As a seasoned and grizzled veteran of the financial services industry for now going on 50 years, the most commonly asked questions I have received, and still do to this day, are: when to buy and when to sell a stock? Moreover, these very questions are the mother of how and why I have been labeled “Mr. Valuation.” You see, from my perspective, the answers to these important questions are directly linked to valuation, which is why so much of my work over the years has been on how to value a business. Therefore, in this context, the real question is how do you value a business?

For starters, the prudent investor must accept that you cannot value a business with perfect precision and therefore should not try. Instead, you want to have a range of valuations that are based on realistic assessments of what a business can produce on its shareholders’ behalf. Nevertheless, once you have a reasoned understanding of the value of the business then and only then can you make intelligent buy, sell or hold decisions. But once again, not with perfect timing but with prudent calculations offering a range of value that prudent investors can embrace.

Moreover, there are timeless principles of valuation that are rooted in sound fundamental analysis. Over the years, I have written about these timeless principles on numerous occasions. Consequently, instead of trying to reinvent the wheel, I have decided to refresh, update and repost some of my earlier work. In 2010 I published a series of articles on the principles of valuation. Over the course of the next several weeks, I will be presenting a new series of updated versions of those original works. This article will be the first in that series.

When to Buy, When to Sell

The two most important questions that investors in common stocks want answered are: When to buy, and when to sell?

As I alluded to in the introduction, I don’t believe that perfect answers to either question are possible. There are sound answers, prudent answers, and intelligent answers – but no perfect answers.

On the other hand, there often exists obvious times when a stock should be bought or sold. Thus, obvious buy and sell mistakes can be avoided by investors who understand the fundamental principles behind valuation. Prudent investors, through the application of intelligent research, can engage in a reasoned approach to finding the appropriate answers.

The main reason that perfect answers are not possible can be found in the classic Warren Buffett quote: “The fact that people will be full of greed, fear or folly is predictable. The sequence is not predictable.“

Buffett is speaking to the reality that the stock market can and often does temporarily miss-appraise stocks. During times of greed, the market is quite capable of overvaluing companies, sometimes to an outlandishly high level. When fear reigns, the market can significantly undervalue a company and keep it that way for an outlandishly long period of time.

Yet for the most part and over the longer run, the market will price stocks close to intrinsic value, and when deviations do occur, they inevitably revert to the mean or correct themselves. The insidious part of this last statement is the confusing fact that the correction process can happen very quickly or drag on over very long periods of time. Worse yet, there is often no rhyme or reason to explain why. When people are gripped with emotion they can, and will, do crazy and irrational things. Crazy and irrational behavior cannot be quantified or predicted, therefore, quite often there are no answers or insights to be found.

The saddest part of what has been written so far is how it has caused people to think about the stock market, or the stock price movements of individual stocks. My observations based on anecdotal evidence gathered from speaking to hundreds if not thousands of investors leads me to conclude that many investors today possess a general distrust and apprehension regarding stocks and value.

Many believe that the markets are rigged against them, and others believe that there is no such thing as intrinsic value. These are just a few examples of the jaundice and prejudiced views that people hold regarding the financial markets and/or the people and institutions that oversee them.

This is not just sad; it also represents a serious potential obstruction against people achieving the financial security and independence we all desire. Knowledge is power, and this first of a series of articles on the principles of valuation and how to value common stocks is offered to provide investors empowerment. With this series of articles, I endeavor to provide rational answers to these important questions based on timeless principles of business, economics and accounting.

To be clear, I am not suggesting that I can tell people how to perfectly time the markets. Quite the contrary: I believe that perfect timing of individual stock price movements or markets is an undeniable impossibility. As the great investor Bernard Baruch so aptly put it: “Don’t try to buy at the bottom or sell at the top. This can’t be done except by liars.”

On the other hand, I am suggesting that investors are capable of, and can within a reasonable range determine the True Worth™ of an operating business. As previously stated, although this cannot be done with absolute perfection, it can be done within reasonable and practical levels of accuracy. Most importantly, within this process we will endeavor to show how calculating intrinsic value can be accomplished while simultaneously providing the investor a margin of safety.

