U.S. Consumer Outlook, Pension Protests in France, and Australia’s Wildfire

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUMMARY

- U.S. Consumers Carry the Day

- Of Paris And Pensions

- Australia Under Fire

January can be a precarious month for personal finances and personal fitness. The financial and dietary costs of holiday revelry must be paid this month, and doing so is not always easy. As this process unfolds, many resolve to tighten their belts: physically on their waistbands, and metaphorically in their wallets.

This month of quieter consumption is a good time to take stock of the outlook for U.S. consumers. Consumer spending has been the most encouraging trend in recent reports of U.S. economic growth. While trade uncertainty made exports volatile and took business investment into negative territory, consumer spending showed reliably strong growth in the first three quarters of 2019. A $21 trillion economy is quite a burden for consumers to carry, but they appear to be up to the task.

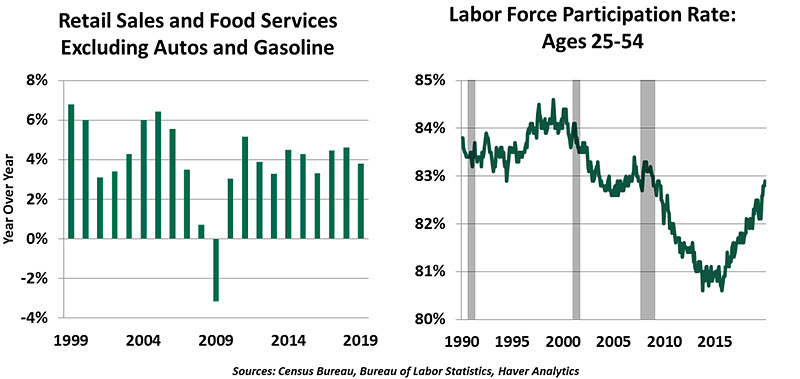

Closing the books on 2019, we see another year of healthy consumer spending. Retail sales grew by a strong 5.8% in December, helped by a late Thanksgiving that pushed the peak holiday shopping weeks later into the year. E-merchants continued to gain at the expense of traditional department stores, but overall results beat expectations for the season.

It should be no surprise that consumers remained active in 2019. When consumers work, they gain income, and they spend it. The unemployment rate is holding at a historically low level of 3.5%, and job openings are plentiful. For the past two years, over 20% of small business owners surveyed by the National Federation of Independent Business identified a lack of quality labor as the most important problem facing their companies.

December’s employment report reflected the continuing strength of the American labor market. While job creation of 145,000 jobs was modestly below expectations, it came on the heels of an upside surprise in November. The best news was the rise in the labor force participation rate for workers age 25-54 years. We watch this metric closely to assess whether the labor market has reached capacity. The current cycle high of 82.9% remains below the peaks seen in past cycles, suggesting some slack remains.

“Very strong job creation has restored incomes and bolstered consumption.”

This growth in the labor force brings many benefits. Employers are able to grow their headcount without shocks to their labor costs. The marginal workers who re-enter the workforce are learning new skills, earning income and paying taxes. They are potentially moving off disability or other welfare programs. And by expanding the labor force, they are growing the potential output of the total economy, clearing the way for continued growth.

Wages continue to grow, albeit more slowly than we would expect from past cycles. The availability of workers on the margin is among the factors keeping wage growth muted; in turn, inflation has yet to gain any momentum. Central bankers are worried that inflation has not reached its target. But from a worker’s perspective, the current level of moderate inflation is generally positive: incomes are growing faster than expenses, and price shocks are rare. Though we were unsure of how the economy would adapt to higher tariffs, trade protections have been structured to avoid most consumer products; the worst-case scenario of tariffs weighing on consumer spending has not played out.

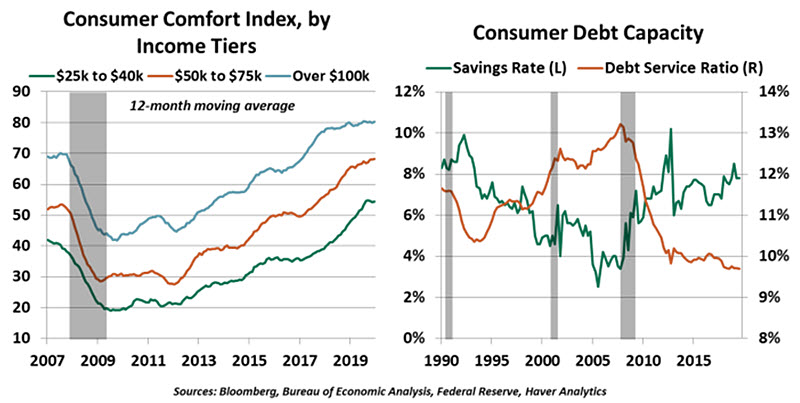

This confluence of favorable conditions is coming through in the data. The Bloomberg Consumer Comfort Index, which assesses financial capacity for purchases, has shown solid improvement across income levels.

Favorable circumstances do not mean that every consumer is in perfect shape. The record-setting stock market does not benefit everyone: The Federal Reserve estimates that only 52% of Americans own equities directly or through a retirement portfolio, so many of the gains of the recent bull market have not accrued to workers. Stock holders are often wealthier Americans with a lower propensity to spend their higher income, or retirement savers who will not spend their short-term gains. “Wealth effects” from strong equity markets have been modest during the past decade.

Consumers are earning more but also saving more. Over the past two years, the national saving rate has climbed from 6.5% to nearly 8%. In the event of a downturn, this high savings rate may provide a cushion to consumers who saved. But consumers have a long way to go toward building nest eggs. The Fed estimates that 48% of Americans lack retirement savings accounts. As these workers grow older, their spending will contract. And in both cases, these averages hide an income disparity: 89% of households in the bottom income quintile have no retirement savings, while 40% of consumers do not have the liquidity to afford an unplanned $400 expense.

“Consumers and lenders have handled debt judiciously in this cycle.”

Good employment and low interest rates have allowed consumer debt to grow sensibly. TransUnion reports 197 million consumers are carrying a total debt load of $13.8 trillion. Throughout the recovery, debt balances have grown in every sector except home equity lending. However, this growth has come in the context of steady economic gains. Household debt service ratios, a measure of debt obligations relative to disposable income, have held steady at or below 10% since 2012, falling from a high of over 13% entering the financial crisis in 2007. We have seen a modest uptick in credit card and auto loan delinquencies, but these come from a low base and are not yet considered threatening.

There are risks to continued gains in U.S. consumption. If turmoil in the Middle East escalates into an armed conflict, energy prices will rise. Consumers may not feel small fluctuations in headline inflation rates, but higher gasoline prices immediately weigh on spending decisions. And while labor markets have been resilient, job openings and weekly hours worked are starting to fall, especially in goods-producing sectors, which can presage layoffs. But the presence of additional savings should provide a buffer against consumer collapse.

Two weeks into the new year, it’s easy to feel optimistic. Year-end bonuses and tax refunds should help balance our checkbooks, and renewed trips to the gym should offset our holiday consumption of food and drink. More broadly, the behavior of U.S. consumers seems better balanced than it has been in the past, which should bode well for economic growth.

Back Against the Wall

Amid a surge in global populism, setting sound policy is getting harder. No one knows this better than French President Emmanuel Macron. Protests across France that began with the yellow vest movement pushing back on increased fuel taxes have evolved into a broader stance against the government’s economic policies. A proposed overhaul of the country’s pension system only added fuel to the fire.

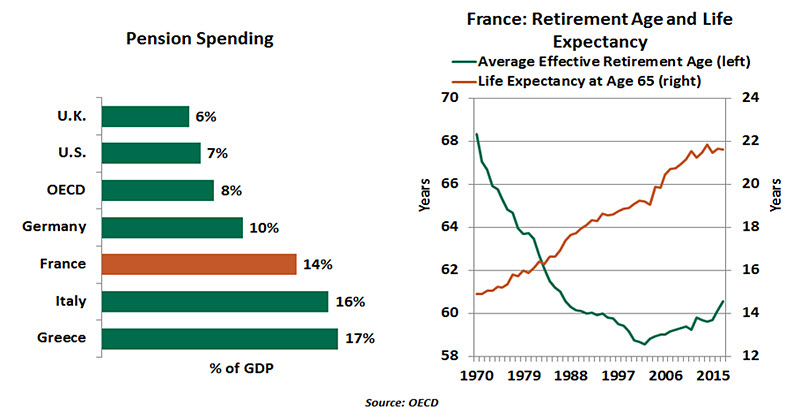

France has a generous pension system when compared to its European and other advanced counterparts. The French government acts as a source of funds and as the overseer and guarantor of the pension system. Through France has raised the official retirement age from 60 to 62 in the past decade, it remains one of the lowest in Europe. Moreover, French workers in professions such as train engineers are able to retire much earlier, in some cases from the age of 55. An average age for retirement in France is 60 compared to an average of 63 for Europe and 64 across all Organization for Economic Co-operation Development (OECD) nations. In the U.K., the retirement age for state pensioners is 65, expected to increase to 67 by 2028.

Under the reform plan, the government intended to raise the full-benefit retirement age to 64 from 62. The plan would consolidate the current system of 42 different pension regimes, each tailored to match different professions in both the public and private sectors, with a universal points-based system under which all workers would have the same rights. Workers would accumulate points and cash them in at retirement in the form of pension benefits.

