The Opportunities Go to Those Who Can See Past the Negative Headlines

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

“Follow the trend lines, not the headlines.”

The quote, attributed to former President Bill Clinton, is one of my favorite pieces of advice. Clinton was referring to long-term data that show that conditions have actually been improving for the human race despite popular opinion to the contrary. When applied to investing, it cautions against missing opportunities because you’re too busy reacting to negative news.

To be sure, there’s more than enough negative news right now: international trade tensions, volatility in Syria, Brexit, impeachment and much more.

As I’ve said before, I happen to be a news junkie. The U.S. Global Investors office has a number of TVs, all of them tuned to financial news networks. I constantly urge everyone on our team to stay informed and raise their awareness of what’s happening around the world and in their communities.

But this alone doesn’t guide our investment decisions. If we based everything on what the talking heads tell us, we may never have the confidence to invest so much as a dime.

Instead, we focus on fundamentals such as moving averages and standard deviation. We follow leading indicators such as the purchasing manager’s index (PMI) and consumer confidence index. These factors are many times more effective than the headline news at shining a light on the right path.

Mike Matousek, head trader at U.S. Global, has a colorful saying that complements this idea: “It doesn’t matter if they make jelly beans or trash can lids, if a stock’s going up, you want to own it.” And conversely: “If it’s going down, you don’t want to own it.”

Did You Catch These Opportunities?

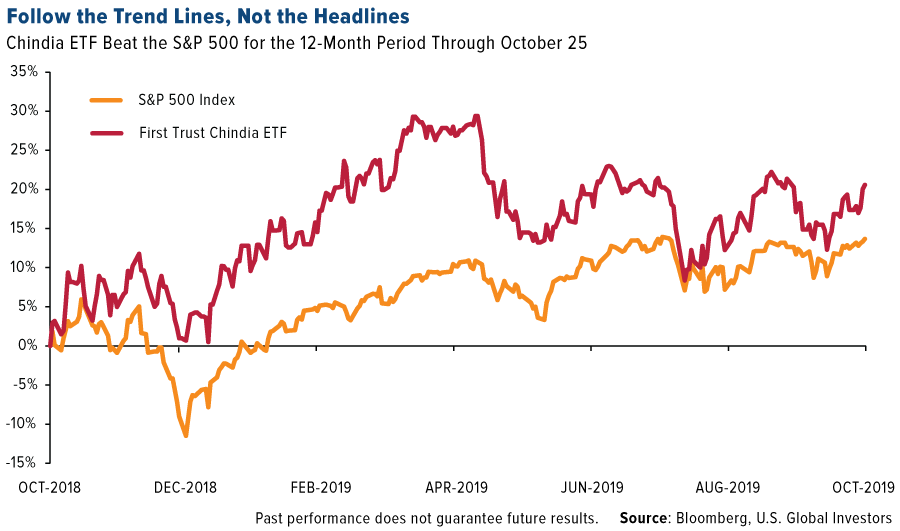

Let me give you some real-world examples of what I’m talking about. A lot of the news coming out of China right now is negative. Its economy is slowing. Tariffs are hurting trade. The Hong Kong protests are causing geopolitical pressure. It’s enough to make an investor run and hide.

Which would be a mistake. Take a look at the chart below. The First Trust Chindia ETF, which invests in companies in both China and India, is up more than 20 percent for the 12-month period through October 25. That’s enough to beat the S&P 500 over the same period.

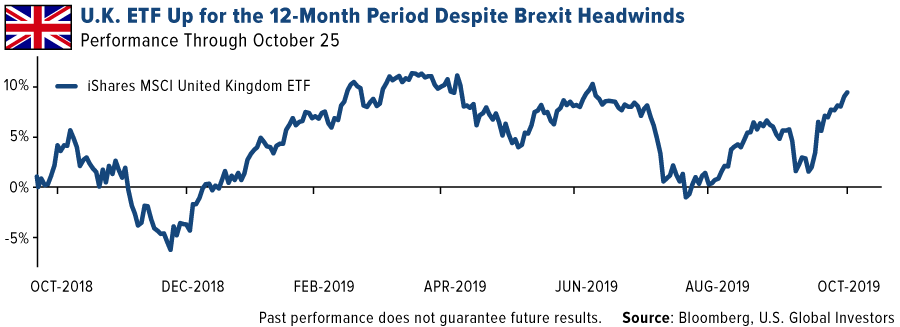

Or consider British stocks. You might think that Brexit uncertainty has made investing in the U.K. a nightmare. And yet the opposite seems to be the case—the iShares MSCI United Kingdom ETF is up close to 10 percent for the 12-month period.