This series of articles is dedicated to what Warren Buffett has often said was the most important lesson he learned from Ben Graham, his mentor. Mr. Graham’s timeless words of wisdom summarize the objectives of this series of articles and are as follows:

“Ben Graham said you should look at stocks as small pieces of the business. Look at (market) fluctuations as your friend rather than your enemy – profit from folly rather than participate in it. He said the three most important words of investing: “margin of safety.” I think those ideas, 100 years from now, will still be regarded as the three cornerstones of sound investing.” Warren Buffett

What gives the business (stock) value?

Ultimately, any business, public or private, has its value derived from the amount of cash flow it can generate for its stakeholders (stockholders). Not only will capital appreciation depend on the level of earnings, dividends are also a function of earnings. It is because of this principle that the discounted cash flow method of valuing a business is so widely accepted by scholars and professional investors. Consequently, this series of articles on how to value a business are going to be strongly based on utilizing fundamental valuations based on cash flows (earnings) as the primary method for finding True Worth™.

However, I am going to spare the reader the tedious task of evaluating or calculating long and complex mathematical formulas in order to achieve our stated goals. Instead, I will focus on presenting logical explanations and straightforward discussions of the principles behind these important valuation methods. Additionally, I will provide what I hope the reader finds as easy to understand pictures and back them up with a video as evidence supporting my points. Anyone who is interested in a more scholarly approach can simply Google: how to value a company using the discounted cash flow method (DCF).

The Commonsense Thesis of Business Value

In this series I will attempt to illustrate what I believe to be the commonsense reality and foundational principle that faster growing businesses offer a higher future value than slower growing businesses. The rationale behind this statement is logical and straightforward. The faster a business grows, the larger the future income stream becomes that investors will be discounting back to the present value. Another way to look at this is that faster growth creates more earnings for markets to capitalize. The more earnings available to be capitalized, the more valuable your business is.

Even more plainly stated, you buy a dollar’s worth of earnings today that you believe will grow into two dollars’ worth of earnings in future time. Once you have twice as many dollars’ worth of earnings than you originally bought, you then have twice as many assets for the market to value. Even if future valuations (P/E Ratios) are lower than when you originally purchased your first dollar’s worth of earnings, odds are in your favor that valuation will be higher since you now possess so much more earnings power. The speed or velocity by which your original dollar’s worth of earnings grow by is going to determine how long it takes for one dollar to grow into two dollars. This leads me into once again sharing a discussion on the power of compounding.

The Rule of 72

There is an urban legend that attributes Albert Einstein with saying that compound interest is the most powerful force in the universe. Whether Albert Einstein said this or not is unknown. But the power of compounding is truly remarkable. Therefore, it should not surprise us that a genius like Albert Einstein might make such a statement. Personally, I was first introduced to the power of compounding by my economics professor in college.

Later, this same man became my mentor and gave me my first job in the money management industry in 1970. My professor, Alvin F. Terry, created a napkin presentation that not only had a great impact on my impressionable young mind, but also crystallized for me the magic of compounding. I would like to share it with you here as follows:

He would start by saying if you invest $20 a month, or $240 a year, over your average working life, which he defined as 36 years (this timeframe makes the math work better), and earn 10% a year on your money, you would accumulate approximately $80,000 (note: this presentation takes minor liberties with the math).

Then he would ask what if you invest the same $20 a month over the exact same 36 year time frame, but instead of 10% you earned 20% per year, how much would you then accumulate? Of course, intuitively many of his students would answer $160,000, or double the $80,000. However, astute readers understand that because of the geometry of compounding, the actual answer is over $1.5 million, or more than 18 times as much money by earning 20% than you would have earned at 10%.

Here is the logic behind the difference utilizing “the Rule of 72.” As everyone in finance is aware, this rule of thumb works like this; divide any rate of return into the number 72 and the answer tells you how many years it takes to double your money. Therefore, 10% divided into 72 means that it takes 7.2 years to double your money.

On the other hand, 20% divided into 72 means it only takes 3.6 years, or half the time to double your money. Since our defined working life is 36 years, if you double your money every 7.2 years by earning 10%, you will get five doubles (36/7.2=5 doubles) over 36 years.

With these numbers in hand and for illustration purposes, let’s track our first $1.00 of investment and double it five times which looks like this; $2.00, $4.00, $8.00, $16.00 and finally $32.00. However, as the Rule of 72 indicates, doubling your return does not double your money; instead it doubles your doubles. So, at a 20% return you will get 10 doubles instead of five (36/3.6=10 doubles) over 36 years.

