Supercharge Your Gold Position With Precious Metal Royalty Companies

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

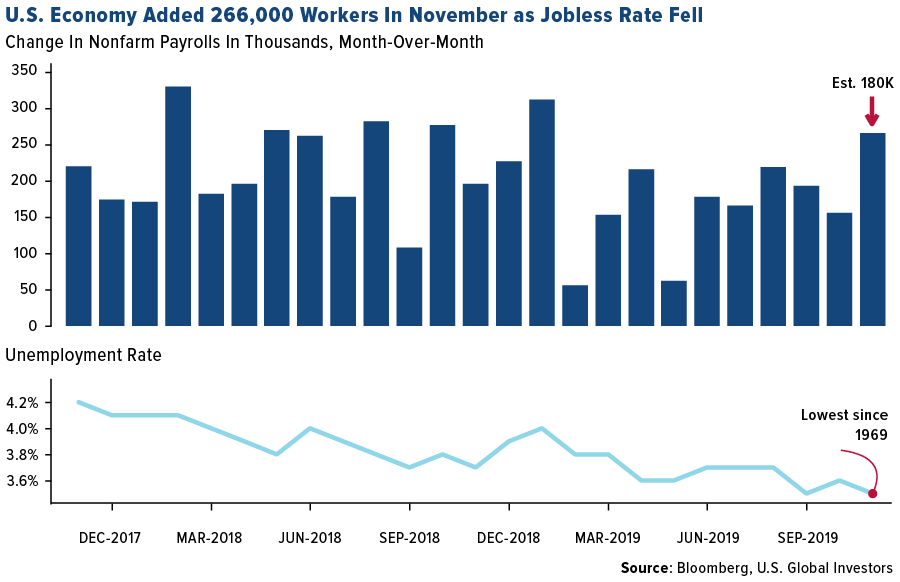

Gold closed down as much as 1.26 percent today on a blowout jobs report that seemed to alleviate investor fears of an impending economic slowdown. The U.S. added as many as 266,000 jobs in November, beating expectations of 180,000, while the unemployment rate ticked down to a 50-year low of 3.5 percent.

The yellow metal remains on sound footing, though, and over the next 12 to 24 months, I see its price advancing further on strong fundamentals. Mean reversion, in particular, is the theme I believe investors should be focused on in 2020 and beyond.

This was the message shared by Bloomberg Intelligence commodity strategist Mike McGlone in a note to investors this week.

The chart below illustrates the 10-year rate of change for gold, the S&P 500 and U.S. trade-weighted dollar. In other words, it shows you how much each asset class has changed from a decade earlier.

As McGlone points out, both the stock market and U.S. dollar have recently increased at their fastest pace since the beginning of the millennium, whereas gold’s rate of change has slumped after hitting its all-time high of $1,900 an ounce in 2011. The law of mean reversion suggests a rerating could occur in the early 2020s.

“The unsustainability of these trends in the third decade is a primary support factor for the dollar price of gold,” McGlone writes.

“Unless the greenback and U.S. stocks are embarking on a new higher plateau,” he adds, “dollar-denominated gold is poised to take the all-time new highs baton.”

Here’s another way to look at it. The left chart below shows the stock market priced in ounces of gold, while the right chart shows the market priced in gold miners, as measured by the NYSE Arca Gold Miners Index. Both bullion and miners are currently below their mean, indicating they’re undervalued relative to the market. For mean reversion to take place, either gold will need to soar to new all-time highs or beyond, or stocks must tumble. In both cases, holding gold, I believe, is rational and prudent.

Royalty of the Precious Metal Industry

There are other ways to get exposure to gold than coins and bars, of course. One of the best ways to “supercharge” your gold position, I believe, is with precious metal royalty and streaming companies. Think Franco-Nevada, Wheaton Precious Metals, Royal Gold and others.

Loyal readers should know that I’ve discussed royalty companies a number of times before. Even so, I still come across new research and data that demonstrates their superiority in the metals and mining industry.

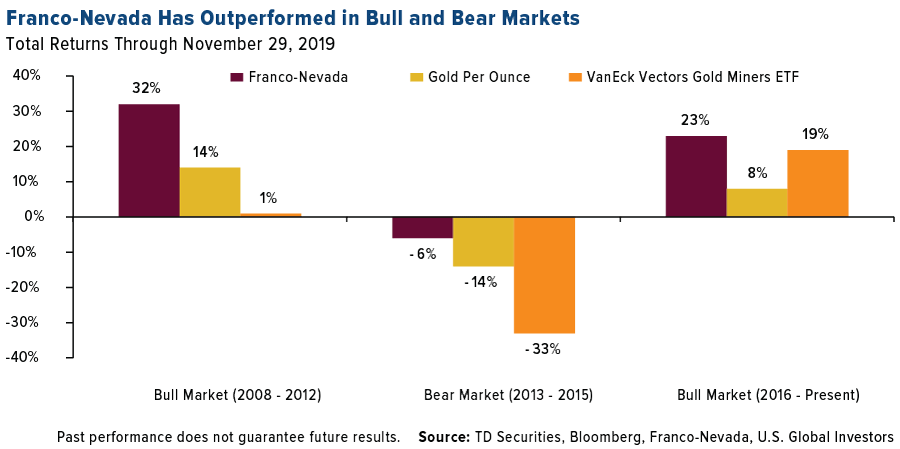

Take a look below. The world’s largest royalty and streaming company with a market cap of $25 billion, Franco-Nevada has outperformed gold bullion and gold equities in both bull markets and bear markets. Investors who like gold do so because they understand that the yellow metal can limit losses in their equity position and reduce volatility. Adding a royalty company such as Franco-Nevada to the mix can be like injecting nitro into your souped-up sports car.

This is because while they enjoy a lot of the upside potential when gold prices are rising, royalty companies share very little of the downside potential with producers and explorers when the metal is in decline. Royalty companies are better insulated from bear markets because they have a diversity of high-quality active mines in their portfolio.

What’s more, they’re not the ones spending money to develop a project. They simply put up the capital, and in exchange they enjoy either a royalty on whatever the miner produces or rights to a stream of metal supply at a fixed, lower-than-average cost.