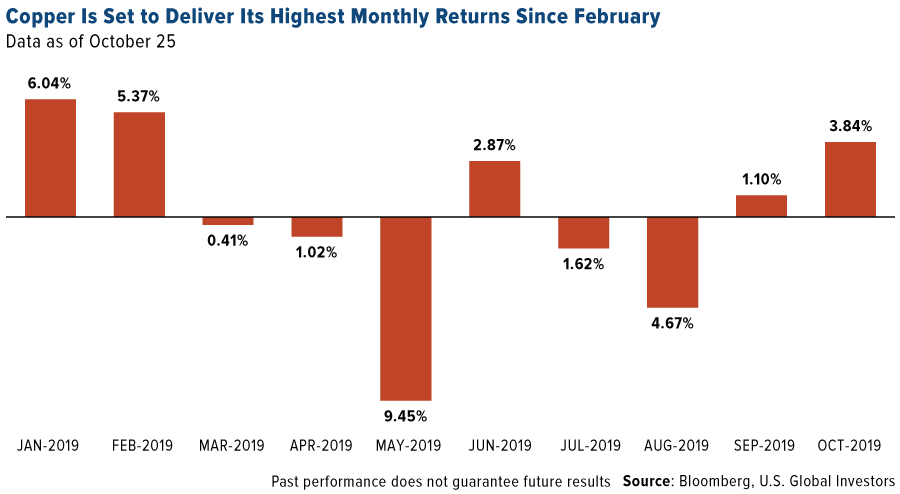

Another good example are the recent copper strikes in Chile. In this case, bad news is actually good news. With production halted for days at Chuquicamata, the world’s largest open pit copper mine by volume, global supply could be disrupted, which may push up prices. Due in part to the strikes, copper is on track for its second straight month of positive gains and its best month since February.

Keeping an Eye on the PMI

Again, one of our favorite leading indicators is the manufacturing purchasing manager’s index, or PMI. The gauge compiles data from thousands of factories and manufacturers across the globe, measuring data points such as output, new orders and employment. At the beginning of every month, we get a number that reflects the health of the industry.

The higher the number is above 50.0, the faster factories are expanding their business. The lower the number is under 50.0, the faster they’re shrinking.

September’s PMI was 49.7. That’s in contractionary mode, but because it’s up slightly from August’s 49.5, factories are pulling back at a slower rate.

We won’t know what the PMI is for October until late next week, but if it shows that we’re back to a neutral 50.0 (or better), it could mean good things going forward for energy and commodities.

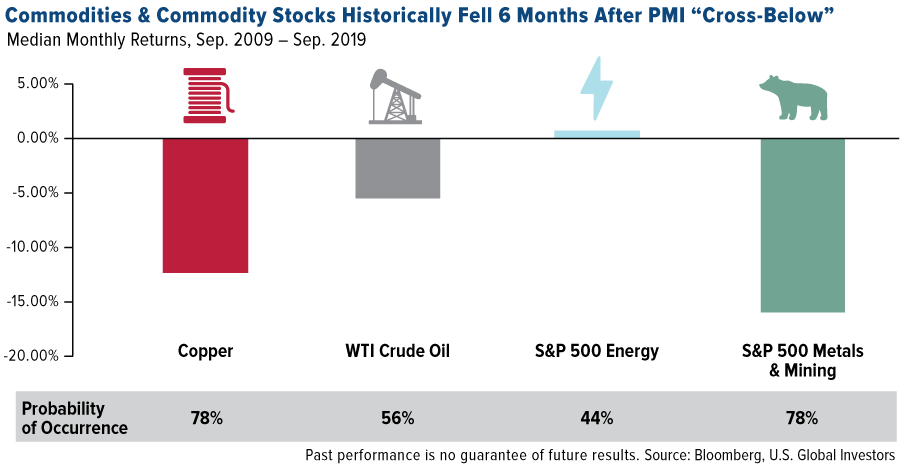

According to our own research going back 10 years, when the global manufacturing PMI rose above its three-month moving average, commodities and commodity stocks appreciated six months later. Copper, for instance, gained an average of around 10 percent, with a 71 percent probability of occurrence. West Texas Intermediate (WTI) oil returned about 5 percent. And so on.

Conversely, when the PMI fell below its three-month moving average, materials historically declined—or, in the case of energy, was essentially flat—six months later.

Again, these results are based on 10 years’ worth of data. We’re hoping for a stronger PMI for the month of October, which would help give commodity prices and mining stocks an extra shot of momentum going forward.

Gold Market

This week spot gold closed at $1,504.67, up $14.82 per ounce, or 0.99 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 2.00 percent. The S&P/TSX Venture Index came in up 0.57 percent. The U.S. Trade-Weighted Dollar rose 0.56 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct-24 | Hong Kong Exports YoY | -7.00% | -7.30%` | -6.30% |

| Oct-24 | ECB Main Refinancing Rate | 0.00% | 0.00% | 0.00% |

| Oct-24 | Durable Goods Orders | -0.70% | -1.10% | 0.20% |

| Oct-24 | Initial Jobless Claims | 215k | 212k | 214k |

| Oct-24 | New Home Sales | 702k | 701k | 713k |

| Oct-29 | Conference Board Consumer Confidence | 128.0 | -- | 125.1 |

| Oct-30 | ADP Employment Change | 125k | -- | 135k |

| Oct-30 | GDP Annualized QoQ | 1.60% | -- | 2.00% |

| Oct-30 | Germany CPI YoY | 1.10% | -- | 1.20% |

| Oct-30 | FOMC Rate Decision (Upper Bound) | 1.75% | -- | 2.00% |

| Oct-31 | Eurozone CPI Core YoY | 1.00% | -- | 1.00% |

| Oct-31 | Initial Jobless Claims | 215k | -- | 212k |

| Oct-31 | Caixin China PMI Manufacturing | 51.0 | -- | 51.4 |

| Nov-1 | Change in Nonfarm Payrolls | 90k | -- | 136k |

| Nov-1 | ISM Manufacturing | 49.0 | -- | 47.8 |

Strengths

- The best performing metal this week was platinum, up 3.96 percent. Gold is back with a weekly gain and its best week in five, trading above $1,500 an ounce on hopes that the Fed will cut borrowing costs next week. The yellow metal also benefitted from haven demand due to geopolitical turmoil from Chile to Lebanon, plus volatility surrounding Brexit negotiations. Holdings in gold-backed ETFs have increased 16 percent so far this year. On Monday alone, ETFs added 82,176 troy ounces of gold to their holdings, according to data compiled by Bloomberg. Silver also had a strong week, up 2.79 percent on an improved industrial demand outlook, reports Kitco News.

