U.S. Economic Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe past month has been generally cheerful for followers of the American economy. Recent data has included a series of upside surprises. While we remain skeptical about “phase one” of trade negotiations between China and the U.S., the temporary truce is welcome. And the timeline for Brexit was extended, preventing a no-deal departure that could upset global markets.

We are encouraged at how resilient the economy has been in the transition to a regime of trade restrictions. Business investment remains a weak point, but consumers and services continue to advance. The U.S. job market remains strong. If current trends hold, we may look back on 2019 as the year the economy executed an elusive soft landing.

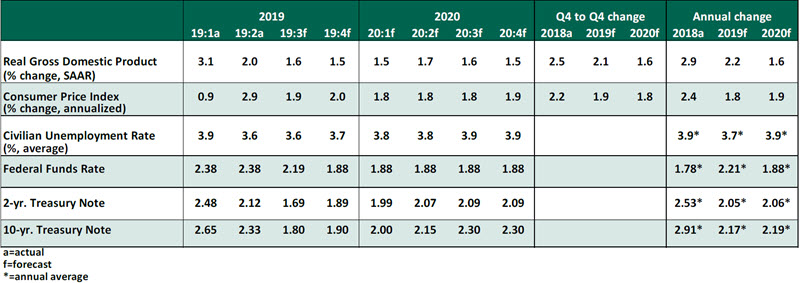

Key Economic Indicators

Influences on the Forecast

- The October job report was a pleasant surprise. 128,000 jobs were created last month, despite disruptions from an automotive labor strike and the beginnings of a wildfire in California. Job creation in prior months was also revised favorably upward. The prime-age (25-54) labor force participation rate reached 82.8%, a level not seen since 2010, further evidence that the recovery is continuing to reach more workers.

- Gross domestic product (GDP) grew at an annualized rate of 1.9% in the third quarter, a higher reading than expected. Consumer spending was the brightest story in the economic data. After six quarters of decline, residential investment grew by over 5%, a sign that lower interest rates are boosting interest rate-sensitive sectors. However, business investment contracted further, to -3% in the third quarter after a -1% reading in the second quarter. Pervasive uncertainty is weighing on business sentiment and capital expenditures.

- At its October 30 meeting, the Federal Open Market Committee (FOMC) lowered the federal funds rate to a range of 1.50-1.75%, accompanied with refreshingly clear messaging that this would be the end of the insurance cuts. The statement accompanying the decision no longer contained a commitment that the FOMC would “act as appropriate to sustain the expansion,” instead shifting to softer language that the FOMC will continue to “assess” the appropriate path of the target rate range. In the post-meeting press conference, Federal Reserve Chair Jerome Powell did not preclude future rate actions, but he set a high bar for both further cuts and eventual increases. Sustained growth is the most likely case, and we do not expect the Fed to take any further actions over the forecast horizon.

- Inflation continues to gather steam after a slow start to the year. The consumer price index (CPI) grew by 1.7% year-over-year in October; on a core basis, excluding food and energy, it grew by 2.4%. Personal consumption expenditures, the Fed’s preferred gauge of inflation, was more tame, growing by 1.3% overall and 1.7% on a core basis. Powell cited a need for core inflation to rise above the Fed’s 2% target before any rate increase would be considered; this outcome is possible but will take time to achieve.

- Recession worries have faded but have not gone away. The Institute for Supply Management Manufacturing Purchasing Managers’ Index recovered some ground with a reading of 48.3 in October, up from 47.8 in September. Though a reading under 50 still shows industrial contraction, we are encouraged that it did not become more severe. Meanwhile, the inversion between the 3-month and 10-year US Treasury yields has ended. We expect the yield curve to gradually recover as market risk sentiment improves, increasing yields on the long end.

- The U.S. and China remain in talks to sign a limited, “phase one” trade deal. Though no terms of a deal have been shared publicly, both sides are setting expectations that the deal will be a first step toward a more comprehensive agreement. The deferral of the October 15 tariff increase by the U.S. was an encouraging step away from escalation.

- The federal government closed the books on fiscal 2019 with a deficit just under $1 trillion. Lower tax receipts have driven down government revenue. Absent a structural change, fiscal capacity to support the economy in a future downturn will be limited.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/disclosures.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All