Every instance of financial speculation today is termed a “bubble”, but true financial bubbles are rarer than most investors believe.

Certainly, bubbles include speculation, but the difference between bubbles and mere speculative periods is that bubbles go beyond the financial markets and pervade society.

As we’ve highlighted in past Insights, there are five defining characteristics beyond speculation that are common to historical financial bubbles:1

1. Increased use of leverage.

2. Increased liquidity.

3. Democratization of the market.

4. Record new issues.

5. Record turnover.

These characteristics seem to be spreading in several markets these days. The technology sector, venture capital, private equity, and distressed debt all show several of these characteristics. Their performance comparisons to other markets are getting extreme and, as in most bubbles, investors’ enthusiasm for the asset classes is growing as those performance disparities get wider. Bubbles tend to significantly hurt the performance of contrarian investors, and this cycle has fit that pattern.

We thought it worthwhile to highlight some of these significant disparities.

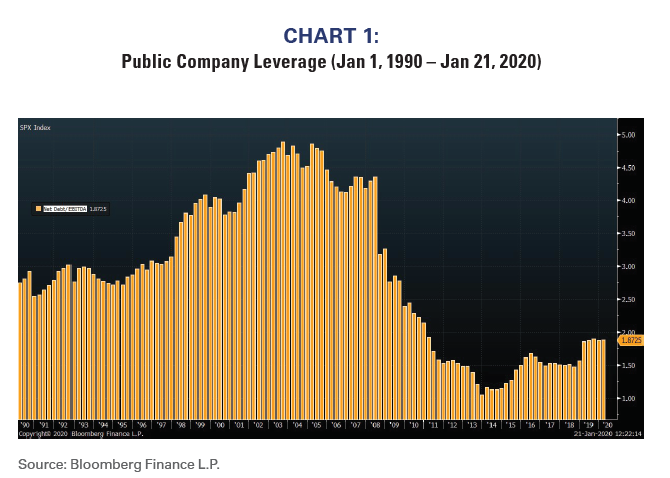

Corporate leverage

Many observers have pointed out that the US corporate sector’s leverage ratios have increased significantly. Chart 1 shows that public company leverage has indeed increased but does not look dire relative to history. Individual sectors have increased leverage (i.e., Consumer Staples, Health Care, and Technology), but public equity leverage ratios in general still look conservative relative to history. One should have expected leverage ratios to increase as interest rates fell because companies simply refinanced and expanded debt levels while keeping interest payments at similar levels.

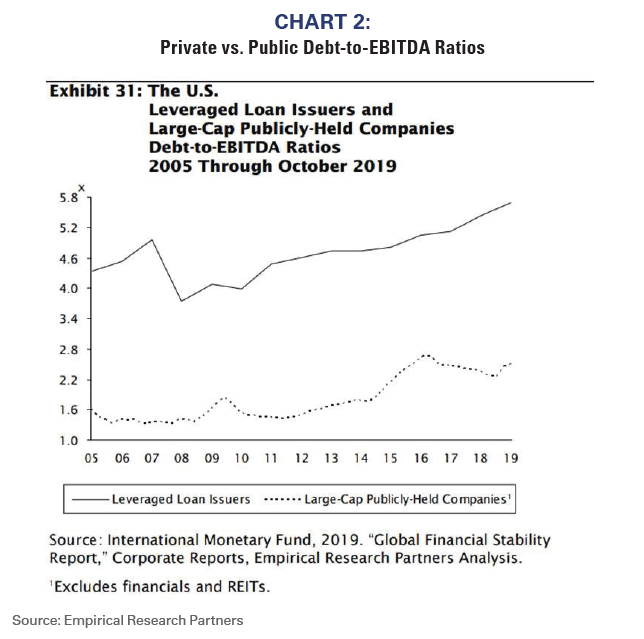

Leverage ratios among public companies have increased, but leverage ratios among private companies has ballooned. According to Empirical Research Partners, Debt-to EBITDA for private companies is more than double that of the S&P 500® (see Chart 2). Investors often point to the higher returns associated with private companies but fail to mention those companies tend to be more cyclical and more highly levered than is the overall public market.