The outline is intended to bring to an end to the system whereby workers get pension benefits based on the salaries of their best working years. The system of multiple schemes with different rules not only undermines labor mobility but also creates inequities.

In the wake of several weeks of strikes and demonstrations disrupting the economy, the government has walked back some of its proposals, including the proposed age limit. It also offered concessions to individual professions—including the police, dancers at the Paris Opera, nurses, flight attendants and airline pilots—by moving back to their tailored retirement structure. Despite this, the protests have continued to rock the French capital as the unions demand withdrawal of the entire reform plan.

The current benefits come at a steep cost for the state. The mandatory pension system consumes 14% of gross domestic product in France, the third-highest share in Europe (after Greece and Italy) and well above the 8% OECD average. In retirement, the French receive from the state an average of 74% of pre-retirement earnings, compared with an OECD average of 59%. Thanks to higher life expectancies (80 for men, 86 for women), citizens are spending about a quarter of a century in their wingchairs (22.7 years for men, 26.9 for women), up from 13 years in 1970, adding to the burden.

France, like the rest of Europe, is facing challenges on multiple fronts: populations are growing older and pension shortfalls are rising. According to a report commissioned by Prime Minister Édouard Philippe, the country's pension deficit could rise to a high of €17.2 billion by 2025 under the existing system. The French government’s proposed move to a single pension system was a step in the right direction that could improve transparency, foster labor mobility, lower management costs, and most importantly, ensure the financial sustainability of the system.

“Retirement ages have not kept pace with life expectancy, adding to the pension burden.”

Good pension systems should not only bring good benefits but also be sustainable. An unsustainable system threatens economic prosperity and stability by creating an excessive burden for governments and taxpayers. Modest reforms today will allow France’s future retirees to live out their lives in comfort and keep them off of the streets.

Conflagration

Carl offers thoughts on the wildfires raging in Australia.

My first visit to Australia was 25 years ago. I had been invited to teach at a conference in the Blue Mountains, a verdant area west of Sydney. I will never forget the charming towns of Leura and Katoomba, and the scent of eucalyptus that filled the air.

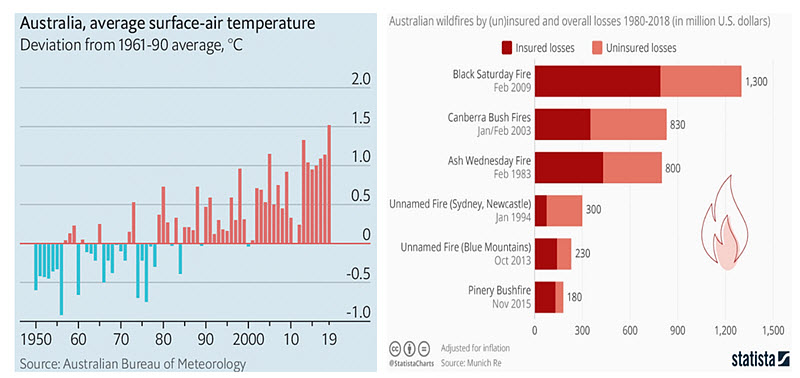

Sadly, a different scent has been filling the air in Katoomba this summer. Bush fires have been bearing down on the Blue Mountains, producing a haze of smoke that has deterred visitors from coming. While Katoomba is at low risk for fire, other communities across Australia have not been so lucky. As of this writing, almost 18 million acres across the country have burned, an area eight times larger than the area covered by California’s devastating fires of two years ago. Weeks of hot summer weather lie ahead.

Climate change has been identified as one of the root causes of the disaster. Average temperatures in Australia have been rising steadily during the past generation, and vast tracts of the country have struggled with drought. Throw in this year’s strong winds, and you have a recipe for disaster.

Direct damage to property from the blazes could exceed AU$1 billion, and could grow to make this year’s fires the most expensive in Australian history. The economic impact is likely to result in an interest rate cut from the Reserve Bank of Australia and a reconstruction program from the Australian government. As we wrote late last year, Australia could use some fiscal stimulus; but we certainly wouldn’t have wished for a disaster to bring it about.

“The costs of climate change are on display in Australia.”

As insurers tally their losses, they will reprice their policies. This will certainly have an impact on the locus of population and the level of economic activity in Australia. In this manner, the long-term costs of climate change are brought forward, which may force the kind of environmental reckoning that some think is long overdue. If there is a silver lining behind the smoke clouds currently obscuring Australia’s visibility, it is that the disaster may allow policy makers to see climate risks more clearly.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2020 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit our terms and conditions page.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All