Which Secular Bull Market Is It – 1950’s or 1920’s?

Membership required

Membership is now required to use this feature. To learn more:

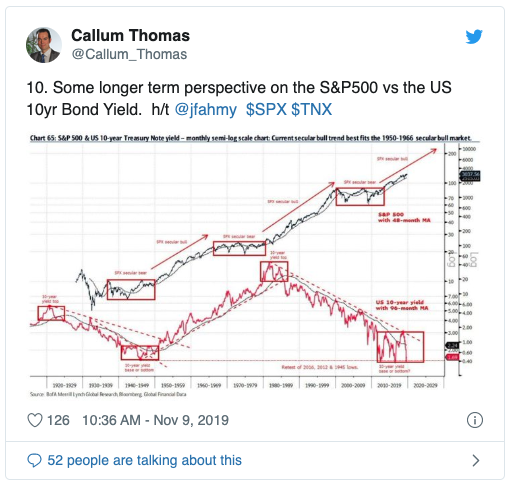

View Membership BenefitsThe following comment was recently making its way around the “twittersphere” suggesting a “new secular bull market” has started.

This isn’t the first time such a call has been made.

“Despite concerns in the third quarter, bears never had a strong argument for why stocks were overvalued and the major indexes simply traded sideways for much of the last six months, wrote Robert Sluymer, technical strategist at Fundstrat Global Advisors.

“We ‘continue to view the market cycle as being a normal pause in an ongoing secular bull market similar to what developed in 2016, 2011 and the ‘cycle’ pullbacks that developed during the secular bull markets in the 50s-60s and 80s-90s.”

It is an interesting point. The current bull market certainly seems unstoppable, but the question that must be answered, fundamentally, is if this is indeed a “secular bull market,” and if so, “where are we” within that cycle.

What is a “secular market?”

“A secular market trend is a long-term trend which lasts 5 to 25 years and consists of a series of primary trends. A secular bear market consists of smaller bull markets and larger bear markets; a secular bull market consists of larger bull markets and smaller bear markets.”

In a “secular bull’ market, the prevailing trend is “bullish” or upward-moving. In a “secular bear” the market tends to trend sideways with severe drawdowns and sharp rallies.

