SUMMARY

Recent retrospectives have noted that we closed both a year and a decade on Tuesday. The 2010s turned out to be far more prosperous than almost anyone could have hoped, given that the scars of the global financial crisis were still visible ten years ago. The global economy enters the new decade in a much stronger position than it began the last one.

But progress has been uneven. Some countries and some communities within countries have not advanced much over the past ten years, leaving them frustrated. This has contributed to a swing in politics and policy that threatens the foundations of global economic progress. Our fortunes over the next ten years will be shaped critically by how these forces evolve.

As of this writing, trade uncertainties have diminished modestly. There is hope of détente between China and the United States, and there was no abrupt Brexit at the end of the year. But there remain myriad trade tensions around the world that will continue to hinder exporters and global supply chains. We'll be watching developments in this area closely.

The following themes will also warrant attention in the year ahead:

-

Policy Rotation. Ten years ago, central banks were the only game in town. Today, by contrast, they may have reached the edges of their effectiveness. Very low global interest rates create an opportunity for intelligent fiscal policy to have maximal effect. We'll be watching to see whether countries take advantage of this opportunity.

-

Global Unrest. A number of protests have broken out in different parts of the world amid increasing income and wealth disparity. While markets haven't reacted strongly, the world's many hotspots have the potential to create macroeconomic instability for both emerging markets and advanced economies.

-

Political Volatility. Elections in Germany (in 2021) and the United States will be telling, and political movements in many places are questioning the value of global cooperation. If international bodies like the World Trade Organization and the International Monetary Fund cannot fulfill their missions, risks to markets will rise.

Our forecast calls for continued global growth in 2020, at a rate that is modest. That may seem unexciting, but it might be the best we can hope for.

A century ago, the world enjoyed what came to be known as The Roaring '20s. Economies and markets pressed forward powerfully for most of that decade, but the excesses created in the process ultimately paved the way for The Great Depression. That is certainly an outcome we'd do well to avoid.

Following are our thoughts on how the world's major markets will fare in the year ahead.

United States

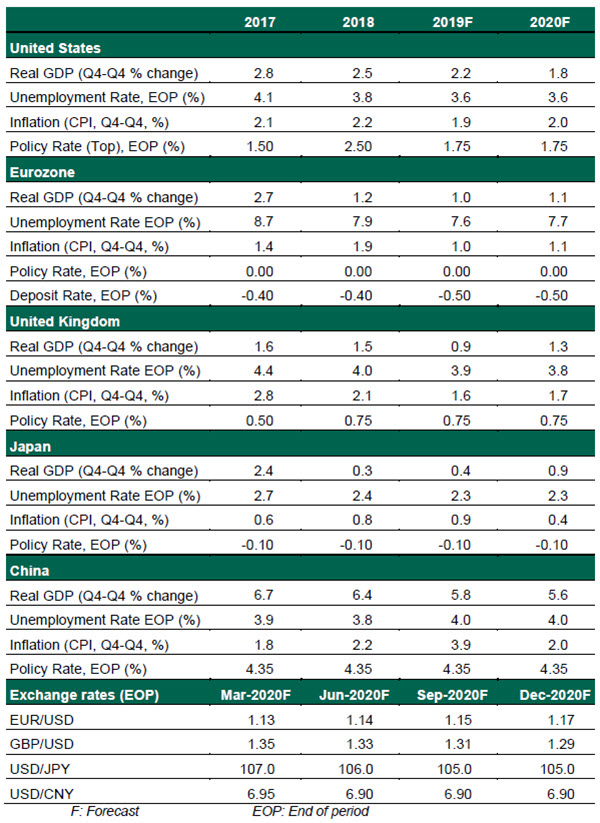

- After a tax-reform-induced rush in 2018, the U.S. economy returned to trend growth last year. Restrictive trade policy produced a slump in business investment that raised recession worries in the middle of 2019, but those concerns proved overstated. The American labor market has continually surprised to the upside: the unemployment rate has held at or below 4% for nearly two years, with job creation still in excess of what we would expect to see this far into a record-setting expansion. Moderate inflation and steady wage growth mean consumers are working, earning and spending. This should be enough to sustain growth at a rate close to its long-run potential.

- In the year ahead, U.S. fiscal and monetary policy will remain accommodative. Low interest rates and deep budget deficits will combine to provide stimulus. The support will be needed, as trade is likely to remain a thorny issue. We are cynical about the substance of the "Phase One" deal with China, and other fronts in the global trade battle remain active. On balance, we expect neither amelioration nor an escalation in trade frictions in the coming twelve months.

- Campaigning for the 2020 U.S. election is already in full swing, and will garner substantial attention in the run up to next November's balloting. But we do not expect the campaign (or the acrimonious politics in Washington) to have much of an impact on performance. Economic and market actors have been resilient as the rhetoric has escalated, and we expect that will continue.

Eurozone

- The slowdown in the eurozone was worrying in 2019, particularly as its core economies, Germany and Italy, hovered perilously close to recession. However, there are early signs that the worst may be over. The recent de-escalation of trade tensions and progress on Brexit will help remove some uncertainties for businesses. Nonetheless, we expect real gross domestic product (GDP) growth to remain sluggish in 2020, barely exceeding last year's results and standing well below potential.

- To address this, eurozone policy makers will need to remain aggressive. As we have written, the European Central Bank has few good options for boosted growth, placing the onus on fiscal policy. We expect a coordinated, sizeable boost from economies that have fiscal capacity (Germany in particular). This should put a floor under the eurozone economy and aid in the effort to get inflation back to its targeted level.

- Though we expect economic activity to improve gradually, a recession triggered by domestic or external factors cannot entirely be ruled out. Public and private debt levels in the eurozone are still high, creating a channel of contagion in a worst-case scenario. From an external standpoint, an escalation of trade tensions with the U.S. would send shockwaves throughout the eurozone.

China

- China's economy is feeling the heat from elevated trade tensions and its own domestic imbalances. Though the U.S. and China have agreed to a limited trade deal, the tentative agreement fails to address the core issues that led to the current dispute. With no further breakthrough expected (nor an escalation), the remaining tariffs will continue to weigh on Chinese exports. We expect China's GDP growth to continue to slide.

- Though China's tolerance of lower headline growth has increased, a major policy easing against the backdrop of faltering growth could deliver some upside surprise to the economy. The Regional Comprehensive Economic Partnership (RCEP), if formally signed, will also bring significant opportunities for Chinese exports, offsetting the impact of U.S. tariffs.

- The risk of a breakdown in trade talks with the U.S. cannot be ruled out entirely. A renewed escalation of trade tensions amid internal rebalancing will take the steam out of China's economy and increase the risk of a hard landing. China is a heavily indebted country; an increase in defaults could undermine consumer and market confidence.

Global Economic Forecast – January 2020

© Northern Trust

© Northern Trust

More Alternative Investments Topics >