Carrying this logic out to its mathematical conclusion, adding five doubles to your original dollar invested looks like this: $64.00, $128.00, $256.00, $512.00 and finally $1024.00. So, for perspective, the first dollar you invested grew into $1024 by earning 20%, or 32 times as much as it would have earned at half the rate of 10%. Importantly, this same impact applied to every additional dollar that was invested.

Herein lies the power of compounding, and herein lies the insight as to why a faster growing company is worth more than a slower growing company. If you had two companies where one grew 10% per year while the other grew at 20% per year, it’s obvious that the 20% grower would generate a significantly larger stream of income with which to discount back to present value. In other words, its future value would be worth a whole lot more.

10% Growth Versus 20% Growth

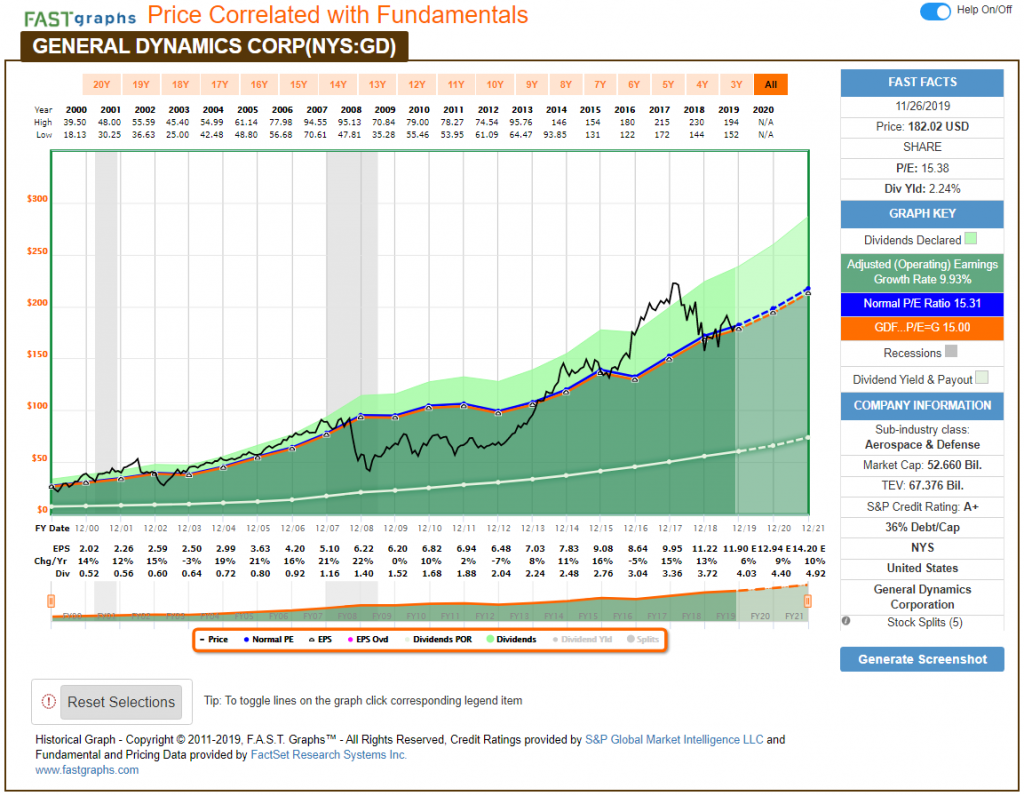

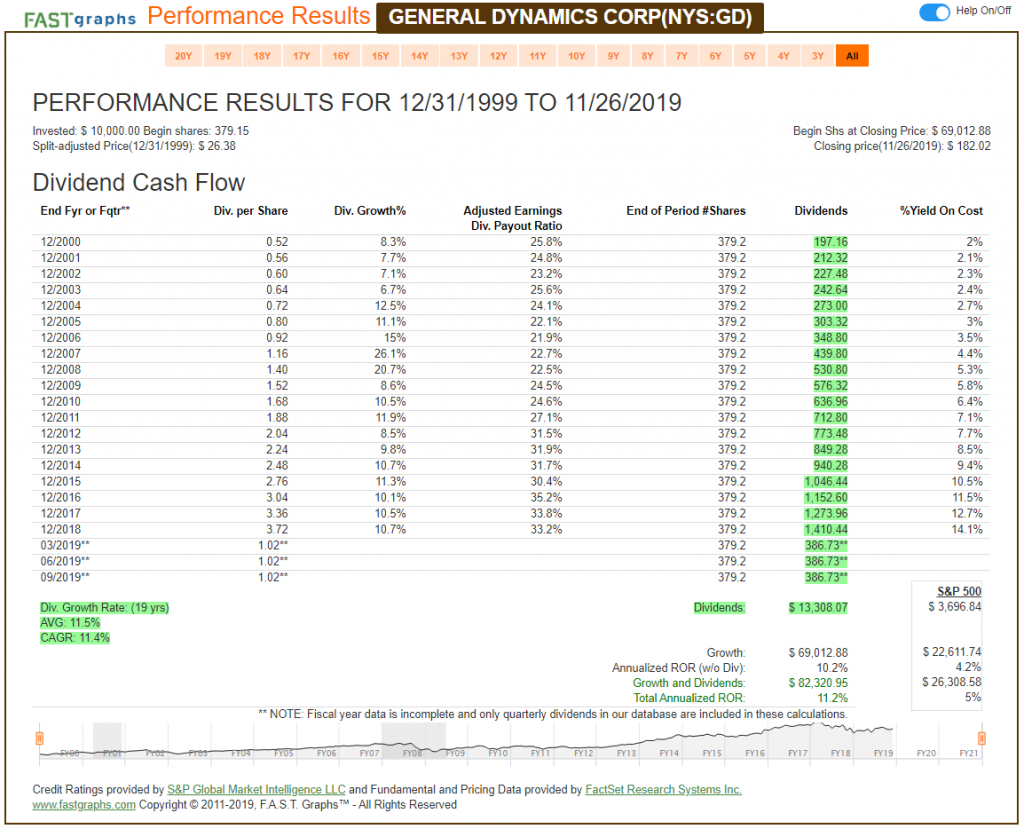

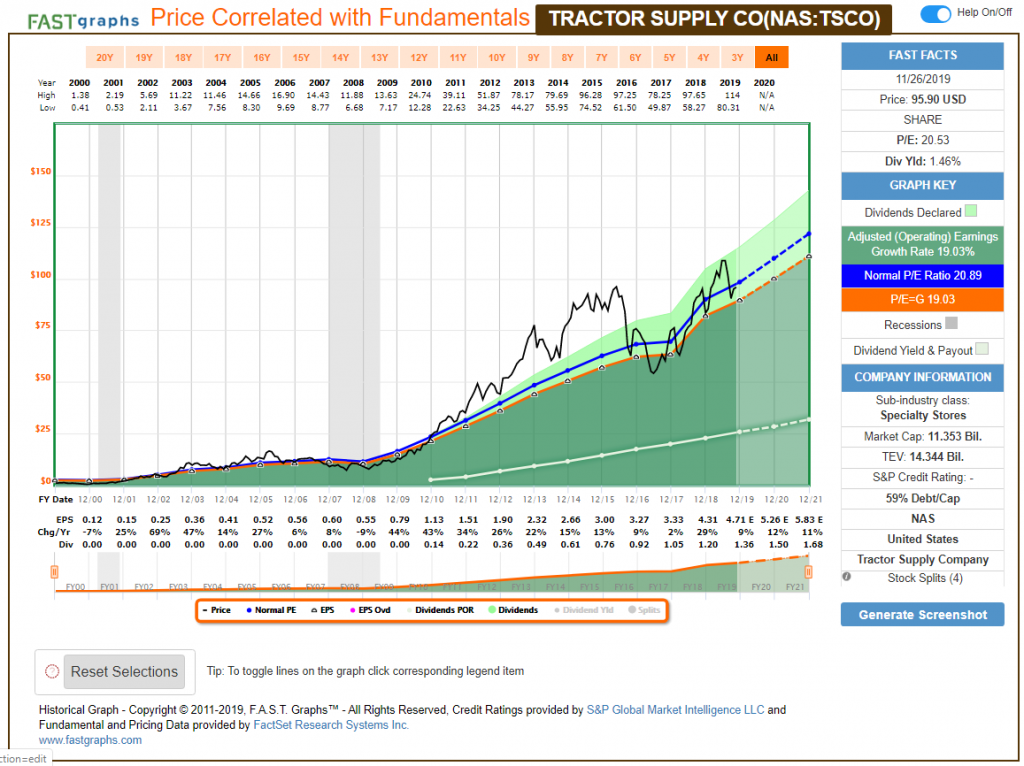

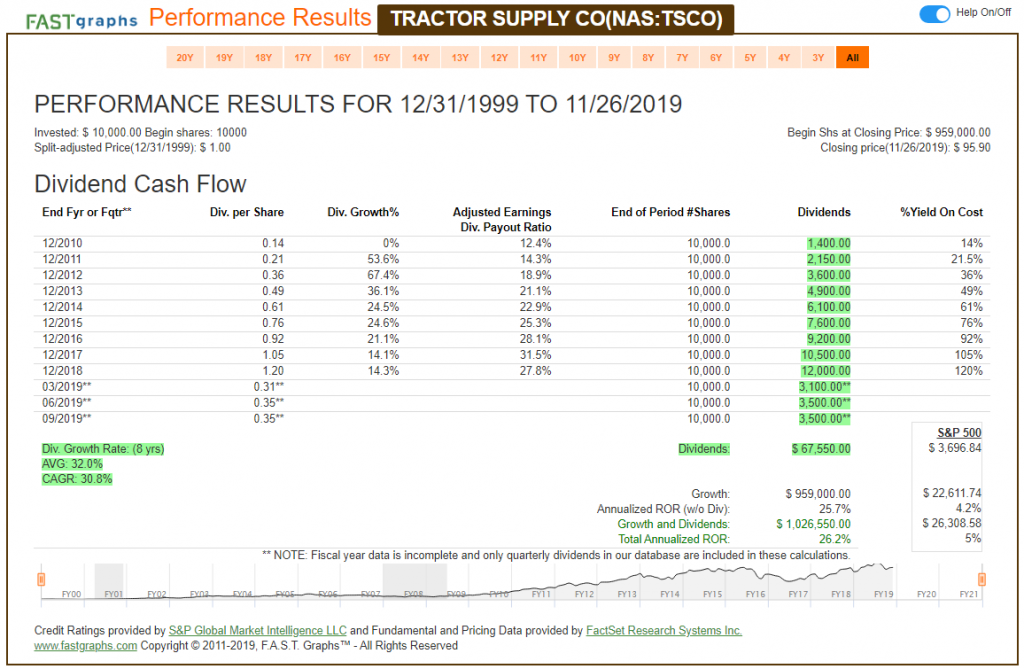

