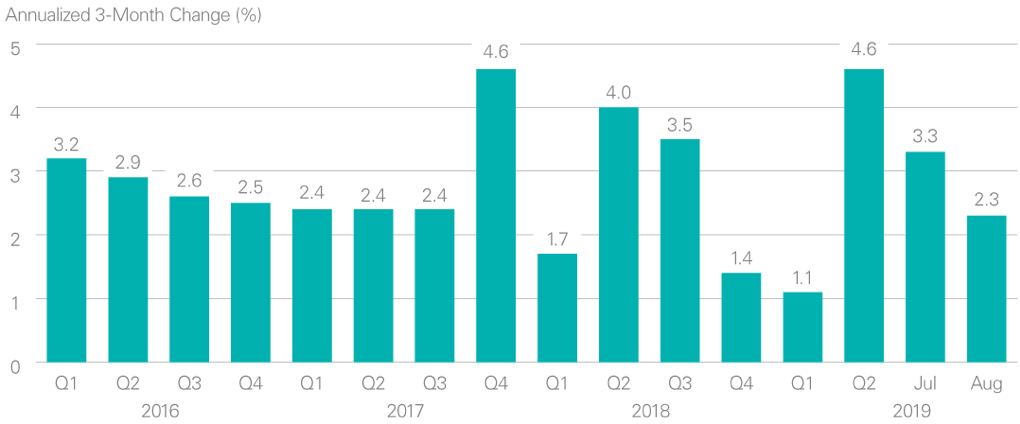

The fourth quarter will provide critical insight into the near-term direction of the US-China trade conflict as well as into whether the Fed will maintain the narrative of a mid-cycle monetary policy adjustment or switch to acknowledging an outright easing cycle. We have become increasingly concerned that the impact of trade tensions is beginning to filter through not just to markets, but also to the broader US economy. Industrial and trade-exposed sectors have been suffering for several quarters, as have the major economies most reliant on these sectors. However, household consumption accounts for roughly 70% of US GDP, and US households remain in a relatively good spot, implying that they can sustain economic growth just as they did during global economic weakness in 2015 and 2016 (see Exhibit).

Exhibit: Household Consumption (~70% of US GDP) Remains Strong

Real Personal Consumption Expenditure

As of August 2019

Source: Bureau of Economic Analysis, Haver Analytics

Nonetheless, weak capex trends suggest that businesses have become more cautious in their expectations and may be inclined to wait and see what happens with policy before putting capital to work. Similarly, jobs growth has slowed, although it is unclear whether this is due to the declining supply of available labor or employers pulling back on hiring in the face of uncertainty. Most importantly, while retail sales still look good and housing activity has rebounded, there are signs that consumer confidence is softening and that households are becoming more concerned about the economic outlook and tariffs.

In the quarter ahead, we will remain focused on the US consumer, looking for evidence of weaker sentiment and slower activity. We also will be monitoring several key global risks: the Japanese consumption tax hike effects, a number of milestones on trade, Brexit, another potential US government shutdown on 21 November, and rising tensions in the Middle East.

As we have emphasized in past quarters, we believe the best strategy for US equity investors against this mixed backdrop—slowing growth globally, supportive central banks, very low interest rates, and equity market resilience amid trade tensions—is to remain overweight equities, but concentrate capital in companies with high sustainable returns on capital that trade at attractive valuations. While equities appear expensive relative to history, we view them as cheap relative to fixed income and believe security selection is critical to avoid overpaying for perceived safety.

The preceding is an excerpt our Outlook on the United States. Read the full paper.

Important Information

Information and opinions are as of 3 October 2019.

Equity securities will fluctuate in price; the value of your investment will thus fluctuate, and this may result in a loss. Securities in certain non-domestic countries may be less liquid, more volatile, and less subject to governmental supervision than in one’s home market. The values of these securities may be affected by changes in currency rates, application of a country’s specific tax laws, changes in government administration, and economic and monetary policy.

This content represents the views of the author(s), and its conclusions may vary from those held elsewhere within Lazard Asset Management. Lazard is committed to giving our investment professionals the autonomy to develop their own investment views, which are informed by a robust exchange of ideas throughout the firm.

This document reflects the views of Lazard Asset Management LLC or its affiliates ("Lazard”) based upon information believed to be reliable as of the publication date. There is no guarantee that any forecast or opinion will be realized. This document is provided by Lazard Asset Management LLC or its affiliates ("Lazard”) for informational purposes only. Nothing herein constitutes investment advice or a recommendation relating to any security, commodity, derivative, investment management service, or investment product. Investments in securities, derivatives, and commodities involve risk, will fluctuate in price, and may result in losses. Certain assets held in Lazard’s investment portfolios, in particular alternative investment portfolios, can involve high degrees of risk and volatility when compared to other assets. Similarly, certain assets held in Lazard’s investment portfolios may trade in less liquid or efficient markets, which can affect investment performance. Past performance does not guarantee future results. The views expressed herein are subject to change, and may differ from the views of other Lazard investment professionals.

This document is only intended for persons resident in jurisdictions where its distribution or availability is consistent with local laws or regulations. Please visit www.lazardassetmanagement.com/global-disclosure for the specific Lazard entities that have issued this document and the scope of their authorized activities.