The Hang Seng Index, tracking Hong Kong's stock market, recently turned 50 years old. Launched in 1969—two years after Hong Kong's tumultuous political riots of 1967—the Hang Seng Index has been a strong performer, generating annualized returns of 12.76% since inception through November 30, 2019.1 In our current era of trade tensions, political protests and geopolitical risks, it is worth remembering that investment gains have often occurred against a backdrop of political and economic uncertainty.

The lessons of 1969 remain relevant half a century later. As global investors look to Asia, some see only short-term risks. At Matthews Asia, we look beyond the headlines to find long-term opportunities. We believe an objective look at Asia shows that the region may have reached a turning point. While the U.S. has been overstimulated by a decade of quantitative easing and, more recently, tax cuts for the upper classes, Asia remains understimulated and, in our view, primed for growth.

Taking the Long View

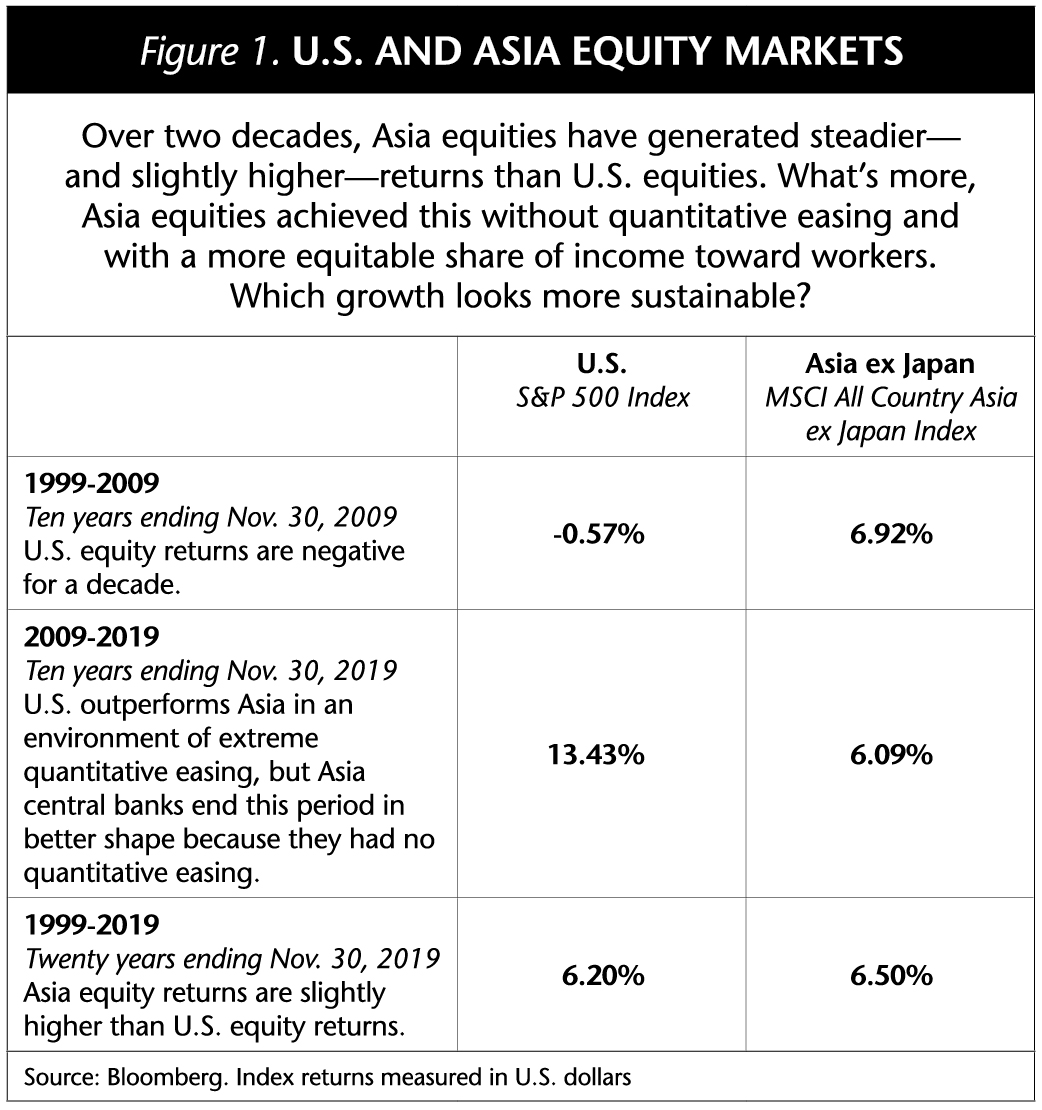

Since the start of the millennium, Asia's stock markets have outperformed the U.S., driven by earnings performance, in turn driven by superior economic growth. (See Figure 1.) Why does that seem so surprising to many? Because the conventional wisdom is that the U.S. market has trounced all-comers. And indeed, if one's view is restricted to the past decade, the U.S. has outperformed Asia ex Japan handsomely; for the first 10 years of this century, however, Asia outperformed by an equally impressive amount. That is quite a conundrum and one that any asset allocator should try to understand.

I have argued that the U.S. stock market's performance in the recent past may be less impressive. The U.S. has been willing to sacrifice income equality for the sake of corporate profit margins and a rising stock market. This was the case even before a corporate-friendly tax program was initiated by the current administration. In contrast, Asia's market performance may be less dismal than it seems as policymakers in the region have been unwilling to trade short-term profits for social stability. So Asia goes into the global deceleration with already-lean companies and a valuation advantage. But it is true that the desire of Asia's policymakers to maintain a better balance in society has been weighing on corporate profit growth and on market performance.

Outperformance is partly due to starting points. After all, Asia's impressive performance in the first decade of the century came from the aftermath of the Asian financial crisis. Asia was clearly depressed relative to the rest of the world and as it was working through this, any great reflation benefited other emerging markets. Once Asia had taken the medicine prescribed by the IMF, and gone through a deflationary period, it emerged as a region hungry for growth. Now, think about it: Couldn't we say much the same about the U.S.? The recovery from its own financial crisis has been slow but steady. Some might say hampered by overly tight fiscal policy; although, the hawks would tell you that is the reason for the post-crisis expansion's longevity. But like Asia, at the end of its own post-crisis expansion, the U.S. economy now seems to be back at full capacity, with all the usual worries over inflation and rising rates seeming to have more justification than they have had in the recent past. Asia, on the other hand, has been running below potential—and has room to accelerate.

