Roundabouts, Not Crossroads

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIt has been challenging to keep up with the pace of breaking news in the past month. Political developments, trade provocations and an oil market disruption dominated the front page. In the background, though, the economy continues to function. Employment and wage gains are strong, but uncertainty about global growth prospects is clouding the outlook for business investment.

On balance, we expect the economy to transition into a period of moderate expansion amid elevated uncertainty. Economic growth will return to its long-run potential rate as the stimulative effects of tax reform and deregulation fade. Healthy consumer activity will be offset by slow business and export growth, and trade headlines will offer little reason for cheer. But slow, steady growth is still growth.

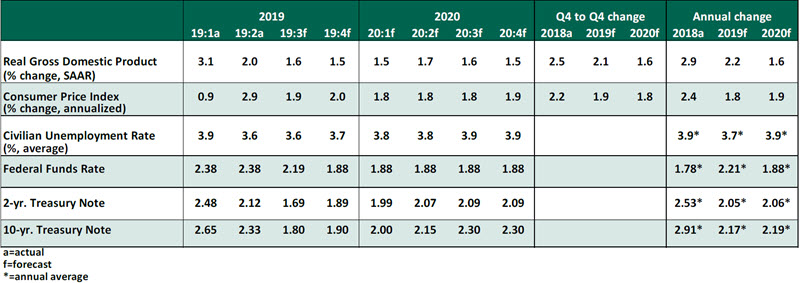

Key Economic Indicators

Influences on the Forecast

- Unemployment fell to a 50-year low of 3.5% in September. Job creation proceeded at a moderate pace; over the past three months, payroll growth has averaged 157,000. This level likely confirms the end of last year’s frenetic pace (the U.S. economy created an average of 223,000 jobs per month last year), but a downward movement is normal this far into an expansion cycle. The prime-age (25-54) labor force participation rate continues to hold at its cycle high of 82.6%. Wage growth fell slightly to 2.9% year-over-year, but the decline was not uniform: production and nonsupervisory workers saw wage gains of 3.5%. As long as wage growth outpaces inflation, we see support for continued strength in consumer spending.

- Commercial activity indicators are the greatest source of concern, with particular attention paid to the fall in purchasing managers’ indices (PMIs). The manufacturing PMI fell further into contraction in September with a reading of 47.8, a new low for the cycle. However, manufacturing represents only 11% of the domestic economy; the PMI has had past episodes of falling without heralding a recession. The services sector continues to show expansion albeit at a slower rate. The fall in activity reflects slow business investment, likely an outcome of trade tensions.

- Inflation measures reveal a mixed picture. The deflator on personal consumption expenditures (PCE) grew by 1.4% year over year in August. Core PCE (excluding food and energy) rose by 1.8%, demonstrating continued progress toward the Federal Reserve’s target of 2.0%. The consumer price index (CPI) displayed a similar trend, with the headline rate growing 1.7% (2.4% on a core basis).

- As widely expected, the Federal Open Market Committee (FOMC) cut the federal funds rate by 0.25% at its September meeting. Given a balance of low unemployment, recovering inflation and stasis in trade and other global growth concerns, we do not expect further rate actions by the Fed in the balance of 2019. Monetary policy works with a lag, and the two cuts thus far this year are still working their way through the economic system. Consumer activity has been a high point of economic news and needs no further stimulus.

Meanwhile, the uncertainty that is slowing business investment is caused by the trade outlook and cannot be cured by small changes to the cost of debt. The “dot plot” in the September Summary of Economic Projections revealed that no FOMC members are advocating a sustained reduction in interest rates.

- Long-term U.S. Treasury yields have been volatile, with yields on the 10-year bond varying from 1.47% to 1.90% in the month of September alone. Investors’ risk appetites have been difficult to predict, manifest in rapid changes to fixed income term premiums.

- Trade negotiations between China and the U.S. resumed, but with no breakthroughs. While the two-week deferral of the next tariff rate increase by the U.S. was a token of goodwill, the Commerce Department subsequently banned 28 Chinese companies from doing business with the U.S. due to concerns over human rights violations. Because each escalation complicates negotiations, we expect tariffs to increase as threatened and no deal to be found.

- The U.S. government has entered a new fiscal year without an approved budget. Absent a budget agreement, continuing resolutions will keep the government running, but the risk of added uncertainty from fiscal brinksmanship has grown.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All