It’s a win-win for the miner and royalty company, a win-win-win if you also include the investor.

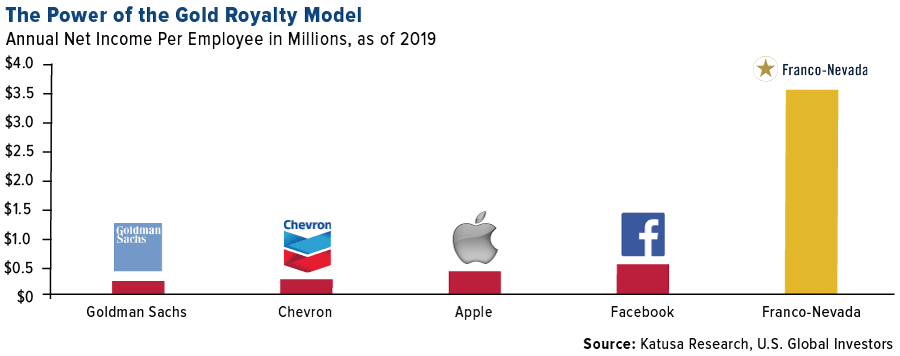

To give you an idea of just how profitable royalty companies can be, look at the chart below, courtesy of Katusa Research. What you see is each company’s net income, or profit, per employee. Some of the world’s most recognizable names are highly profitable, generating around half a million dollars or more per employee after expenses. And then there’s Franco-Nevada, which makes approximately $3.5 million per employee, or seven times Facebook’s net income. It’s in a league all its own.

And it’s not alone. If Royal Gold were in the S&P 500, it would rank second in revenue per employee at $18.4 million, following only Host Hotels & Resorts, which generated an incredible $30.2 million per employee in fiscal year 2018.

It doesn’t hurt that, as of August 2019, Royal Gold had only 23 employees. Compare that to the workforce of major metal producers such as Barrick (18,400 employees), Newmont-Goldcorp (39,600) and BHP Billiton (62,500).

I often recommend the 10 Percent Golden Rule, with 5 percent in physical gold and the other 5 percent in gold equities. But to supercharge your portfolio, I would strongly consider royalty and streaming companies.

Click here to see the estimated year-end distributions for our equity funds.

Gold Market

This week spot gold closed at $1,460.16, down $3.78 per ounce, or 0.26 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 0.23 percent. The S&P/TSX Venture Index came finished up 1.13 percent. The U.S. Trade-Weighted Dollar fell 0.61 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-1 | China Caxin PMI Mfg | 51.5 | 51.8 | 51.7 |

| Dec-2 | ISM Manufacturing | 49.2 | 48.1 | 48.3 |

| Dec-4 | ADP Employement Change | 135k | 67k | 121k |

| Dec-5 | Initial Jobless Claims | 215k | 203k | 213k |

| Dec-5 | Durable Goods Orders | 0.6% | 0.5% | 0.6% |

| Dec-6 | Change in Nonfarm Payrolls | 180k | 266k | 156k |

| Dec-10 | Germany ZEW Survey Current Situation | -22.1 | -- | -24.7 |

| Dec-10 | Germany ZEW Survey Expectations | 0.0 | -- | -2.1 |

| Dec-11 | CPI YoY | 2.0% | -- | 1.8% |

| Dec-11 | FOMC Rate Decision (Upper Bound) | 1.75% | -- | 1.75% |

| Dec-12 | Germany CPI YoY | 1.1% | -- | 1.1% |

| Dec-12 | ECB Main Refinancing Rate | 0.00% | -- | 0.00% |

| Dec-12 | PPI Final Demand YoY | 1.2% | -- | 1.1% |

| Dec-12 | Initial Jobless Claims | 215k | -- | 203k |

Strengths

- The best performing metal this week was palladium, up 2.04 percent as hedge funds increased their net-long position in the futures market to a five-week high. Gold traders and analysts are mostly bullish going into next week in the Bloomberg survey amid mixed signals over progress in the U.S.-China trade war. The yellow metal climbed sharply early in the week after President Trump said that he would be willing to wait another year before striking a deal with China.

- The ISM non-manufacturing PMI fell to 53.9 in November, missing the median estimate of 54.5. Bloomberg reports the decrease was driven by the weakest reading of business activity since 2010. Gold rebounded slightly on Wednesday after ADP data showed fewer-than-expected jobs were added to the economy.

- Australia’s Perth Mint reported a 67 percent increase of sales of coins and minted bars in November from October of 54,261 ounces. This buying is largely driven by purchases by Britons amid uncertainty surrounding Brexit. The Australian Bureau of Statistics shows that Britons bought $5.3 billion of Australian gold in the third quarter of this year, which is the most ever in a single quarter and a 1,400 percent increase over the prior quarter.

Weaknesses

- The worst performing metal this week was silver, down 2.67 percent on little news. According to a government report on Friday morning, the economy added 266,000 jobs in November, the most since January. Gold fell sharply on the news. Gold imports by India fell for a fifth straight month in November amid the slowest economic growth in six years that has curbed demand during peak wedding season, reports Bloomberg. Turkey’s gold reserves continue to fall. The central bank’s holdings fell $102 million from the previous week to now total $26.5 billion. Russia’s gold production from January to September rose 11 percent year-over-year to 268.6 tons.

- Bank of America downgraded Fresnillo to neutral from buy following “fairly disappointing longer-term production guidance”, reports Bloomberg. Centerra Gold says that two employees are missing at its Kumtor Mine in the Kyrgyz Republic after a big rock movement, according to a company statement. Newmont Goldcorp lowered its production forecast and raised its cost outlook. Bloomberg reports that the world’s largest gold miner says output will be 6.7 million ounces in 2020 and all-in sustaining costs will be $975 an ounce. On a positive note, Newmont said it will repurchase as much as $1 billion of its own shares over the next year.