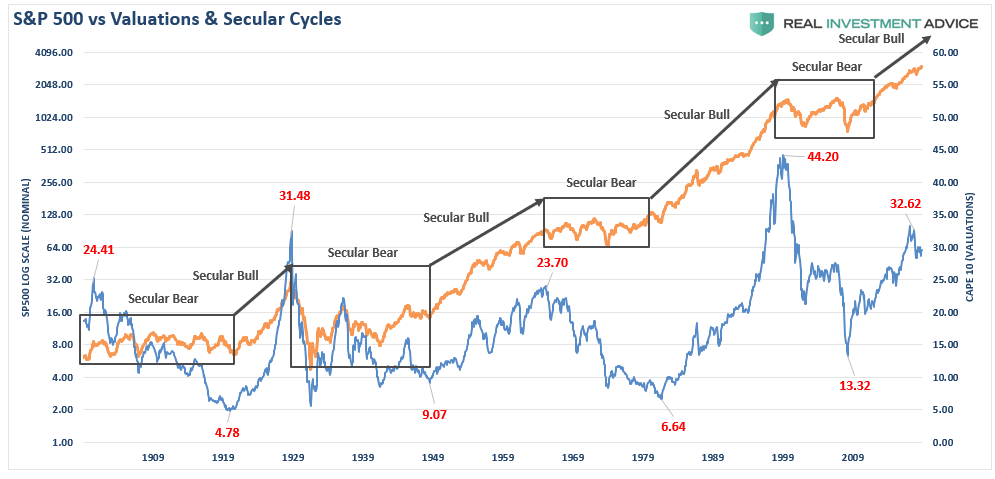

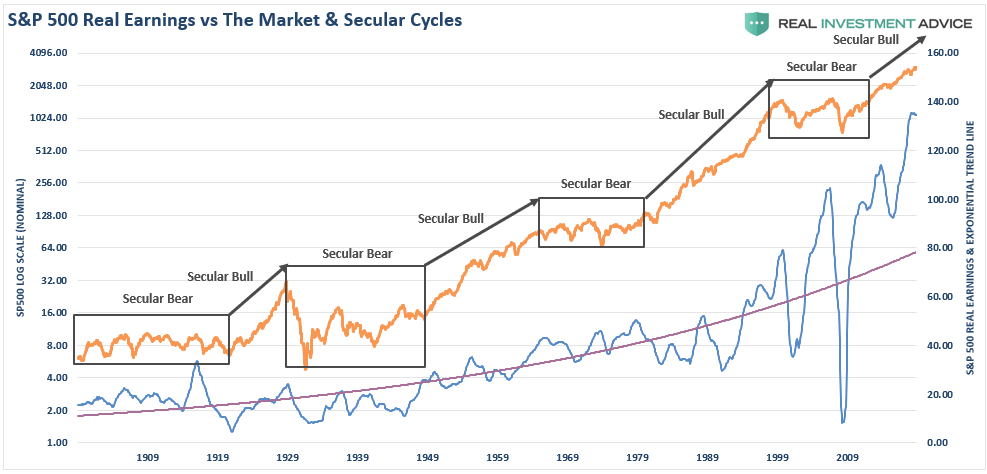

However, what truly defines long-term secular markets are valuations, and whether those valuations are contracting or expanding.

The chart above shows the history of secular bull market periods going back to 1871 using data from Dr. Robert Shiller. One thing you will notice is that secular bull markets tend to begin with CAPE 10 valuations around 10x earnings or even less. They tend to end around 23-25x earnings or greater. (Over the long-term valuations do matter.)

As noted above, what drives long-term secular “bull” markets is “valuation expansion.” In order to have the magnitude of “valuation expansion” needed to support a secular “bull” market, you must both start at “under-valued” levels and have the economic factors and investor enthusiasm to support a return to “over-valued” levels.

The problem with the idea that we are currently in a secular bull market akin to the 1950’s or 1980’s has everything to do with economic growth. Over the long-term, stocks CAN NOT outgrow the economy, as the stock market is a reflection of the companies engaging in the economy. This is why “valuations” are so important. Investors, in their “exuberance” can pay more than a company can generate over the long-term. When this exuberance is realized, valuations “contract” to reflect reality.

For several reasons, as we will discuss, the current “secular bull market,” if you can call it that, is likely more akin to the very brief cycle of the 1920’s.