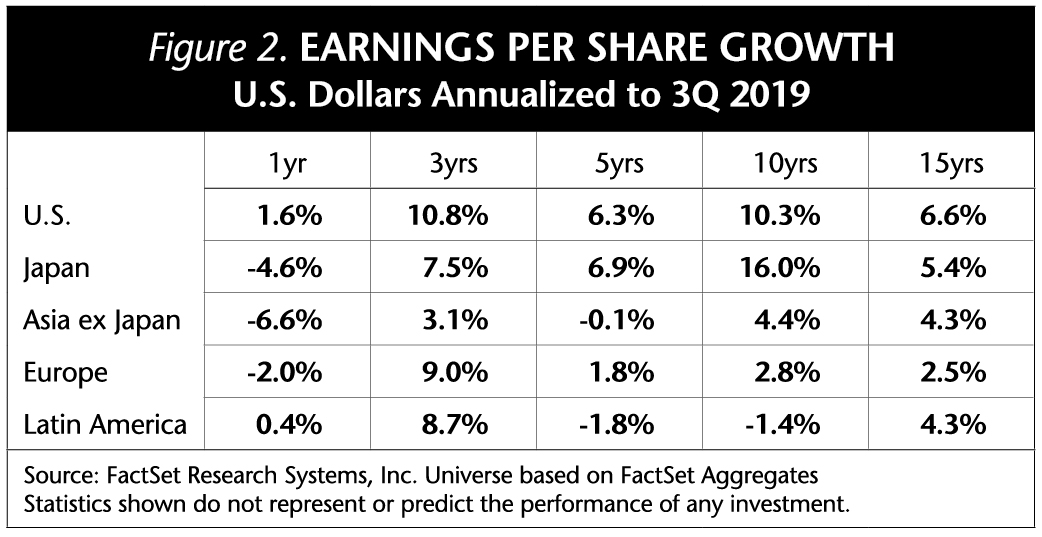

Clearly, slowing growth is being reflected in recent earnings per share (EPS) performance, as are the effects of the willingness of the U.S. to see income inequality rise. (See Figure 2.) We expect that corporate earnings in Asia have the potential to rebound next year as the effects of current stimulus work their way through Asia's economies.

Asia, on the other hand, whilst by no means in crisis, has certainly been understimulated. The symptoms of overheated Asia in the late 1990s were high inflation rates and current account deficits. Conversely, Asia today has high current account surpluses, low inflation and even some fiscal surpluses for the most part. It is as if the region had gone through austerity without a crisis to provoke it! Any global reflation, at this point, any steepening of the yield curve that is a sign of both lower policy interest rates and heightened growth expectations, is likely to give Asian governments an excellent opportunity to reflate. Central bankers and policymakers across Asia ex Japan are well-positioned to do so, especially given their concentration on issues of social stability by raising minimum wages and trying to boost the share of growth that goes into the pockets of workers. Note that this is in stark contrast to recent experience in the West.

Asia Swerves Around Tariffs

The ongoing trade dispute between the U.S. and China creates a lot of noise, but has had less impact on the ground in Asia. The market is, I believe, starting to understand that the magnitude of the dispute is far greater in the headlines than it is in GDP. Asia's ability to swerve around some of the tariffs by using trans-shipment through Vietnam and similar ports, as well as its long-term plan for China to shift manufacturing production into Southeast Asia, makes its businesses far more flexible in facing trade frictions than, say, U.S. farmers. That must weigh into political calculations!

The nimbleness demonstrated by Asia in an environment of slowing economic growth is notable, as some European countries may already be in recession. There is an elevated chance of recession in the U.S. in the next year or two. But the real question is not whether there is a technical recession in the U.S. or not, but whether it is going into a period of slower growth. And indeed, if there is to be a U.S. recession, I would expect it to be one that is mild enough to, under normal circumstances, be offset by traditional stimulus methods.