Liquidity

The days of a stern Chair of the Federal Reserve are long gone. The late Paul Volkers’ strict monetary policies have been followed by a series of Fed Chairman who have fostered increasingly expansive monetary policies and haven’t understood or cared that loose monetary policy causes inflation if not in real assets, then in financial assets. Since the early-1990s, real asset inflation has been largely constrained by globalization, so the Fed’s ongoing free-flowing liquidity created a series of financial asset bubbles.

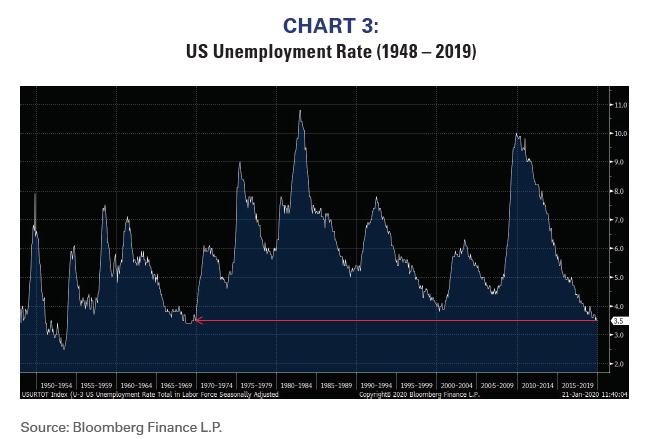

The Fed has a dual mandate of low unemployment and stable prices. The Fed cut interest rates three times during 2019 and began to once again expand its balance sheet despite that the economy was healthy and despite that the unemployment rate was at a 50-year low (See Chart 3). That implies the Fed believed that deflation was a risk and wanted more inflation. Unfortunately, they failed to yet again recognize that loose monetary policy can cause inflation in financial assets.

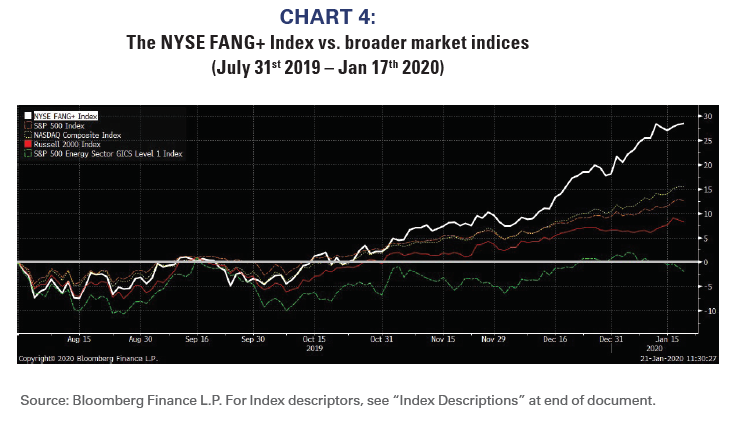

The result of the recent lowering of rates and expansion of the Fed’s balance sheet has been a bubble in the making. Since the Fed cut rates last July, just one segment of the Technology sector has significantly outperformed the overall market (See Chart 4).

Democratization of the market

Bubbles pervade society. Therefore, perhaps the most defining aspect of a bubble is the democratization of the market, i.e., everyone should get to play. The birth of the online day-trader during the tech bubble and people flipping condos and leaving good jobs to become real estate agents during the housing bubble are two examples.

It was especially disconcerting to recently read that major private equity and venture capital firms were heavily lobbying regulators to allow individuals to invest in private markets. First, this seems to totally ignore the history of individuals’ unfortunate experiences with private markets and why today they do not have access. Second, it seems to ignore the vast amounts of “dry powder” or funds that have been raised for private equity and venture investing that have yet to be called (over $2 trillion by some reports).

Individuals are being offered entry at a very late stage. Third, it also ignores that recent flows to private equity and venture have eclipsed the historic flows into public equity mutual funds during the technology bubble. Fourth, and perhaps most important, it reflects the standard refrain during bubbles that everyone should get to play and denying individual investors access to a market hinders their wealth creation.

