In this short week before the Thanksgiving holiday, we decided to offer some brief insights on issues of the day. For those celebrating the holiday, we hope that Thursday finds you surrounded by friends, family and food.

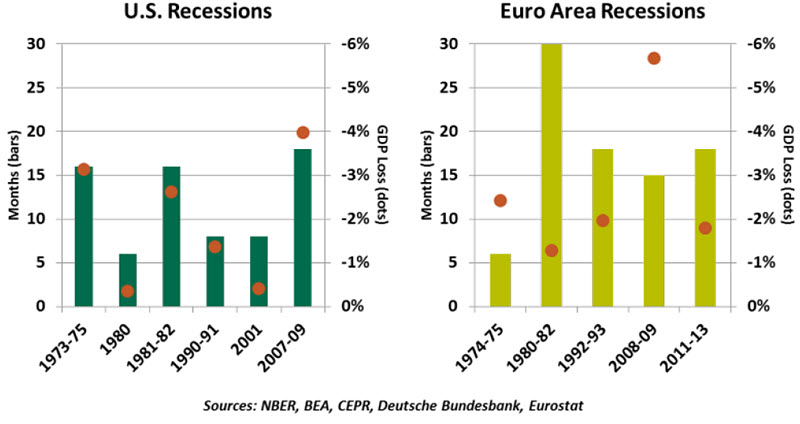

- We spend a lot of time worrying about recession, but most recessions are mild and provide useful rebalancing. The 2008-09 episode was especially severe, but atypical. And trying to prevent recession at all costs has costs itself.

But inflation is already running below its target in many places, and would certainly retreat in a downturn. This could turn into deflation, a condition that strikes fear among central bankers. No policy maker wants to preside over the “Japanification” of the local market; so monetary authorities press on, even though their policies may not be the right tools for the job.

It’s hard to acknowledge there is nothing more you can do, but central banks may have exceeded the edge of their effectiveness.

- We remain skeptical about the state of trade relations between China and the United States. Deal announcements arrive with great fanfare, but subsequent negotiations typically stall. “Phase one” of an agreement between the two countries is in limbo, with the next round of tariffs approaching on December 15. Yet somehow markets continue to be overly impressed by even the merest suggestion that tensions have diminished.

Both sides feel time is on their side. Both see political gain in sustaining a veneer of strength. Both seem able to buffer the economic blow to domestic businesses and banks. The odds of a deal before the 2020 election don’t look that strong.

-

The world is ablaze with protests and Latin America, whose future just a decade ago seemed bright, is at the center of that blaze. From Bolivia to Ecuador to Venezuela to Chile, all are witnessing political and environmental turmoil (regime changes, protests, migration crisis and deforestation).

Though progress has been made, Latin America remains one of the most unequal regions of the world. Higher commodity prices since the new millennium have brought rapid economic growth, but governments have failed to leverage this advantage to undertake institutional and structural reforms. Corruption, unfortunately, is an affliction that has diminished the region’s performance.

Dwindling economic fortunes across the region along with an outburst of scandals have only heightened the tensions. An unequal society is a fractured society. Only by involving the entire population in economic progress can a country grow steadily and avoid unrest.

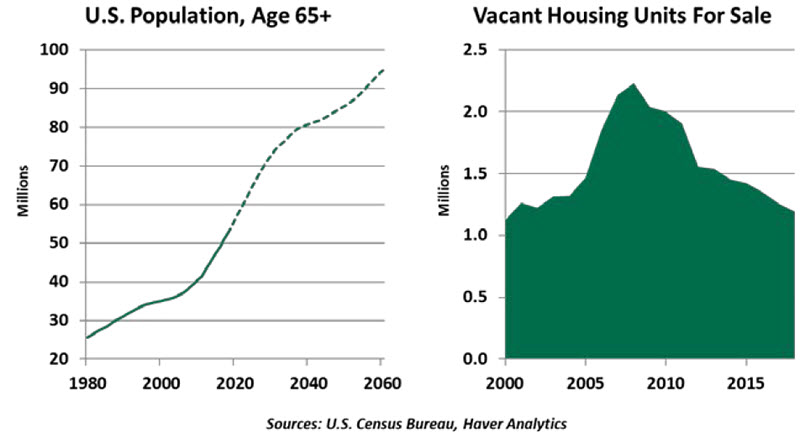

- The United States is facing what some would term a good problem to have: More people are living longer. But the housing market is struggling to adapt to elderly Americans’ desire to stay in their homes as they grow older.

The appeal of aging in place is clear: Our homes are familiar and provide independence. To keep things comfortable, the elderly are investing in remodeling. This helps the home evolve with them as they age.

Economically, more people staying in their homes means fewer homes are being sold. The homes where seniors are staying are typically older stock and single-story residences that would make good starter homes. The lower supply of housing is supporting prices but excluding potential buyers. This is another area where demographics are increasingly impacting the economy.