- In a big surprise, Germany’s central bank bought gold for the first time in 31 years. Reserves climbed to 108.34 million ounces in September, up from 108.25 a month earlier, and the first change since 1988. International Monetary Fund data shows that Turkey also increased reserves in September, rising to 17.29 million ounces from 16.49 million ounces a month earlier.

- Several miners reported strong third quarter results this week. Agnico Eagle Mines beat expectations and reported quarterly net income of $76.7 million, up significantly from the same time last year of $17.1 million in net income. The company said it had record gold production of 476,937 ounces. Hochschild Mining also reported stronger production, with output rising 9 percent in the third quarter to 67,797 ounces. Yamana Gold reported net free cash flow of $99.9 million due to higher gold prices and declared a fourth quarter dividend of $0.01 per share, which is a 100 percent increase.

Weaknesses

- The worst performing metal this week was palladium, up 0.60 percent. Pre-Diwali sales of gold and silver in India fell as much as 40 percent as high prices and lower consumer spending hits, reports the Economic Times. The Confederation of All India Traders (CAIT) said “there was a decline of business from 35 to 40 percent which is a cause of major worry for the traders.” Falling demand out of India is a concern, as it is the world’s second largest consumer of gold.

- Joe Foster, portfolio manager and strategist at VanEck, says that market complacency is to blame for disrupting gold’s rally. In a phone interview with Bloomberg, Foster said “until the market loses that complacency and there’s less risk sentiment, that’s when gold really takes off.” Foster says we’re at the point of a potential full blown recession and that “something’s got to give at some point.” Bloomberg’s Sungwoo Park is bearish on gold in the near-term, writing that “the metal will struggle to find a way back up from here for some time” due to rising real yields, which reduce the appeal of non-interest paying bullion.

- As some miners reported strong third quarter results, others disappointed. Fresnillo Plc reported a fall in output in the third quarter due to lower grades, saying that silver production fell 14.5 percent and gold production fell almost 7 percent. Glencore reported a 4 percent drop in copper output so far this year and trimmed its full-year guidance as it plans to suspend some operations in the Democratic Republic of Congo.

Opportunities

- Calibre Mining Corp., which bought two gold mines in Nicaragua from B2Gold Corp., was added to the S&P/Toronto Stock Exchange Composite Index, reports Bloomberg News. Company executives are hoping to build “a profitable, ETF-qualifying gold business that generates significant free cash flow.” B2Gold has a 31 percent equity ownership stake in Calibre.

- The World Gold Council (WGC) published a report this week highlighting the gold sector’s carbon footprint and steps the industry can take to become net-neutral. Chief Financial Officer Terry Heymann says “it’s not an easy path right now but it’s feasible for mining companies to play their role and operate with net-zero emissions. It’s only going to get easier as technology advances.” The report highlights the cheaper costs of green energy and that in some cases diesel generation products can be more volatile in price. Several companies have announced green initiatives at mines and often highlight what they’re doing to combat climate change in presentations to investors.

- Sprott Inc. CEO Peter Grosskopf says this time gold’s rally is different because monetary policy has reached the point of being ineffectual. “Gold’s 2019 performance is quite different than prior rallies in that the gold market is no longer small and gold is no longer seen as a fringe asset.” Grosskopf added that “the Fed is in checkmate and gold is now a mandatory” portfolio holding. Australia & New Zealand Banking Group is also bullish on the yellow metal, saying that it could hit $1,700 an ounce in the next six months, citing expected changes in U.S. interest rates.

Threats

- The House Natural Resources Committee voted on Wednesday giving preliminary approval to update a 147-year-old hardrock mining law that was signed by President Ulysses S. Grant in 1872. The Hardrock Leasing and Reclamation Act would protect national parks and tribal areas from being leased for mining, increase mining royalties and create a fund to clean abandoned mines. Bill proponents say it brings mining into the 21st century, while critics say that it will do major harm to mining companies. Cronkite News reports that the bill would impose a minimum 8 percent royalty on mineral production at already existing mine sites and a 12.5 percent royalty on mines with permits issued after the law takes effect.

- Bloomberg’s Katherine Doherty reports that it’s beginning to look a lot like 2009 based on a key indicator of credit. According to S&P Global Ratings data, upgrades of U.S. companies in the high-yield market are trailing downgrades by the most since 2009. Plus, the number of risky credits is on the rise and hit a 10-year high in September with 263 companies rated B- or lower.

- Violent anti-government demonstrations and work strikes in Chile are disrupting the mining industry. Chile, the world’s largest copper producer, is facing delays and supply shortages at many of its mines. Antofagasta Plc, which has four mines in the country, said it could cut its production by 5,000 tonnes. Reuters reports that several of the world’s largest miners, such as BHP Group, Anglo American and Teck Resources, have operations in the nation that also mines gold and silver.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.70 percent. The S&P 500 Stock Index rose 1.24 percent, while the Nasdaq Composite climbed 1.90 percent. The Russell 2000 small capitalization index gained 1.54 percent this week.

- The Hang Seng Composite lost 0.16 percent this week; while Taiwan was up 1.04 percent and the KOSPI rose 1.32 percent.

- The 10-year Treasury bond yield rose 4 basis points to 1.799 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing by 4.33 percent compared to an overall increase of 1.22 percent for the S&P 500 Index.