- Burkina Faso has become increasingly dangerous for miners as a wave of militants from neighboring Mali moved eastward. Last month 39 people were killed on a bus convoy that was heading for a Semafo operation. The country is responding by increasing spending on defense and security to 13 percent of its 2020 budget. Bloomberg reports that gold mining and cotton are expected to help push economic growth in the West African nation to around 6 percent next year.

Opportunities

- 2019 is on track to be a 50-year high in central banks’ net gold purchases. Bloomberg Intelligence reports that central banks have been absorbing about 20 percent of global gold mine supply. Based on the gold-to-silver ratio, it looks like silver might have more upside if demand for safe haven assets rises. Bloomberg’s Eddie van der Walt writes that the gold-silver ratio has dropped to 86 from 93 in July and that means silver has outperformed on the back of gold’s gains. UBS analyst Giovanni Staunovo is bullish on palladium and platinum. Staunovo wrote in a December 5 report that palladium will likely enter its ninth straight year of market deficit in 2020 and could climb above $2,000 an ounce. Even as platinum is set to enter a surplus, its price could be driven by gold. “As platinum is highly correlated to gold, our bullish view for gold should mean higher platinum prices, which we expect to trade at around $1,000 an ounce next year.”

- Zijin Mining Group Co. has agreed to buy Continental Gold in a rare all-cash deal worth C$1.37 billion – the second big takeover in a few weeks of a junior Canadian gold miner. Bloomberg reports the offer reflects a 29 percent premium to the Continental Gold share price from the past 20 days and that major shareholder Newmont Goldcorp was supportive of the deal. In hostile M&A news, Centamin Plc rejected Endeavour Mining Corp.’s $1.9 billion takeover offer saying that it undervalues its assets, reports Bloomberg News. Centamin has been a takeover candidate since the size of its Egyptian mine was discovered at the start of the decade, though the company has faced many operational setbacks.

- Kinross Gold has been busy raising cash. Kinross announced this week that it has agreed to sell its remaining shares of Lundin Gold for C$150 million to Newcrest Mining and the Lundin Family Trust. Kinross earlier announced that it has sold its royalty portfolio to Maverix Metals for $74 million.

Threats

- ABN Amro strategist Georgette Boele says they see gold weakening in the coming weeks and months with a price average of $1,400 an ounce. However, they do expect prices to increase to $1,600 by December of 2020. Before this happens, extreme net-long positioning would clear up because “these positions currently hang over the market and prevent prices from moving substantially higher.”

- Another sign of a weakening economy was released last week. The ISM manufacturing PMI unexpectedly declined to 48.1 in November, below the median forecast of 49.2. The reading remains below the 50 level that indicates activity is shrinking.

- Bloomberg’s Enda Curran writes that cheap borrowing costs have sent global debt to another record - $250 trillion of government, corporate and household debt. This level is almost three times global economic output and policymakers are now grappling with how to keep economies afloat – with more debt? According to Cornerstone Macro’s head of technical analysis Carter Worth, his S&P 500 chart signals a 5 to 8 percent decline in the coming months. Bloomberg reports that the S&P 500 fell 1.4 percent on Tuesday, pushing it below an upward trend line established in October.

Index Summary

- The major market indices finished mix this week. The Dow Jones Industrial Average lost 0.13 percent. The S&P 500 Stock Index rose 0.22 percent, while the Nasdaq Composite fell 0.10 percent. The Russell 2000 small capitalization index gained 0.69 percent this week.

- The Hang Seng Composite gained 0.84 percent this week; while Taiwan was gained 1.05 percent and the KOSPI fell 0.29 percent.

- The 10-year Treasury bond yield rose 6 basis points to 1.84 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector of the week, increasing by 1.52 percent versus an overall increase of 0.12 percent for the S&P 500.

- Ulta Beauty was the best performing S&P 500 stock for the week, increasing 12.12 percent.

- Ulta Beauty stock rallied after it issued positive financial results for its third quarter of fiscal 2019, reports Yahoo! Finance. The operator of beauty stores posted adjusted earnings per share of $2.23, a 3.2 percent increase from the prior quarter, on net sales of $1.68 billion.

Weaknesses

- Industrials was the worst performing sector for the week, decreasing by 1.09 percent versus an overall increase of 0.12 percent for the S&P 500.

- Apache was the worst performing S&P 500 stock for the week, falling 10.28 percent.

- Apache’s stock plunged to an 18-year low on Monday, writes MarketWatch, after the oil and natural gas producer provided a disappointing update of its first exploratory well in Block 58 offshore Suriname.

Opportunities

- It looks like Diamondback Energy is starting a new chapter, reports Nasdaq. The energy company spent the past five years building out a large-scale drilling operation in the oil-rich Permian Basin. As a result, the company has rapidly grown its oil production in recent years through a combination of acquisitions and organic drilling, the article explains. However, it plans to slow its investment pace in the new year. That will enable it to turn its focus toward generating free cash flow, which was one of the key themes on its third-quarter conference call. That could make it a big winner next year.

- Expedia’s CEO and CFO are leaving and the stock market seems to like the move, reports Barron’s. Shares rose on Wednesday morning after the travel-booking company announced that its chief executive and chief financial officer are leaving, after poor financial results led to disagreements with the board on strategy.

- UBS analysts placed a buy rating on Jacobs Engineering saying: “We expect the next leg up in the stock to be driven by cleaner earnings reports with fewer adjustments, improved cash flow, and results approaching JEC's identified earnings potential. We think earnings will be driven by steady core growth, margin initiatives, some M&A, and buybacks. JEC is in the middle of shifting its business mix to higher-margin opportunities.”

Threats

- Oil and gas stocks have never fallen for three straight years in the S&P 500 Energy Index’s three-decade history. This year, however, that streak is at risk of ending. The industry gauge was up only 1.2 percent for the year, as of Thursday, after dropping as much as 19 percent from a peak in April. Energy had the worst year-to-date performance among the S&P 500’s 11 main industry groups through Thursday, when it lagged behind the broader index by 23 percentage points.

- Although Zoom Video Communications raised its full-year revenue outlook, RBC Capital warns that the narrowing upside surprise on revenue compared to last quarter, and the divergence of billings and RPO growth rates may serve to pressure the share price in the near-term. Analyst Alex Zukin cut his price target by $20 to $75 per share.