The following two graphs and associated performance charts provide real-life examples of two companies, one historically growing earnings at approximately 10% and one historically growing earnings at approximately 20%. (Note: that I have chosen examples where valuation is in alignment at both the beginning and the end. Therefore, the total annualized returns for both companies closely correlate to their earnings growth rates).

General Dynamics (GD) (approximately) 10% Growth

Tractor Supply Company (TSCO) (Approximately) 20% Growth

FAST Graphs Analyze Out Loud Video Elaborating On When To Buy And When To Sell

Utilizing the two examples above, the following video will elaborate on how to know when to buy and sell based on valuation.

Conclusions

This first article in this series of articles on how to know when and why to buy or sell a business laid down a foundation of principles that future articles will be built upon. It’s important that readers understand that my discussions are predicated on investing in businesses rather than trading stocks.

One of my primary goals is to help investors avoid obvious mistakes. I define these as erroneous decisions that can, and should be avoided by investors. In other words, investors should be able to avoid selling a stock for significantly less than its True Worth™, or perhaps even worse, paying significantly more than the stock is truly worth.

At the end of the day, it comes down to understanding and calculating intrinsic value based on fundamentals. I am not suggesting a method for perfect market timing, which as I previously stated believe to be an impossible objective. Instead, the methods I will be presenting are designed to help investors think their way through the research process and make sound fundamental decisions, rather than impossible perfect ones based on market timing.

Although the methods for valuing a business are based upon similar economic and mathematical principles, not all companies can be valued identically. This offers a clue to the importance of compounding and why it was discussed in this introductory piece. In future articles I will focus on how to calculate sound value for three categories of companies.

I will look at how to value low growth companies, moderate growth companies and high growth companies. Once again, although the formulas for valuing these companies are all based on cash flows (earnings), adjustments and calibrations will be applied to accommodate each category.