- Biogen was the best performing stock for the week, increasing 30.89 percent.

- The S&P 500 climbed past its all-time closing record Friday, rising 0.5 percent to 3,026. Technology firms paced the final leg higher after Intel’s upbeat forecast. The benchmark for American equities last closed at a record on July 26.

Weaknesses

- Real estate was the worst performing sector for the week, decreasing 1.11 percent.

- Twitter was the worst performing stock for the week, falling 22.29 percent.

- Amazon took a nosedive after reporting a less profitable quarter than expected. Amazon reported third-quarter earnings on Thursday, missing Wall Street estimates on profit — sending the stock tumbling as much as 8.62 percent after the release.

Opportunities

- Walmart has launched an in-home delivery service where customers can have items delivered directly to their fridge when they're not at home. Walmart workers gain access to customers' homes using smart-lock technology controlled from a mobile phone.

- Google scientists claimed a massive breakthrough in cutting-edge computing with “quantum supremacy.” Google scientists ran an experiment to demonstrate just how much faster quantum computers would be compared to today's computers.

- German flying-taxi startup Lilium said it has taken a big step toward providing intercity rides for $70. Lilium has demonstrated that its electric jet can take off vertically and then move into "level flight" — flying forward — and hit speeds of up to 62 mph.

Threats

- HSBC is reportedly planning to axe 10,000 jobs amid a brutal year for global bank workers. The Financial Times reported that most of the jobs being cut will be at the higher levels of the bank.

- WeWork's IPO woes are bleeding into the biotech market — and health startups’ plans to go public now look dimmer. M&A bankers say the WeWork debacle is part of what's weighing on health firms’ IPO plans.

- Takeover volumes since the start of September have fallen to the lowest level in eight years, according to data compiled by Bloomberg. The U.S. Labor Day holiday is typically the start of fall dealmaking, so that’s left bankers to worry whether CEOs will be able to shrug off the year’s anxieties and again consider transactions. “Clearly we’re seeing a bit of softness in the M&A market,” said Dusty Philip, co-head of global of mergers and acquisitions at Goldman Sachs Group Inc. “There has been a marked increase in market volatility that started in August, and we’ve also seen somewhat weaker levels of corporate confidence. There’s real uncertainty related to trade and politics with both Brexit and the U.S. election.”

The Economy and Bond Market

Strengths

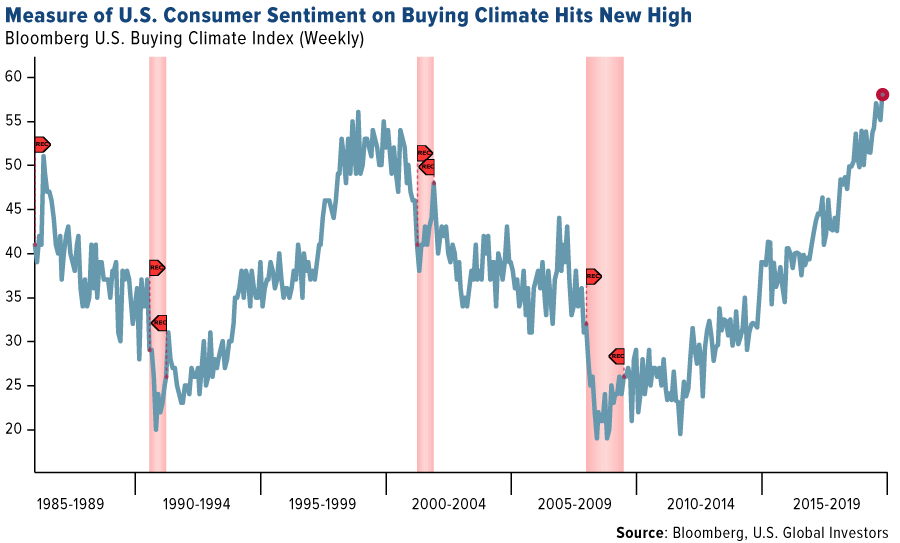

- A gauge of buying conditions in the U.S. advanced last week to a fresh high, according to Bloomberg Consumer Comfort Index data. The purchasing climate figure indicates a strong labor market, income growth and low inflation will help keep consumers spending and could provide comfort to retailers ahead of the holiday shopping season.

- According to the IHS Markit Purchasing Managers' Index (PMI) report for October, economic activity in the manufacturing sector expanded at a more robust pace than expected with the Manufacturing PMI coming in at 51.5 and beating the market expectation of 50.7.

- The number of people who applied for U.S. jobless benefits in mid-October fell slightly and clung near a 50-year low, showing the resilience of strong labor market that has held up remarkably well in the face of a slowing economy. Initial jobless claims, a rough way to measure layoffs, fell by 6,000 to 212,000 in the seven days ended October 19. Economists polled by MarketWatch estimated new claims would total a seasonally adjusted 215,000.

Weaknesses

- Orders placed with U.S. factories for business equipment declined for a second straight month and shipments matched the biggest drop since 2016, the latest sign the dimmer global growth outlook and trade tensions with China are weighing on companies. The proxy for business investment – booking for non-military capital goods orders excluding aircraft – fell 0.5 percent in September after a downwardly revised 0.6 percent drop the prior month, according to Commerce Department figures. The broader measure of bookings for all durable goods declined 1.1 percent, the most since May and also below forecasts.