- Yext, a New York City technology company, plunged as much as 23 percent on Friday after disappointing third-quarter results and a forecast cut, its biggest drop since going public in 2017. Yext said the launch of its new search product disrupted its sales execution and prolonged purchasing cycles.

The Economy and Bond Market

Strengths

- Hiring roared back in a big way in November. U.S. employers added 266,000 jobs last month, topping all estimates in a Bloomberg survey, according to Labor Department report Friday. The surge was boosted by General Motors Co. workers returning to work after a 40-day strike.

- American consumer attitudes improved markedly in December, the University of Michigan said Friday in a preliminary estimate. The University of Michigan’s gauge of consumer sentiment rose to a preliminary December reading of 99.2 from a final November reading of 96.8. Economists polled by MarketWatch expected a December reading of 96.9.

- The jobless rate dipped to 3.5 percent and average hourly earnings climbed 3.1 percent from a year earlier, beating forecasts.

Weaknesses

- Manufacturing activity continued to lag in November amid a decline in inventories and new orders, according to the latest ISM Manufacturing reading released Monday. The reading came in at 48.1 versus an expectation of 49.4 and the previous month’s reading of 48.3. Though the level is usually reported as a simple number, it actually denotes the percentage of manufacturers planning to expand operations. A reading below 50.0 represents contraction; November was the fourth straight month below the expansion level.

- U.S. services sector activity slowed more than expected in November amid lingering concerns about trade tensions and worker shortages, which could revive fears about the economy’s health. The Institute for Supply Management (ISM) said on Wednesday its non-manufacturing activity index fell to a reading of 53.9 in last month from 54.7 in October. Economists polled by Reuters had forecast the index dipping to a reading of 54.5 in November.

- Spending on U.S. construction projects fell 0.8 percent in October, dragged down by declines in apartment and multi-family homebuilding. Private construction spending declined 1 percent in October, the Commerce Department said Monday. That follows another significant 1.1 percent decline in September. Overall private residential construction dipped 0.9 percent, with multifamily projects declining 1.6 percent in October after a 2.1 percent decline in September.

Opportunities

- The spotlight next week will fall on the Federal Reserve meeting on Wednesday. Markets are confident rates will be kept unchanged, pricing in no chance of a rate cut, as policymakers have been clear that they will stay on hold for some time.

- Retail sales numbers for November will come out on Friday. They are expected to move up marginally to 0.4 percent from last month’s 0.3 percent.

- Consumer price index (CPI) inflation figures for November will come out on Wednesday before the Fed decision. The forecast is for inflation to ramp up to 2 percent on a year-over-year measure, up from the previous 1.8 percent reading.

Threats

- In China, the world’s second-largest economy, trade data for November will be released over the weekend, and inflation figures for that month will follow on Tuesday. Markets typically pay most attention to exports and producer prices – the former seen as a gauge of global demand and the latter of factory activity in China. While these could be important for global risk appetite, the main factor will be what happens in the trade saga. The coming week is crucial because unless a “phase one” deal is reached – or at least appears imminent – then the Trump administration has stated it will slap tariffs on almost all remaining imports from China on December 15.

- On the data front out of the Eurozone, Germany’s ZEW survey for December is due on Tuesday. Given the country’s recent economic weakness, a disappointing survey would further unsettle investors.

- State and local governments’ frenzy to seize on lower interest rates could leave them issuing new bonds next year at a faster pace than they’re paying them off, causing an increase in the net supply of outstanding securities. Usually, that’s viewed as a negative in the $3.8 trillion municipal market, given that the increase in supply can exert a drag on prices.

Energy and Natural Resources Market

Strengths

- The best performing major commodity for the week was crude oil, which gained 7.05 percent with Saudi Arabia pledging additional oil production cuts post this week’s OPCE+ meeting. Cleveland-Cliffs Inc., the largest U.S. miner of iron ore, is set to buy AK Steel Holding Corp. for $1.1 billion. Bloomberg reports that this is the biggest takeover of a U.S. steelmaker since President Donald Trump imposed tariffs to protect the domestic steel industry. Cliffs CEO Lourenco Goncalves says the takeover is “creating a premier North American company, self-sufficient in iron ore pellets and geared toward high value-added steel products.”

- American uranium miners rose on Thursday after a White House task force recommended that President Trump direct the government to buy more uranium from domestic producers, reports Bloomberg News. Energy Fuels Inc. rose 18 percent and Ur-Energy Inc. rose 16 percent on the positive news.

- Blackrock, the world’s largest money manager, just raised $1 billion from over 35 institutional investors for its third global renewables fund focusing on wind, solar and battery-storage projects, reports Bloomberg. Blackrock’s global head of renewable power David Giordano says renewables are becoming one of the most active sectors in infrastructure. This is a strong sign of investor demand for cleaner energy projects.

Weaknesses

- The worst performing major commodity for the week was wheat, which fell 3.18 percent, giving back much of the prior week’s gain. Oil and gas stocks that make up the S&P 500 Energy Index might be on trend to fall in price for a third straight year, something that has never happen in their 30-year history. The benchmark is down 19 percent from its peak, set earlier in the year but is now only up 1.2 percent. There is a 23 percent gap between the energy stocks and the S&P 500 so far this year. If that persists, it would be the fourth time in six years that the energy index has lagged the market by more than 20 percent. OPEC reached a new deal that adjusts official production targets, but removes only a few barrels from the market that is forecast to return to a surplus in early 2020. On Friday morning, Saudi Arabia surprised the markets by announcing even deeper production cuts, hoping that Saudi Aramco will surge to a $2 trillion valuation.

- A researcher at China’s economic planning department said at the BloombergNEF summit in Shanghai this week that LNG consumption in 2021-2025 will grow at a slower pace than it has in the current five-year period. China is the driver of global LNG use and has expanded its use 9.5 percent so far in 2019, which is down from 18 percent in 2018, reports Bloomberg News. The nation’s slowing economy has prompted the government to focus less on pollution control, which was previously one of the big demand drivers for gas.