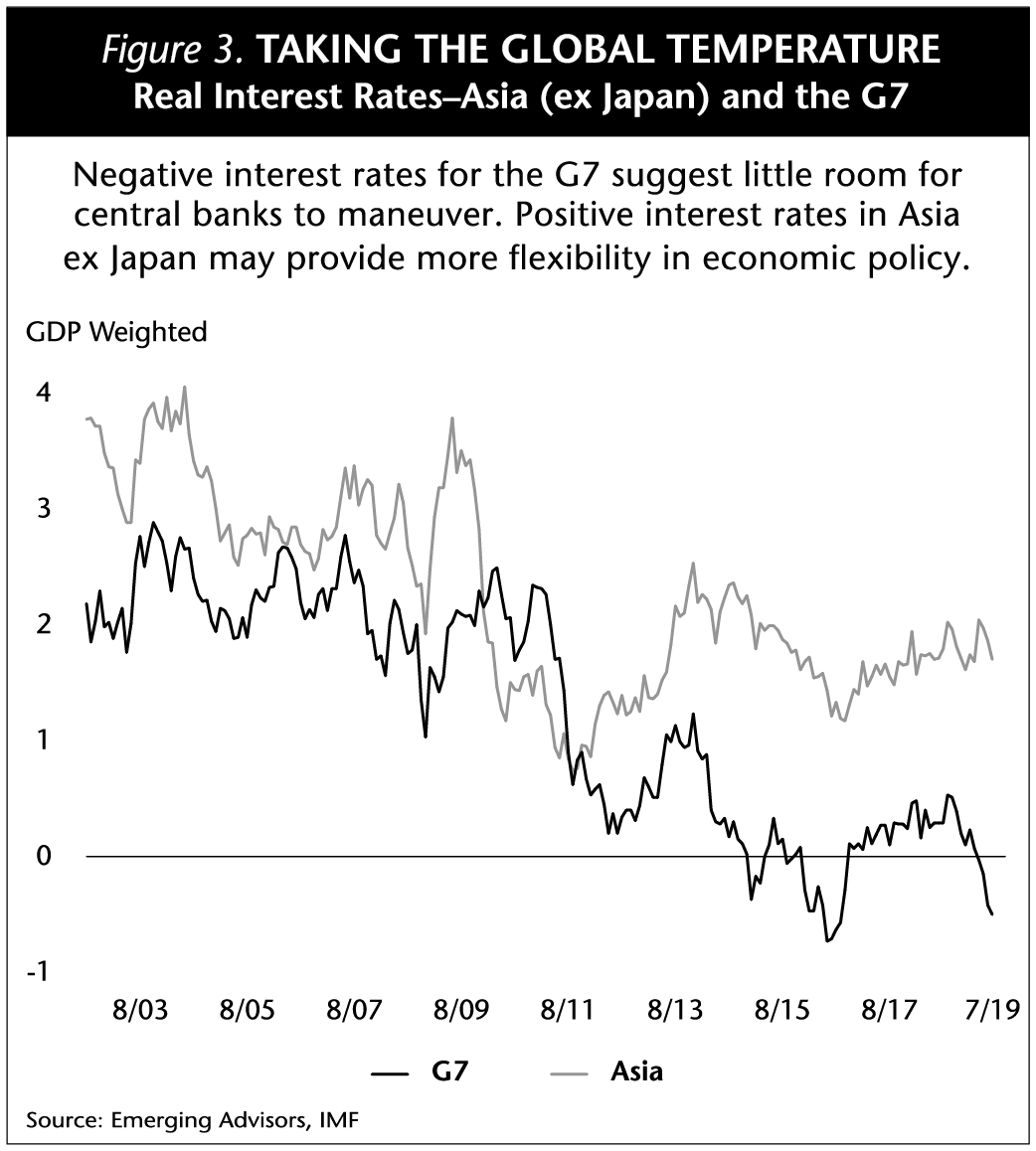

The U.S. has already started. Interest rate cuts, traditional interest rate policy, already being used to offset the weakness in global economies. If the weakness were to continue and the U.S. is forced to turn to fiscal stimulus, it can do so but only in a limited form—automatic stabilizers such as unemployment benefits would probably provide most of the effects of fiscal policy. Europe is far more constricted in policy choices; traditional interest rate policy is not available because interest rates are already extremely low, even negative. (See Figure 3.) Quantitative easing is an option but is politically controversial. Fiscal policy suffers also from the European Union's lack of ability to coordinate across member countries. Europe seems stuck in the mud.

So the question then is: what parts of the world are best-placed to use monetary and fiscal policy to lean against this slower growth?

Room to Reflate in Asia

We believe Asia is far better positioned to support economic growth. We see low inflation across much of the region and high current account surpluses. Both traditional interest rate policy and fiscal stimulus seem available to the region's governments. Because of this, although slow global growth is typically a difficult environment for Asian market returns, both the scale and the duration of any headwinds are likely to be less than historical averages.