- Home sales fell more than expected in September as the market continues to struggle with a dearth of properties for sale, especially for cheaper homes. The National Association of Realtors said on Tuesday that existing home sales fell 2.2 percent to a seasonally adjusted annual rate of 5.38 million units last month, reversing two straight months of gains.

- Consumer sentiment dipped to 95.5 in October, coming in just below the prior reading and Street estimate of 96. Consumers surveyed by the University of Michigan have repeatedly expressed concern about trade tensions, which have resulted in billions of dollars in tariffs on consumer goods.

Opportunities

- It’s going to be an action-packed week next week, with preliminary GDP data for the third quarter hitting the markets on Wednesday.

- Also on Wednesday, the Fed will conclude its policy meeting where investors will tune into Chairman Powell’s remarks to get an update on the Fed’s perspective of the economy. The Fed is virtually certain to cut rates for a third consecutive time, with investors assigning a 90 percent probability for such an action. Thus, the market reaction will depend mostly on the signals policymakers send about the likelihood of future action, not on the rate cut itself.

- Personal income and spending figures will follow on Thursday where American consumers are expected to continue spending at a solid pace.

Threats

- The core PCE price index for September will be released on Thursday. Prior weak inflation readings continue to pose challenges to a robust expansion.

- The nonfarm payrolls report for October will be released on Friday. A more modest pace of job creation is expected at 90,000 new jobs.

- Last but not least, the ISM manufacturing PMI will attract significant attention given the hardships faced by the sector amidst the trade war.

Energy and Natural Resources Market

Strengths

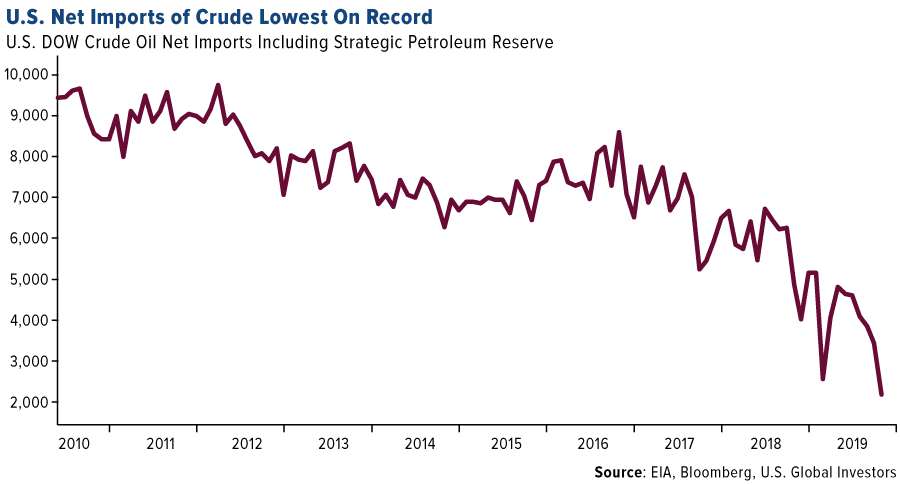

- The best performing major commodity for the week was crude oil, which gained 5.37 percent. Oil rallied above $55 a barrel for the first time in three weeks on Wednesday after data showed a surprise drop in U.S. crude stockpiles. The Energy Information Administration reported inventories fell by 1.7 million barrels last week and that imports of foreign crude slumped to the lowest in more than two decades. The data signaled strengthening demand for the fuel.

- Bloomberg Businessweek reports that California will become the first state to require almost all new homes to draw some power from the sun starting in 2020. Solar already makes up about one-seventh of electricity supply in the state and leads the U.S. in home solar panels. BHP Group has signed contracts to power two of its giant Chilean copper mines completely on renewable power – a giant shift showing that top miners are under pressure from investors to cut emissions.

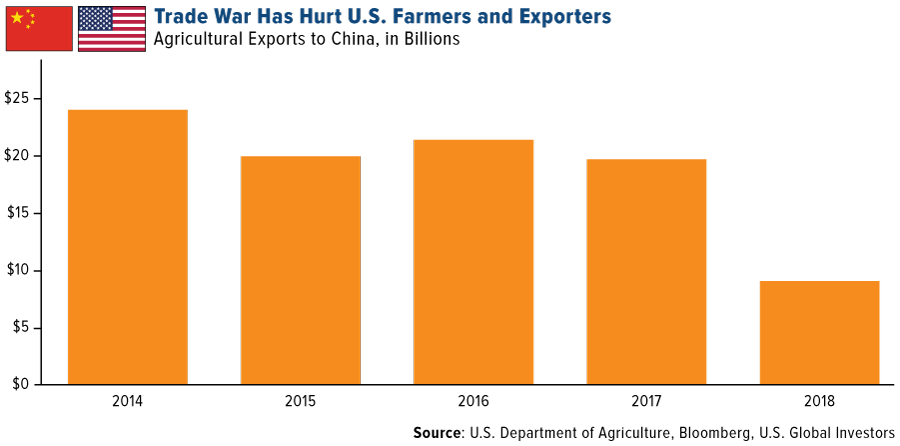

- Positive news emerged this week in the trade war. President Trump said that negotiations on an initial trade deal are advancing and raised expectations of an agreement next month. China said that it will aim to buy at least $20 billion of agricultural productions in a year if there is a deal signed. U.S. Department of Agriculture data show that the trade war has significantly hurt farmers and exporters, with less than $10 billion of exports to China last year. An end to the trade war could support stronger global demand for commodities.