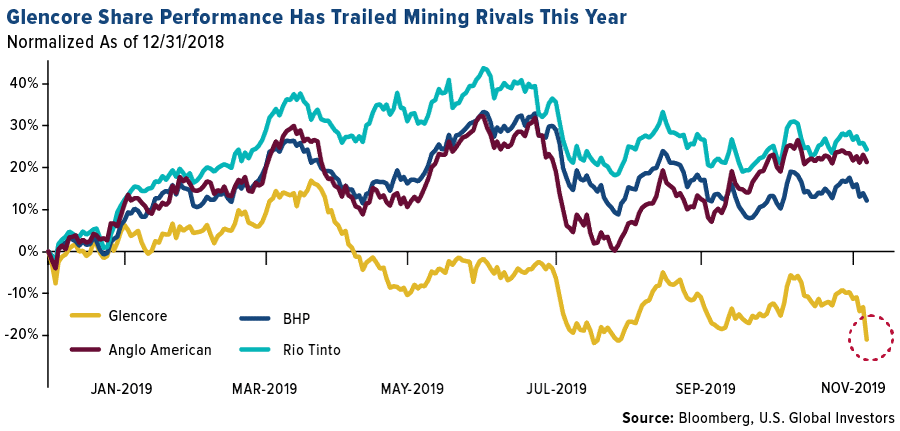

- Glencore Plc, the world’s biggest commodities trader, is being investigated by U.K. authorities for bribery. Shares fell 8.6 percent in London on the news, reports Bloomberg. Glencore is already facing corruption probes in the U.S. and Brazil. Hunter Hillcoat, an analyst at Investec Securities Ltd., says, “Glencore was already trading at a discount because of the Department of Justice, but when this news comes out it gets whacked again.”

Opportunities

- Trina Solar Ltd. Chairman Gao Jifan said in an interview this week that annual solar capacity additions in China are forecast at 50 gigawatts in 2021 and then increasing 10 percent every year through 2025, reports Bloomberg. This is a positive turnaround for the solar industry in China after installations fell in 2018 and 2019 due to the removal of government subsidies. The country is also working to boost demand for electric cars. China raised its 2025 sales target for electrified cars, saying it wants 25 percent of all new cars sold to be electric.

- Orsted A/S inked a deal with Covestro AG to sell 100 megawatts of power from a German wind farm in the North Sea, reports Bloomberg. The companies said that this is the largest corporate purchase agreement ever for offshore wind. Orsted says that this is an example of how massive renewable power projects can secure cash flow without government subsidies.

- Apple is making big steps to achieving its greenhouse gas reduction goal. The tech giant is taking delivery this month of the first batch of carbon-free aluminum produced by a venture between Rio Tinto Group and Aloca Corp., reports Bloomberg. The new technology emits pure oxygen when producing the metal rather than carbon.

Threats

- President Trump re-imposed steel and aluminum tariffs on Argentina and Brazil, saying that the nations are weakening their currencies to the detriment of American farmers, reports Bloomberg. Argentina and Brazil had become alternative suppliers of soybeans to China, which has taken away market share from American farmers.

- The World Meteorologic Organization (WMO) says that the world’s average temperature is moving toward a gain of 3 to 5 degrees Celsius by the end of the century – far from targets to contain global warning to 1.5 degrees. WMO Secretary General Petteri Taalas said “if we wanted to reach a 1.5 degree increase we would need to bend emissions and at the moment countries haven’t been following on their Paris pledges.”

- Carmakers globally are cutting more than 80,000 jobs in the coming years, according to data compiled by Bloomberg News. Daimler AG and Audi both announced around 20,000 job eliminations in the past week. Researcher IHS Markit says the global auto industry will make 88.8 million cars and light trucks in 2019, a 6 percent drop from a year ago. Auto companies are working to cut costs due to lower demand and a shift toward greener car technology.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 1.84 percent. The country’s banking regulator eased measures on how banks classify credit to once-troubled companies, helping lenders to potentially avoid adding more non-performing loans to their books.

- The Hungarian forint was the best performing currency this week, gaining 1.49 percent.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 2.62 percent. The country’s central bank maintained its longest interest rate pause on Wednesday, playing down concerns over a slowing economy and signaling no change in monetary policy until the end of its term.

- The Turkish lira was the worst performing currency in the region this week, losing 65 basis points. Turkey’s decision to test the S-400 anti-aircraft missile system purchased from Russia sparked fresh talks in the U.S. Senate to imposed sanctions on the NATO ally mandated by the current law.

- Consumer staples was the worst performing sector among eastern European markets this week.

Opportunities

- The world’s biggest natural gas exporter and one of the globe’s top consumers of the fuel cemented their energy cooperation on Monday with the launch of Russia’s giant Power of Siberia pipeline to northern China, writes Bloomberg. The 3,000-kilometer link, which has become a symbol of President Vladimir Putin’s pivot to the fast-growing economies of Asia as relations deteriorate with the West, begins shipping gas from Russia’s enormous reserves in its eastern regions to the border.

- Eurozone factory activity rose to a three-month high last month. The Purchasing Managers’ Index for the 19-nation euro region rose slightly to 46.9 in November as confidence improved and a drop in new orders slowed. Composite PMI stabilized at 50.6 in November, above initial 50.3 reading. France remained the region’s top performer posting “solid” growth, with Ireland and Spain also expanding.

- In Turkish stocks this year, small is beautiful, thanks to local investors, writes BN's Tugce Ozsoy. Even as international fund managers have walked away from the market in recent months, domestic buyers poured in, leading to a homegrown rally that has sent shares of smaller companies soaring.

Threats

- The U.S.-France trade tiff has deepened. France says the European Union will retaliate if the U.S. slaps tariffs on $2.4 billion of its products, including sparkling wine, cheeses, handbags and makeup. The U.S. threat is payback for a French tax on online revenue that hits Google, Apple, Facebook and Amazon.