- Around the world, national budget policy generates very strong opinions from a number of corners. But there seems little doubt that one of three things is in the future: Tax increases, curtailment of social benefits or an increase in borrowing costs. That is a mathematical observation, not a political statement.

As we discussed in our recent piece on the Laffer Curve, the notion that you can have very low taxes, very strong growth and a balanced budget is a stretch at best and dangerous at worst. Something is going to have to give.

- Christine Lagarde, the new president of the European Central Bank (ECB), should not expect much of a honeymoon period. Inflation is running at just over half the ECB’s target, and several eurozone countries are struggling to stay out of recession. Something needs to be done.

Unfortunately, the traditional monetary toolkit is bare, and there is strong resistance to further easing among the ECB’s governing council. So Lagarde has renewed the calls of her predecessor for additional public spending. Key countries have been reticent about relaxing budget rules, fearing a loss of spending discipline would ensue. But the alternative is prolonged stagnation. Look for Lagarde’s skill as a financial diplomat to win the day and get funds flowing in the eurozone.

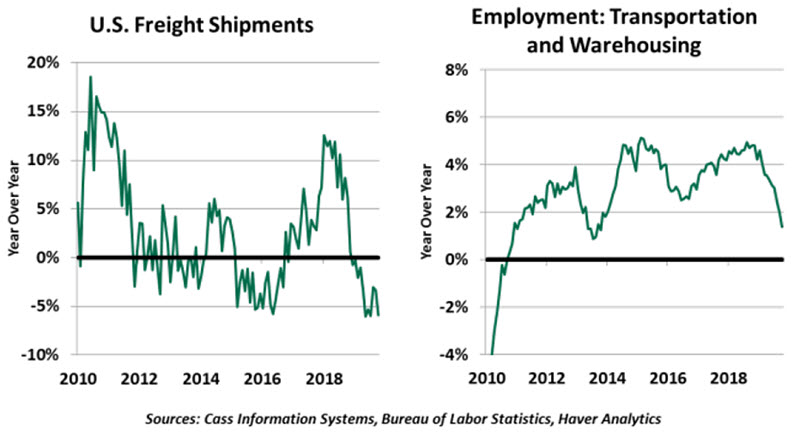

- Economic worries in the United States have stemmed from a decline in the manufacturing sector. The manufacturing purchasing managers’ index (PMI) remains in contraction. The slowdown has contagious effects, specifically on the transportation sector. In 2019, freight shipments within the United States on both trucks and railcars fell.

Shippers have lived at the whims of many market uncertainties. Tariff threats led to frontloading of imports, pushing up freight volumes last year. This year’s General Motors strike cut into shipments of parts into, and finished vehicles out of, GM’s factories.

Last year, the hottest market for semi-skilled labor was truck driving. The driver shortage appears to have ended. But on behalf of the 4.8 million Americans employed in the transportation and warehousing sector, we hope this industry sees only a gradual slowdown.

- We rarely have the luxury of watching new industries sprout, but legalized cannabis has been a remarkable growth story. Medical legalization started in California in 1996 and has since spread to 33 states; recreational legalization started in Colorado in 2012, with 10 more states following suit thus far.

Entrepreneurs in this sector face many challenges trading in a controlled substance. Federally-chartered banks and electronic payment networks cannot serve growers and dispensaries, but state banks and credit unions have helped fill this niche. Goods cannot be shipped across state lines, requiring local production that inhibits scale.

State and municipal governments welcome the additional tax revenue from cannabis sales, though revenue enhancements after legalization have been modest. Any social benefit must be weighed against the risks of impaired driving and the detrimental effects of drug use on youth.

A subtle byproduct of legalization will be less incarceration. A reduction in drug arrests will mean fewer convictions that impair job candidates, which might help to keep the labor market growing.

- While wallet issues are the key driving force behind the surge in global unrest, tourists swarming vacation hot spots has sparked protests, too. Confluences of macroeconomic factors (like a growing middle class) and changing business trends (social media) have led more tourists crowding to popular destinations. In 2017, there were 1.4 billion tourist arrivals with Europe alone absorbing half of them. Tourism accounts for 3% of the world’s GDP.

While tourism creates jobs, wealth, investments and cross-cultural exchanges, there is a growing recognition of less positive outcomes, including environmental degradation and the pricing-out of local consumers. This has led to crackdowns on tourism, particularly in Europe. Many cherished places are at risk of losing the charm that lures tourists in the first place; a recent editorial urged the Louvre to take down the Mona Lisa, for example. The backlash doesn’t seem entirely odd, but let’s not forget tourism also brings tremendous good.

- If you travel much at all, you’re bound to run into flight delays. There are always people who get really annoyed on those occasions, but there are also people who take them in stride with good humor. You want to be among the latter community; it’s classier and your stress levels will be lower. Be sure you have plenty of reading and video packed on your electronic devices. And be kind to those trying to rebook or reroute you, as any problems are not their fault.

Here’s hoping that your holiday travel is uneventful!

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2019 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.