Weaknesses

- The worst performing major commodity for the week was iron ore, which fell 6.78 percent. The London Metal Exchange (LME) has begun an inquiry into nickel trading following the biggest-ever decline in inventories. Bloomberg reports that since mid-September about half of all the nickel in LME warehouses has been withdrawn and spot contracts have traded at the biggest premium to futures in 12 years. The metal is down 10 percent since reaching multi-year highs last month.

- Caterpillar Inc. fell after the company cut its earnings forecast for 2019 and reported the first decline in quarterly profit in almost three years. The company, which is the world’s largest maker of mining and machinery equipment and often looked at as a bellwether of the overall economy, said sales fell 5.2 percent and that it expects fourth quarter demand to be flat. Caterpillar CFO Andrew Bonfield said “most of our customers who buy goods are making large purchasing decisions and when there is global uncertainty, uncertainty in the economic outlook, they probably defer making those decisions.”

- California is facing more blackouts as power companies work to keep falling power lines from igniting wildfires. More than half a million people across the state lost power on Thursday, reports Bloomberg. Edison International and Sempra Energy increased outages to more than 34,000 homes and business nears Los Angeles and San Diego as winds move south. A fire broke out in Sonoma County on Thursday and PG&E told regulators that one of its transmission lines went down minutes before the fire started. The company, which was responsible for massive fires last year, saw its shares fall 12 percent.

Opportunities

- According to the head of the International Seabed Authority (ISA), China is likely to become the first country in the world to start mining seabed minerals if the international rules for exploitation are approved next year, reports Reuters. The ISA has signed 30 contracts with governments, research institutions and commercial entities for exploration, and China has five of those. It would still take two to three years to obtain permits to start deep sea mining and it is still unknown if it will be cost-effective to explore for seabed minerals such as nickel, copper, cobalt and manganese.

- Rio Tinto Group has started pilot production of lithium in California and will consider an expansion to become the top domestic supplier. The company said in a statement that work to reprocess waste piles from a 90-year-old mining site successfully produced lithium carbonate, which is needed in rechargeable batteries for electric vehicles. Bloomberg reports that Rio is the first top diversified miner to add lithium output to its portfolio.

- Hoffmann Green Cement Technologies went public on the Paris exchange this week with a big promise to shake up global production of cement and reduce carbon emissions. Cement manufacturing has a big carbon footprint and is responsible for about 7 percent of carbon emissions, which is more than all trucks on the road. The new company aims to change the composition of cement so that it no long containers clinker, which is the main source of emissions.

Threats

- Chile, the world’s top copper-producing nation, has been rocked by violent protests, anti-government demonstrations and worker strikes. Mining unions have called for worker stoppages as they call for the government to withdraw the state of emergency and listen to demands, reports Bloomberg. Although a reduction in supply due to strikes could support higher prices, it spells bad news for mining companies. Antofagasta Plc, which has four mines in the country, said it could cut its production by 5,000 tonnes.

- Singapore’s minister for the environment and water resources said that climate change is the defining issue of our times and that a strong response is needed. Masagos Zulkifli said “our weather is getting warmer, our rainstorms heavier, and dry spells more pronounced.” Singapore is a land-scarce and low-lying city and is going to try and find room for more than a quarter of a million new trees and shrubs to step up measure to combat climate changes, reports Bloomberg News.

- Russia hosted the first-ever Russia-Africa summit this week that was attended by 43 of Africa’s 54 countries. President Vladimir Putin has been pushing for greater influence in the region and Russia has doubled its annual trade with Africa in the last five years to exceed $5 billion. Reuters reports that Russia has signed military cooperation agreements with at least 28 African countries and that it’s geological survey agency has signed agreements with South Sudan, Rwanda and Equatorial Guinea to search for carbon resources. Although new resource development is positive, it’s a threat to the U.S. in potentially losing access to the continent’s vast resources.

Emerging Europe

Strengths

- Russia was the best performing country this week, gaining 4.4 percent. European stocks performed well this week after Boris Johnson, Prime Minister of Great Britain, was able to pass his new Brexit deal in the parliament and the chance for U.K. exiting the eurozone without a deal declined. Russian oil and gas stocks outperformed this week, with Surgutneftegas common shares gaining 30 percent in the past five days.

- The Turkish lira was the best performing currency this week, gaining 30 basis points against the U.S. dollar. Improving geopolitical developments lifted the country’s currency despite the central bank cutting its main rate by 250 basis points on Thursday.

- Energy was the best performing sector among eastern European markets this week. Surgutneftegas, a Russian gas producer and distributor, was the best performing equity, gaining 30 percent over the past five days.

Weaknesses

- Poland was the worst relative performing country this week, gaining only 50 basis points. Polish banks sold off. Alior Bank lost 20 percent of its market share in the past five days, after the bank announced the implementation of the Court of Justice of the European Union (CJEU) ruling on early loan repayments, which will have a negative effect on third and fourth quarter results. Alior Bank is the most exposed in the sector to the risks posed by the CJEU judgment.

- The Hungarian forint was the worst performing currency in the region this week, losing 1.6 percent. The central bank left its main rate unchanged at 90 basis points and maintained its view of downside risks to inflation.

- Consumer staples was the worst performing sector among eastern European markets this week. Dino Polsak, a Polish food retailer, was the worst preforming equity, losing 6 percent in the past five days.

Opportunities

- With the geopolitical situation improving in Turkey, shares trading on the Istanbul exchange could bounce. President Putin and Erdogan met in Sochi this week and both agreed to work together in Northern Syria. Russian forces will help to clear the area by the Turkish border of Kurdish forces (YPG). The U.S. lifted sanctions on Turkey imposed last week over its offensive against Kurdish fighters.