- Turkey has just tested radar systems for the Russian S-400 missile-defense technology, writes Bloomberg, providing further ammunition for U.S. lawmakers who favor punishing their NATO ally for the purchase. Such measures, if imposed, could limit any gains in Istanbul stocks, leaving investors facing geopolitical risks disproportionate to their potential returns.

- German factory orders unexpectedly fell, suggesting Europe’s largest economy is still struggling to overcome a manufacturing slump and fend off recession. Demand dropped 0.4 percent in October, defying estimates for a 0.4 percent gain. It was driven by weak demand for investment goods within Germany and outside the euro area. Orders were down 5.5 percent from a year earlier in October, highlighting the damage global trade conflicts have inflicted on German industry.

China Region

Strengths

- The best performing index in the region was Indonesia’s Jakarta Composite, which jumped 3.02 percent on the week, handily outpacing its regional peer indices.

- Industrials and information technology were the top performers in the Hang Seng Composite on the week, climbing 3.83 and 1.48 percent, respectively.

- China’s official manufacturing PMI rose to 50.2 last month, marking the first reading above the 50 level since April. The Caixin factory gauge also beat estimates, clocking in at 51.8. Official non-manufacturing PMI came in at 54.4, ahead of estimates for a 53.1 reading, and the Caixin services PMI also beat handily, with a 53.5 reading versus expectations for only a 51.2 print.

Weaknesses

- The worst performing index in the region was Thailand’s SET Index, which fell by 1.97 percent amid weaker data.

- Energy was the worst performing sector in the HSCI on the week, falling 76 basis points.

- Following Thailand’s recent GDP disappointment, the Markit Thailand Manufacturing PMI dipped into contractionary territory at a 49.3 reading, down from 50.0 in October.

Opportunities

- A Phase One U.S.-China trade deal remains an opportunity, and while President Trump said recently that he has no deadline of any sort, reports nonetheless swirl that the two sides are “close”—read as positive by markets—and late this week China waived retaliatory tariffs on imports of U.S. pork and soy, which is certainly not a negative. Bloomberg News reported that National Security Advisor Robert O’Brien told Fox News that the two sides are nearing a deal.

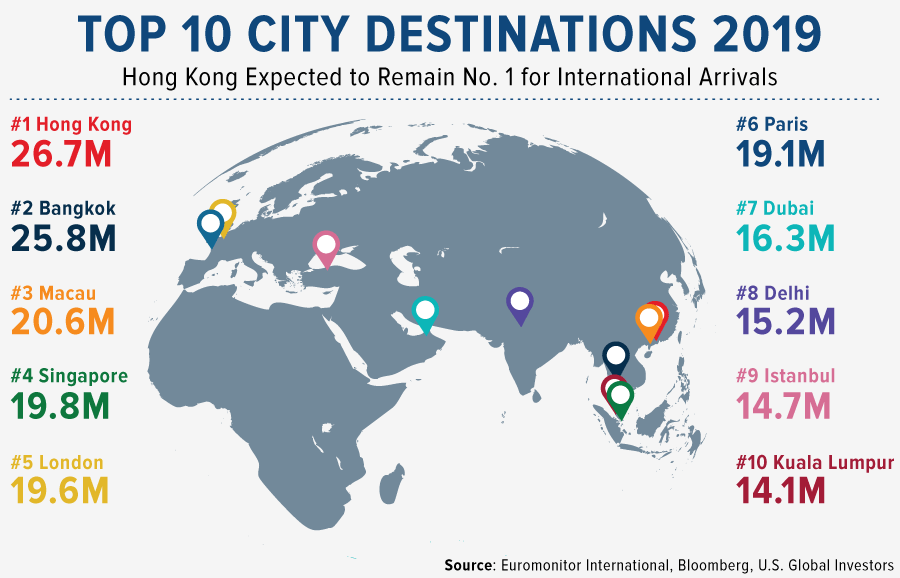

- One upside to the issues of Hong Kong, perhaps, might be discernable in tourist arrivals to Singapore, which leaped to a record 5 million in the third quarter.

- Hong Kong remains troubled by ongoing protests, to be sure, and there’s no doubt that changes in visitor patterns and traffic have cut deeply into numbers like HK’s Retail Sales and Visitor Arrivals, etc. But note well: life goes on in the meantime, and according to a Bloomberg Spotlight chart this week that featured data from Euromonitor International, “Hong Kong is likely to hold on to its status as the world’s most popular city with international visitors in 2019, despite months of political unrest that led to a sharp drop in tourist numbers.” The other cities in the top five? Here they are in order, starting with a close second: Bangkok, then Macau, followed by Singapore, and finally, London. There’s some food for thought.

Threats

- In keeping with this section’s views, we again reiterate that trade war escalation must remain a threat until it isn’t. While progress of late appears more positive than otherwise, as mentioned above—especially given the agricultural waivers and comments from O’Brien—there remains a significant risk that sentiment and prices could deteriorate quickly if there is no deal of any sort between the United States and China.

- The situation in Hong Kong continues to remain problematic, with weekend protests lined up and some talk of a possible strike next week. Time will tell, but the tension continues and thorny issues remain resolved. Following last week’s signing of the new HK bill into law and a HK protester march to the U.S. embassy over last weekend as a measure of thanks to the United States, China vowed to sanction some U.S. rights organizations and suspend further Hong Kong port visits by U.S. Navy ships. This week the House of Representatives passed the Uighur Act, banning exports to China of items that can be used for surveillance of individuals, including facial and voice-recognition technology, which may exacerbate things further, although it can hardly come as a surprise at this point. The Act—which yet requires Senate passage and a presidential signature before it could become U.S. law—also calls, for the first time, for sanctioning a member of the powerful Chinese politburo.

- Related to the political issues in Hong Kong are, of course, the economic ones, some of which have already been hinted at above. Retail sales in the SAR suffered a record contraction in October, by value contracting some 24 percent year over year and marking a fourth month of double-digit declines. By volume, sales fell 26 percent percent, also a record. Financial Secretary Paul Chan said Hong Kong will probably have its first budget deficit since 2004, according to a Bloomberg News report earlier this week, which noted that the economy has sustained damage equivalent to 2 percentage points of output growth and that the HK economy is currently forecasted to contract 1.3 percent in 2019 from a year earlier.