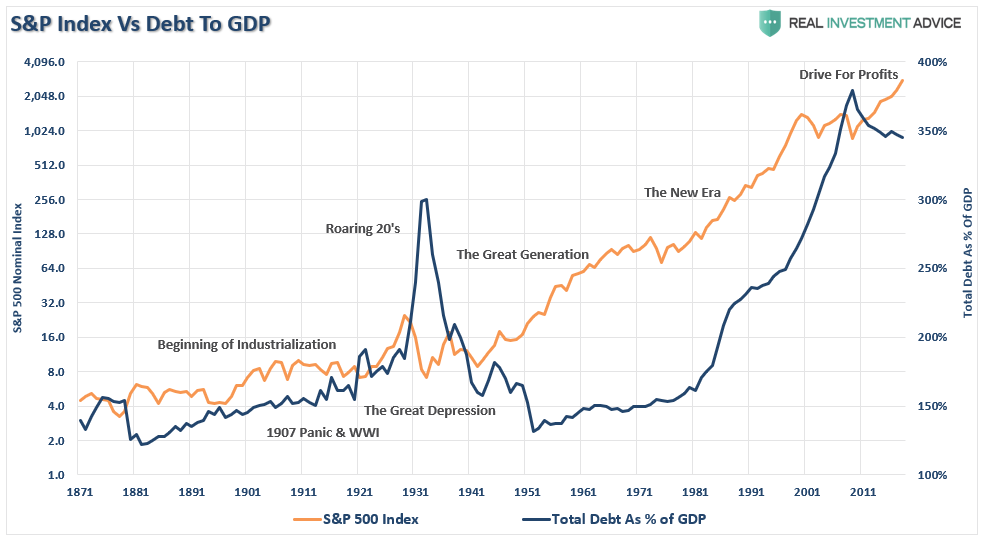

Interest Rates & Debt

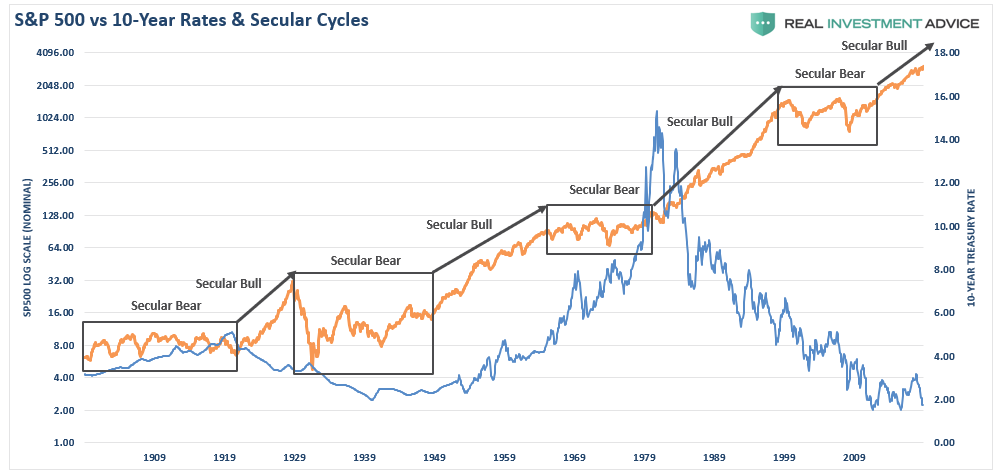

The argument that the U.S. has entered into another “secular bull market” is because interest rates are low. While the chart clearly shows that interest rates have hit the same levels as last seen in 1946, the view rates will rise strongly from current levels assumes that the same economic drivers exist today.

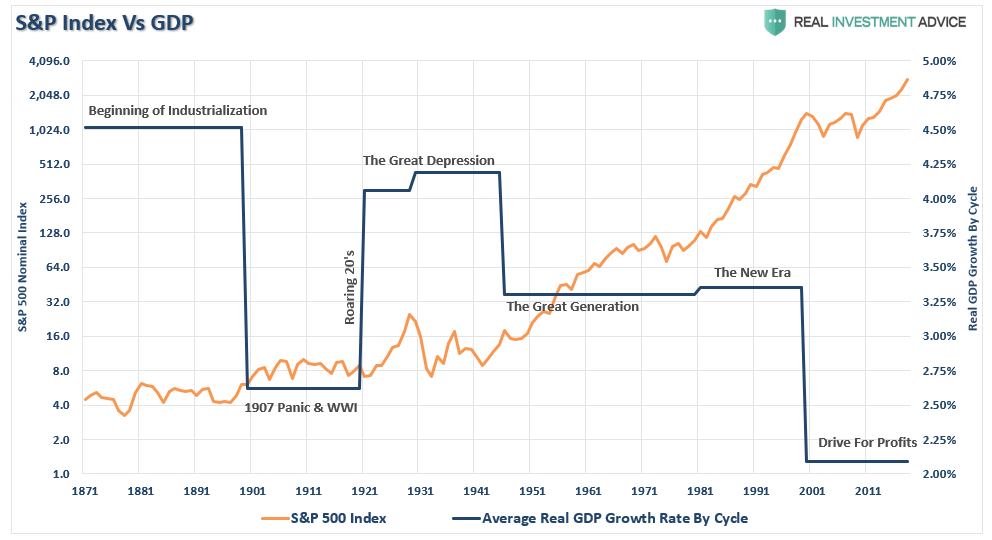

Rising interest rates are a function of strong, organic, economic growth that leads to a rising demand for capital over time. If we refer to the GDP chart above, there have been two previous periods in history that have had the necessary ingredients to support rising interest rates. The first was during the turn of the previous century as the country became more accessible via railroads and automobiles, production ramped up for World War I, and America began the shift from an agricultural to industrial economy.

The second period occurred post-World War II as America became the “last man standing” as France, England, Russia, Germany, Poland, Japan, and others were left devastated. It was here that America found its strongest run of economic growth in its history as the “boys of war” returned home to not only start rebuilding the countries that they had just destroyed, but

But that was just the start of it.

Beginning in the late 50’s, America embarked upon its greatest quest in history as man took his first steps into space. The space race that lasted nearly twenty years led to leaps in innovation and technology that paved the wave for the future of America. Combined with the industrial and manufacturing backdrop, America experienced high levels of economic growth and increased savings rates which fostered the required backdrop for higher interest rates.

Currently, the U.S. is no longer the manufacturing powerhouse it once was and globalization has sent jobs to the cheapest sources of labor. Technological advances continue to reduce the need for human labor and suppress wages as productivity increases. Today, the number of workers between the ages of 16 and 54 is at the lowest level relative to that age group since the late 1970’s. This is a structural and demographic problem that continues to drag on economic growth as nearly 1/4th of the American population is now dependent on some form of governmental assistance.