- The European Central Bank (ECB) left rates unchanged this week, as expected. The bank reiterated Thursday that the second round of quantitative easing will start on November 1 at a monthly pace of 20 billion euros ($22.3 billion) per month. Christine Lagarde, former director of International Monetary Fund, will replace Mario Draghi on November 1, as the head of the ECB and she is expected to stick to stimulus plans proposed by Mr. Draghi.

- Russia delivered the biggest rate cut since 2017 and signaled more easing. The benchmark rate was lowered to 6.5 percent from 7 percent and end-of-year inflation forecast was revised down to 3.2 percent from 3.7 percent. Russia already cut rates three times this year, and according to the central bank’s Governor Elvira Nabiullina, rates will stay low and could go lower in order to support the country’s sluggish growth.

Threats

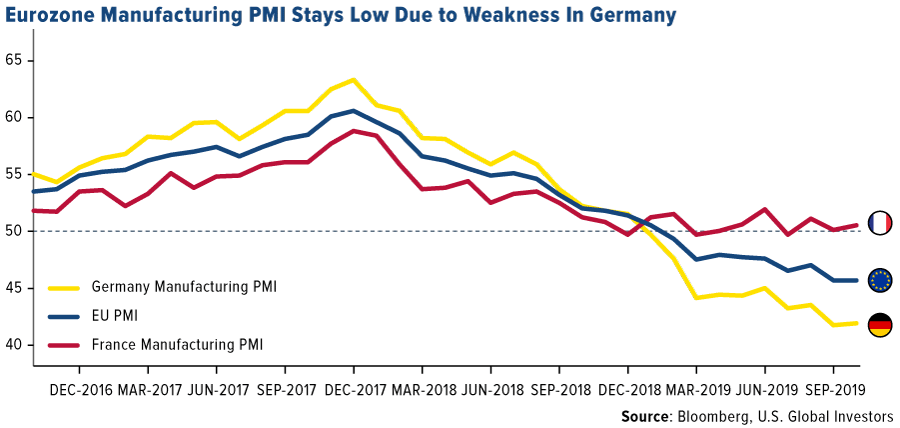

- The latest eurozone preliminary Manufacturing PMI data was reported at 45.7, below the 50 level that separates contraction from expansion. Germany reported weak manufacturing data again, with its PMI at 41.9. The strongest manufacturing PMI came out of France, and the gap between Germany and France remains large.

- For now, Europe has been responding positively to developments in Great Britain and the noise around the country’s exit from the eurozone scheduled for October 31. The new Brexit deal was approved by lawmakers, however the timetable was not. The Prime Minister proposed to lawmakers to discuss the new deal within a few days, a process that normally would take weeks or months. Snap elections could happen December 12, but needs parliamentary approval.

- Bloomberg reported the European Commission told five countries including Italy and France that their draft budgets for 2020 risk breaching the eurozone's fiscal rules. The EU's executive arm sent letters to Rome and Paris as well as to the governments in Spain, Portugal and Belgium demanding further clarifications on the draft plans they submitted to Brussels earlier in October.

China Region

Strengths

- The best performing index in the region for the week was South Korea, up 1.32 percent. Consumer confidence in the nation rose to 98.6 from 96.9.

- Jefferies upgraded Taiwan stocks to modestly bullish from modestly bearish. They see Taiwan as one of the first emerging markets to leave the manufacturing contraction behind.

- Industrial & Commercial Bank of China Ltd., the world’s largest lender by assets, saw a 5.8 percent increase in profits in the third quarter despite a deepening economic slowdown. Bloomberg reports that ICBC led China’s largest state-owned banks in reporting stable earnings even as the economy expanded at the slowest pace since the early 1990s.

Weaknesses

- The worst performing index in the region was Thailand, down 2.34 percent. Thai stocks were the top losers in Asia on economic growth concerns after the International Monetary Fund (IMF) forecast for moderate 2020 growth. This has stoked concern that the Thai economic expansion may recover slowly.

- The IMF lowered its 2020 real GDP forecast for China from 6 percent down to 5.7 percent. The IMF cut growth in several other countries including Singapore, India and the Philippines.

- Asia’s biggest stock, Tencent Holdings Ltd., closed down 0.3 percent in Hong Kong on Thursday and is down 20 percent since a peak in April. The company has lost $93 billion in market value. Bloomberg reports that sentiment is souring from investors in China and there is concern surrounding its decision to air NBA games.

Opportunities

- This week was filled with mostly positive news on the trade war front. President Trump said that negotiations on an initial trade deal are advancing and raised expectations of an agreement next month. China said that it will aim to buy at least $20 billion of agricultural products in a year if there is a deal signed. U.S. Department of Agriculture data show that the trade was has significantly hurt farmers and exporters, with less than $10 billion of exports to China last year. President Trump said during a Cabinet meeting at the White House on Monday that “they have started the buying” but that he “wants more.”

- According to pro-Beijing lawmaker Michael Tien, the Chinese government is considering a plan to replace Hong Kong’s CEO Carrie Lam. Tien said in an interview that the government assessed that the Hong Kong protests could go on for a while and that action needs to be taken. “Dragging this thing out is actually bad for everyone, for Hong Kong, the police. So now they need to take a sort of action. And I have heard it’s going to be next year, probably February or March.” Is this good new or bad news? It’s always an opportunity for the months-long Hong Kong protests to end, as economic data shows it has hurt the economy. However, removing Lam as CEO might not end the civil unrest.