Blockchain and Digital Currencies

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performing for the week ended December 6 was Blockium, up 423.62 percent.

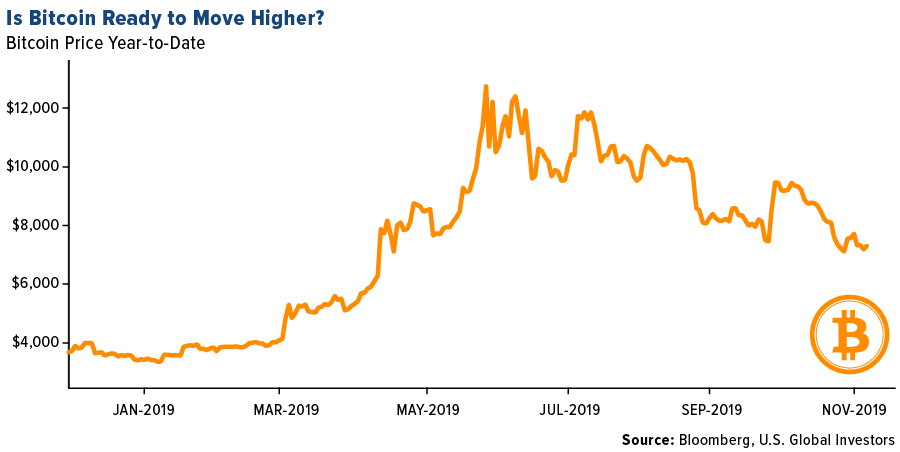

- Mike McGlone, Bloomberg Intelligence commodity strategist, wrote this week that increasing adoption of bitcoin has titled his team’s price outlook on the coin favorably for 2020 and the next decade. “This year was part of its transition toward the crypto-market version of gold. The maturation process should continue, notably as volatility declines.” McGlone adds that bitcoin sustaining below $6,500 is unlikely and $10,000 is the initial resistance for 2020.

- Cryptographic research hub Matter Labs has unveiled Layer 2 scaling solutions for Ethereum payments, reports CoinDesk. On Thursday, the testnet of ZK-Sync was released, in which the firm claims is a step toward making blockchains compete with centralized systems for handling millions of transactions a day.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performing for the week ended December 6 was FirmaChain, down 99.92 percent.

- Nearly 70 cryptocurrency-focused hedge funds are closing this year, according to San Francisco-based Crypto Fund Research. As Bloomberg reports, that means the number of new funds launched is less than half the amount started in 2018. One reason for the retrenchment is the volatile year that digital currencies have had. Despite the swings, advocates like Fidelity Investments continue to move forward with initiatives making it easier to own cryptocurrencies.

- According to filings, Great North Data (a firm that runs bitcoin mining and A.I. processing data centers in Canada) has filed for bankruptcy. While the firm has 4.6 million Canadian dollars in assets, it owes creditors CA$13.2 million. As reported by CoinDesk, the data processor also owes CA$313,718 to the Business Investment Corporation of the provincial Newfoundland and Labrador government.

Opportunities

- Gemini, a top global cryptocurrency exchange, has hired Julian Saqyer, a former CEO and co-founder at United Kingdom-based Starling Bank, to lead Gemini Europe, reports CoinTelegraph. An announcement by Gemini president Cameron Winklevoss explains that Sawyer is joining the exchange with a total of 20 years’ experience at growing financial service organizations. For example, prior to Starling, he founded Bluerock Consulting, a financial management consultancy, which he sold in 2012.

- BlockFi, the cryptocurrency lending service, is expanding into trading with an unusual, zero-fee model, writes CoinDesk. The service will have a different profit model, the article explains: the money will be coming from selling data on the users’ trades to big institutional crypto firms that, in turn, will act as market makers at BlockFi, providing liquidity.

- KT Corporation, South Korea’s largest telecoms provider, is boosting a partnership with Cina Mobile targeting blockchain technology and 5G roaming, writes CoinTelegraph. The two companies are working on a blockchain system which will allow them to save time and costs when computing roaming charges for mobile users, the article explains.

Threats

- State Street bank has cut hundreds of developer jobs as it rethinks its blockchain strategy, reports CoinDesk. People familiar with the matter explain that the focus is now more on digital assets such as tokenized stocks and bonds through to cryptos, rather than the distributed ledger technology (DLT).

- On December 4, the Financial Stability Oversight Council (FSOC) highlighted in a report the potential problems resulting from stablecoins gaining wider recognition. In the report, as shared by CoinTelegraph, the regulators stated “If a stablecoin became widely adopted as a means of payment or store of value, disruptions to the stablecoin system could affect the wider economy. Financial regulators should review existing and planned digital asset arrangements and their risks, as appropriate.”

- One of the original co-founders of payments company Circle has quit, reports CoinTelegraph. Co-CEO and co-founder Sean Neville launched Circle with Jeremy Allaire in 2013 and “has presided over its metamorphosis in the ensuing years, including a pivot away from bitcoin and the acquisition of crypto exchange Poloniex last year,” the article explains. Circle, however, is now selling Poloniex and Neville described the current event as forming an appropriate time to switch roles. He will now transition to a post on the company’s board of directors in January.

Airline Sector

Strengths

- In the quarter ended September 30, Singapore Airlines Ltd. saw a 68 percent rise in profit year-over-year. The carrier reported that net income was around $70 million and that sales climbed 3.9 percent. Singapore Air has added more fuel-efficient A350s and 787-10s to its fleet to help mitigate uncertainty related to fuel costs.

- IAG SA, parent company to British Airways, is set to buy Spanish carrier Air Europa for $1.1 billion in a push to strengthen Madrid as a rival to European hubs. Daniel Roeska, analyst at Berstein, wrote in a note to clients that the deal is “strategically sensible” and will give IAG 26 percent market share of the Europe-Latin America routes, up from 19 percent.