This structural employment problem remains the primary driver as to why “everybody” is still wrong in expecting rates to rise.

However, this is also why whenever there is a discussion of valuations, it is invariably stated that “low rates justify higher valuations.” The argument is based on an assumption that rates are low BECAUSE the economy is healthy and operating near full capacity.

The reality is quite different. The main contributors to the illusion of permanent prosperity have been a combination of artificial and cyclical factors. Low interest rates, when growth is low, suggests that NO valuation premium is “justified.“

Currently, investors are taking on excessive risk, and thereby virtually guaranteeing future losses, by paying the highest S&P 500 price/revenue ratio in history and the highest median price/revenue ratio in history across S&P 500 component stocks.

Importantly, when talking about “Secular Bull Markets,” the amount of debt in the system plays an important factor. The last time that debt-to-GDP ratios hit such a peak was going into the “Great Depression.” Since debt retards economic growth by diverting savings into debt payments rather than productive investments, it is hard to suggest a “secular bull market” can gain traction given excessive debt levels.

Earnings Reversions

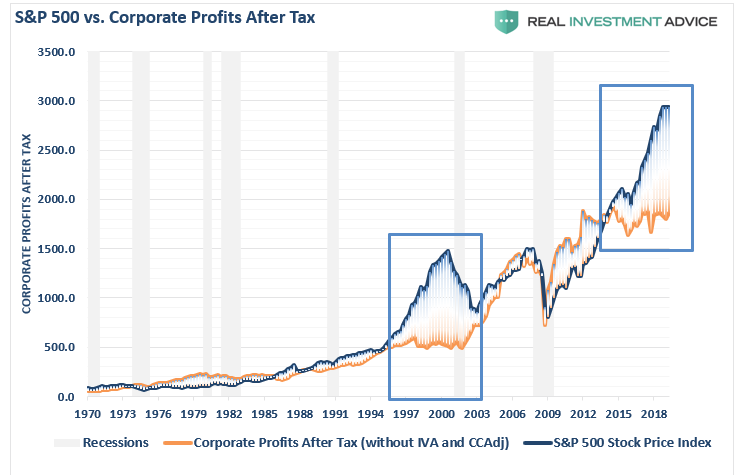

One of the more significant reasons the markets have likely not entered into the next great “Secular Bull Market” is due to the artificial inflation of earnings from massive share repurchases, corporate tax cuts, and excessive liquidity from Central Bank interventions.

Given the current deviation of both earnings from their long-term growth trend, and the deviation from reported profits, as shown below, the eventual mean reversion will likely be brutal.

The Great 9-Year Secular Bull Market

While the idea of a new “secular bull market” is certainly optimistic, it is also a dangerous concept for investors to “buy” into.

As stated above the stock market, over the long-term, is a reflection of the underlying economic activity. Personal consumption makes up roughly 70% of that activity. Given the consumer is more heavily leveraged than at any other point in history, it is highly unlikely they will be able to become a significantly larger chunk of the economy. With savings low, income growth weak, and debt back at record levels, the fundamental capacity to re-leverage to similar extremes is no longer available.

Let’s also not forget the singular most important fact.

The breakout of the markets in 2013, following the two previous bear markets, was NOT one based on organic economic fundamentals. Rather it was from massive monetary interventions by Central Banks globally. The previous secular bull markets in our history were ones which were derived from extreme under-valuations, washed out financial markets, and extreme negative sentiment.

Such is clearly not the case today.

The “secular bull market” of the 1920’s is probably the best example of the cycle we are in currently. Then banks were lending money to individuals to invest in the IPO’s the banks were bringing to market. Interest rates were falling, economic growth was rising, and valuations were rising faster than underlying earnings and profits.

There was no perceived danger in the markets, and little concern of financial risk as “stocks had reached a permanently high plateau.”

It all ended rather abruptly.

Currently, it is clear that stock prices can be lofted higher by further monetary tinkering. However, the larger problem remains the inability for the economic variables to “replay the tape” of the ’50s or the ’80s. At some point, the markets and the economy will have to process a “reset” to rebalance the financial equation.

In all likelihood, it is precisely that reversion which will create the “set up” necessary to actually begin the “next great secular bull market.” Unfortunately, as was seen at the bottom of the market in 1974, there will be few individual investors left to enjoy the beginning of that ride.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All