China is likely to stimulate further, albeit moderately. Despite what we hear about China's headline inflation and new outbreaks of pig disease, core inflation is actually at 1.5% year over year, which seems much too low. China will not stimulate recklessly, however, due to the fact that it is treading the line between wanting to clean up the credit system (and in doing so, incurring tighter monetary policy) and boosting domestic aggregate demand (but thereby retarding credit reform). It's a balancing act that may continue for some time but there is no need for it to cause real hardship.

India surprised with the scope of its fiscal stimulus. It was an attempt to put more money in the hands of corporate CFOs in the hope that they would invest it and also perhaps kick-start bank lending. You have to hand it to the Indian government—the reform process has been well thought out and a series of clever policies, even the much-feared demonetization, seemed to work much better than the naysayers feared. Yet, it is still an uphill battle for the reformists. I think, on reflection, it is likely that the tax cuts in India are going to have a more dramatic effect than the corporate tax cuts did in the U.S. And India continues to post the fastest economic growth rates of any large Asian economy.

And finally, to Japan, where we have seen monetary stimulus now for much of the past decade. The effect? Rising profit margins, rising returns on equity, faster earnings growth and strong market performance. Market performance that began with the financials and broadened into all sectors and ultimately the smaller capitalization stocks. I continue to see Japan as a roadmap, in terms of policy and market reaction, for where the rest of the region may go, if policymakers can find the economic environment conducive to stimulus. Asia is not emerging from a financial crisis-inspired depression, as it was in the late nineties. Asia is emerging from a period of suboptimal economic growth, however, driven by tight fiscal and monetary policy.

The potential for the monetary and fiscal stimulus to take hold across the world and cause yield curves to steepen once more would be a strong environment for Asian stock markets, for small and mid caps and for the underappreciated secular but not spectacular growth companies outside of the cyclical tech and semiconductor sectors.

Momentum Returns to Asia's Markets

Short-term sentiment toward Asia is yet again in the doldrums. Excitement over a trade deal is giving way to the realization that the U.S. and China do not share the same attitude to global trade and that any deal may be partial and temporary. And global growth has been slowing; slow growth is typically not a favorable backdrop for Asian market performance. And yet, experience indicates that when sentiment is at its weakest, Asian markets make their lows. Maybe the current environment is also one where Asia's markets may be unduly depressed relative to their own history and even to the rest of the world.

So, I believe we are on the cusp of a turning point for the medium term. But my view is that more of the same is likely in the short term. That would mean the U.S. continues to skirt recession, despite ominous signs in the data. But it also means that momentum has come back into Asia's markets. After all, the MSCI China A Onshore Index, representing China's domestic stock markets, is up 27.13% year to date through Nov. 30, 2019, in U.S. dollars terms, while the S&P 500 Index is up 27.63% over the same period. Both markets have shown strong momentum year to date. China's economy, however, with greater income parity for its middle class, may be better positioned for more sustainable growth over the long term. Momentum may provide a clue about the near term, but turning points are more important for those investing with a long-term view.

Robert J. Horrocks, Ph.D.

Chief Investment Officer

Matthews Asia

1 Inception date for the Hang Seng Index was November 24, 1969.

Hang Seng Index: The Hang Seng Index is a free float-adjusted market-capitalization-weighted stock-market index in Hong Kong. It is used to record and monitor daily changes of the largest companies of the Hong Kong stock market and is the main indicator of the overall market performance in Hong Kong.

MSCI China A Onshore Index: The MSCI China A Onshore Index captures large and mid cap representation across China securities listed on the Shanghai and Shenzhen exchanges.

MSCI All Country Asia ex Japan Index: The MSCI All Country Asia ex Japan Index is a free float—adjusted market capitalization—weighted index of the stock of markets of China, Hong Kong, India, Indonesia, Malaysia, Philippines, Singapore, South Korea, Taiwan and Thailand.

S&P 500 Index: The S&P 500 Index is a broad market-weighted index dominated by blue-chip stocks in the U.S.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

© Matthews Asia

© Matthews Asia

Read more commentaries by Matthews Asia