the energy density of hydrocarbons, especially in applications like airplanes, cargo ships and long-distance trucks. Electric vehicles are promising for personal transportation but will not completely replace internal-combustion engines. Continued use of petroleum adds urgency to the adoption of low-carbon energy sources wherever possible.

Wind and solar generation already represented over 8% of U.S. electricity production in 2018, and long-run forecasts predict they will exceed 50% of global electricity capacity by 2050. The movement to clean energy is no longer a far-off dream. Change is literally in the air.

Hedging Event Risk

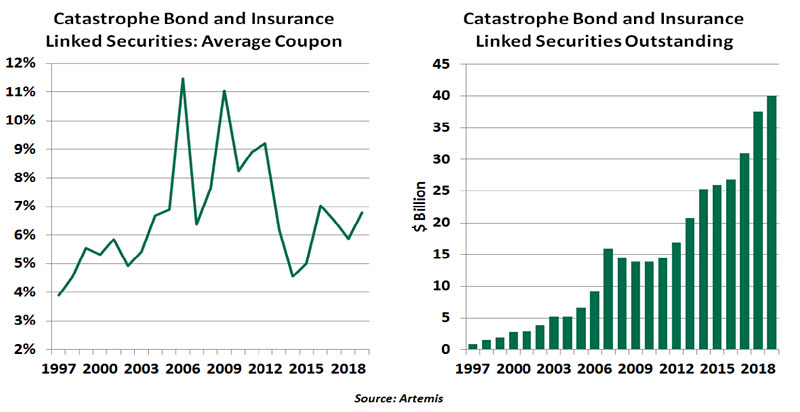

As discussed earlier, natural disasters are increasing in both their quantity and their intensity. Economic losses are growing, increasing the burden on insurance firms. But where many of us see risks, the insurance industry found rewards: Insurers created “catastrophe bonds” in the 1990s to alleviate some of their payout risks and sate investors’ appetite for high yields.

Catastrophe (or “cat”) bonds are insurance-linked securities (ILS) issued by an insurance firm that transfers a listed set of risks from a sponsor to investors. Cat bonds work quite simply: if no natural calamity occurs during its term, investors get back their principal along with relatively high yields. On the other hand, if a catastrophe occurs, investors’ principal is used to pay policy claims. The bonds are typically high-yielding, but are rated below investment grade. They are most often purchased by hedge funds and asset managers.

“Investors have an appetite for tail risk.”

The cat bond market is relatively small but growing. Investors see it a useful way of diversifying economic risk, since the market isn’t directly linked to broader financial market movements. That said, a cat-bond trust is only as safe as the investments made. And a flood of capital into the sector has depressed yields, much like the movements seen in the sovereign bond market. According to Artemis, the global cat bond and ILS market increased from $0.8 billion in 1997 to $40 billion in 2019. Around $14 billion of cat bonds were issued in 2018.

Insurance firms aren’t the only issuers in this market; some governments are also issuing cat bonds. The U.S. Federal Emergency Management Agency sold $300 million of cat bonds to balance likely payouts under the National Flood Insurance Program.

With the magnitude and frequency of natural catastrophes projected to increase, cat bondholders may be called upon more often to help satisfy claims. Thus far, cat bonds have remained in high demand, despite higher risk and lower yields. But as both the physical and investment climates change, buyers will have to exercise caution.

© Northern Trust

www.northerntrust.com

© Northern Trust

More Factor-Based Investing Topics >