- Although its economy is hurting and money is flowing out, Hong Kong is still the world’s third largest venue for IPOs this year amid mass protests, with companies having raised $18.6 billion. Bloomberg reports that the city has hosted two initial public offerings of more than $1 billion since early June. ESR Cayman Ltd., a warehouse operator, is still testing investor appetite and is looking at a share sale of as much as $1.45 billion.

Threats

- The drama continues between MSCI Inc. and U.S. lawmakers. The global index provider is facing criticism by Senator Marco Rubio for adding hundreds of Chinese stocks to its benchmark emerging markets index last year and then increasing the weighting to them this year, reports Bloomberg News. A few companies in the index, such as Hangzhou Hikvision, have recently been placed on a U.S. blacklist. American Securities Association CEO Chris Iacovella said “MSCI continues to look the other way as it funnels billions of dollars of American money out of the U.S. and into Chinese companies that are fraudulent, on the sanctions lists, or do-not-do business list.” MSCI’s CEO says there are no U.S. laws or regulations that prohibit an index company from creating an index containing China A securities.

- Indonesia’s Finance Minister Sri Mulyani Indrawati said this week that the nation’s budget deficit is set to widen, citing a struggling manufacturing sector and falling commodity prices. Bloomberg reports that the 2019 budget deficit projection is 1.93 percent of GDP, still below the legally mandated ceiling of 3 percent. Indrawati said “the pressure on revenue is huge mainly because of current economic conditions.”

- The U.S. Treasury report on foreign currency manipulators is due in the next few weeks and several Asian nations are on guard. Singapore, Malaysia and Vietnam were cited in the May report for the first time, and the Treasury says it keeps newcomers on the list for at least two straight reports, according to Bloomberg News. China, Japan and South Korea were also on the list in May.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 25 was Cryptonex, up 636.51percent.

- Speculators in bitcoin are gaining the upper hand, writes Bloomberg, as the popular digital currency has become “boring” for many in the get-rich-quick crowd with volatility ebbing. According to data trackers Skew and BitcoinTradeVolume, at $5 to $10 billion a day, the amount of derivatives traded globally exceeds bitcoin spot volume by 10 to 18 times. Asian-based exchanges are leading the charge in derivatives trading.

- According to CEO Brian Armstrong, Coinbase has earned more than $2 billion in transaction fee revenue since launching in 2012, writes CoinDesk. The company has turned a profit over the last three years, including during the 2018 bear market.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended October 25 was FNB Protocol, down 68.61percent.

- ING CEO Ralph Hamers told the Financial Times on Tuesday that banks may drop Facebook as a customer if the company continues with its experimental foray into cryptocurrency without addressing regulatory concerns, writes CoinDesk. According to Hamers, the potential for Libra users to evade anti-money laundering standards and facilitate “financial…crime” raises questions for banks to “take measures and exit the client, or not accept the client.”

- Bitcoin maven Mike Novogratz is warning that the popular digital asset’s next leg lower could take it to $6,500, writes Bloomberg, which would represent a 13 percent drop from current levels. In a CNBC television interview, Novogratz commented “There’s been a bunch of negative things that have happened recently…it will need new energy.” Mid-week, bitcoin dropped as much as 10 percent, a five-month low, as hostility toward Facebook’s Libra cryptocurrency appears to be weighing on sentiment for the coin.

Opportunities

- Beijing-based Bitmain, the world’s largest maker of bitcoin-mining computers, has chosen an old Alcoa aluminum-smelting plant in Texas for a new mine, reports CoinDesk. The plant has an initial power size of 25 megawatts, but will be expanded to 50 megawatts and potentially 300 megawatts. According to officials, Texas has an abundance of power resources, so the new plant is unlikely to affect local electricity prices.

- On Thursday, Bakkt announced that it would “launch the first regulated options contract for bitcoin futures,” reports CoinDesk. Adding a new product to its current slate of physically-settled bitcoin futures contracts. “We’re committed to bringing trust and utility to digital assets and the options contract is an example of the many products we’re developing for regulated markets,” wrote CEO Kelly Loeffler.

- An October 24 press released from the Securities and Exchange Commission (SEC), shows that the Global Financial Innovation Network (an alliance of 50 organizations aimed at supporting financial innovation) has onboarded a handful of U.S. regulatory agencies. As reported by CoinTelegraph, some of the agencies joining include the Commodity Futures Trading Commission (CFTC), the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), along with the SEC itself.

Threats

- A recent research paper entitled “Hijacking Routes in Payment Networks” highlights the fact that the bitcoin lightning network could be vulnerable to a simple and disruptive attack, reports CoinDesk. In the paper, a denial-of-service (DoS) attack is explained, and although the behavior hasn’t been seen in the wild, and the lightning’s technology is still in progress, it is still considered a major flaw in the network as it stands today.

- Facebook chief executive Mark Zuckerberg testified this week before the House Financial Services Committee on a proposal for the company’s Libra cryptocurrency. Zuckerberg faced sniping at plans to launch the digital asset, writes the Washington Post, including its pockmarked track record on privacy and diversity, along with its struggles to prevent the spread of misinformation. Zuckerberg did commit to Facebook not launching Libra anywhere in the world without approval from all appropriate U.S. regulators.

- Despite the U.S. Securities and Exchange Commission’s recent injunction against messaging platform Telegram’s token offering, investors in the blockchain project have opted to stick with the firm, reports CoinDesk. Both groups of investors in Telegram’s twin funding rounds have now agreed to accept extensions for the Telegram Open Network launch following the October 23 deadline.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits