SUMMARY

- Brexit: Close To the Finish Line

- What's Old Is New Again in Ireland

- The Future of Freddie and Fanniey

Last October, former British Prime Minister Theresa May was negotiating a deal with the European Union (EU) for a Brexit plan under which the United Kingdom would stay in a “temporary” customs union, but with no end date. That deal didn’t lead to Brexit, but rather Thexit – Mrs. May’s departure from high office.

One year later, current Prime Minister Boris Johnson has surprisingly secured a modified deal and has a decent chance of securing the legislative approval that eluded his predecessor. The timing of ultimate resolution remains somewhat uncertain, but recent developments must be viewed as encouraging for the U.K.

Last week, the U.K. and EU agreed to a reworked Withdrawal Agreement Bill (WAB). This outcome, which came less than two weeks before the current Brexit deadline, surprised many observers. Johnson, it was thought, was more interested in scoring political points by stressing differences with the EU than negotiating with them.

Johnson’s deal differs from May’s in that the U.K. will have no customs union with the EU, no “level playing field” arrangements and a more limited free trade agreement. Northern Ireland will become part of the U.K. customs territory rather than the EU customs area and will comply with certain EU rules. This will lead to regulatory and customs checks between Britain and Northern Ireland, but in the Irish Sea instead of at the land border. The WAB also guarantees the rights of EU citizens to stay, sets a £39 billion divorce bill and extends all EU laws through 2020.

“The current deal might be the least-worst solution to Brexit.”

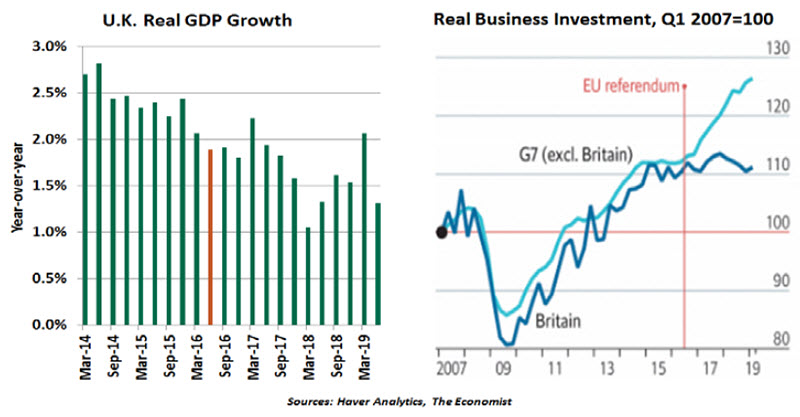

Many forecasters expected Brexit to plunge the country into recession. Even the government’s own 2016 study predicted a significant house price crash and a substantial rise in unemployment. Thankfully, those downside risks haven’t materialized. The economy has held up relatively well: the unemployment rate has dropped to a 25-year low while equity market returns have stayed positive. Only the pound has shown some weakness.

Despite this resilience, the uncertainty of Brexit has exacted undeniable costs. The U.K.’s gross domestic product (GDP) growth has slowed. Whether orderly or disorderly, Brexit will also disrupt supply and distribution chains as companies adapt to the new reality. London is already witnessing the relocation of financial services activities abroad, a body blow to one of the world’s biggest international financial centers.

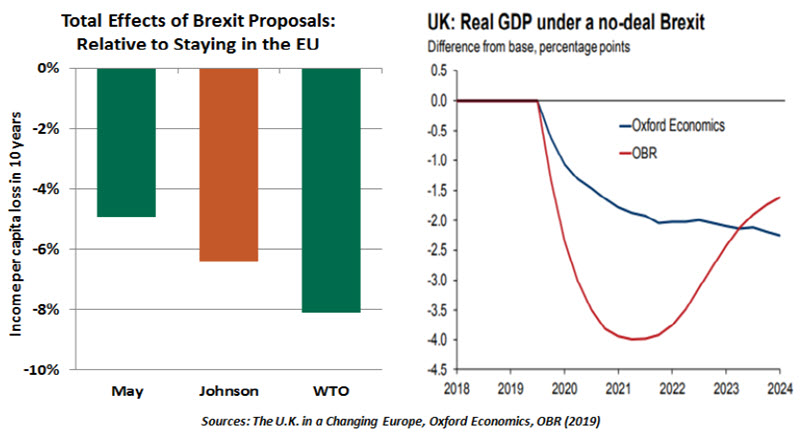

According to a study by The U.K. in a Changing Europe, Johnson’s Brexit deal would have a worse impact on British incomes than May’s proposal. Johnson’s proposed deal would reduce per capita GDP over ten years by 6.4% relative to the expected value if the U.K. remained part of the EU. That’s greater than the 4.9% loss estimated under Theresa May’s deal but less than the estimated 8.1% loss under a no-deal Brexit that would revert to World Trade Organization terms.

The key reason for these relative outcomes is trade. The EU is the largest British export destination, accounting for about 48% of its exports. Under the current proposal, the U.K. and the EU have agreed to tariff-free trade; but the non-tariff barriers in the Johnson deal will likely be higher than being part of a customs union. In a nutshell, the looser Britain’s ties are with the EU, the more economic performance will suffer.

It is not surprising that the current administration has rebuffed demands for a study of Brexit’s economic impact. Costs are casting a shadow on any benefits: the word “cost” is mentioned about 300 times in the government’s appraisal of the deal, compared to the word “benefit” featuring about 100 times. A report by the U.K.’s tax authority noted that introduction of customs checks would add £7.5 billion per year in administrative costs.

But it does bear noting that almost any deal between the U.K. and the EU would be better than no deal at all. The uncertainty and chaos created by an abrupt departure would have substantial short-term costs for both sides. The signing of an agreement would initiate a transition period until at least end of 2020, offering time to work out remaining details and avoid economic disruption. During the transition, the U.K. will have to establish new trade agreements with a number of other countries, which will not be an easy task: the scrutiny trade is getting around the world will make negotiations difficult.

From the European standpoint, the impact of the proposed deal will likely be far smaller. But with the European economy already struggling amid external trade uncertainties, reducing the tail risk of a “no-deal” Brexit is a good outcome.

“There is still a lot of uncertainty over how (and when) parliament will implement the new deal.”

The Brexit process is edging forward, with new developments daily. Per legislation passed earlier this year, Boris Johnson was forced to ask the EU for an extension of the negotiating deadline; it appears that January 31 will be the updated exit date. The proposed deal could still be ratified before the October 31 deadline (or shortly thereafter). In the alternative, elections could be called and concluded in the next couple of months, which would delay ratification. In either case, lots of parliamentary maneuvering is expected.

Brexit has damaged the reputation of the U.K. as a stable place for business. But while remaining a full EU member would produce the best projected economic outcomes, the proposed arrangement might be the best that Britain can hope for.

In one of the lowest moments of World War II, Winston Churchill attempted to rally public sentiment by characterizing the situation as “the end of the beginning.” While commerce is not war, we may be at a similar juncture with Brexit.

Time Is a Great Storyteller

Old problems are finding new life in Ireland. To read Irish history is to be immersed in a stream of misfortune. The country’s modern history is marked by decades of famine, wars and civil unrest.

Ireland formally joined the United Kingdom in 1801, but the union was not to last. Irish organizers fought the Irish War of Independence in 1919-1921. Though Britain conceded, six counties in the northeast preferred to stay within the U.K., forming today’s Northern Ireland. Meanwhile, disagreements over the terms of the departure treaty led to civil war in the new Irish Free State.

Then, starting in the 1960s and continuing for 30 years, the Troubles played out in and around Northern Ireland, with continual confrontations between those loyal to the U.K. and those seeking to unify Ireland. The Good Friday Agreement, which ended the Troubles in 1998, is a recent memory.

These conflicts had themes that continue today. Foundationally, they were arguments over whether to remain in a larger alliance and how to withdraw from it, just as with today’s Brexit. And in hindsight, these disputes had no clear solution: Ireland could have survived intact as a country in the U.K., or as a unified independent state. Partitioning the island was a compromise.

“The conflicts that created today’s Ireland have found new life in Brexit.”

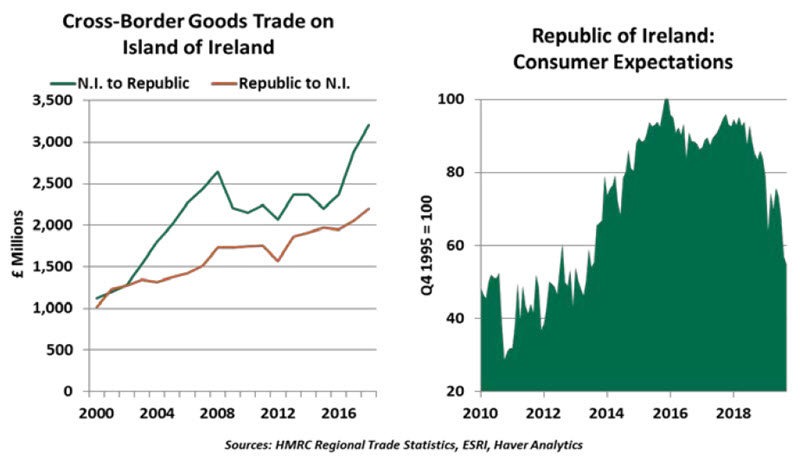

Skepticism endures, as 56% of Northern Ireland residents voted to remain in the EU; only Scotland and London had greater shares voting to remain. People, goods and capital flow freely across today’s soft border, to mutual benefit. Forecasted employment growth in the Republic of Ireland is much stronger than that in Northern Ireland, while the North is a regional tourism destination.

The Good Friday Agreement contained a provision for a future vote to unify the island. There has not yet been a strong push to reunite Ireland, given the long history of tension around the issue. But polls show growing support for reunification. A bad Brexit could force this issue to a head.

The Irish people take pride in being lighthearted and celebratory, whatever the circumstances. (For illustration, visit an Irish-American funeral.) Today’s Irish residents are steadfast in not allowing their border to lead to new troubles. We are confident they will find a solution.

Back To BAU?

The anniversary of the 2008 economic crisis barely merited mention this year. The decade-after retrospectives we got last year were pretty comprehensive, so perhaps there was nothing much more to say. And many would prefer to close the books on the whole episode.

Almost all of the U.S. government support programs crafted during the crisis were closed long ago. ProPublica estimates they have produced a profit of $116 billion for American taxpayers. One chapter from that era has not yet concluded: the bailout of the American mortgage agencies, Freddie Mac and Fannie Mae. But there may be movement on this front: recent proposals would return the two companies to their shareholders.

Fifteen years ago, underwriting standards in the American mortgage market were declining rapidly. At the same time, government-sponsored enterprises (GSEs) like Freddie and Fannie began increasing their underwriting of securities containing risky mortgages. And during intervals when these securities were hard to sell, Freddie and Fannie kept them on their balance sheets.

Whereas private institutions would be expected to hold a reasonable amount of capital against those holdings, the GSEs were required to hold very little. Private firms are constrained in their activities by the availability of liquidity to fund their operations; Freddie and Fannie had a credit line from the U.S. Treasury, which was a valuable backstop. The GSEs were allowed to take a lot of risk; their shareholders profited if things worked out, but the public was on the hook if they didn’t.

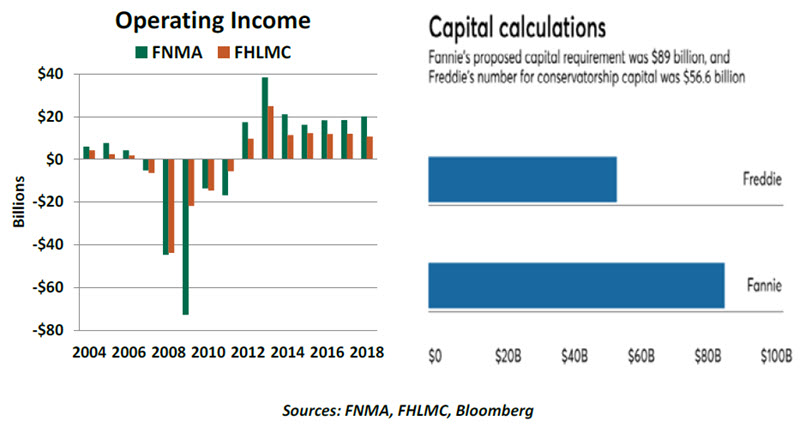

When housing values cracked and mortgage defaults mushroomed, Freddie and Fannie came under immense pressure. In early September of 2008, the two companies were placed into conservatorship by the U.S. government, where they remain today. The use of conservatorship avoided a bankruptcy, which would have been chaotic for the global financial system. And it gave the government time and space to determine what to do with the two behemoths.

Ultimately, the U.S. government invested about $190 billion to keep Freddie and Fannie afloat. In an effort to recoup that investment, Congress decided to add all of Freddie and Fannie’s profits to the Treasury, a move that has produced $245 billion in revenue since 2012. That cash flow may be one reason why progress on GSE reform has been slow.

During the past decade, there have been proposals to return some of what Freddie Mac and Fannie Mae do to the private sector. Investment banks certainly have experience forming and distributing asset-backed securities. But some legislators worry that the supply and cost of mortgage credit would increase in this model, putting housing further out of reach for middle-class families.

“Returning GSEs to their former states without reform is a bad idea.”

After all the policy debates, though, the administration seems to have settled on letting the GSEs carry on as they were. Recent proposals would allow Freddie and Fannie to begin retaining their earnings to build sufficient capital to support their activities. This might take some time, given estimates that the two firms would need well over $100 billion in capital to operate properly.

At some point, the companies would be returned to their shareholders, with only minor alterations to their charters. The companies would continue to have access to the Treasury as a liquidity backstop. These outcomes would have been unthinkable ten years ago.

Housing is an important industry for the United States, and the GSEs play a useful role in making credit available to prospective homeowners. But a healthy housing industry is a stable housing industry, less prone to the excesses of fifteen years ago.

Having Freddie and Fannie in conservatorship for all this time afforded an opportunity to make meaningful reforms. Disappointingly, the government appears inclined to give us more of the same.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

© Northern Trust

More Factor-Based Investing Topics >