- Air Arabia ordered a whopping 120 single-aisle A320 aircraft worth approximately $14 billion at the Dubai Air Show, reports Bloomberg News. Air Arabia says the deal is a “game-changer for Air Arabia’s business” as the new planes will allow the discount carrier to expand into Southeast Asia and Africa. This is a big victory for Airbus as rival Boeing continues to see orders cancelled due to its two high profile crashes in the last 18 months.

Weaknesses

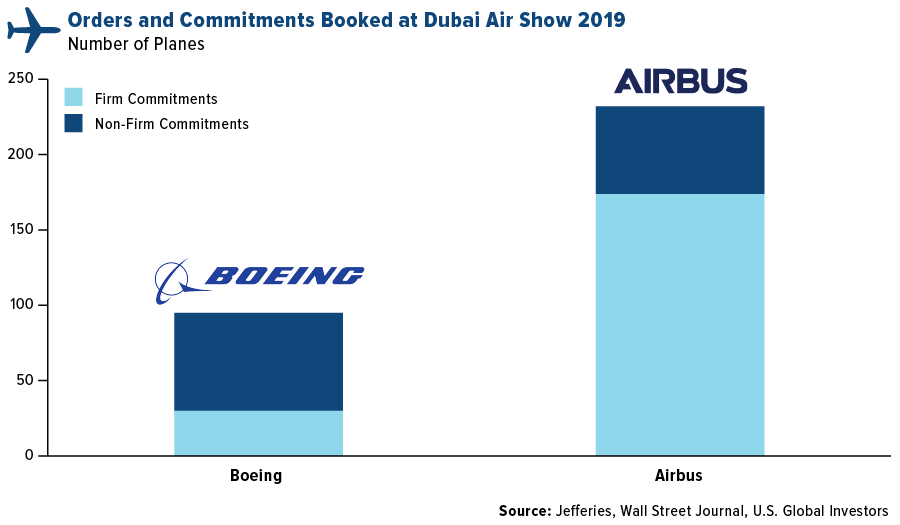

- Although Airbus scored big deals, the biennial Dubai Air Show, known as one of the largest air shows in the world, had a lackluster year overall. The three-day show in mid-November said on site orders totaled $54.5 billion this year, down significantly from $113.8 billion in 2017. Airbus landed orders and non-firm commitments for 232 commercial planes versus Boeing’s 95. Although Boeing saw a big drop in sales due to its ongoing issues with the737 MAX jets, the fact that it secured orders for more of the jet is a positive sign.

- The Boeing 737 MAX 8 jet that was involved in two deadly crashes remains grounded with an unknown return to service date. Many expect the jet to be in the air again in 2020, but airlines that fly the plane have it removed from flight schedules until at least March. On November 25, Boeing quietly unveiled a new version of the jet, the Max 10, which can hold 30 more passengers than the Max 8. The Max 10 is Boeing’s competition to the Airbus A321 XLR, which was a star of the Dubai Air Show.

- One of the world’s fastest growing carriers, IndiGo, has been forced to ground some of its Airbus SE A320neo planes for engine upgrades, which could impede its expansion, reports Bloomberg News. India’s Directorate General of Civil Aviation said that a series of problems involving the carrier’s jets, including in-flight shutdowns, must be addressed by upgrading engines. For every jet that IndiGo adds to its fleet, it must ground another jet, essentially preventing it from adding new routes or increasing frequencies until all engine problems are resolved.

Opportunities

- According to Boeing, the Latin America aviation market will more than double in 20 years and drive a need for 2,960 new planes due to Brazil’s recovering economy and discount carriers boosting demand. Brazil makes up 40 percent of the region’s market and will grow 4 percent to 5 percent in the next year as economic growth slowly resumes and capacity returns, reports Bloomberg News. International Air Transport Association (IATA) data shows that the number of passengers carried by Latin America airlines have more than doubled in the last decade.

- The first blockchain-based airline tickets were issued this week. German airline Hahn Air flew passengers with blockchain-powered tickets on a routine flight between Dusseldorf and Luxemburg, reports Reuters. The airline partnered with Winding Tree, an open-source travel distribution platform, to issue the tickets. Hahn Air head of corporate strategy and government and industry affairs Jorg Troester said “it is important to look into the future to understand how can we make distribution faster.”

- As airlines are under growing pressure to reduce carbon emissions, especially in Europe, some carriers are taking initial steps. EasyJet announced that it will spend 25 million pounds ($32.3 million) on planting trees and protecting deforestation with the objective of removing as much carbon dioxide from the atmosphere as its fleet emits, reports Bloomberg News. EasyJet CEO Johan Lundgren said “it’s not to say that this is the perfect solution, we know it’s an interim step before new technologies come into play.” Aircraft are becoming increasingly fuel efficient, but hybrid and fully electric jetliners are not expected until the 2030s.

Threats

- The U.S. Federal Aviation Administration (FAA) downgraded Malaysia to a category 2 nation, banning the nation’s carriers from setting up new flights to America. The FAA said that Malaysia does not currently meet International Civil Aviation Organization safety standards. It was awarded a category 1 status in 2003. Bloomberg reports that the only other category 2 countries are Bangladesh, Thailand, Costa Rica, Curacao and Ghana.

- The airline operating the first Boeing MAX 737 crash has largely escaped criticism over its role in causing the disaster. Lion Air, a low-cost Indonesian carrier, has a long track record of overworking pilots, faking training certifications and forcing pilots to fly planes they worried were unsafe, according to an investigation by the New York Times. Lion Air Flight 610 crashed shortly after takeoff in part due to a flawed anti-stall system, but new details about the crash show that other factors contributed including improper maintenance, overworked pilots and improper recordkeeping of the planes issues. The airline, which is the world’s fastest growing and benefits from strong political connections, has not fully acknowledged the concerns regarding its safety practices.

- Allen Onyema, a Nigerian businessman who is owner and CEO of Air Peace, was indicted by U.S. authorities on charges of fraud and money laundering, reports Bloomberg News. A statement by the U.S. Department of Justice says that Onyema moved more than $20 million from Nigeria to the U.S. involving fake documents based on the purchase of airlines.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All