Record new issues

Although the IPO market may have recently fizzled, the combination of unbridled creation of new private and venture funds and the overall plentiful availability of speculative capital should warrant caution.

Bubbles divert capital away from productive use, and there are many current examples of such ill-advised allocations. Investors’ long-term returns are always higher when capital is scarce, and bubbles create scarcities in non-bubble industries or sectors. Our now famous (infamous?) report from March 2000 “Attention Venture Capitalists: Leave Silicon Valley for West Texas” reflected how the energy sector was starved for capital and that returns on capital were likely to be higher in the energy sector than in the bubble-financed technology sector.

For example, today there are companies with lofty valuations that:

- Will take wealthy individuals on outer-space

- Will dominate the auto industry without distribution, without sufficient cash flow, and with competition

- Are the modern day “conglomerates”. Business school case studies often center on “stick to your knitting” and the failure of the conglomerate model, but today’s conglomerates are assumed to be

- Exist in product markets that are rapidly fragmenting with little competitive advantage to differentiate any

- ◗ Etc., etc., etc…

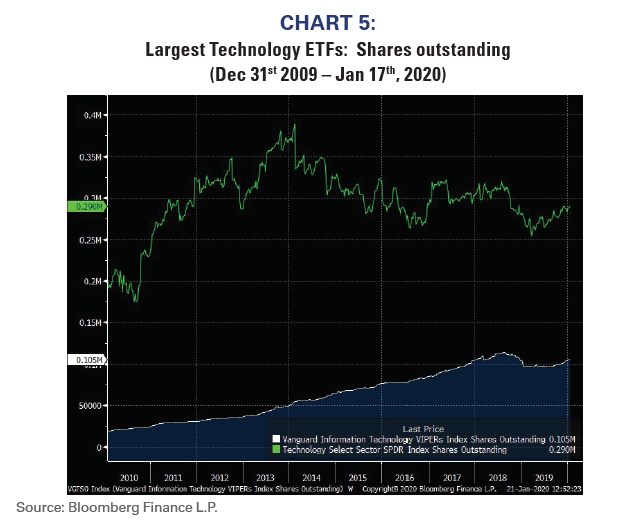

Another way to measure “new issues” is the shares outstanding for ETFs. When the shares outstanding increase it reflects higher demand for the ETF. Chart 5 shows the shares outstanding of the two largest technology sector ETFs. Both ETFs’ shares outstanding increased during 2019.

Record Turnover

Admittedly, it is virtually impossible to measure turnover or trading volume for private investments largely because they do not trade. Illiquidity among private investments is often considered a positive factor because the added risk should be compensated with added returns. Whereas there might have been a significant illiquidity premium in private investments 25 years ago when few investors were interested in private investments, we strongly doubt that premium exists today.

If it quacks like a bubble…

Many, if not all, of the characteristics of a financial bubble seem evident in some technology or “disruptor” shares, private equity, and venture capital. One can never predict when a bubble might deflate. However, it seems relatively clear to us that investors should not be adding positions in such frothy sectors.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices.

Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

Indexes are not available for direct investment.

The past performance of an index is not a guarantee of future results.

NYSE FANG+: The NYSE FANG+ Index is an equal-dollar weighted index designed to represent a segment of the technology and consumer discretionary sectors consisting of highly-traded growth stocks of technology and tech-enabled companies such as Facebook, Apple, Amazon, Netflix, and Alphabet’s Google.

S&P 500®: The S&P 500® Index is an unmanaged, capitalization- weighted index designed to measure the performance of the broad US market. The index includes 500 leading companies covering approximately 80% of available market capitalization.

Russell 2000: Russell 2000 Index. The Russell 2000 Index is an unmanaged, market-capitalization-weighted index designed to measure the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index.

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s.

© Copyright 2020 Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

1 Thanks to Edward Chancellor for outlining these characteristics in his seminal book, “Devil Take the Hindmost: A History of Financial Speculation”.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors